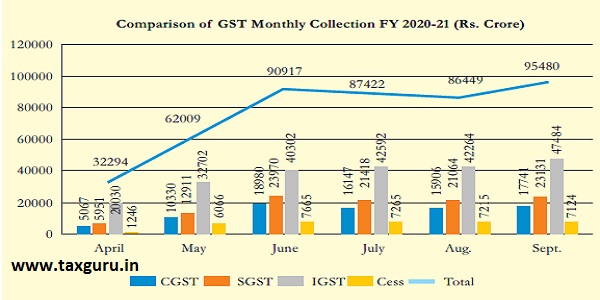

GST Revenue for September, 2020

In the month of September 2020, gross GST revenue was Rs. 95,480 crore, comprising CGST Rs. 17,741 crore, SGST Rs. 23,131 crore, IGST Rs. 47,484 crore (including Rs. 22,442 crore collected on import of goods) and Cess of Rs. 7,124 crore (including Rs. 788 crore collected on import of goods). The total revenue after regular settlement in this month was Rs. 39,001 crore for Central Government and Rs. 40,128 crore for State Government. The below chart shows the trends in GST monthly collection during the current financial year:

The revenues for the month of September 2020 are 4% higher than the same month last year. During the month, the revenues from import of goods were 102% and the revenues from domestic transaction (including import of services) were 105% from these sources during the same month last year. The State-wise GST collections during the month of September 2020, as compared to September 2019 (excluding GST on import of goods), has shown positive growth of 5%. From the above, it appears that major industrial states have shown a positive growth in GST collection, which indicates that, the economic recovery is on track.

Source: For April and May 2020 break up is compiled from Interactive Statistics available on www.gst.gov.in and for June to September 2020 is compiled from PIB press releases.

With the upcoming festive season in the months of October / November, there is all likelihood for a better recovery in GST collection.

Source: PIB Press Release, dated 01.10.2020

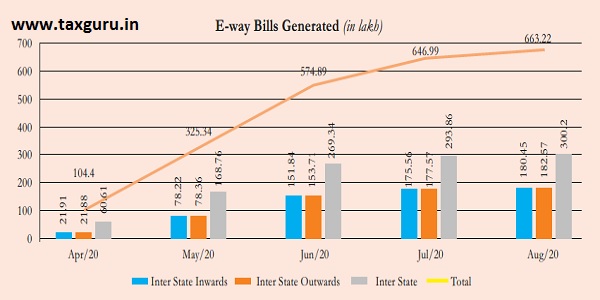

E-way bill

The number of e-way bills generated in August 2020 is 663 lakhs which is, 90% of the average number of e-way bills generated in pre-Covid-19 period (April 2019 to February 2020). This indicates affirmative signs of economic growth as the business activities are unlocking gradually despite the adverse impact of Covid-19. There are indicators of economic recovery. The month wise details of e-way bills generated during the current financial year are shown below:

Source: www.gst.gov.in/download/gststat_interactive

IGST Settlement

The Government has settled IGST in order to the settle the cross utilization of credits between Centre and States. The settlement of IGST with States and UTs for the Financial Year 2020-21 (upto August 2020) is as follows:

