Merchant exporters are instrumental in a boosting of country’s exports especially exports from MSME and small manufacturers.

As per Foreign Trade Policy, Para 9.33 “Merchant Exporter” means a person engaged in trading activity and exporting or intending to export goods.

Para 9.32 of FTP, “Manufacturer Exporter” means a person who exports goods manufactured by him or intends to export such goods.

Merchant Exporters buy goods from the Indian manufacturers and sell them abroad. They may not have their own manufacturing unit or processing facility. Merchant exporters sell and buy on their own account and thus assume the risks involved in exporting. They have generally intimate knowledge of export markets and exportable products. They may have extensive contact network all over the specific regions in the world and have access to focused markets. They usually have a system of gathering market information and keep a close watch on market trends. The nature of their business makes it possible for them to assess the marketability of products and the prospects of their success. They often specialize in certain commodities or in certain areas.

Merchant exporters are usually well financed and they usually extend pre-shipment finance to supporting manufacturers. They may have technical and commercial expertise who can guide on product development, packing, inspection, regulatory and other related aspects of exports. They often have specialized resources and may have their own Shipping, Documentation and Insurance Department and also may maintain their branches at port towns and in important centers abroad. In addition, merchant exporters often co-operate with producers in developing countries to adapt products, for instance, by providing product specification giving designs and styling guidance, offering in quality control, and counseling on packaging, labeling and shipping.

This method of exportation through Merchant Exporters is useful when the company is small and lacks expertize in exporting and it’s related nitty-gritties, therefore, not in a position to start exports on it’s own.

Advantages of Exporting through Merchant Exporters:

Merchant Exporting is more suitable for a small company which does not possess adequate financial and managerial resources required for making a successful entry in to a foreign market. The main advantages are:

- The merchant exporter takes care of all botheration involved and assumes all sales and credit risks

- Export merchants usually finance manufacturers against purchase of their goods. Hence their capital is not tied up.

- The firm does not have to spend money on market research or on setting up branches abroad.

- They are frequently arranges overseas buyers and provide sales opportunities

- The manufacturer is free to concentrate on production and not to bother about export marketing and other export formalities.

- Export entry through merchant exporters is the easiest and least costly.

- Selling through such merchant exporters automatically ensures that the goods will reach the important distributors and through them down the distribution system and therefore enable penetration of product and brand image in the overseas markets.

Merchant Exports – Earlier Practice :

Under the Earlier Central Excise provisions, Merchant Exporter have to get CT-1 form from the Jurisdictional Commissioner / Deputy Commissioner / Asstt. Commissioner as the case may be after executing the General Bond along-with Surety / security and handed over this CT-1 Form to the Manufacturer-Supplier with duly signed ARE-1 Form. Supplier would submit a copy of the CT-1 to their jurisdictional Central Excise Department.

The Merchant Exporter may opt for Sealing of goods and examination at place of dispatch or Examination of goods at the place of export. For self-sealing Circular No. 26/2017 – Customs, dated 01.07.2017; Circular No. 36/2017 – Customs, dated 28.08.2017 may be followed.

Material may directly be shipped to the port by the Manufacturer-Supplier as per the instruction along with the supplier’s excise invoice and duly filled ARE-1. After that Merchant Exporter may raise export invoice and packing list and complete other Export formalities.

Merchant Exporter shall be required to mention name and address of supporting manufacturer of the export product on the export document viz. Shipping Bill / Airway Bill / Bill of Export / ARE-1.

Merchant Exporter would have to file the proof of export and duly acknowledged copy of the same would be provided to the supplier for his future use.

For waiver of CST Merchant Exporter to provide H form to the Manufacturer – Supplier.

Let us now discuss in this paper how merchant exporter exports under GST regime.

Merchant Exporter to Register under GST :

Taxable event in the GST regime is supply of goods. Exports being inter-State supply (Sec 7(5) of IGST Act, 2017), Merchant Exporter would be required to obtain GST registration (Compulsory Registration – Sec 24 of CGST Act 2017).

Merchant Exports under GST

The concept of merchant or manufacturer exporter would become irrelevant under the GST regime. The procedure in respect of the supplies made for export is same for both merchant exporter and a manufacturer exporter.

The earlier CT-1 Bond, and ARE-1 formalities are no more relevant. Merchant exporters were availing exemption from CST against Form-H but there is no such provision on the lines of Form H under the CST Act in the GST. That means there is no exemption from Taxes. Merchant exporters have to pay GST and avail Credit.

