Case Law Details

In re HIC-ABF special foods (P) Ltd. (GST AAAR Kerala)

Ready-to-Eat Food Products Classified Under HSN 21069099 Because Final Product Nature Prevails Over Ingredients; Tuna Tomato Rice and Prawn-Based Products Held Classifiable Under HSN 21069099 Because They Are Prepared Food Items; Vegetable Curries Not Covered by Chapter 20 Because They Are Ready-to-Eat Food Preparations; Boiled Chinese Potato Reclassified Because Original HSN Code Did Not Exist; Kerala AAAR Upholds Residual Food Preparation Classification for 26 Food Products.

The Kerala Appellate Authority for Advance Ruling (AAAR) considered an appeal filed by a food products manufacturer regarding the classification of 27 food items under the GST tariff. The appellant challenged the Advance Ruling Authority’s (AAR) decision that classified most of its products under HSN 21069099 as “food preparations not elsewhere specified or included.”

The appellant argued that various products such as vegetable curries, coconut-based preparations, meat and fish products, and other food items should be classified under more specific tariff headings in Chapters 16 and 20 rather than under the residual Heading 2106. It relied on principles of tariff interpretation that specific entries should prevail over general entries and that ambiguities should be resolved in favor of the assessee.

The AAAR examined the classification dispute item by item. It agreed that specific tariff descriptions generally prevail over residual entries but observed that such principles apply only when ambiguity remains after applying the Rules for Interpretation of the Tariff.

For Items 1 to 6, namely Puli Inji, Sambar Curry, Avial Curry, Kadala Curry, Kappa Puzhukku, and Fish Kappa Biriyani, the appellant sought classification under Chapter 20 as vegetable preparations. The Authority held that these products are ready-to-eat packaged food preparations rather than merely prepared or preserved vegetables. Since Chapter 21 specifically covers edible food preparations for human consumption, the products were correctly classifiable under HSN 21069099.

Regarding Item 7, Thenga Varutharachathu (Varutharappu), the appellant proposed classification under Chapter 20 as a nut-based preparation. The AAAR held that the product is a packaged ready-to-eat food item and therefore falls under HSN 21069099 rather than Chapter 20.

For Items 8 to 21, including Mutton Curry, Mutton Roast, Beef Fry, Beef Roast, Beef Curry, Kerala Chicken Curry, Chettinadu Chicken Curry, Chicken Stew, Chicken Biriyani, Fish with Shredded Coconut and Malabar Tamarind, Fish with Shredded Coconut and Mango, Fish Biriyani, Tuna Tomato Rice, and Prawn Chutney Powder, the appellant argued that they should be classified under Chapter 16 because they contained more than 20% meat, fish, or prawn content. The AAAR rejected this contention, observing that the products are ready-to-eat packaged food items and not merely prepared or preserved meat or fish products. It held that the nature of the final product must be considered as a whole and not solely the percentage of animal content. Accordingly, these items were correctly classified under HSN 21069099.

The Authority specifically noted that Tuna Tomato Rice, though not a curry, remained a ready-to-eat packaged food product and therefore also merited classification under HSN 21069099.

With respect to Items 22 to 26, namely Soya Coconut Fry, Masala Rice, Coconut Rice, Vegetable Pulao, and Tomato Rice, there was no dispute regarding classification, and the AAAR noted that the advance ruling application concerned classification only and not GST rates.

For Item 27, Boiled Chinese Potato (Koorka), the AAAR found merit in the appellant’s contention that the AAR had classified the product under a non-existent tariff entry, HSN 20041010. The Authority held that while the AAR’s reasoning was broadly correct, the correct classification was HSN 20052000, covering potatoes prepared or preserved otherwise than by vinegar or acetic acid. The product did not qualify under HSN 0710 because it was not frozen, nor under HSN 0711 because that heading concerns provisionally preserved vegetables unsuitable for immediate consumption. Accordingly, Item 27 was reclassified under HSN 20052000.