States / UTs-wise details of IGST Settlement during FY 2020-21

| Code | State | April | May | June | July | August |

| 1 | Jammu and Kashmir | 32.69 | 101.31 | 144.00 | 277.35 | 238.84 |

| 2 | Himachal Pradesh | 13.61 | 45.92 | 79.40 | 166.39 | 157.45 |

| 3 | Punjab | 54.34 | 273.36 | 361.60 | 613.75 | 530.12 |

| 4 | Chandigarh | 4.58 | 21.47 | 36.10 | 71.38 | 57.84 |

| 5 | Uttarakhand | 25.81 | 30.83 | 111.40 | 63.66 | 92.26 |

| 6 | Haryana | -15.77 | 345.25 | 521.70 | 667.01 | 513.17 |

| 7 | Delhi | 80.07 | 585.58 | 329.00 | 685.13 | 528.08 |

| 8 | Rajasthan | 113.55 | 332.77 | 539.00 | 905.99 | 852.97 |

| 9 | Uttar Pradesh | 318.24 | 990.99 | 1,218.20 | 2,320.86 | 1,838.22 |

| 10 | Bihar | 104.59 | 422.53 | 539.10 | 1,057.60 | 758.69 |

| 11 | Sikkim | 1.54 | 4.96 | 10.90 | 20.15 | 15.33 |

| 12 | Arunachal Pradesh | 8.41 | 18.39 | 23.20 | 44.32 | 31.11 |

| 13 | Nagaland | 6.68 | 14.19 | 23.50 | 38.00 | 29.27 |

| 14 | Manipur | 6.56 | 28.75 | 25.20 | 57.43 | 27.50 |

| 15 | Mizoram | 8.32 | 14.21 | 24.00 | 37.76 | 29.60 |

| 16 | Tripura | 4.21 | 23.85 | 35.20 | 70.68 | 46.27 |

| 17 | Meghalaya | 4.47 | 12.54 | 21.80 | 44.48 | 34.49 |

| 18 | Assam | 47.30 | 171.49 | 226.80 | 324.65 | 275.84 |

| 19 | West Bengal | 155.14 | 438.46 | 503.20 | 835.69 | 772.41 |

| 20 | Jharkhand | 44.14 | 108.36 | 154.30 | 228.39 | 236.40 |

| 21 | Odisha | 59.76 | 231.25 | 319.50 | 435.59 | 286.92 |

| 22 | Chhattisgarh | 92.83 | 136.49 | 77.10 | 175.60 | 122.46 |

| 23 | Madhya Pradesh | 101.97 | 360.83 | 455.20 | 1,011.53 | 785.55 |

| 24 | Gujarat | 35.96 | 491.26 | 357.40 | 613.87 | 396.57 |

| 25 | Daman and Diu | 1.41 | 6.18 | (1.50) | 2.87 | (3.45) |

| 26 | Dadra and Nagar Haveli | 11.14 | 4.6 | 5.60 | 2.59 | 6.57 |

| 27 | Maharashtra | -330.74 | 1085.29 | 1,339.40 | 2,113.70 | 1,258.26 |

| 29 | Karnataka | 264.53 | 724.82 | 960.80 | 1,616.12 | 1,389.08 |

| 30 | Goa | 6.21 | 30.62 | 58.00 | 57.15 | 45.88 |

| 31 | Lakshadweep | 0.54 | 1.09 | 0.80 | 1.81 | 1.68 |

| 32 | Kerala | 73.47 | 326.36 | 520.60 | 872.43 | 733.74 |

| 33 | Tamil Nadu | 150.29 | 745.62 | 890.10 | 1,294.72 | 663.69 |

| 34 | Puducherry | -0.13 | 12.02 | 17.50 | 31.49 | 25.53 |

| 35 | Andaman & Nicobar | 2.31 | 7.54 | 14.10 | 20.26 | 13.85 |

| 36 | Telangana | 197.55 | 363.62 | 572.30 | 950.94 | 982.15 |

| 37 | Andhra Pradesh | 144.48 | 366.73 | 546.90 | 1,025.14 | 827.38 |

| 38 | Ladakh | — | 1.59 | 2.80 | 16.19 | 9.41 |

| 97 | Other Territory | 3.02 | 39.25 | 52.50 | 65.11 | 39.01 |

| 99 | Center Jurisdiction | 1833.08 | — | — | — | — |

| Grand Total | 8920.41 | 11116.8 | 18,837.78 | 14,650.14 |

Source: www.gst.gov.in/download/gststatistics

The 37 GST Council meeting held on 20 September, 2019, has approved introduction of e-invoice in a phased manner. In the 39 GST Council Meeting held on 14 March, 2020, it is further recommended that certain classes of registered persons would be exempted from issuing e-invoices. As per Notification No. 60 & 61/2020-CT, dated 30.07.2020, it has been mandated for all taxpayers having annual aggregate turnover of above Rs. 500 Crore for their B2B transactions from 1 October, 2020.

