GST implementation brings several issues to the fore viz., determination of the revenue neutral rate, consensus on the divisible pool of resources, sharing the benefits of cesses, the administrative edifice and the technological platform. A dispute prevention mechanism would facilitate a smooth transition to the GST. The evolution in central transfers and evolving fiscal federalism will have a key bearing on the health of state finances over the medium term.

1. Introduction

4.1 In India, taxes on goods and services levied by the Central and state/ local governments are subject to different sets of rates, procedures and compliance. The existing legal framework for these indirect taxes pose several challenges, viz.,

(i) multiplicity of rates; (ii) cascading effect of taxes; (iii) excessive compliance/procedures; and (iv) fractured flow of import credits. A single goods and services tax (GST) is best suited to overcome these challenges.

4.2 Notwithstanding several benefits, the implementation of GST may involve several issues which have been debated in policy circles in recent years. Primary among them is the issue of the revenue neutral rate – the rate which would ensure that the migration to the proposed GST would not entail any revenue shortfall for the Center and states from the current level. In order to achieve this goal, rates have to be appropriately set, exemplifying the true spirit of fiscal federalism in which revenues are equitably shared by the Center and states. Nevertheless, the levy of cess by the Center on several goods and services is a contentious issue as revenues from cesses are not shareable. For the effective

implementation of GST, a comprehensive and effective dispute resolution mechanism is necessary along with a robust technological infrastructure. Furthermore, an efficient administrative arrangement can ensure seamless coordination among all stakeholders and facilitate smooth transition to a GST regime. This chapter delves into these issues with a view to providing a narrative around the evolving legislative and policy developments relating to the GST. From a medium term policy perspective, central transfers and debt sustainability of states warrants careful scrutiny as they are going to shape the contours of state finances in the years ahead.

2. Debate on the Revenue Neutral Rate

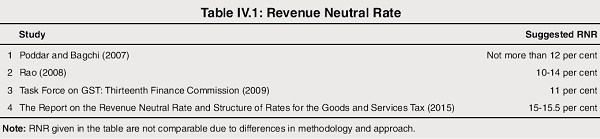

4.3 The rationale for implementation of the GST is to reform the in-built inefficiencies in the prevalent tax structure. One of the most debated issue in GST implementation has been the appropriate level of the “revenue neutral rate (RNR)”. According to the Report on the Revenue Neutral Rate and Structure of Rates for the Goods and Services Tax (GST), (2015) (Chairman: Arvind Subramanian), “RNR refer to a single rate, which preserves revenue at desired (current) levels” 1 . The RNR is different from the “Standard Rate” which is defined as the rate applicable on goods and services whose taxation is not clearly stated2 . Along with other factors such as administrative simplicity, inflation neutrality, compliance friendliness and lower tax burden for the public, the RNR is an indicator of the success of the new tax system (i.e., GST). Nevertheless, there is no clarity on whether a precise RNR exists (Box IV.1). This is primarily due to growth uncertainties and its impact on different industries/sectors which impinges on tax revenue.

4.4 Studies have indicated different RNRs,based on various methodology/assumptions (Table IV.1). One of the earliest studies in the Indian context concluded that if the GST is to be levied on a comprehensive base, the combined Center- state revenue-neutral rate (RNR) need not be more than 12 per cent (Poddar and Bagchi, 2007). This rate would apply to all goods and services with the exception of motor fuels, which would continue to attract a supplementary levy to maintain the total revenue yield at their current levels. A study based on 2003-04 all-India input-output matrices undertook two approaches to arrive at GST rates; i.e., GDP-based estimates and a private final consumption-based approach (Rao, 2008). On the former basis, a 10 per cent GST rate was estimated as adequate to raise the revenues required to replace central value added tax (CENVAT) and service tax at the central level, and sales tax, passenger and goods tax, electricity duty and entertainment tax at the state level. Based on the latter approach, the required GST rate was estimated at about 14 per cent3 . The study concluded that improvement in the tax regime and tax administration would ensure the same revenues through a lower GST rate (Rao, 2008).