Export may be made under bond/LUT. Unutilized credit can be availed as refund. Alternatively, you merchant exporter export the goods on payment of integrated tax (IGST) and claim refund of integrated tax.

The procedures relating to export have been simplified so as to do away with the paper work related documents like CT – 1, ARE – 1, H-Form etc and intervention of the department at various stages of export.

In case of goods the shipping bill is the only document required to be filed with the Customs for making exports. Requirement of filing the ARE 1/ARE 2 has been done away with.

The supplies made for export are to be made under self-sealing and self-certification without any intervention of the departmental officer.

The shipping bill filed with the Customs is treated as an application for refund of IGST and shall be deemed to have been filed after submission of export general manifest and furnishing of a valid return in Form GSTR- 3 by the applicant.

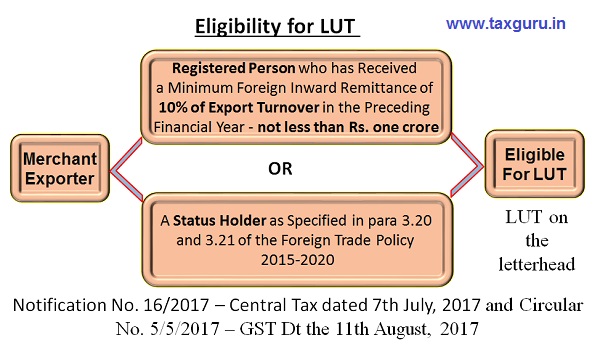

Eligibility for LUT :

Notification No. 16/2017 – Central Tax dated 7th July, 2017 specifies conditions to be fulfilled for export under Letter of Undertaking (LUT) in place of bond. In the extant Central Excise provisions, LUTs were limited to manufacturer exporters only. The intent of the said notification is to liberalize the facility of LUT and extend it to all kind of suppliers (Manufacturer-Exporter or Merchant Exporter)

According to the Notification any registered person who has received a minimum foreign inward remittance of 10% of export turnover in the preceding financial year is eligible for availing the facility of LUT provided that the amount received as foreign inward remittance is not less than Rs. one crore. This means that only such exporters are eligible to LUT facilities who have received a remittance of Rs. one crore or 10% of export turnover, whichever is a higher amount, in the previous financial year.

It may however be noted that a status holder as specified in paragraphs 3.20 and 3.21 of the Foreign Trade Policy 2015-2020 is eligible for LUT facility regardless of whether he satisfies the above conditions.

Bond & Bank Guarantee

Exporters who are not eligible for submission of LUT need to submit bond backed by surety / security. Circular No. 4/4/2017 dated 7th July, 2017 provides that bank guarantee should normally not exceed 15% of the bond amount. However, the Commissioner may waive off the requirement to furnish bank guarantee taking into account the facts and circumstances of each case.

i. an exporter registered with recognized Export Promotion Council can be allowed to submit bond without bank guarantee on submission of a self-attested copy of the proof of registration with a recognized Export Promotion Council

ii. In the GST regime, registration is State-wise which means that the expression ‘registered person’ used in the said notification may mean different registered persons (distinct persons in terms of sub-section (1) of section 25 of the Act) if a person having one Permanent Account Number is registered in more than one State. It may so happen that a registered person may not satisfy the condition regarding foreign inward remittances in respect of one particular registration, because of splitting and accountal of receipts and turnover across different registered person with the same PAN. But the total amount of inward foreign remittances received by all the registered persons, having one Permanent Account Number, maybe Rs. 1 crore or more and it also maybe 10% or more of total export turnover. In such cases, the registered person can be allowed to submit bond without bank guarantee.

