Dr. Sanjiv Agarwal

GST Council met for the 34th time since its constitution yesterday (19th March, 2019) for taking crucial decisions on real estate sector. Taking forward the discussions and decisions of 33rd GST Council meeting dated 24.02.2019 GSTC has now taken important decisions in relation to levy of GST on real estate sector including manner of transition to new lower tax regime w.e.f. April 1, 2019.

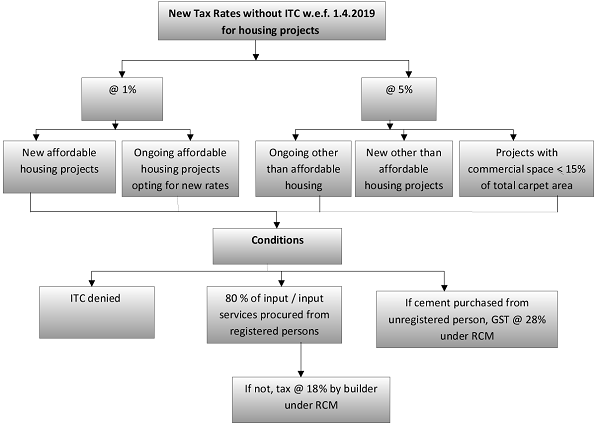

As already announced, GST on affordable housing shall be @ 1% and on other than affordable housing @ 5%. The ongoing projects will have an one-time option to continue under old scheme with ITC or switch over to new one without ITC. The time limit for transition will be discussed with states. However, reversal of ITC will have to be done in proportion to area or space. In the new scheme, 80% of the materials shall be procured from registered dealers except for capital goods, development rights, leases premium etc. This is a stringent condition as on shortfall of purchases from 80%, builders shall be liable to pay GST @ 18% under reverse charge mechanism. In case of cement purchased from unregistered supplier, GST shall be levied @ 28% under reverse charge method. Relief has also been granted to commercial apartments (shops, offices etc) in any residential project for lower GST rate of 5% where carpet area of such commercial space is not more than 15% of the total carpet area of all apartments. In case of Transfer of development rights, FSI and long term lease premium, burden of GST has been shifted to builder under reverse charge with time of supply to be determined on the basis of date of issue of completion certificate. The same time of supply would apply to JDA’s. In case of input tax credit, ITC rules shall be amended to have clarity and provide procedure for monthly and final determination of ITC and its reversal for real estate projects.

Salient features of decisions taken by the GST Council in the 34th meeting held on 19th March, 2019

Option for under construction projects

√ Under Construction projects as on 31st March, 2019 shall have an option to choose old rates (effective rate of 8% or 12% with ITC) with input tax credit or new rates without input tax credit.

√ If the option is not exercised within the prescribed time limit then new rates shall apply.

Conditions for the new tax rates:

√ Atleast 80% of the material to be procured from registered dealers. Further, on shortfall of purchases from 80%, tax shall be paid by the builder @ 18% on RCM basis.

√ However, Tax on cement purchased from unregistered person shall be paid @ 28% under RCM, and on capital goods under RCM at applicable rates.

√ Input tax credit shall not be available.

Applicability of new tax rates:

The new tax rates which shall be applicable as follows:

√ 1% without input tax credit (ITC) on construction of affordable houses shall be available for:

-

-

- Houses having area of 60 sqm in non- metros / 90 sqm in metros and value upto RS. 45 lakhs

- Under construction affordable houses presently eligible for concessional rate of 8% GST (after 1/3rdland abatement)

-

√ 5% without input tax credit shall be applicable on construction of:

-

-

- Under construction houses other than affordable houses presentlybooked prior to or after 01.04.2019. For houses booked prior to 01.04.2019, new rate shall be available on instalments payable on or after 01.04.2019.

- Commercial apartments having carpet area of not more than 15% of total carpet area of all apartments.

-

Transition for ongoing projects opting for the new tax rate:

√ Ongoing projects not been completed by 31.03.2019 shall transition the ITC in proportion to booking of the flat and invoicing done for the booked flat is available subject to a few safeguards.

√ For mixed project transition of ITC shall be allowed on pro-rata basis in proportion to carpet area of the commercial portion.

Treatment of TDR/ FSI and Long term lease for projects commencing after 01.04.2019

√ Supply of TDR, FSI, long term lease (premium) of land by a landowner to a developer shall be exempted with the condition constructed flats are sold before issuance of completion certificate and tax is paid on them.

√ Exemption can be withdrawn (limited to 1% of value in case of affordable houses and 5% of value in case of other than affordable houses) if flats sold after issue of completion certificate.

√ Builder shall be liable to pay tax on TDR, FSI, long term lease (premium) on the date of date of issue of completion certificate.

Election Commission of India has announced the schedule for general elections in India, i.e., from 10th April, 2019 in seven phases with counting taking place on 23rd May, 2019. This also indicates that GSTC may now not be able to take major tax reforms and other tax friendly measures in view of the embargo of election code of conduct. There will now be no meeting till General Elections over except emergency issues.

