Article covers Meaning of Annual Return,Who should file Annual Return, Due date for filing annual return, Different types of Annual Return, Penalty for late filing of Annual GST return, Broad Overview of GSTR -9, Format of GSTR -9 and How to prepare GSTR-9.

This is our first ever annual return since the implementation of Goods and Services act 2017. Everyone would have started preparation for your first ever Annual Return and I know you are busy in that, But what I say is you must read this Article before you start filing the Annual Return.

Page Contents

1. Meaning of Annual Return under GST

An Annual Return is a return that has to be filed once in a year by the Persons registered under GST. It consists of details regarding the supplies of Goods and/or Services made and recieved during the year which includes both Inter state and Intra state supplies. It consolidates the information furnished in monthly and quarterly returns during the year.

2. Who Should file Annual Return under GST?

Every registered taxpayer other than the following person is required to file annual return under section 44 of CGST Act 2017

- Input Service Distributor

- A person paying tax under Section 51 (TDS)

- A person paying tax under Section 52 (TCS)

- A casual taxable person

- Non resident taxable person.

3. Due date for filling Annual Return

As per Section 44(2) of CGST Act, Every Taxable person shall file annual return in FORM GSTR-9 for every financial year electronically on or before 31st December following the end of such financial year. However this provision shall not apply to,

- Input Service Distributor

- A person paying tax under Section 51 or 52 (TDS or TCS)

- A casual taxable person

- Non resident taxable person

NOTE: For Instance, For Financial year 2017-18, the due date for filing GSTR-9 is 30th June 2019. However for the FY 18-19 Annual return must be filed on or before 31st December 2019.

NOTE: In case a person opted to pay tax under composition scheme, then he shall furnish annual return in FORM GSTR-9A.

4. Different types of Annual Return under GST

There are 4 types of Annual Return:

1. GSTR-9 : It should be filed by the Regular Taxpayers filing GSTR-1 & GSTR-3B.

2. GSTR-9A: It should be filed by Persons opted to pay tax under Composition Scheme.

3. GSTR-9B: It should be filed by the e-Commerce operators who have filed GSTR-8 during the year.

4. GSTR-9C: It should be filed the taxpayers whose annual turnover exceeds 2 crores during the financial year. All such taxpayers are also required to get their accounts audited & file a copy of audited annual accounts and Reconciliation statement of tax already paid and tax payable as per audited accounts along with GSTR-9C.

5. Penalty for Late filling of Annual Return under GST

As per Section 47(2) of CGST Act 2017, Any Registered person who fails to furnish annual return, as required under section 44, by the due date shall be liable to pay a late fee of Rs.100 per act (SGST Act & CGST Act) for every day during which such failure continues subject to a maximum of an amount calculated at a quarter per cent. of his turnover in the state or union territory.

Thus it is Rs.100 under CGST Act and Rs. 100 under SGST Act, the total penalty is Rs.200 per day of default. There is no late fee on IGST .

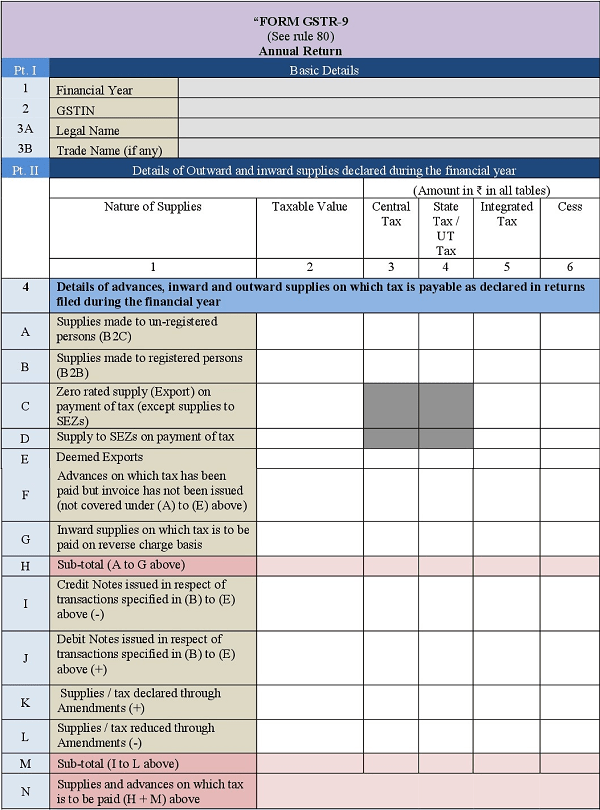

6. Broad Overview of GSTR -9

GSTR -9 is devided into 6 Parts and 19 Tables

- Part-I : This part asks for basic details, such as the Financial year, GSTIN, Legal and Trade names. These details will be auto-populated in the form. ( From Table 1 to Table 3A).