Irrespective of the turnover, e-invoicing shall not be applicable to the following categories:

1. Supply by SEZ Units

2. Insurer or a banking company or a financial institution, including a NBFC;

3. Goods Transport Agency;

4. Registered persons supplying passenger transportation service; and

5. Registered persons supplying services by way of admission to exhibition of cinematograph films in multiplex screens.

E-invoicing

The registered persons have to follow the following procedure to generate e-invoices:

1. Form GST INV-01 is to be filled up, to be uploaded on Invoice Reference Portal (IRP) https://einvoice1.gst.gov.in/ and Invoice Reference Number (IRN) is to be obtained. Upon successful registration of invoice on IRP, it will return a signed e-invoice JSON to the supplier with IRN and QR Code. [Rule 48(4)]

2. A special provision has been done for the month of October 2020 that, the Invoice IRN for such invoices shall be obtained from the IRP within 30 days of date of invoice.

3. In case a registered person has issued an invoice dated 03-10-2020 without obtaining IRN but reports the details of such invoice to IRP and obtains the IRN of the invoice on or before 02.11.2020, then it shall be deemed that the provisions of rule 48(5) of the CGST Rules 2017 are complied.

4. The Quick Reference (QR) code having an embedded IR) is to be printed on the e-invoice. The QR code which comes as part of signed JSON from IRP, shall be extracted and printed on the invoice. (Source: FAQ No.59)

5. Once QR code is printed on e-invoice, no physical copy of this invoice will be required to be carried along with conveyance during movement. The QR code having an embedded IRN in it, may be produced electronically, for verification by the proper officer in lieu of the physical copy of such tax invoice.

6. A special provision for October 2020, the penalty leviable under section 122 of the CGST Act, 2017, for such non-adherence to provisions, shall stand waived if the IRN for such invoices is obtained from the IRP

within 30 days of date of invoice.

Sources: Notification 60, 61 & 70/2020-CT, dated 30.09.2020 & Notification No. 68, 69,70,71 and 72/2019-CT all dated 13.12.2019 and Press release dated 30.09.2020.

Amendment to GST Rules 2017 in relation to E-invoice

1. In Rule 46, a clause (r) has been inserted vide Notification No.72/2020-CT dated 30.09.2020 as “(r) Quick Reference (QR) code, having embedded Invoice Reference Number (IRN) in it, in case invoice has been issued in the manner prescribed under sub-rule (4) of rule 48.”

2. Once QR code is printed on e-invoice, no physical copy of this invoice will be required to be carried along with conveyance during movement. The QR code having an embedded IRN in it, may be produced electronically, for verification by the proper officer in lieu of the physical copy of such tax invoice.

3. In view of rule 48(4), the formulation of rule 138A (2) has been amended vide Notification No.72/2020-CT dated 30.09.2020 as “In case, invoice is issued in the manner prescribed under sub-rule (4) of rule 48, the QR code having an embedded IRN in it, may be produced electronically, for verification by the proper officer in lieu of the physical copy of such tax invoice.”

4. A Proviso has been added to Rule 48(4) vide Notification No. 72/2020-CT dated 30.09.2020 as “Provided that the Commissioner may, on the recommendations of the Council, by notification, exempt a person or a class of registered persons from issuance of invoice under this sub-rule for a specified period, subject to such conditions and restrictions as may be specified in the said notification.”