The AAAR therefore upheld the AAR’s classification of Items 1 to 26 under HSN 21069099 and modified the classification of Item 27 by classifying Boiled Chinese Potato (Koorka) under HSN 20052000. The Authority also corrected the appellant’s GSTIN, which had been incorrectly recorded in the original ruling.

Read AAR Ruling in this case: Classification of Food Products under GST: HIC-ABF Ruling

FULL TEXT OF ORDER OF APPELLATE AUTHORITY OF ADVANCE RULING, KERALA

M/S HIC-ABF special foods (P) Ltd., 11/630-B Aroor Industrial development area, Project colony road, Aroor, 688534. (Hereinafter referred to as the appellant) is in the business of food products and are registered under CGST Act 2017 with GSTIN: 32AAACH9887R1ZO. The appeal stand field section 100(1) of the CGST Act, 2017 by the applicant

2. In this ruling, a reference to the provisions of the CGST Act, Rules and Notifications issued thereunder shall include a reference to the corresponding provisions of the KSGST Act, Rules and the Notifications issued thereunder.

3. BRIEF FACTS OF THE CASE:

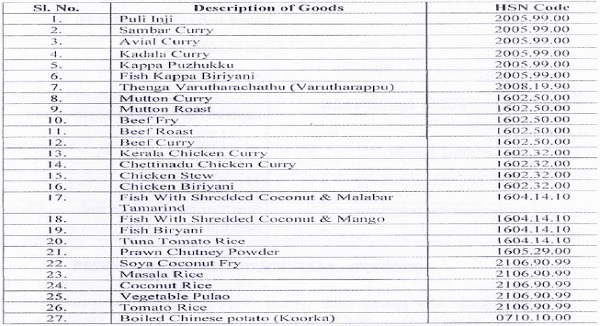

3.1.The brief facts of the appeal are as follows. The appellant is a manufacturer of various food products. The appellant had filed an Advance Ruling Application vide Reference No.AD3204230040140 seeking the appropriate classification of various food items manufactured by them. In the original application before the AAR, the appellant had provided a list of items manufactured by them along with the classification as interpreted by them and requested the appropriate classification of the items. The list of items and classification as interpreted by them is as follows.

3.2. In the Ruling, it was held that the classification of items at Si No 22 to 26 were as interpreted by tent. Further, it was also held that the classification of item at S1 No 27 merits classification under HSN 20041010 and all other items in the list merit classification under HSN 21069099.

3.3. Aggrieved by the said order, the appellant has now approached the appellate authority with the following submissions.

4. GROUNDS OF APPEAL:

4.1.The appellant submits that items 1 to 18 and 20 to 21 of the Advance Ruling Order have been incorrectly classified under the residuary entry 21069099 of Chapter 21, despite the availability of more specific classifications based on the nature and composition of the products, which include preparations of vegetables, meat, seafood, and nuts. As per Rule 3(a) of the General Rules for Interpretation of the Customs Tariff Act, 1975, specific descriptions must prevail over general ones in tariff classification. The appellant contented that The Authority for Advance Ruling (AAR) failed to consider this principle and the specific product characteristics while assigning the classification. The appellant relies on the Supreme Court’s ruling in Dunlop India Ltd. & Madras Rubber Factory Ltd. v. Union of India (AIR 1977 SC 597), which held that consigning a clearly classifiable product to a residuary category undermines the foundational principles of classification.

