What is harm in making single head for payment of GST in E-Cash Ledger of registered person?

As of now, by mistake if you pay CGST in place of IGST, then inter-head adjustment of these taxes are not allowed in GST returns, you will have to claim refund of this tax erroneously deposited under CGST head and again pay the correct tax under IGST head and only then you can file your GST return. Inter-head adjustment of CGST & IGST etc., is allowed only for input tax credit and not for tax paid in cash.

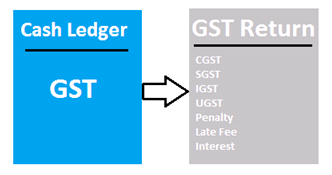

Do you agree that payment of GST shall be made under only one head in E-cash ledger and apportionment of this tax to respective heads like, CGST, SGST, UGST, IGST, Penalty, Late Fee, Interest etc. shall be allowed to be made in GST returns itself. Under the current direct tax regime, similar adjustment are allowed, like in TDS and Income Tax challans, where a tax deposited under single head can be utilised for payment of various tax liabilities under the same Act.

Also, since amount of balance in this E-Cash Ledger is available for utilisation by the government only when such balance is set off for payment of taxes with respective liabilities in GST returns etc. In other words, a registered person by filing his GST returns authorizes the government to claim and use the balances available in these E-Cash & E-Credit ledger for respective heads of taxes and duties.

So, in my opinion there is no harm in making single head for payment of GST in E-Cash Ledger of registered person, which can be used for discharge of liabilities of a registered person under various head of taxes. This will not only reduce the chances of error in depositing taxes under wrong heads. But also, in case of apportionment of these taxes under wrong heads, rectification or revisions of such returns would be much easier and without any loss of government exchequer and without any financial hardships to the registered person.

Author Bio

I think, your suggestion definitely may be taken by the GST Council, if it comes to their knowledge. ITC Ledger is o.k. But Cash Ledger should be common to utilize to any heads of Tax Liability.

Thanks for your Thinking, on the Tax Payers concern.

It is a very good suggestion which will reduce the burden on dealer. In fact, GSTN should create an E-Wallet for each dealer into which all credits such as ITC, export incentives, payment made in cash or bank transfer by the dealer himself should all be credited and from the E-Wallet all outgoings as per GSTR3B as CGST SGST or IGST can all be debited. This will make process simple and error free.