Sources: Notification 72/2020-CT, dated 30.09.2020

The Taxation and Other Laws (Relaxation & Amendment of Certain Provisions) Act, 2020

The Parliament passed “The Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020” replacing the Ordinance promulgated on 31.03.2020. The Act will provide for the extension of various time limits for completion or compliance of actions under the specified Acts and reduction in interest, waiver of penalty and prosecution for the delay in payment of certain taxes or levies during the specified period in the outbreak of Covid-19. Amendments made to the Central Goods and Services Tax Act, 2017 are as follows:

After section 168 of the CGST Act, 2017, the following section shall be inserted, namely:

168A. (1) Notwithstanding anything contained in this Act, the Government may, on the recommendations of the Council, by notification, extend the time limit specified in, or prescribed or notified under, this Act in respect of actions which cannot be completed of complied with due to force majeure.

(2) The power to issue notification under sub-section (1) shall include the power to give retrospective effect to such notification from a date not earlier than the date of commencement of this Act.

Explanation – For the purposes of this section, the expression “force majeure” means a case of war, epidemic, flood, drought, fire, cyclone, earthquake or any other calamity caused by nature or otherwise affecting the implementation of any of the provisions of this Act.

Source: The Gazette of India, published dated 29.09.2020

Administrative Instructions-Recovery of interest on net cash tax liability

The CBIC has issued instructions for recovery of interest on net cash tax liability under GST vide F. No. CBEC- 20/01/08/2019-GST dated 18.09.2020. Post issuance of Notification 63/2020 – CT, dated 25.08.2020, in order to implement the decision of the GST Council in its true spirit, and at the same time working within the present legal framework, the CBIC has issued the following instructions to its field formations:

2. For the period 01.07.2017 to 31.08.2020, field formations in your jurisdiction may be instructed to recover interest only on the net cash tax liability (i.e. that portion of the tax that has been paid by debiting the electronic cash ledger or is payable through cash ledger); and

b. Wherever SCNs have been issued on gross tax payable, the same may be kept in Call Book till the retrospective amendment in section 50 of the CGST Act is carried out.

Source: F. No. CBEC- 20/01/08/2019-GST, dated 18.09.2020

Notifications

Anti-Profiteering Seeks to amend Notification No. 35/2020-CT dated 03.04.2020 to extend due date of compliance under Section 171 of CGST Act, 2017 which falls during the period from “20.03.2020 to 29.11.2020” till 30.11.2020. Source: Notification No 65/2020, dated 21.09.2020

Goods removed on approval for sale or return

Vide Notification No. 66/2020-CT dated 21.09.2020 in respect of goods being sent or taken out of India on approval for sale or return which, falls during the period from the 20th March, 2020 to 30th October, 2020, and where completion or compliance of such action has not been made within such time, then, the time limit for completion or compliance of such action, is extended upto the 31st October, 2020.

Source: Notification No 66/2020, dated 21.09.2020

Relief to Composition Taxpayers in late fees for delayed filing Late fees in case of delayed filing of GSTR-4 for the period July 2017 to March 2019 has been waived off fully in case of NIL tax liability and restricted to Rs. 500 (Rs. 250 CGST + Rs. 250 SGST) per return in other cases if the taxpayer furnishes the said return between the period from 22th September, 2020 to 31st October, 2020.

Source: Notification No.67/2020, dated 21.09.2020

Late fee in filing Form GSTR-10

The Government has waived the late fee payable under Section 47 of the CGST Act, 2017 which is in excess of Rs.250, for the registered persons who fail to furnish the return in FORM GSTR-10 by the due date but furnishes the said return between the period from 22th September, 2020 to 31st December, 2020.

Source: Notification No 68/2020, dated 21.09.2020

Due date for furnishing Annual Return

The Government has extended due date for furnishing Annual Return in

Form GSTR-9 and GSTR 9C for FY 2018-19 from 30.09.2020 to 31.10.2020 by amending the earlier Notification No. 41/2020-CT, dated 05.05.2020.

Source: Notification No 69/2020, dated 30.09.2020

Implementation of QR Code on B2C invoices

Seeks to amend Notification No. 14/2020-CT, dated 21.03.2020 to extend the date of implementation of the Dynamic QR Code for 2C invoices till 1st December 2020.