Box IV.1:

Can there be an Optimal Rate for Taxing Commodities

The issue of the ideal or the optimal way to tax commodities has been of keen interest among economists for a long time. In the early half of the twentieth century, a Cambridge mathematical economist posed the following problem: suppose a government has a target amount of tax revenues to mobilize and that it can only tax commodities. In this situation, what is the optimal design of the tax structure? The solution is that commodity taxes on all the goods should be set in a manner such that there is a proportional drop in demand along the compensated demand curve for each of the commodities (Ramsey, 1927).

Does this imply proportional taxation? Not ordinarily, although it can be shown that uniform or proportional taxation would hold if either of the following conditions prevails: (i) preferences are homothetic and the utility function is separable between consumption and labor; and (ii) labor supply is completely inelastic (Sandmo, 1976). From a policy perspective, the issue of uniformity of commodity taxes has been a matter of substantial and special interest. The theoretical justification for uniform commodity taxes in the form of VAT must ultimately be traced to some restriction on consumer preferences or the formal properties of the labor supply function.

In a more general treatment of the optimal tax problem incorporating optimum income and commodity taxes, there is a realization that there are limits to the redistributive powers of indirect or commodity taxes and the overall result seems to be that commodity taxes may be set at uniform rates and any correction for vertical equity or distributive justice ought to be achieved via making direct taxes (income tax) suitably progressive (Atkinson and Stiglitz, 1980; Nygard and Revesz, 2017).

In the Indian context, the debate on RNR has highlighted a serious concern about the revenue mobilization capacity of the proposed GST which has to yield more than the combined revenue of the present Central excise and all the state level sales taxes. Any major shortfall would cause a serious dent on the public finances of both the Center and states; therefore, the projected GST rate/rates have to be suitably calibrated. In this regard, the GST Council has settled for a 4-tier structure set at 5, 12, 18 and 28 per cent which would reflect purely revenue concerns. It, perhaps, is also indicative that there can be no single optimal rate for taxing commodities.

References

(i) Atkinson, A B and J E Stiglitz (1980): Lectures on Public Economics, McGraw-Hill.

(ii) Nygard, O E and J T Revesz (2017): A literature review on optimal indirect taxation and the uniformity debate, Review of Public Economics.

(iii) Sandmo, A. (1976): Optimal taxation – an introduction to the literature, Journal of Public Economics 6, 37-54.

(iv) Ramsey, F. (1927): A contribution to the theory of taxation, Economic Journal 37, 47-61.

4.5 The report of the Task Force on Goods and Services Tax (2009), (Chairman: Arbind Modi), which was set up by the Thirteenth Finance Commission (FC-XIII), estimated RNR to be 11 per cent exclusive of revenue gains from increased tax compliance and higher GDP. In actual practice, therefore, the RNR of 11 per cent is not revenue neutral – it may actually increase total revenue. The report also recommended that formula based devolution (based on State Finance Commission recommendations) of an amount equivalent to collection of state GST (SGST) at 2 percentage points should be made to the local bodies such as municipal corporations (as GST will lead to abolition of all entry and octroi taxes by state and other sub-national governments).

4.6 The Subramanian Committee (2015), cautioned that it is difficult to posit one single number as the appropriate rate with any degree of confidence. Therefore, it recommended that the RNR be in a range of 15 to 15.5 per cent, with a strong preference for the lower end of the range. Even so, it will still place India at relatively higher than many of its emerging market peers – a higher rate implying greater regressivity. Countries that have well-developed social safety nets can better offset this regressivity. It is argued that a higher rate in the initial stages of implementation may reduce tax compliance and increase dissatisfaction, besides being inflationary. Accordingly, a lower rate will be more prudent in terms of wider acceptability, ensuring better tax compliance.

4.7 A related issue is the revenue potential of the Center and its capability to provide adequate compensation to the states. If revenues fall short and the fiscal position of both the Center and states are affected, the Center runs the risk of having to compensate the states which would be an additional burden on Central finances. Furthermore, multiple rates may be a problem as low rates on some goods have to be balanced through higher rates on other goods to ensure overall revenue neutrality; this will enhance the scope of tax evasion, besides posing administrative difficulties. The GST Council has settled for a four-tier structure in the range of 5-28 per cent based on revenue considerations which is broadly consistent with the RNR of 15-15.5 per cent. Although the details of commodities in each tax bracket is yet to be decided by the GST Council, it is expected that food and other necessary items would be taxed at the lowest rate with some of them being exempted fully. This would minimize the regressive burden of the tax.

