Definition of Capital Goods [Section 2(19)]

“Capital goods” means goods, the value of which is capitalized in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business.

Goods will be regarded as capital goods if the following conditions are satisfied:

(a) The value of such goods is capitalized in the books of account of the person claiming input tax credit;

(b) Such goods are used or intended to be used in the course or furtherance of business.

The following aspects need to be noted:

(a) Assuming that the value of capital goods was not capitalizedin the books of account, the person purchasing such capital goods would still be eligible to claim input tax credit on them since the definition of ‘input tax’ applies to goods that are not capitalized;

(b) Capital goods lying at the job-workers premises would also be considered as ‘capital goods’ in the hands of the purchaser as long as the said capital goods are capitalized in his books of account.

Eligibility and conditions for taking input tax credit Sec.16 of CGST Act 2017.

(1) Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him, Which are used or intended to be used in the course or furtherance of his business and The said amount shall be credited to the electronic credit ledger of such person.

Section 49. Payment of Tax, Interest, Penalty and other Amounts

(1) Every deposit made towards tax, interest, penalty, fee or any other amount by a person by internet banking or by using credit or debit cards or National Electronic Fund Transfer or Real Time Gross Settlement or by such other mode and subject to such conditions and restrictions as may be prescribed, shall be credited to the electronic cash ledger of such person to be maintained in such manner as may be prescribed.

(2) The input tax credit as self-assessed in the return of a registered person shall be credited to his electronic credit ledger, in accordance with section 41; to be maintained in such manner as may be prescribed.

(3) The amount available in the electronic cash ledger may be used for making any payment towards tax, interest, penalty, fees or any other amount payable under the provisions of this Act or the rules made thereunder in such manner and subject to such conditions and within such time as may be prescribed.

(4) The amount available in the electronic credit ledger may be used for making any payment towards output tax under this Act or under the Integrated Goods And Services Tax Act in such manner and subject to such conditions and within such time as may be prescribed.

Sec. 16(2) No registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless, –

(a) He is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

(b) He has received the goods or services or both

(c) Subject to the provisions of section 41, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilization of input tax credit admissible in respect of the said supply; and

(d) He has furnished the return under section 39.

(3) Where the registered person has claimed depreciation on the tax component of the cost of capital goods and plant and machinery under the provisions of the Income Tax Act, 1961,

The input tax credit on the said tax component shall not be allowed.

(4) A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after

The due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or Furnishing of the relevant annual return, whichever is earlier

Rule 36

(3) No input tax credit shall be availed by a registered person in respect of any tax that has been paid in pursuance of any order where any demand has been confirmed on account of any fraud, wilful misstatement or suppression of facts.

(4) [Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37,

Shall not exceed 20 per cent. of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37] (vide Notf no. 49/2019-CT dt. 09.10.2019)

Note: As per My Personal Opinion 120% of the ITC reflecting in 2A.

As it is not specifically mentioned anywhere in the Act or rules So , there are lot of Difference of opinions regarding the same (Your opinion may differ on this point, aforesaid is as per my personal opinion)

Rule 37

Reversal of input tax credit in case of non-payment of consideration.

According to second proviso to Section 16 (2) (d) of CGST Act, 2017 “where a recipient fails to pay to the supplier of goods or services or both,

Other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon

Within a period of one hundred and eighty days from the date of issue of invoice by the supplier,

An amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed.”

According to rule 37 (1) of CGST rules, 2017 “a registered person, who has availed of input tax credit on any inward supply of goods or services or both,

but fails to pay to the supplier thereof, the value of such supply along with the tax payable thereon,

within the time limit specified in the second proviso to sub-section (2) of section 16,

shall furnish the details of such supply, the amount of value not paid and the amount of input tax credit availed

of proportionate to such amount not paid to the supplier

in FORM GSTR-2 for the month immediately following the period of one hundred and eighty days from the date of the issue of the invoice.”

(Aforesaid is as per Sub rule 1&2 of rule 37)

(3) The registered person shall be liable to pay interest at the rate notified under sub-section (1) of section 50 (@18%)

for the period starting from the date of availing credit on such supplies till the date when the amount added to the output tax liability, as mentioned in sub-rule (2), is paid.

RULE 42.

Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

(1) The input tax credit in respect of inputs or input services, which attract the provisions of sub-section (1) or sub-section (2) of section 17, being partly used for the purposes of business and partly for other purposes,

Or partly used for effecting taxable supplies including zero rated supplies

And partly for effecting exempt supplies,

Shall be attributed to the purposes of business or for effecting taxable supplies in the following manner, namely,-

a) The total input tax involved on inputs and input services in a tax period, be denoted as ‘T‘;

b) The amount of input tax, out of ‘T‘, attributable to inputs and input services intended to be used exclusively for the purposes other than business, be denoted as ‘T1‘;

c) The amount of input tax, out of ‘T‘, attributable to inputs and input services intended to be used exclusively for effecting exempt supplies, be denoted as ‘T2‘;

d) The amount of input tax, out of ‘T‘, in respect of inputs and input services on which credit is not available under sub-section (5) of section 17 (Blocked Credit), be denoted as ‘T3‘;

e) The amount of input tax credit, credited to the electronic credit ledger of registered person, be denoted as ‘C1‘ And

calculated as- C1 = T- (T1+T2+T3);

f) the amount of input tax credit attributable to inputs and input services intended to be used exclusively for effecting supplies other than exempted but including zero rated supplies, be denoted as ‘T4‘;( Means for Taxable Supplies)

g) ‘T1‘, ‘T2‘, ‘T3‘ and ‘T4‘ shall be determined and declared by the registered person at the invoice level in FORM GSTR-2; [and at summary level in GSTR-3B];

h) Input tax credit left after attribution of input tax credit under clause [(f)] shall be called common credit, be denoted as ‘C2‘

And calculated as: C2 = C1- T4;

Note: Common credit here means the credit that partly relates to Business/ Taxable Supplies and partly for Exempt/Non Business (Means Combination of Business/taxable supplies+exempt+Non Business).

i) The amount of input tax credit attributable towards exempt supplies be denoted as ‘D1‘

And calculated as D1= (E÷F) × C2 where,

‘E‘ is the aggregate value of exempt supplies during the tax period, and

‘F‘ is the total turnover in the State of the registered person during the tax period.

Note :Tax Period here means monthly or quarterly as the case may be .

j) The amount of credit attributable to non-business purposes if common inputs and input services are used partly for business and partlyfor non-business purposes,

Be denoted as ‘D2‘, (Related To Non business)

And shall be equal to five per cent Of C2 (Common Credit); and

k) The remainder of the common credit shall be the eligible input tax credit attributed to the purposes of business and for effecting supplies other than exempted supplies but including zero rated supplies and shall be denoted as ‘C3‘,

Where – C3 = C2 – (D1+D2); (Eligible credit)

l) The amount ‘C3’, D1’, and ‘D2’ shall be computed separately for the Input tax credit of central tax, State tax, Union territory tax and integrated tax and declared in FORM GSTR-3B or through FORM GST DRC-03

m) The amount equal to aggregate of ‘D1‘ and ‘D2‘ shall be

[Reversed by the registered person in FORM GSTR-3B or through GSTR DRC-03];

Provided that where the amount of input tax relating to inputs or input services used partly for the purposes other than business and partly for effecting exempt supplies has been identified and segregated at the invoice level by the registered person,

The same shall be included in ‘T1‘ and ‘T2‘ respectively, and the remaining amount of credit on such inputs or input services shall be included in ‘T4‘.

(2) [Except in case of Supply of services covered by clause (b) of paragraph 5 of Schedule II of the Act,

The input tax credit] determined under sub-rule (1) shall be calculated finally for the financial year

before the due date for furnishing of the return for the month of September following the end of the financial year to which such credit relates, in the manner specified in the said sub-rule and

a) where the aggregate of the amounts calculated finally in respect of ‘D1‘ and ‘D2‘ exceeds the aggregate of the amounts determined under sub-rule (1) in respect of ‘D1‘ and ‘D2‘,

Such excess shall be [reversed by the registered person in FORM GSTR-3B or through GSTR DRC-03] in the month not later than the month of September following the end of the financial year to which such credit relates and

The said person shall be liable to pay interest on the said excess amount at the rate specified in sub-section (1) of section 50 (@18%)

For the period starting from the first day of April of the succeeding financial year till the date of payment; or

b) Where the aggregate of the amounts determined under sub-rule (1) in respect of ‘D1‘ and ‘D2‘ exceeds

The aggregate of the amounts calculated finally in respect of ‘D1‘and ‘D2‘,

Such excess amount shall be claimed as credit by the registered person in his return for a month not later than the month of September following the end of the financial year to which such credit relates.(Registered person cannot claim the interest on that amount)

Note:

Determined here means, that is computed for each tax period (monthly or quarterly as the case may be)

And Calculated here means that is computed annually for the whole financial year.

Rule-43

Manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases

Rule 43 and principles embedded therein

Section 17(1) and section 17(2) are cause of creation of rule 43. Section 17(1) intends that ITC in respect of capital goods shall not be available to the extent these are used for non-business purposes.

Similarly, section 17(2) intends that ITC in respect of capital goods shall not be available to the extent these are used for effecting exempt outward supplies.

So, Rule 43 is based on following principles –

1. If inward supply of capital goods is used for effecting taxable outward supplies then ITC shall be available in respect of such goods to the extent these are used for said purpose.