Author Bio

I have booked under construction 2BHK flat in Jan-2019 with token amount of which possession is in Dec-2021. Agreement of this flat is done by builder after 1st Apr 2019 and I received all demand letters after 1st Apr 2019 only. Builder has considered 12% GST; So, please advice which GST rates will be applicable for my flat – old or new?

I have booked a Flat for Rs.27,61,700/- plus applicable GST having Carpet Area-583 Sq.ft. & Saleable Area-921 Sq.ft. vide an agreement for sale and constructions of the flat dated 16/03/2018.

I have paid total amount of GST Rs.2,56,188/- & Rs. 3,504/- @12% & 1% on Rs.21,34,916/- and Rs. 3,50,434/- respectively as per prescribed Government rate.

Builder has send the final demand note for taking over the possession of flat with a demand note for Rs.2,79,110/- without passing benefit of Input GST credit.

Please suggest and provide the Govt.order if any.

I will be very thankful to you in this regards.

I am Mohammad Younus from (Nagpur) I have booked new flat on Dec -2018 with price Rs 19 L (non metro city), and the sale agreement also done on month Jan-2019, (At the time of booking non affordable GST rate are 5%/8%/12 %). Now also the flat under construction stage the builder will be complete the project end of July-20. (Now the builder is asking GST has pay 12% instead of 8% as per new govt rules). Kindly advice what is an actual GST I have to pay as on today to builder as a common person question.

I have booked flat in 2017 and GST was 12% but in 2019 it was revised to 1% but builder is charging 12% and on new sale it is 1% whereas property is Under construction and possession still not proposed. Is builder can charge different Rate of GST in one project.

i have bought a flat worth 27,00,000 with an area of 65.6 sq.m. Flat was booked in March 2017. Upto agreement in April 2018, i paid 11,00,000. Started a payment of 790000 (april 2018) and then 273000 (02.04.2019), 162000 (27.04.2019), 159000 (10.07.2019) and 159000 (23.09.2019), 84000 (is yet to be paid). what is the percentage of GST that i have to pay from April 2018? Paid already prior to that. Please help. possession is still not received

I have booked by flat on Jan-2018 and registration was done at the same time. In the cost sheet and in agreement builder has not mentioned how much ITC he is passing to buyer’s in number. He just mentioned that ITC benefit is reduced from agreement value and he is charging 12% GST. Now till now he has completed 3rd slab and all the demands were with 12 % of GST. My question here is as the GST rates are revised after 1 April-2019 for under construction property and now what would be the GST rate with the new demands after April 2019.. My property is in Pune (non-metro city) and agreement value is less than 45 lac with carpet area less than 90 SQ.Mtrs. Please advise

thank for sharing good content.

Hi Sir, I am planning to buy a villa in a new project which started in Jun 2019, total value 45 Lacs Carpet area 1610 sq ft, The builder is doing 2 agreements on Agreement of Sale for land 15 Lacs and agreement of construction 30 Lacs. He is charging GST on both @5%.

My question is whether GST would apply on 15 Lacs component???? Please advise

Whether builder can charge two rate of gst 5%&12%simultaneously on under construction same bldg.from april 2019 onwards in mumbai kidly reply at the earliest

Whether builder can charge two rate of gst 5%&12%simultaneously on under construction bldg.or only one rate in mumbai from april 2019 onwards?

I had booked a flat registration on Jan. 2019 and with 12% gst I and now project is completed now have to pay the remaining amount what Gst rate will be applicable for me 12% or 5% or 1% ?

Kindly give us proprietary Tax location : Palghar- state: Maharashtra

I had booked a flat on august 2017 and paid the booking amount with 12% gst after that I paid partial amount with 12% of GST and now project is completed now have to pay the remaining amount what Gst rate will be applicable for me 12% or 5% or 0% ?

I have booked a flat in Dec18 and paid 5% as token amount alongwith GST 6% (builder paid rest 6%). I did registration on Apr19. Now he had sent me his next demand with GST 6% instead on new GST i.e 5%. He says his architect had given him approval before Mar19 and hence I have to pay 6% GST. Please suggest if he correct

Sir, I have a query as per the amended GST Rates, 1% is applicable for 60 SQM and worth upto 45 Lacs in Metro and 90 SQM and worth upto 45 Lacs in Non – Metro…. and rest will be charged @ 5%

But if the case is like the carpet area is beyond the limits prescribed but the worth is less than the limit prescribed? … Say like the carpet area is 110 SQM and the worth of the flat is 40 Lacs in a metro area?

What is the GST Rate that will be leived?

what about resale property deals?

NICE DECISION GST RATE IS BIFURCATION NCE

In case of less than 80% purchases from registered dealers, the builder has to pay GST under reverse charge mechanism on shortfall amount or the entire procurement ?