Ref: Notification No. 16/2017 – GST dated 7th July, 2017 and Circular No. 2/2/2017 – GST dated 5th July, 2017; Circular No. 4/4/2017 – GST dated 7th July, 2017; and Circular No. 5/5/2017 – GST Dated the 11th August, 2017

Exports : Zero Rated Supply :

As per Sec 2(23) of IGST Act: “zero-rated supply” shall have the meaning assigned to it in section 16;

Sec 16. (1) of IGST Act : “zero rated supply” means any of the following supplies of goods or services or both, namely:––

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

Exports & Refunds :

On account of zero rating of supplies, the supplier will be entitled to claim input tax credit in respect of goods or services or both used for such supplies even though they might be non-taxable or even exempt supplies. Every person making claim of refund on account of zero rated supplies has two options. Either he can export under Bond/LUT and claim refund of accumulated Input Tax Credit or he may export on payment of integrated tax and claim refund of thereof as per the provisions of Section 54 of CGST Act, 2017. Thus, the GST law allows the flexibility to the exporter (which, will include the supplier making supplies to SEZ) to claim refund upfront as integrated tax (by making supplies on payment of tax using ITC) or export without payment of tax by executing a Bond/LUT and claim refund of related ITC of taxes paid on inputs and input services used in making zero rated supplies.

As per Sec 16. (3) of IGST Act : A registered person making zero rated supply shall be eligible to claim refund under either of the following options, namely:––

a) he may supply goods or services or both under bond or Letter of Undertaking, subject to such conditions, safeguards and procedure as may be prescribed, without payment of integrated tax and claim refund of unutilised input tax credit; or

b) he may supply goods or services or both, subject to such conditions, safeguards and procedure as may be prescribed, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied,

in accordance with the provisions of section 54 of the Central Goods and Services Tax Act or the rules made thereunder.

No Refund in Certain Cases

As per Sec 54(3) of CGST Act : Subject to the provisions of sub-section (10), a registered person may claim refund of any unutilised input tax credit at the end of any tax period:

Provided that no refund of unutilised input tax credit shall be allowed in cases other than––

(i) zero rated supplies made without payment of tax;

(ii) where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be notified by the Government on the recommendations of the Council:

Provided further that no refund of unutilised input tax credit shall be allowed in cases where the goods exported out of India are subjected to export duty:

Provided also that no refund of input tax credit shall be allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

Export Directly From Premises of Manufacturer or other Premises:

Merchant Exporter can export the goods either directly from the premises of the manufacturer, with or without sealing of the export consignments, or through other premises.

The merchant exporter has the option of exporting directly from the manufacturer’s premises. In such case as per Sec 10. (1)(b) of IGST Act, 2017, though goods moved directly for export from the manufacturer’s premises on direction of merchant exporter, the place supply shall be the principal business place of merchant exporter. Since supply from Manufacturer to Merchant Exporter is treated as normal supply, GST is applicable. The manufacturer will raise Tax Invoice on the Merchant exporter.

If the merchant exporter & the manufacturer supplier are in the same state, this transaction is intra-state (within the same state) & will be subject to levy of CGST & SGST.

If the merchant exporter & the manufacturer supplier are located in different states, this transaction is inter-state & will be subject to levy of IGST

(Pl. note that there is no exemption like in the previous regime).

Strain on Working Capital :

Prior to the implementation of GST on July 1, Merchant Exporters were exempted from paying Excise Duties by following CT-1 / ARE -1 formalities. Also CST is exempted against H – Form. Now, they have to pay the tax first and then seek a refund, a process that ties up a portion of their working capital and pushes up manufacturing costs as they have to pay taxes on inputs. This has particularly hit small exporters, who work on meagre resources and for whom getting bank financing is tough.

According to industry claims, about Rs 1.85 lakh crore of working capital will get stuck annually due to the implementation GST. Several exporters said they are already facing a capital shortage and have begun to turn away orders.

This will increase transaction costs, which puts pressure on exporters who are already facing difficulties in view of slow- down of global economy, appreciation of rupee in addition to infrastructure and other transactional issues.

Time Bound Refund :

Relief strain on working capital requirement of exporters, following provisions are made for timely release of refunds.

As per Sec 54(6) of CGST Act, 90% of the Total Amount so claimed shall be refunded on a Provisional basis within 7 Days. Further as per Sec 54(7) of CGST Act, the proper officer shall issue the order under sub-section (5) within 60 days from the date of receipt of application complete in all respects. As per Notification No. 13/2017 – Central Tax, 28th June, 2017, Interest @ 6% is payable if full refund is not granted within 60 days.

Refund Process :

GST law also provides for grant of provisional refund of 90% of the total refund claim, in case the claim relates for refund arising on account of zero rated supplies. The provisional refund would be paid within 7 days after giving the acknowledgement. The acknowledgement of refund application is normally issued within a period of 14 days but in case of refund of integrated tax paid on zero rated supplies, the acknowedgement would be issued within a period of three days. The provisional refund would not be granted to such supplier who was, during any period of five years immediately preceding the refund period, was prosecuted.