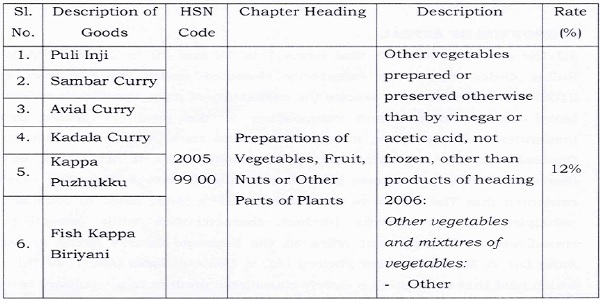

4.2 The appellant further submits that in items 1 to 6 of the Advance Ruling Order—Pali Inji, Sambar Curry, Avial Curry, Kadala Curry, Kappa Puzhukku, and Fish Kappa Biriyani—are all cooked vegetable preparations preserved using retort processing, a method that ensures food safety through vacuum sealing. These products fall squarely within the scope of Heading 2005 of Chapter 20, which specifically covers “Other vegetables prepared or preserved otherwise than by vinegar or acetic acid, not frozen,” rather than the general residuary heading 2106. The Authority for Advance Ruling’s view that these are not “vegetables or mixtures of vegetables” but “food preparations made using vegetables” ignores that Chapter 20 expressly includes such “preparations.” The appellant cites the Tribunal ruling in Manilal Commodities Pvt. Ltd. v. Collector of Customs [1992 (59) ELT 189] to support classification based on predominant content. Thus, under the General Rules of interpretation and supported case law, these items should be classified under Heading 2005 at 12% GST, not under the broader 2106 90 99. Accordingly, the appellant submits that items at Si. Nos. 1 to 6 are classifiable under the below specific description under Chapter 20 rather than the residual entry of 2106 90 99:

4.3 The appellant submits that in items 7 of the Advance Ruling Order, Thenga Varutharachathu (Varutharappu), is a cooked preparation made primarily from coconut, which is a type of nut, and preserved using retort processing. The correct classification for this item falls under Heading 2008 of Chapter 20, which specifically covers “Fruit, nuts and other edible parts of plants, otherwise prepared or preserved, whether or not containing added sugar or other sweetening matter or spirit, not elsewhere specified or included.” This specific heading is more appropriate than the residuary entry 2106 90 99, which the AAR had arbitrarily applied. Accordingly, the appellant submits that Item 7 is classifiable under HSN Code 2008 19 90 at 12% GST, as it meets the criteria of a preserved nut-based preparation more accurately than the general

| Si. No |

Description of Goods |

HSN Code |

Chapter Heading | Description | Rate (%) |

| 7. | Thenga Varutha-rachathu (Varutharappu) | 2008

19 90 |

Preparations of Vegetables, Fruit, Nuts or Other Parts of Plants | Fruit, nuts and other edible parts of plants, otherwise prepared or preserved, whether or not containing added sugar or other sweetening matter or spirit, not elsewhere specified or included:Other, including mixtures:– Other |

12% |

4.4 The appellant submits that in items 8 to 18 and 20 to 21 of the Advance Ruling Order, which include various meat, poultry, fish, and prawn-based preparations such as Mutton Curry, Chicken Biriyani, and Tuna Tomato Rice, are misclassified under the residuary entry 2106 90 99 of Chapter 21 by the AAR. These items contain more than 20% by weight of meat, poultry, fish, or crustaceans, and as per Explanatory Note 2 to Chapter 16 and Note 1(e) to Chapter 21 of the Customs Tariff, • they must be classified under Chapter 16, which deals specifically with such high-content animal-origin food preparations. Each of these items, as supported by their respective ingredient compositions (e.g., Beef Fry with 62.91% beef, Fish with Coconut and Mango with 44.74% tuna, etc.), exceeds the 20% threshold and therefore fits more specifically under Chapter 16 rather than under the general or residual category of Chapter 21. The weight percentage specification in this regard is as follows.

| Sl. No. |

Description of Goods |

Ingredients |

||

| Description | Quantity | % Weight | ||

| 8. | Mutton curry | Mutton Curry Cut | 4 Kgs | 42.08% |

| 9. | Mutton Roast | Mutton Curry Cut | 4 Kgs | 44.42% |

| 4. | Beef Fry | Beef Curry Cut | 54 Kgs | 62.91% |

| 5. | Beef Roast | Beef Curry Cut | 4 Kgs | 44.42% |

| 6. | Beef Curry | Beef Curry Cut | 4 Kgs | 42.08% |

| 7. | Kerala Chicken Curry | Frozen Chicken Boneless Breast and Chicken Bone | 49.5 Kgs | 40.45% |