2. If inward supply of capital goods is used for effecting zero rated outward supply then ITC shall be available in respect of such goods to the extent these are used for said purpose.

3. If inward supply of capital goods is used for effecting exempt outward supplies then ITC shall not be available in respect of such goods to the extent these are used for said purpose.

4. If inward supply of capital goods is used for non-business purpose then ITC shall not be available in respect of capital goods to the extent these are used for said purpose.

Since this a settled position of law that a rule cannot override the provisions of Act, so in addition to above, ITC in respect of those capital goods shall also not be available which falls within the scope of section 17(5) (Blocked Credit). This point has been focused specifically because rule 43 is silent on ITC of such capital goods.

Assumption taken by rule 43 (for commonly used capital goods)

1. Capital goods has a life of 5 years i.e. 60 months i.e. 20 quarters. So, ITC in respect of a capital goods shall be available over a period of 5 years/60 months/20 quarters. Rule 43 specifically uses 5% per quarter.

2. When we compare rule 43 with rule 42, there is no provision for annual calculation in rule 43 as is there in rule 42. So, rule 43 has been drafted in such a manner that calculation of credit for a particular month must be accurate and final within that period itself.

In other words, it can be concluded that as soon as a tax period (i.e. month) is over, self-assessment of 1/60th of the credit is over. Now one doesn’t need to see this 1/60th part in next tax period(s).

Similarly, one can conclude that as soon a quarter is over, self-assessment of 5% is over. Rule 43 one step further clarifies that a part of quarter shall be treated as complete quarter.

3. One can take credit in respect of a capital goods as soon as four conditions as specified in section 16(2) are fulfilled, if otherwise is not ineligible for credit.

Example

Suppose a capital goods was purchased and received on 16.07.2018 along with invoice of even date. IGST charged on invoice was Rs. 6,60,000.

Till December 2018, it was being used for effecting exempt supplies.

But from January 2019 to June 2019, it was used commonly for effecting taxable supplies, exempt supplies and for the purpose of business as well as non-business purpose.

From July 2019 to September 2019, it was used exclusively for effecting taxable supplies.

| Turnover type | January 2019 | February 2019 | March 2019 | April 2019 | May 2019 | June 2019 |

| Exempt | 4 crores | 5 crores | 2.5 crores | 4 crores | 2 crores | 3.5 crores |

| Non-business | 5 lakh | 5 lakh | 5 lakh | 5 lakh | 5 lakh | 5 lakh |

| Total | 10 crores | 15 crores | 10 crores | 20 crores | 11 crores | 12.25 crores |

Since up to December 2018, it was being used for effecting exempt supplies, ITC would have not been taken up to December 2018.

Monthly proportionate ITC = Tax ÷ 60 = 6,60,000 ÷ 60 = 11,000

ITC finalized upto December 2018 = monthly proportionate ITC × number of months lapsed

=11,000 × (months from July 2018 to December 2018)

= 11,000 × 6 = 66,000

So, out of Rs. 6,60,000, self-assessment of ITC of Rs. 66,000 has become final.

In other words, since it was being used from July 2018 to December 2018 (i.e. for 2 quarters) for effecting exempt supplies, proportionate amount of ITC i.e. Rs. 66,000 shall not be allowed.

Now we will see treatment of remaining ITC of Rs. 5,94,000 i.e. 6,60,000-66,000.

For the month of January 2019, it was used for common purposes.

For this purpose, proviso to rule 43(1)(c) read with rule 43(1)(d) specifies that ITC in respect of commonly used capital goods (i.e. common credit) denoted by “A” [ or ƩA= Tc] shall be calculated as under –

Input tax on such capital goods 6,60,000

Less: 5% for every quarter from date of invoice 66,000

(i.e., 6,60,000 × 5% × 2) ——————

TC = ƩA 5,94,000

Logically, if we exclude the proportionate exempt or non-business part from this Rs. 5,94,000, balance credit should be granted to the taxpayer.

When we move further, we see an error in drafting of rule 43. Look at this –

As per rule 43(1)(e), proportionate monthly common credit (denoted by Tm; Tm = Tc / 60) on such goods shall be Rs. 9,900 i.e. 5,94,000/60

But it should logically be Rs. 11,000 i.e., 6,60,000/60. However, treatment given in rule is beneficial for the taxpayer. Look at this –

Proportionate exempt part i.e. common credit attributable towards exempt supplies denoted by Te shall be calculated as under –

Te = (E÷F) × Tm

| as specified in rules | Logically |

| Te = (4÷10) × 9900 = 3,960 | Te = (4÷10) × 11,000 = 4,400 |

E = Exempt turnover for the tax period i.e. for January 2019 in our example

F = Total turnover for the tax period i.e. for January 2019 in our example

| Calculation of ITC in respect of said capital goods for January 2019 | |||

| Particulars | Remark / calculation | Amount

(as specified in rules) |

Amount (logically) |

| Amount to be credited in electronic credit ledger (i) | TC | 5,94,000 | 5,94,000 |

| Amount to be added in output tax liability (ii) | Te | 3,960 | 4,400 |

Rule 43(1)(h) specifies that it shall be added to output tax liability along with applicable interest.However, it is important to note that no interest shall be levied on this amount because ITC on such goods has itself been taken in month of January 2019 itself.