Source: Notification No 71/2020, dated 30.09.2020

Exemption on two type transportation services

Seeks to amend Notification No. 12/2017-CT (Rate), dated 28.06.2017 to extend exemptions on supply services by way of transportation of goods by an aircraft from customs station of clearance in India to a place outside India and services by way of transportation of goods by a vessel from customs station of clearance in India to a place outside India under CGST Act till 30.09.2021. Similar changes made in the IGST Act, 2017 and UTGST Act, 2017 by amending Notification No. 9/2017-Integrated Tax (Rate) dated 28.06.2017 and Notification No. 12/2017-Union Territory Tax (Rate) dated 28.06.2017 respectively.

Source: Notification No. 04/2020-Central Tax (Rate), Notification No. 04/2020-Integrated Tax (Rate), and Notification No. 04/2020-Union Territory Tax (Rate), all dated 30.09.2020

GST Portal updates

♦ Late fee – The facility to file Form GSTR-4 (Quarterly Return) and Form GSTR-10 with late fee relaxation as per Notification No. 67/2020 and Notification No. 68/2020 dated 21.09.2020 is now available on GST Portal.

Updated on 23.09.2020

♦ Changes in navigation – The functionality “Comparison of liability declared and ITC claimed” has been removed from ‘Return Dashboard’ and made available on the main page, under the ‘Services’ tab.

Updated on 23.09.2020

♦ Compare ITC with purchase register – An offline tool has been made available to the taxpayers to match ITC, as auto populated in Form GSTR-2B, with their purchase register. This tool will help them to claim correct ITC, while filing Form GSTR-3B.

Updated on 18.09.2020

♦ Delinking of Credit Note/Debit Note – The taxpayers have now been provided the following facilities on GST Portal:

- Report in their Form GSTR-1/GSTR-6, single credit note or debit note issued in respect of multiple invoices

- Choose the note supply type as Regular, SEZ, DE, Export etc., to identify the table to which such credit note or debit note pertains

- Indicate Place of Supply (POS) against each credit note or debit note, to identify the supply type i.e. Intra-State or Inter-State

- Debit /Credit Notes can be declared with tax amount, but without any taxable value also i.e. if credit note or debit note is issued for difference in tax rate only, then note value can be reported as ‘Zero’. Only tax amount will have to be entered in such cases.

- Similar changes have been made while reporting amendments to credit note or debit note

- Corresponding changes have also been made in refund module. Updated on 17.09.2020

♦ E-invoicing – The following updates/information are made available on GST Portal:

- FAQs on e-invoicing, awareness videos.

- Obligation to issue e-invoice in terms of Rule 48(4) lies with concerned taxpayer.

- All the taxpayers who were having aggregate annual turnover of above Rs. 500 Cr. were enabled by default on e-invoice portal.

- Mobile app is also available for verification of authenticity of e-invoice (QR code/IRN).

- The E-Commerce Operators (ECO) have also been enabled to register and test the APIs on the sandbox system.

Updated on 12.09.2020 and 16.09.2020

♦ System computed values – A pdf statement has been made available to taxpayers, filing monthly GSTR-1 statement, with system computed values of Table 3 of Form GSTR-3B.

Updated on 05.09.2020

♦ TCS facility and Amendment in Form GSTR-8 – TCS facility is now extended for composition taxpayers also. The provision to make multiple amendments in Table 4 of Form GSTR-8 is now available on GST portal.

Updated on 01.09.2020

♦ Filing of GSTR-4 by Composition Taxpayers – With effect from 1 st April, 2019, all composition taxpayers are required to file Form GSTR-4 (Annual Return), this facility is now available on GST portal.

Updated on 01.09.2020

Source:www.gst.gov.in/newsandupdates

*****

Source- http://www.gstcouncil.gov.in