3. Dispute Resolution Mechanism and IT Infrastructure

4.8 Tax disputes often arise due to differences in the interpretation of the taxation law by the tax imposing authority and the tax payers. Hence, all efforts should be made to simplify tax laws to avoid ambiguity ensuring effective and timely settlement through a dispute resolution mechanism – a prerequisite for the overall efficiency of tax administration and a conductive business environment. Under the GST, multiple parties such as the Centre, states, and tax payers would be involved and the possibility of such disputes arising cannot be ignored. Disagreement may arise at several levels – between the Center and states; between states; and between tax payers and tax authorities – regarding (i) the need of filing appeals at two places under GST (at the state level for SGST and at the Centre for CGST); and (ii) where to file appeal – in the state in which production occurs or where they are consumed (Joshi et al, 2016).

4.9 Initially, states were apprehensive that the GST dispute settlement authority (previously proposed under article 279B) would circumscribe the fiscal powers of the Center and states. Hence, this provision has been done away with and a new provision has been made in Article 279A itself, empowering the GST Council to decide about the modalities of dispute resolution4 . The GST Council may decide modalities of the redressal mechanism; for example, a retired judge could oversee the resolution panel for legal issues, while other experts could be considered for non-legal issues. The GST Council would take decisions through a three-fourth majority – the Center will have one-third voting rights while the states will have the remaining two-third, based on a formula under which no party is in a disadvantageous position. Transparency in rules and procedures, easy availability of information, and cooperation among the relevant parties may help in dispute prevention even as outreach by tax authorities and guidance in filing returns may go a long way in minimizing cases of disputes. This would minimize recourse to dispute settlement procedures.

Box IV.2:

Goods and Services Tax Network (GSTN)

In view of the sensitivity of information at the disposal of GSTN, the Empowered Group recommended that the Government retains strategic control over GSTN through measures such as (i) control over the composition of the Board; (ii) mechanisms of special resolution and shareholders agreement; (iii) induction of Government officers on deputation; and (iv) agreements between GSTN and governments. The shareholding pattern would ensure that the Centre (individually) and states (collectively) are the largest stakeholders at 24.5 per cent each. Together, the Government shareholding at 49 per cent would far exceed that of any single private institution. After roll out of the GST, the revenue model of GSTN would consist of user charge to be paid by all stakeholders. Thus, it is envisaged to be a self-sustaining and financially viable entity.

The common GST portal developed by GSTN will function as the front-end of the overall GST IT eco-system. The IT systems of central board of excise and customs (CBEC) and state tax departments will function as the back-office that would handle tax administration functions such as registration approval, assessment, audit, and adjudication. A common and shared IT infrastructure for taxpayers will handle registration applications, filing of returns, creation of challans for tax payment, settlement of IGST payments (like a clearing house) and generation of business intelligence and analytics. In this regard. about 70 per cent of the existing registrants have already migrated to the GSTN system.

GSTN has selected 34 IT, IT enabled services and financial technology companies , to be called GST Suvidha Providers (GSPs), who would develop applications for taxpayers interacting with the GSTN. In this context, the GST portal will prepare a summary of all payment confirmations received by it from banks every day and share the same with the RBI and accounting authorities for reconciliation. No tax money will come to GSTN; it will only get confirmation of payment from banks.

References

http://www.gstn.org

http://www.cbec.gov.in

4.10 The success of GST and effective dispute prevention depends on creation of a sound information technology (IT)

infrastructure. In this regard, the goods and services tax network (GSTN) – a nongovernment private limited company – has been set up under erstwhile Section 25 of the Companies Act, 1956 primarily to establish a uniform interface for the tax payer through a common and shared IT infrastructure between the Centre and states that enables processing and exchange of information amongst all stakeholders, viz., tax payers, Central and state governments, accounting offices, banks and the RBI (Box IV.2). In this regard, GSTN would be developing back-end IT modules for states who have opted for it .

