Introduction to GST- Section 63- Assessment of Unregistered Persons

-Section 63 of CGST Act, 2017 is applicable to unregistered persons i.e., persons who are liable to obtain registration under Section 22 and have failed to obtain registration, will come within scope of operation of this section.

-This provision also covers cases where registration was cancelled under section 29(2).

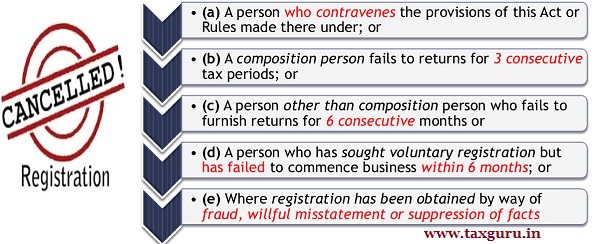

5 instances where GST registration may be cancelled by proper officer:

Uniqueness of Section -63 – Assessment of Unregistered Persons

- This is a remarkable provision where even when a taxable person is ‘unregistered’,

- Proper Officer is vested with jurisdiction to not only identify taxable transactions,

- But also pass an order of assessment on best judgment basis and fasten an enforceable demand.

- As in the case of section 62, this section 63 too contains a period of limitation of 5 years from due date applicable for filing annual return for the financial year to which tax not paid relates

Ingredients for section 63 to be attracted

♦ Taxable person

-All ingredients to establish a person to constitute ‘taxable person’ as per section 2(107) must be satisfied. In the absence of SCN, Proper Officer appears to come under great scrutiny for invoking this jurisdiction.

♦ Fails to obtain registration

– ‘Fail’ is not the same as ‘omits’ to obtain registration. Clearly, being conscious of the requirement to obtain registration will be required.

♦ Registration cancelled but liable to pay tax.

– It is not taxable person’s responsibility, If registration is cancelled by Proper officer as per section-29(2), and then proceeds to invoke Best Judgment order under section-63. It would be appropriate that proper officer “Suspends” registration instead of cancelling the registration.

Author Bio

If a person crossed threshold limit in the year 2018-19,later in the financial year 2019-20 he registered under gst.If it is possible to assessed under section 63 for the year 2018-19