Explore the issues surrounding the constitution of the Goods and Services Tax Appellate Tribunal (GSTAT) despite amendments in the Finance Act, 2023.

Tribunals play a vital role in delivering justice in specific domains of law. Unfortunately, despite the implementation of the Goods and Services Tax (GST) in the country nearly six years ago, the Goods and Services Tax Appellate Tribunal (GSTAT) has not been constituted. Furthermore, there have been no sincere efforts from the government to establish it, except for recent amendments placed in Sections 109 and 110 of the CGST Act, 2017. This article aims to highlight one of the several issues that may persist even after the amendments made through The Finance Act, 2023.

Originally, Section 109(3) of the CGST Act, 2017 provided for the constitution of the National Bench of GSTAT, which would be presided over by a President (Judicial) and two technical members (one from the Centre and one from the State). Similarly, Clause (9) of Section 109 provided for the constitution of State Benches of GSTAT.

In the case of Revenue Bar Association Vs. UOI [2019 (30) GSTL 584 (Mad.)], the Hon’ble Madras High Court observed that a properly trained judicial mind is necessary to decide issues related to the decision-making process of the adjudicating authority or the appellate authority, the interpretation of notifications, and sections under the GST law. This requirement cannot be fulfilled solely by technical members. Consequently, Sections 109(3) and (9) were struck down.

The Finance Act, 2023 aims to substitute the existing Sections 109 and 110 of the CGST Act, 2017 to address the legal deficiencies in the constitution of GSTAT, including the issue described above. The newly substituted Section 109(3) provides for the constitution of the Principal Bench of GSTAT in New Delhi with a total of four members, including the President (Judicial), another judicial member, and two technical members (one from the Centre and one from the State). Similarly, Section 109(4) provides for the constitution of State Benches with a total of four members, consisting of two judicial members and two technical members.

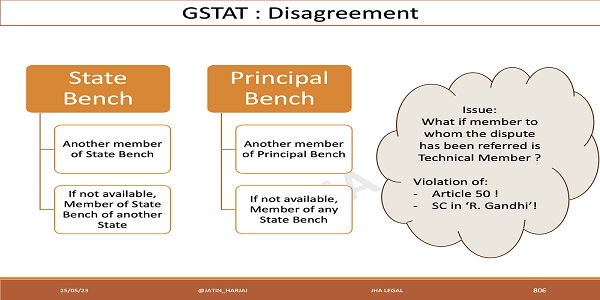

The law stipulates that most cases will be heard by a Division Bench comprising one Judicial Member and one Technical Member, except for cases specified in Section 109(8), which will be heard by a single-member bench. In the event of a disagreement between the members on any point, the matter shall be referred to another member for further consideration. The relevant provision is extracted below:

(9) If, after hearing the case, the Members differ in their opinion on any point or points, such Member shall state the point or points on which they differ, and the President shall refer such case for hearing,-

(a) where the appeal was originally heard by Members of a State Bench, to another Member of a State Bench within the State or, where no such other State Bench is available within the State, to a Member of a State Bench in another State;

(b) where the appeal was originally heard by Members of the Principal Bench, to another Member from the Principal Bench or, where no such other Member is available, to a Member of any State Bench,

and such point or points shall be decided according to the majority opinion including the opinion of the Members who first heard the case.

GSTAT Disagreement

Perusal of above clause revels that president may refer the case for further hearing on such disputed point(s) before any of the other member be it Judicial Member, Technical Member (Centre) or Technical Member (State). In case the such disputed point(s) are referred to either of the Technical Members and decided accordingly to the majority of the three members including two who originally heard the case, the decision shall be outcome of bench consisting two technical members and one judicial members, which is primarily against article 50 of the Constitution of India which provides that the State shall take steps to separate the judiciary from the executive, in the public services of the State.

While deliberating upon validity of constitution of NCLT and NCLAT under the Companies Act, 1956 hon’ble supreme court in the case of Union of India Vs. R. Gandhi [(2010) 11 SCC 1] summarised broad principles for correction in legal provisions made for constitution of the tribunals under the said law. One of the aspects described by hon’ble apex court was as under:

(xiii) Two-member Benches of the Tribunal should always have a judicial member. Whenever any larger or special Benches are constituted, the number of technical members shall not exceed the judicial members.

Hence, it may be concluded that sec. 109(9) may further be revisited by government and suitable amendment be proposed to ensure that in case any point(s) is referred to third member, the same should be judicial member only.

[i] Till the time of writing this article date of effect of such amendments are yet to be notified.

Author Bio