4. Administrative Control of GST

4.11 After implementation of GST, there will be one CGST law, 31 SGST laws for each of the states including two Union Territories with legislature, one UTGST for Union Territories without legislature and one IGST law governing inter-state supplies of goods and services. CGST, UTGST and IGST will be administered by the Centre, while the SGST will be managed by the respective state governments. Both Centre and states will simultaneously levy GST across goods and services. CGST and IGST will be administered by the Central Board of Excise and Customs (CBEC) and the SGST will be administered by the State Commercial Tax Departments of the respective state governments. Furthermore, after enactment of GST, the apex indirect tax body CBEC will be re-named as the Central Board of Indirect Tax and Customs (CBIC) which will implement the rules, including exemptions and threshold, to be set by the GST Council.

4.12 The dual GST is proposed in view of the federal structure in India defining taxation jurisdiction of the Centre and states. In order to address the issue of dual control over assessees, the GST Council has approved the division of audit and assessment responsibility between the Central and state governments. State authorities would control 90 per cent of the assessees with annual turnover of less than `1.5 crore, while the Centre will control the remaining 10 per cent. Assessees with a turnover above `1.5 crore will be administratively controlled by the Centre and states in equal measure. It has been opined, however, that there should be an option to divide the entire tax base vertically wherein the taxpayers are divided between the Centre and the states in a fixed proportion.

4.13 The fitment of goods and services in the various agreed slab rates is an important issue. In this regard, the GST Council has decided on a four-slab structure, as mentioned earlier, along with a cess on luxury and `sin’ goods such as tobacco. States have been given the powers to levy tax on economic activity within 12 nautical miles of coastal territory. It is proposed to have a common registration and common portal for filing of returns for Central and state tax administrations.

4.14 In order to ensure rollout of the GST on the scheduled timeline of July 1, 2017, the GST Council is actively engaged in resolving administrative and structural issues. On April 06, 2017, the Parliament passed four supplementary GST laws viz. the Central Goods and Services Tax Bill (CGST), the Integrated Goods and Services Tax Bill (IGST), the Goods and Services Tax (Compensation to States) Bill and the Union Territory Goods and Services Tax Bill (UTGST). These will now be presented before the President for his consent following which all states will pass another legislation viz. the State Goods and Services Tax Bill (SGST). As on May 01, 2017, 5 states viz, Telangana, Bihar, Rajasthan, Jharkhand and Chhattisgarh have passed their SGST Act with other states expected to follow shortly.

5. Fiscal Federalism and GST

4.15 Fiscal federalism deals with the division of governmental functions and financial relations among various levels of government within a federal structure (Musgrave, 1959). As a subfield of public economics, fiscal federalism is concerned with understanding which functions and instruments are best centralised and which are best placed in the sphere of decentralised levels of government (Oates, 1999). From an operational perspective, it consists of the division of responsibilities in respect of taxation and public expenditure between the Centre and state governments. In a federal setup, fiscal transfers are effected through tax devolutions and grants, often supplemented by loans from the Centre to the states. In line with the practice followed in other countries with federal structures, fiscal transfers in India are guided by the principle of ‘equalisation’, which neutralises insufficiency in fiscal capacity (but not revenue effort) across states. Therefore, the objective of fiscal transfers is to correct vertical and horizontal imbalances (Rao and Singh, 2005) – the former referring to the simultaneous imbalance between means and responsibilities in two different tiers of governments because states bear expenditure responsibilities disproportionate to their sources of revenue (Rangarajan and Srivastava, 2011); and the latter pertaining to differences in resource capabilities/uniformities between states.

4.16 Under the current system of transfers in India, tax devolution plays a dual role of correcting vertical as well as horizontal imbalances while grants-in-aid are primarily targeted towards achieving a degree of equalisation among states. In recognition of problems relating to vertical and horizontal imbalances, the Constitution of India has made several provisions to bridge the resource gap between the Centre and the states. They include Article 268, which facilitates levy of duties by the Centre but equips the states to collect and retain the same. Similarly, Articles 269, 270, 275, 282 and 293 define ways and means of sharing resources between the Centre and states. Apart from the abovementioned provisions, Article 280 provides an institutional framework to facilitate Centre-state transfers in the form of Finance Commissions (FC) which determines the share of states in tax revenues of the Centre. FC recommendations are required to address the vertical imbalance between the Centre and state governments as well as the horizontal imbalance among states. There are other constitutional and institutional arrangements for transfer of resources from the Centre to states such as through the budget and making provisions for fiscal transfers and borrowings to strengthen Centre-state financial relations.