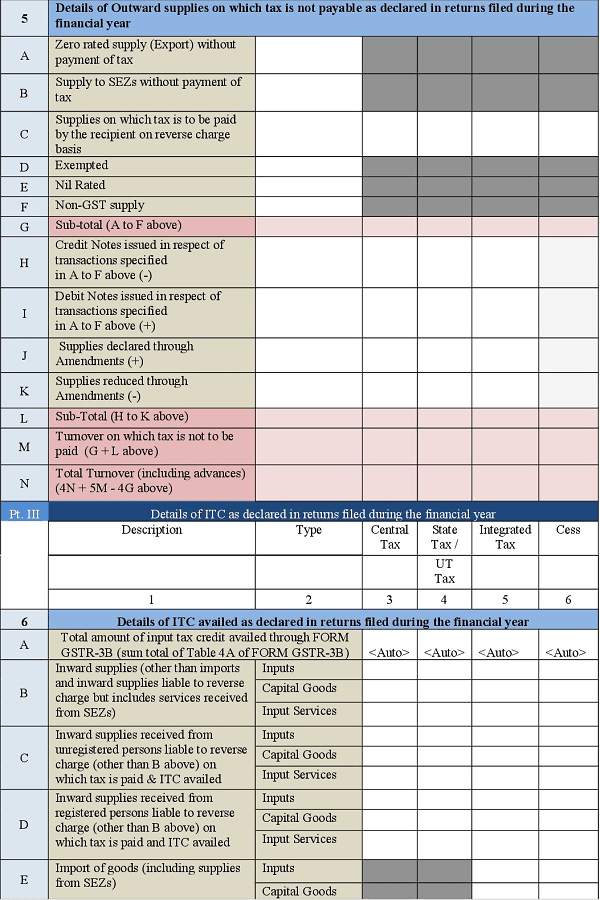

- Part-II : This part asks taxpayers to provide the details of Inward and Outward supplies declared during the financial year. ( From Table 4 to Table 5).

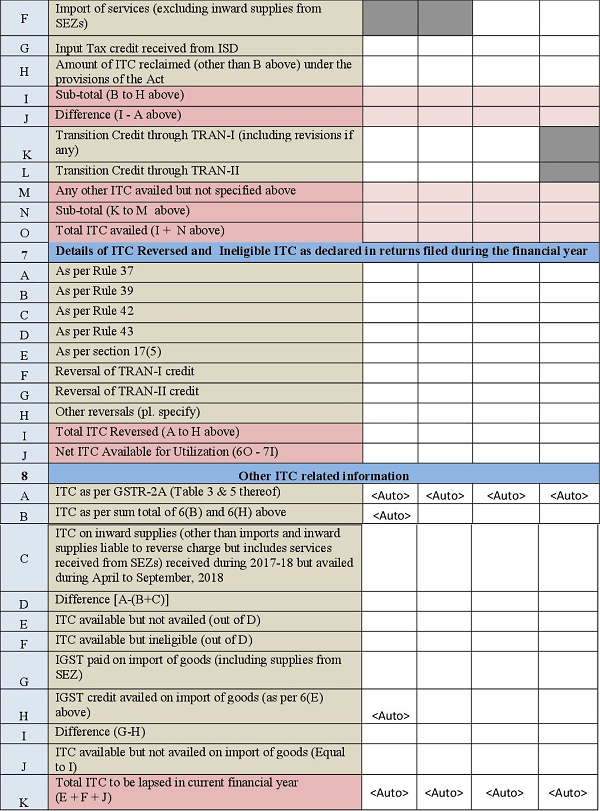

- Part-III : This is where taxpayer provide the details of Input Tax Credit (ITC) as declared in returns filed during the financial year. Part III also asks for details of the ITC reversed and Ineligible ITC as declared in Individual returns. ( From Table 6A to Table 8A).

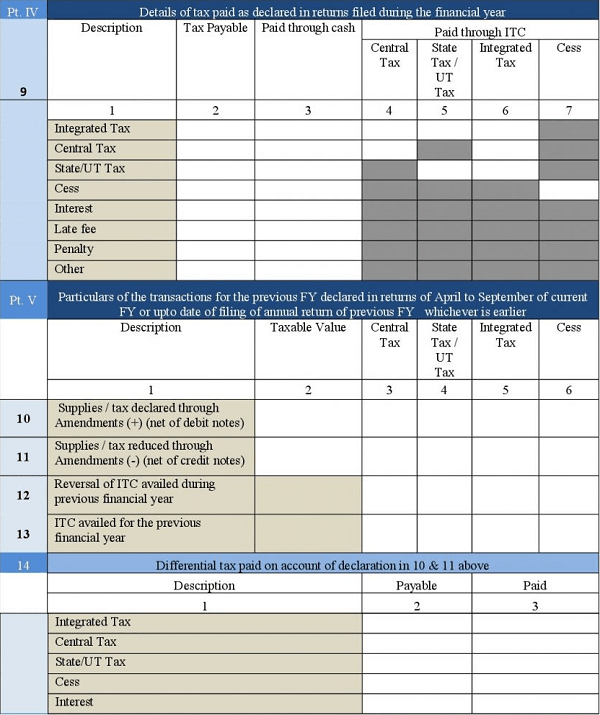

- Part-IV : Here, Taxpayers will input details of taxes paid as declared in returns filed previously during the fiscal year. (Table 9).

