Indeed, rolling out of GST from July 1, 2017 is unstoppable. But to provide relief to the taxpayers, GST Council in its latest meeting, extended the time period for filing of return i.e. FORM GSTR-1 & FORM GSTR-2 for the first two months after the roll out of GST.

In this write-up, the Process of filing of Return of Outward Supplier & Inward Supplier is being covered.

Introduction

As per Section 2(83), “outward supply” in relation to a taxable person, means supply of goods or services or both, whether by sale, transfer, barter, exchange, license, rental, lease or disposal or any other mode, made or agreed to be made by such person in the course or furtherance of business.

As per Section 2 (67), “inward supply” in relation to a person, shall mean receipt of goods or services or both whether by purchase, acquisition or any other means with or without consideration.

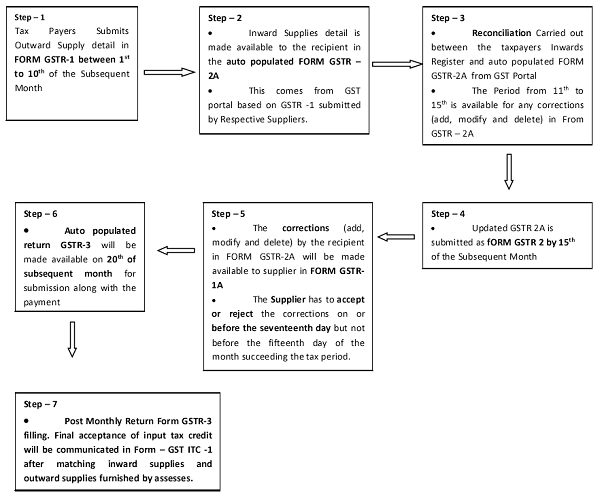

Process of Filing of GSTR-1 & GSTR-2

- Every Registered person* (outward supplier) shall furnish, electronically FORM GSTR-1before the tenth day of the month succeeding the said tax period. But in any case not between 10th to 15th of the succeeding.

*. other than an Input Service Distributor, a non-resident taxable person and a person paying tax under the provisions of section 10 or section 51 or section 52.

2. The same shall be auto- populated to Recipient in PART A of FORM GSTR- 2A, FORM GSTR- 4A, FORM GSTR- 6A.

3. Now, Recipient (Inward Supplier) furnish GSTR-2, which is auto- populated to the supplier in FORM GSTR-1A from 10thto 15th of the succeeding month.

4. Now, either outward supplier accepts or rejects the details furnished by inward supplier. If the supplier rejects the return then he has to do the same from 15th to 17th of the succeeding month.

5. Once the return is rejected by the supplier, the difference of tax an amount to the extent of discrepancy shall be added to the output tax liability of the recipient in his return to be furnished in FORM GSTR-3for the month succeeding the month in which the discrepancy is made available.

| Name of the Person | Actual Date | Extended Date for the 1st two months |

| Outward Supplier (for the month of July) | 10th August | 5th September |

| Outward Supplier (for the month of August) | 10th September | 20th September |

| Inward Supplier Supplier (for the month of July) | 15th August | 10th September |

| Inward Supplier (for the month of August) | 15th September | 25th September |

As per Rule 1(3) & (4) of Returns:

| Form filed by Outward Supplier | Auto populated to Inward Supplier |

|

FORM GSTR-1 |

FORM GSTR-2A (for every registered person, other than an Input Service Distributor, a non-resident taxable person and a person paying tax under the provisions of section 10 or section 51 or section 52) |

| FORM GSTR- 4A (Auto drafted details for registered persons opting composition levy) | |

| FORM GSTR- 6A (Details of supplies auto drafted from GSTR-1 or GSTR-5 to ISD.) | |

| Form filed by Inward Supplier | Auto populated to Outward Supplier |

| FORM GSTR- 4 (Quarterly return for registered persons opting composition levy) | FORM GSTR- 1A |

| FORM GSTR- 6 (Return for input service distributors) | |

| Please note that, Service Tax Return for the period from 1st April, 2017 to 30th June, 2017 is to be filed by 15th of August, 2017 (Notification No. 18/2017-ST). |

Conclusion

There is a mis-conception that implementation of GST will bring in more compliances then present tax structure and it is going to be a cumbersome process. So far as filing of Returns with respect to Form GSTR-1, Form GSTR-2 & GSTR-3 is concerned, when the outward supplier fills Form GSTR-1 by the 10th of next month, the same get automatic updated in Form GSTR-2 of the Inward Supplier(recipient), which is to be filed by the Recipient by 15th of the next month.

GSTR 2 is not to be filed by anybody. It will be appearing automatically on their own account and they can confirm it. If there is any transaction missing in purchase and is not showing because the person from whom you bought has forgotten to put it, then you get a right to add it. It is an auto-populated return. Click it and accept it online. By 17th of the month, both the supplier and the recipient would have to reconcile the invoice details and file the third return (GSTR-3) by 20th of the month.

In Nutshell:

GSTR-3 is a blend of FORM GSTR-1 and FORM GSTR-2, which is computer generated and gives the summary of total output tax liability, input tax credit and the difference is the tax liability for the month.

Hope this information will help you in your Professional endeavors. For further assistance/query, feel free to write to us.

Author: C S Ekta Maheshwari is the Author of this article and is Company Secretary by profession. The Author can be reached at csektamaheshwari14@gmail.com

Disclaimer:

The entire contents of this article is solely for information purpose and have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation.. It doesn’t constitute professional advice or a formal recommendation. The author has undertook utmost care to disseminate the true and correct view and doesn’t accept liability for any errors or omissions. You are kindly requested to verify & confirm the updates from the genuine sources before acting on any of the information’s provided herein above.

Author Bio

1.Do anybody filed GSTR3 for the month of July. 2.Whether it should be done manually after filling GSTR3 form or it will appear in Dashboard. In my Dashboard i dont get GSTR3.

We are manufacturer supplying in state and interstate. Some material purchased during July 2017 have not consumed during July and will be consumed in next month.

we intent to deposit the Tax on all our sales but ITC is to utilised only for quantity consumed to manufacture the final product. Is it provided in the return

or we have to take full utilization of ITC

HI EKTA….! THIS ANIRBAN……………..! THANKS FOR UR UPDATES………..! ITS REALLY SO USEFUL FOR ALL ………!

Please provide notification number for GST updates related to return dates.

Thankyou

Please provide reference/notification no. for extension dates for GST returns.

Thank you,

Thanks Ekta.

Excellent presentation on GSTR facts.

Will lead to a lot of conflict.

Sir, GSTR 2, also we have to check whether the counter party accepted or not if they have not accepted or not uploaded in there sales we have to do need full (calls, emails and etc.,) so that is also one work only. GSTR3 also we have to check with our calculation if difference we have to find where the problem arises.