4.17 Regarding financial relations between the Centre and states, the Seventh Schedule (Article 246) of the Indian Constitution lays down the respective fiscal powers and functional responsibilities following the principles of federal finance under three categories viz., the Union List, the State List and the Concurrent List. 5 The concurrent list is the one in which both the Centre and states can make legislations; however, federal laws prevail in case of a conflict or tie.

4.18 The Centre has been given exclusive powers to levy taxes and collect revenue which are divided between the Centre and states. State governments have freedom to decide the amount of taxation which are levied, collected and retained by them although the tax rates tend to differ among states. The major taxes which state governments can levy and collect revenue are Sales Tax/VAT, entry tax/octroi duty, stamp duties and registration fees, profession tax, land revenue, agricultural income tax (see Chapter III) and the like.

Impact of GST

4.19 The GST is drawing out a new course for fiscal federalism in India focusing on cooperation. After its enactment, tax powers may overlap and the Centre and states Will have to agree on GST rates. The GST will subsume taxes levied by the Centre, states and local bodies; therefore, the fiscal capability of local bodies may be affected after implementation of GST.

4.20 The state of vertical imbalances would depend on the pattern and the rate of the GST that will be put in place under the dual rate regime. Therefore, the GST rates should be determined taking into account the present level of revenues of the two-tiered tax structure so as to ensure that the fiscal imbalance does not increase (Rangarajan and Srivastava, 2011).

4.21 In the context of varying rates of taxes across states, the GST endeavours to simplify the tax regime. To the extent, however, that it leads to disagreement between states and between the Centre and the states, it may defeat the spirit of fiscal federalism. Moreover, any single state may have to go with the collective decision even if it is in disagreement with the views of the Council.

4.22 It has been argued on the one hand that GST would lead to loss of fiscal autonomy for states as it would curb their ability to alter tax rates. States would forfeit their right to levy new taxes, or change the existing tax rate or give exemptions to any class of goods or services. On the other hand, with well-defined areas for the application of Central GST (CGST), State GST (SGST) and integrated GST (IGST) to avoid conflict and given the proposed dual-tier structure, the GST is expected to promote cooperative federalism while reducing competitive federalism. Both Parliament and state assemblies have power to make laws on taxation of goods and services, while the GST Council will settle inter-state or Centre-state disputes by consensus. Furthermore, states are free to levy VAT on sale of petroleum and crude products until a decision is taken by the GST Council. The assignment of concurrent jurisdiction to the Centre and the states for the levy of the GST would, therefore, require an institutional mechanism that would ensure joint decisions about the structure, design and operation.

6. Central Transfers to States

4.23 In a federal structure, a widely debated issue is the transfer of resources from Centre to states. Vertical and horizontal imbalances are common features of a federal structure and India is no exception. Central Government transfers have played a significant role in bridging the resource gap between states expenditure commitments and their own resources for funding such expenditure. Although both own revenue and central transfers to states have increased in the past few years, the increase has been significant in the case of the latter (Table IV.2).6

4.24 States have been seeking an increase in the share of central taxes citing a number of reasons viz., (i) reduction in the size of the divisible pool due to increase in the scope of cesses and surcharges; (ii) declining shares of state plan outlays; and (iii) increasing expenditure needs of states in areas such as infrastructure development, social and human development, environmental protection and pay revisions. 7 The FC-XIV attempted to address these issues and made major recommendations in the area of Centre-state transfers. In order to improve the vertical distribution, the Commission recommended a compositional shift in transfers from grants to tax devolution to meet the twin objectives of increasing the flow of unconditional transfers to the states and yet leave appropriate fiscal space for the Union. While the share of tax devolution has increased from 32 per cent to 42 per cent of the divisible pool, sector-specific Finance Commission grants are dispensed with.