- Part-V : This part asks for transaction particulars of the previous fiscal year, declared in returns from April to September of the current fiscal year, or up to the date of annual returns of the previous fiscal year were filed, whichever is earlier. Additional or omitted entries belonging to the previous fiscal year, but reported in current fiscal year, would be declared here as well. ( From Table 10 to Table 14)

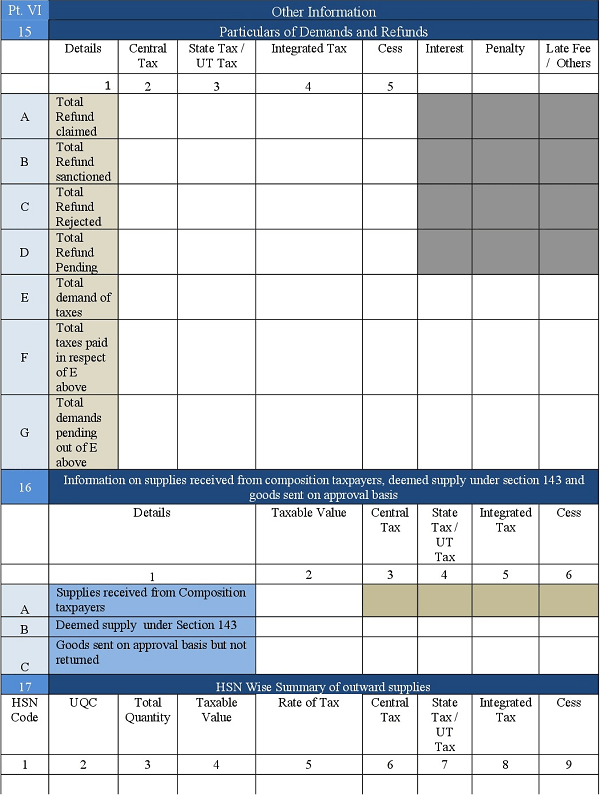

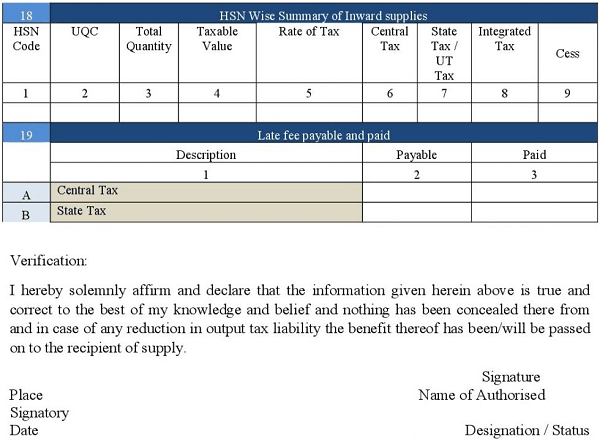

- Part-VI : Taxpayers will report other information here. This could include Demand & Refund details; supplies received from composition tax payers; Deemed supply of goods sent on approval basis; HSN wise summary of outward and inward supplies; late fees payable as well as those paid. ( From Table 15 to Table 19)

7. Format of GSTR -9

8. How to prepare GSTR-9?

The declaration of the information in Annual Return has multiple implications. Any incorrect information can attract tax demands, interests and penalties on the same. The principle source for preparing GSTR 9 will be GSTR 1 and GSTR 3B returns. All the information must be cross checked with the books of accounts before declaring in the annual returns.

Broadly, the form entails the declaration of annual sales, bifurcating it between the cases subject to tax and cases not subject to tax. On the Purchase side the annual value of inward supplies and ITC availed thereon, classified as inputs, input services and capital goods and the ITC to be reversed due to Ineligibility.

So you should note down all these above things and should be filed carefully because Once you file the annual return , it cannot be revised again.

we Have filed GSTR1 & GSTR 3b but GSTR1 sale data is correct & incorrect data filed in GSTR 3b which is adjusted in next FY , then i have to file return on what basis as per GSTR1 or GSTR 3b. pls help

hello

exempted purchase kis colum me bharna hai.

please add me