When the taxpayer claims refund of monies arising out of exports of goods or services, then an authorized officer can issue a provisional refund order in Form RFD-04 of an amount of 90% of the refund claim. Such a provisional refund can be made when the taxpayer:

- Has not been prosecuted for evading taxes for an amount exceeding Rs. 250 lakhs over a period of 5 years.

- Has a GST compliance rating of more than 5 out of 10.

- Has no appeal or review pending with respect to refunds.

Where the authorized officer feels that documents are in consonance with law, then he may pass a final order to that effect.

The Government shall maintain a cash ledger for the taxpayer. It will be constantly updated with the figures as mentioned or declared in the returns. The credit must match with the ledger or else the credit cannot be availed. It is similar in lines of Form 26AS in case of Income Tax, where the amount of TDS and TCS matches with the Form.

In all other cases, the refund application shall be processed within 60 days from the application date. Once the authorised officer adjudges the refund to be true, then he will issue a final order in Form RFD-05 within a period of 60 days from the application date. If the officer fails to pass an order within the said 60 days, then the taxpayer shall receive an interest @ 6% p.a. for the period exceeding the expiry of 60 days until the receipt of refund.

Author Bio

What if Manufacturer and customer both are outside India?

We are merchant exporters handling Detergents. Can you comment if exporters can claim refund of GST paid to various vendors relating to pre-shipment expenses incurred on the shipment, including THC, IHC and CHA charges.

Your View of Merchant Exporter Is very simple .

Issues of following this system is

1) Merchant Exporter don`t get permission for stuffing at Manufacturing site in another state for containerized Cargo.

2) LUT can not be used if the good are not brought back to the state of registration (eg Maha. LUT can not be used for goods Manufactured in Gujarat and Sent to Gujarat port ( closest Port ) .

3) In case where there are Imported Raw Materiel used there is difficulty release of Bond on Duty and no refund on CESS to Manufacture

4) Cost of operation and process of permission to stuff a container at different sites would make it too expensive to operate as Merchant Exporter would deal will many states not just on or two

5 ) In case of EOU unit GST same would be considered as a DTA sale and would not count as a fulfillment of export obligation

Most the defined process don`t actually work on the ground unless the Merchants profit margin is very huge .

To pay 18% or 28% GST on a the shipment and wait for refund where the Merchant profit margins are 3% to 10% Max is just not economical.

Besides the additional man power to manage GST systems is a big burden on the trade . It would cost mush less to Buy the product from Thailand or Vietnam and sell it to another country . It would be even cheaper to carryout the business from Free Trade zones like Dubai where there is no or low income tax.

Dear Mr Panigrahi,

I have gone through your extremely helpful and guiding write up on GST.

Here is our case, we are a Merchant exporter in Maharashtra, in July 17 and October 17’ we procured electrical cables from a supplier in Gujarat for exports. We were already holding a LUT and produced the same to the suppliers at the time of invoicing. Based on their CAs advise the supplier raised an invoice with 28 % and 18 % gst respectively..subsequently we had to pay the principle and gst to the supplier as they started to incur penalty..

We have filed our gst returns in August and October duly claiming the refund of gst..

My questions,

1) Are we on the right track on our claim for refund or is there a different process may be the supplier modify his invoice and refunds us the gst position by claiming it from the department etc.

2) for the future exports I think we are eligible to procure goods by paying only a 0.1% gst against LUT. How do we explain this to the suppliers.

Many thanks in advance for your time and guidance..

ek exporter jo up ka hai or me bhi up ka hon mujhse handicrafts purchase kerna chahta hai dusri country me export ke liye or us items per gst rate 18% hai, but woh 1% tax de raha hai, or notification no 41/2017 ko padhne ke liye boll raha hai kya yeh sahi hai,

Whether 100% EOU manufacturer use imported raw material for Merchant Export transaction by debiting B-17 Bond for customs duty liability. Can he reverse out Liability on receipt of proof of shipment from the Merchant Export

WHAT IS ADVISABLE FOR MERCHANT EXPORTER – ON PAYMENT OF IGST OPTION OR UNDER BOND OR LUT AND ITC REFUND ? WHY ? PLEASE ANSWER