| 8. | Chettinadu Chicken Curry |

Frozen Chicken – Boneless Breast and Chicken Bone | 23.4 Kgs | 36.49% |

| 9. | Chicken Stew | Frozen Chicken Boneless Breast and Chicken Bone | 3.5 Kgs | 28.00% |

| 10. | Chicken Biriyani | Frozen Chicken – Boneless Breast |

1.4 Kgs | 21.82% |

| 11. | Fish With Shredded Coconut 86 Malabar Tamarind | Tuna Meat Skipjack | 38.76 Kgs | 47.55% |

| 12. | Fish With

Shredded Coconut 86 Mango |

Tuna Meat Skipjack | 38.76 Kgs | 44.74% |

| 20. | Tuna Tomato Rice | Skipjack Tuna Meat | 21.37 Kgs | 24.84% |

| 21. | Prawn Chutney Powder | Dried Prawn | 6 Kgs | 28.44% |

Since Chapter 16 provides a clearer, more specific classification within the same tariff section (Section IV), the items should be correctly reclassified under Chapter 16 headings.

4.5 The Appellant submits that, in line with the principle laid down by the Hon’ble Supreme Court in Commissioner of Central Excise, Bhopal v. Minwool Rock Fibres Ltd. [2012 (278) E.L.T. 581 (S.C.)], wherein it was held that in a classification dispute the entry most beneficial to the assessee must be adopted, and further supported by STP Limited u. Collector of Central Excise [1998 (97) E.L.T. 16 (S.C.)], where the Court ruled that any ambiguity in the interpretation of taxing provisions must be resolved in favour of the assessee, the impugned items at Si. Nos. 8 to 21, which comprise various cooked meat, poultry, fish, and prawn-based preparations, are more appropriately classifiable under specific headings of Chapter 16 of the Customs Tariff (such as 1602 for meat preparations, 1604 for tuna fish products, and 1605 for crustacean preparations), rather than under the residual category 2106 90 99 of Chapter 21, thereby warranting a reclassification of the items under Chapter 16 at a concessional rate of 12%, as detailed in the tariff description and supported by the ingredient-wise content presented earlier. The classifications identified by the appellant are as follows.

| Sl.No. | Description of Goods | HSN Code |

Description | Rate (%) |

| 8. | Mutton Curry | 1602

50 00 |

Other prepared or preserved meat, meat offal, blood or insects:

– Of bovine animals |

12% |

| 9. | Mutton Roast | |||

| 22. | Beef Fry | |||

| 23. | Beef Roast | |||

| 24. | Beef Curry | |||

| 25. | Kerala Chicken Curry |

1602

32 00 |

Other prepared or preserved meat, meat offal, blood or insects:

Of poultry of heading 0105: – Of fowls of the species |

12% |

| 26. | Chettinadu Chicken Curry | |||

| 27. | Chicken Stew | |||

| 28. | Chicken Biriyani | |||

| 29. | Fish with Shredded Coconut and Malabar Tamarind | 1604

14 10 |

Prepared or preserved fish;

caviar and caviar substitutes prepared from fish eggs : |

12% |

| 18. | Fish with Shredded Coconut and Mango | Tunas, skipjack tuna and bonito (Sarda spp.):

– Tunas |

||

| 20. | Tuna Tomato Rice | |||

| 21. | Prawn Chutney Powder | 1605

29 00 |

Crustaceans, molluscs and other aquatic invertebrates, prepared or preserved: Shrimps and prawns:

– Other |

12% |

4.6 The Appellant submits that the Advance Ruling Order is inadequate in respect of Items 20 and 22, as the learned AAR failed to issue a reasoned or speaking order justifying the classification of Item 20 (Tuna Tomato Rice) under HSN 2106 90 99, particularly in light of the significant tuna content warranting classification under Chapter 16. Further, while Item 22 (Soya Coconut Fry) was also classified under HSN 2106 90 99, which aligns with the Appellant’s submission, the AAR failed to confirm the applicable tax rate under Entry No. 45 of Schedule II of Notification No. 01/2017 — Central Tax (Rate) dated 28 June 2017, which prescribes a GST rate of 12% for “Texturised vegetable proteins (soya bari),” thus leaving ambiguity on the correct rate of tax for this item. The learned AAR has classified Item 22, Soya Coconut Fry, under the HSN 2106 90 99 as was also adopted by the Appellant, however, the learned AAR has failed to clarify whether the rate of 12% as provided by Entry at Sl. No. 45 of Schedule II of Notification No. 01/2017 — Central Tax (Rate) dated 28 June 2017 may be availed in respect of the Item.

