Concept, Levy, Scope & Applicability

Concept, Levy, Scope & Applicability

We are pleased to share that we have launched Series ‘GST Simplified’ wherein we would attempt to explain nitty-gritty of GST in most lucid manner through write-ups, presentations and videos.

Series#1 explains ‘Concept, levy, scope & applicability of GST.

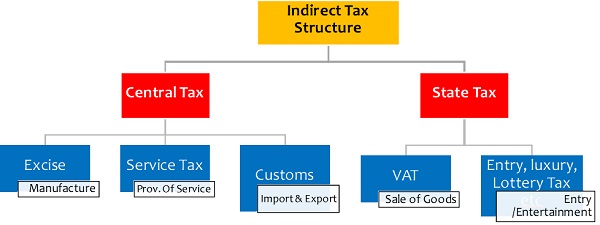

Before discussing GST, Let’s first understand the existing indirect tax structure and issues therein.

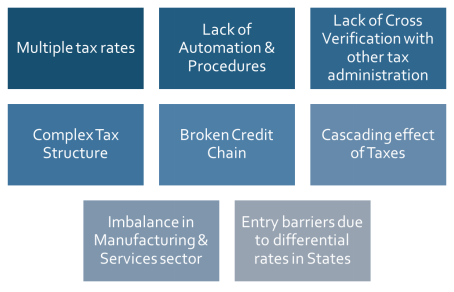

Current Indirect Tax Structure is grappled with following inherent imperfections:

GST has been an attempt to put an end to aforesaid challenges and that’s why is it quoted that ‘GST is not just a tax reform but a business reform’.

Let’s now understand how will GST mitigate current challenges and ride to the path of transparent tax structure.

Concept of GST

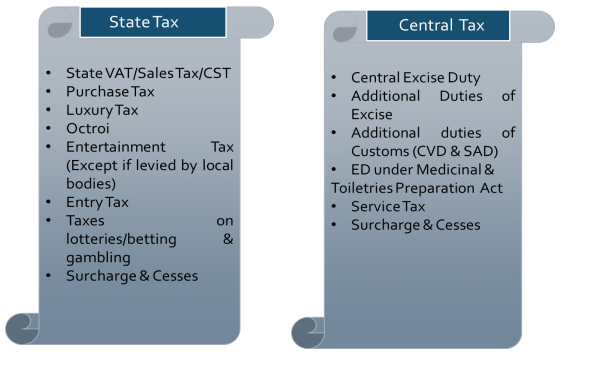

GST- Goods & Services Tax is multi-stage tax each point of supply of goods and/or services in India. It is nothing but a comprehensive tax which subsumes most of current indirect taxes levied by Centre as well State. It will be a two way structure wherein Centre will levy Central GST and State will levy State GST. Following are taxes to be replaced by GST:

Note: Basic Customs Duty shall continue to be levied on imports/exports.

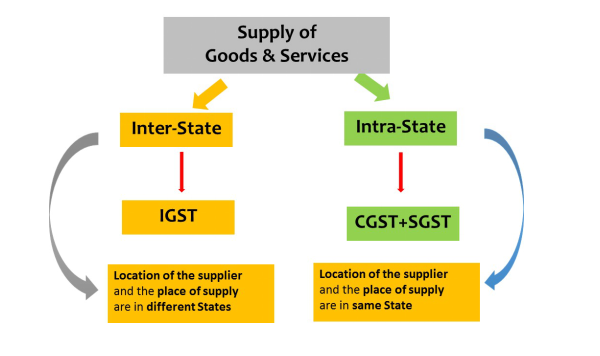

Supply of goods and /or services within the State will face CGST & SGST whereas, supply outside state will face IGST explained as under:

Constitutional Amendment

States and Central Government are empowered to levy tax under Article 246 of Constitution of India read with 7th Schedule comprising following 3 lists:

i. List I: Union List

ii. List II: State List

iii. List III: Concurrent List

As of now, State Governments cannot levy tax on supply of services and Centre cannot levy tax on sale of goods within the state. To pave the way for constitutionally valid GST law, new Article 246A has been incorporated to empower both Centre & States to levy tax on goods and services.

Why GST

Whether GST will prove to be Game Changer in Indian Economy in coming times, only time will tell. But we expect following benefits coming out on implementation of GST.

Will apply where ?

GST will apply to whole of India except J&K in its current form. There has been lot of debates and discussion on how J&K will come under legal framework of GST since J&K being Special State is having its own taxation powers and laws and do not follow Central Excise Duty/Service & VAT.

Will apply on which items ?

Indirect taxation law is moving towards negative list based regime wherein every item is taxable except if it is specifically kept out Following items are kept out of GST:

√ Electricity

√ Property transaction leviable to Stamp Duty / Property Taxes

√ Petroleum products* (excluded as of now)

√ Alcohol for human consumption

(*)Petroleum Products to include 5 items- petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel. These have been kept out as of now but might be included at later stage

GST on ‘Supply’

GST will apply on ‘Supply’ of goods and/or services in India. The word ‘Supply’ is quite wide in its scope. The same will be explained in detail in next series.

GST Council

From planning to formulation to structuring to implementation to operationalization, for every critical issue all states have been kept in loop by way of various meetings of Empowered Committee of State Finance Ministers. However, post necessary amendment in Constitution in respect of GST, this place has been replaced by GST Council. Model GST Law contains enabling provisions to the effect that critical aspects of GST like rates, exemptions, special provisions etc. will be firmed up on recommendation of GST Council. It has been done to ensure participative decision making and consensus amongst all states so that GST can be implemented across states with minimum deviations from Model GST Law. GST Council will comprise of representative from each State including Union Territories with partial State Hood and also Union Minister of State. The Council will be chaired by Finance Minister.

About Author: CA Nikhil M. Jhanwar is practicing Chartered Accountant in Delhi/NCR specialising in Indirect Tax, Start-up Advisory, Corporate Finance. He is also GST Faculty of ICAI. He can be reached as nmjhanwar@gmail.com/+91-8860876960.

Read Other Related Articles:-

Author Bio

Thanks all for kind appreciation, I will keep writing insightful posts…

Eagerly waiting for the second issue

Really… easily explained, informative and you have informed the crux of basic GST provisions….waiting for Series#2

Keep it up!!

sir, its Superb analysis ! To the point and well presented… please keep sharing !

Very nice and knowledgeable article. We are waiting next serious as early as possible.

Thanks

Very nice article and we are welcome to next article.

Nice and lucid presentation.

I like it.

Wating egarly for second issue.

Very nice artilce on GST.& ITS easy to understand

Dear Sir

I am also in finance profession brief about GST act

THIS IS MOST AWAITED SERIES

PLZ CONTINUE THIS SERIES ON DAILY BASIS SO WE CAN STUDY IT

Very nice & Informative Article……

We are welcome to this series………….

ITs really GST Simplified & proves its name,

we are Eagerrrrrrrrrrrrr for upcoming Series#2

With BEST Regards,

Nilesh Sonawane, Nashik , Maharashtra.