Important to note here is that rule 43 is silent on proportionate non-business part i.e. common credit attributable towards non-business use.

However, section 17(1)intends that if capital goods are used for non-business purpose then ITC shall not be available in respect of capital goods to the extent these are used for said purpose.

Since Act Will prevail, it is a suggestion that while calculating exempt turnover for the tax period i.e. January 2019 in our example, non-business turnover shall also be added.

In this way, a reasonable amount attributable towards non-business purposes shall also be added to output tax liability. Non-business turnover can be determined by applying valuation rules.

| Calculation of ITC in respect of said commonly used capital goods from February 2019 to June 2019 | ||||||

| Particulars | Remark / calculation | February 2019 (as per rules) | March 2019

(as per rules) |

April 2019

(as per rules) |

May 2019

(as per rules) |

June 2019

(as per rules) |

| Tr (Rs.) | As per rules | 9,900 | 9,900 | 9,900 | 9,900 | 9,900 |

| E (Rs.) | As per rules | 5 crores | 2.5 crores | 4 crores | 2 crores | 3.5 crores |

| F (Rs.) | As per rules | 15 crores | 10 crores | 20 crores | 11 crores | 12.25 crores |

| ITC to be taken | Nil | Nil | Nil | Nil | Nil | |

| Amount to be added in output tax liability | Te = (E÷F) × Tm

(as per rules) |

3,300 | 2,475 | 1,980 | 1,800 | 2,828.57 |

| Interest to be added | As per rules on amount added above | From Jan-19 to Feb-19 | From Jan-19 to Mar-19 | From Jan-19 to April-19 | From Jan-19 to May-19 | From Jan-19 to Jun-19 |

as suggested, exempt turnover shall include non-business turnover also.

No need, because Rs. 5,94,000 has already been credited in electronic credit ledger in month of January 2019

logically this amount should have been calculated based on Tm being Rs. 11,000 in place of 9900 which is as per rules.

because ITC of Rs. 5,94,000 was taken in January 2019.

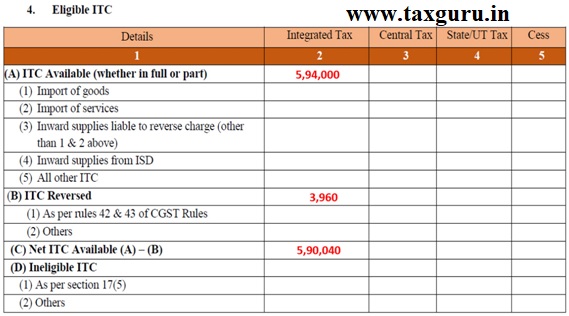

Presentation in GSTR-3B of January 2019

From here, it can be clearly seen that even if rules intend to add the amount in output taxliability but while implementing the law, amount is being reversed from ITC.

Now we come on July 2019.

From July 2019 and onward, said goods was used for taxable purpose, hence no separate treatment is requiredbecause ITC in respect of said goods has already been taken in January 2019. (This is why rule 43 does not specify any treatment for this)

When capital goods being used exclusively for effecting taxable supplies are subsequently used for common purpose

Similarly, for such cases, proviso to rule 43(1)(d) has specified that in such case common credit (Tc) shall be calculated as under –

Input tax on such capital goods

Less: 5% for every quarter lapsed from date of invoice

————

TC = ƩA

However, there is no need to take any ITC because ITC would have been taken on fulfilment of conditions of section 16(2) of the Act.

Remaining procedure is same as discussed earlier.

*****

Disclaimer: The Purposes of the article is knowledge sharing while the information is believed to be accurate to the best of my knowledge and belief. I do not make any representation or warranties, express or implied, as to the accuracy or completeness of this information. I accept no responsibilities for any errors it may contain, whether caused by negligence or otherwise or for any loss, howsoever caused or sustained, by the person who relies upon it.

Author Bio

when a situtaion raise to buy a trailor for business purpose weather Can I avail the input, and it could be used for business in that case am a transporter can I rasie invoice to another transporter Under GTA as 0% output tax?

Sir,

Thank you for your excellent presentation of Rules in an easily understandable manner.