4.7 The Appellant submits that the learned AAR erred in classifying Item 27 (Boiled Chinese Potato/Koorka) under the non-existent HSN 2004 10 10, and further failed to appropriately consider that the product, being cooked by boiling and preserved through retort technology, is a ready-to-cook food not meant for immediate consumption. The AAR’s observation that the item merits equal classification under HSN 0710, 0711, and 2004 straightens the case for applying the classification most beneficial to the assessee. In line with the Hon’ble Supreme Court rulings in Minwool Rock Fibres Ltd. [2012 (278) E.L.T. 581 (S.C.)] and STP Limited [1998 (97) E.L.T. 16 (S.C.)], which emphasize that ambiguity in tax classification should be resolved in favour of the assessee, the Appellant respectfully submits that Item 27 be classified under HSN 0710 10 00 (Vegetables uncooked or cooked by steaming or boiling in water – Potatoes, frozen), which is a valid and beneficial entry attracting GST at the rate of 5%.

| Si. No. | Description of Goods |

HSN Code |

Chapter Heading |

Description | Rate (%) |

| 27. | Boiled Chinese Potato (Koorka) | 0710

10 00 |

Edible vegetables and certain roots and tubers | Vegetables (uncooked or cooked by steaming or boiling in water), frozen : – – Potatoes | 5% |

4.8 The Appellant submits that the Advance Ruling Order contains a factual inaccuracy in Paragraph 1, wherein the GSTIN of the Appellant has been erroneously recorded as 32AATFD1308H1ZO. The correct GSTIN of the Appellant is 32AAACH9887R1ZO, and the same may kindly be corrected in the interest of proper adjudication and accurate record. In view of the facts and grounds submitted above, the appellant prays to set aside or suitably modify the impugned Advance Ruling Order, dated 13/09/2024, passed by the Authority for Advance Ruling, to the extent challenged herein and to Pass such further or other order(s) as this Hon’ble Authority may deem just and proper in the facts and circumstances of the case.

5. PERSONAL HEARING:

A personal hearing was granted to the appellant on 21/05/2025 in which the authorized representative of the appellant Shri.Vishnu Kadengal, Chartered Accountant appeared and reiterated the submissions made in the written application.

6. DISCUSSION & FINDINGS:

6.1.We have examined the original application, the original ruling, and the appeal filed by the appellant. Before addressing the dispute on item-wise classification, it is necessary to consider certain contentions raised by the appellant. The appellant has cited the Customs Tariff and a decision of the Hon’ble Supreme Court to assert that, in tariff classification, a specific description should prevail over a general one. This is a valid contention and a well-established principle in determining product classification. The appellant has further relied on various Supreme Court judgments to argue that, in classification disputes, the entry most beneficial to the assessee should be adopted, and that any ambiguity in interpreting taxing provisions should be resolved in favour of the assessee. While these principles are recognised, they apply only as a last resort when ambiguity persists, and not where classification can otherwise be determined through the Rules for the Interpretation of the Tariff.

6.2 The sole issue involved is the classification of the 27 items enlisted in the application. The classification proposed by the appellant and the classification decided by the authority are as follows.

| Sl. No. |

Description | Classification proposed by appellant | Classificati on decided by the Authority | Remarks |

| 1 | Puli Inji | 20059900 | 21069099 | |

| 2 | Sambar Curry | 20059900 | 21069099 | |

| 3 | Avial Curry | 20059900 | 21069099 | |

| 4 | Kadala Curry | 20059900 | 21069099 | |

| 5 | Kappa Pu zhukku | 20059900 | 21069099 | |

| 6 | Fish Kappa Biriyani | 20059900 | 21069099 | |

| 7 | Thenga Varutharachathu (Varutharappu) | 20081900 | 21069099 | |

| 8 | Mutton curry | 16025000 | 21069099 | |

| 9 | Mutton Roast | 16025000 | 21069099 | |

| 10 | Beef Fry | 16025000 | 21069099 | |

| 11 | Beef Roast | 16025000 | 21069099 | |

| 12 | Beef Curry | 16025000 | 21069099 | |

| 13 | Kerala Chicken Curry | 16023200 | 21069099 | |

| 14 | Chettinadu Chicken Curry | 16023200 | 21069099 | |

| 15 | Chicken Stew | 16023200 | 21069099 | |

| 16 | Chicken Biriyani | 16023200 | 21069099 | |

| 17 | Fish With Shredded Coconut & Malabar Tamarind | 16041410 | 21069099 | |

| 18 | Fish With Shredded Coconut 86 Mango | 16041410 | 21069099 | |

| 19 | Fish Biriyani | 16041410 | 21069099 | |

| 20 | Tuna Tomato Rice | 16041410 | 21069099 | |

| 21 | Prawn Chutney Powder | 16052900 | 21069099 | |

| 22 | Soya Coconut Fry | 21069099 | 21069099 | No dispute |

| 23 | Masala Rice | 21069099 | 21069099 | No dispute |

| 24 | Coconut Rice | 21069099 | 21069099 | No dispute |

| 25 | Vegetable Pulao | 21069099 | 21069099 | No dispute |

| 26 | Tomato Rice | 21069099 | 21069099 | No dispute |

| 27 | Boiled Chinese Potato (Koorka) | 07101000 | 20041010 |

6.3 The appellant has alleged that the item at Sl. No. 27 has been classified by the authority under a non-existent heading, viz. 20041010, and this allegation appears to be correct. We have also verified that such an entry does not exist. Accordingly, we propose to address this item first. The item in question is Chinese Potato, commonly called Koorka in Kerala. The appellant states that the product is boiled, preserved using retort technology, and marketed as a ready-to-cook item, not intended for immediate consumption. The Advance Ruling Authority (AAR) appears to have taken note of these facts. In its reasoning, the AAR observed that while heading 07101000 broadly covers the product, it could also be classified under heading 0711 (“Vegetables provisionally preserved, but unsuitable in that state for immediate consumption”) or under heading 2004 10 00 (“Other vegetables prepared or preserved otherwise than by vinegar or acetic acid-Potatoes, frozen”). Applying Rule 3(c) of the Rules for the Interpretation of the Tariff-where goods cannot be classified under Rules 3(a) or 3(b), they are classified under the heading that occurs last in numerical order among those which equally merit classification-the AAR concluded that the correct classification was 2004 10 10. While we find the logic behind this approach correct, we note that the AAR erred in classifying the item under CTH 20041010 instead of CTH 20052000. The latter covers “Potatoes” falling under the general heading 2005- “Other vegetables prepared or preserved otherwise than by vinegar or acetic acid, not frozen, other than products of heading 20.06.” Further, classification 0710 applies to “Vegetables (uncooked or cooked by steaming or boiling in water), frozen,” which is inapplicable here, as the product is not frozen and has been preserved using retort technology. Classification 0711 applies to “Vegetables provisionally preserved but unsuitable in that state for immediate consumption,” but it does not specifically include potatoes. Therefore, the most appropriate classification for this product is 20052000, which specifically covers “Other vegetables prepared or preserved otherwise than by vinegar or acetic acid, not frozen, other than products of heading 20.06-Potatoes.” This classification is precise to the product, leaving little room for dispute.

6.4 With respect to items at Sl. Nos. 1 to 6, the appellant has proposed classification under CTH 20059900, whereas the AAR ruled that the applicable classification is 21069099. The classification proposed by the appellant, 20059900, covers “–other” under the subheading “-Other vegetables and mixtures of vegetables” within the heading “Other vegetables prepared or preserved otherwise than by vinegar or acetic acid, not frozen, other than products of heading 20.06.” Chapter 20 as a whole relates to “Preparations of Vegetables, Fruits, Nuts, or other parts of Plants.” However, the products in question are “ready-to-eat packaged food” rather than mere “prepared or preserved vegetables.” Chapter 21 covers “Edible preparations” and appears more appropriate for items commonly referred to as “curry,” which are directly edible (possibly after heating). A “curry” is an edible food .reparation, distinct from “prepared” or “preserved” vegetables.

6.4.1 The Supplementary Notes to Chapter 21 specifically state that heading 2106 includes “preparations for use, either directly or after processing (such as cooking, dissolving, or boiling in water, milk, or other liquids), for human consumption.” Although these products are not specifically listed under any entry in Chapter 21, they clearly fall within the scope of heading 2106, which covers “Food preparations not elsewhere specified or included.”

6.4.2 Applying Rule 3(a) of the Rules for the Interpretation of the Tariff, HSN 2106 provides a more specific description of these items than HSN 2005. Therefore, in light of the specific inclusion under Chapter 2106, we agree with the Advance Ruling Authority that these products are classifiable under heading 2106 rather than 2005. More precisely, they fall under HSN 21069099, covering “ready-to-eat packaged food and milk containing edible nuts with sugar or other ingredients,” as held by the Authority.

6.5 With regard to Thenga Varutharachathu (Varutharappu), the appellant proposes classification under CTH 20081990, which covers “—Other” under subheading 200819 (“–Other, including mixtures”) within heading 2008 (“Fruit, nuts, and other edible parts of plants, otherwise prepared or preserved, whether or not containing added sugar or other sweetening matter or spirit, not elsewhere specified or included”). This falls under Chapter 20, whose scope has already been explained earlier. Since the item is a packaged ready to eat item, for the same reasons set out in respect of items at Sl. Nos. 1 to 6, we are of the view that this product does not fall under Chapter 20. Instead, it is appropriately classifiable under CTH 21069099, for the reasons already elaborated above.

6.6 Items at Sl. Nos. 8 to 12 were proposed by the appellant to be classified under CTH 16025000, whereas the AAR ruled that they fall under CTH 21069099. Heading 16025000 (“Of bovine animals”) falls under heading 1602, which covers “Other prepared or preserved meat, meat offal, blood or insects.” Chapter 16 pertains to “Preparations of meat, fish, crustaceans, molluscs, other aquatic invertebrates, or insects.” The products in question are of the nature of “curry” and are therefore “ready-to-eat packed food” rather than merely “prepared or preserved meat.” Accordingly, we concur with the AAR that the correct classification is CTH 21069099.

6.7 Similarly, items at Si. Nos. 13 to 21 have also been classified by the appellant under Chapter 16 for the same reasons applied to Si. Nos. 8 to 12. For the reasons already discussed above, we find that they too fall under CTH 21069099. The mere fact that the meat content of an item exceeds 20% does not by itself justify classification under Chapter 16; the nature of the final product as a whole must be considered. A ready-to-eat packaged curry is a distinct product, different from “prepared or preserved meat” in the sense intended by Chapter 16.

6.8 With regard to the item at SI. No. 20,Tuna Tomato Rice, although it is not “curry” per se, it is still a ready-to-eat packaged product. Therefore, on the grounds set out above, it also merits classification under CTH 21069099 rather than under Chapter 16.

6.9 We find that there is no dispute on classification of Items at S1 No 22 to 26 and further that the Advance Ruling application was limited to classifications of the items and the question of rate of GST was not covered in the question.

7. In the light of the facts and legal position as stated above, the following order is issued:

ORDER

The classification of the items at SI No 1 to 26 in the list is upheld as classified by the Authority for Advance Ruling. Item at Si No 27 is classified under CTH 20052000. The GSTIN of the applicant erroneously mentioned as 32AATFD1308H1Z0 stands corrected as 32AAACH9887R1ZO.

Author Bio