4.25 The FC-XIV has also dealt with interstate devolution to mitigate the impact of the differences in fiscal capacity and cost disability among states through horizontal distribution. It has removed the distinction between non-special category and special category states and assigned weights to different indicators, viz., population (17.5 per cent); income distance (50.0 per cent); area (15.0 per cent); the newly introduced criteria of demographic change (10 per cent); and forest cover (7.5 per cent). It recommended post-devolution revenue deficit grants for states where devolution alone could not cover the assessed gap.

4.26 The Union Budget 2015-16 has implemented some of the major recommendations of FC-XIV, viz, (i) increasing the states’ share in tax devolution of the divisible pool, as stated earlier, thereby increasing the flow of unconditional transfers to states; and (ii) modifying the Centre-state funding pattern of some of the centrally sponsored schemes (CSS), in view of the larger tax devolution to the states. The CSS have been recently grouped into three categories viz., (i) schemes which will be fully supported by the Centre, (ii) schemes which will run with changed sharing pattern, and (iii) schemes which will be delinked. These changes have resulted in a major shift in Centre-state financing pattern.

Recent Trends in Central Transfer to States

4.27 Central transfers, which have been declining since 2011-12, increased sharply in 2014-15. This change, both in magnitude and direction, needs to be seen from the perspective of two policy changes which affected the transfer of resources to states. First, transfer of funds under CSS prior to 2014-15 was effected through the dual mode of a) state budgets; and b) direct transfer to district rural development agencies and independent societies. In this regard, state governments had expressed their concern that direct transfers to the implementing agencies circumvented state budgets, thereby diluting the responsibilities of the states in ensuring proper utilisation of funds. To address this issue, the entire financial assistance to the states for CSS is routed through the consolidated funds of the states since 2014- 15 under the category ‘central assistance to state/union territory (UT) plans’ (RBI, 2015). As a result, the consolidated funds of states has recorded a significant increase in central transfers. Second, the increase in states’ share in the divisible pool of taxes to 42 per cent from 2015-16 onwards has changed the composition of central transfers in favour of statutory transfers, as against discretionary transfers made earlier. It has also led to greater predictability and certainty in the quantum of funds being transferred to the states. The transition to GST may further change the landscape of central transfers to states. In this regard, the proposed compensation clause for revenue losses on account of introduction of GST may add an element of certainty to state governments’ revenue.

7. Implications of Special Levies

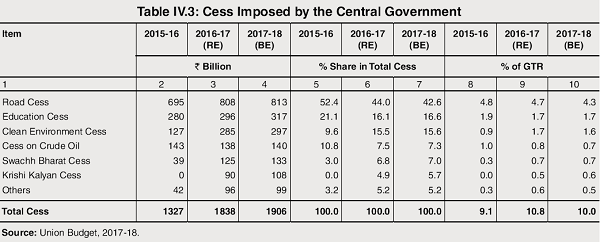

4.28 Over the years, there has been a proliferation of special levies – generally used to finance specific programmes for a finite time period – viz., cess, surcharge and other additional/special duties that the Central Government has resorted to within the ambit of additional revenue mobilisation (ARM) measures. Consequently the amount of tax revenue raised by the Central Government through special levies has increased sharply in the recent period. The share of special levies in the Central Government’s gross tax revenue (GTR) has increased rapidly from 8.8 per cent in 2012-13 to 15.2 per cent in 2016-17, mainly reflecting the impact of the imposition of two new cesses, viz., Swachh Bharat cess and Krishi Kalyan cess in the Union Budget of 2015-16 and 2016-17, respectively.

4.29 At present, the Central Government imposes more than 20 cesses but it mobilises the maximum revenue through additional duty on excise on motor spirit and high speed diesel – popularly known as the road cess – which is used for development and maintenance of national highways/other roads and railway crossings. In addition, there are a number of other cesses imposed on excise duty on crude oil, bidi, sugar, automobiles, coal, salt, rubber, mica, iron ore, lime stone and dolomite, research and development and the like. Overall, the share of cess in the Central Government’s gross tax revenue (GTR) has increased from 6.7 per cent in 2013-14 to 10.8 per cent in 2016-17 (Table IV.3).

Issues and Perspectives

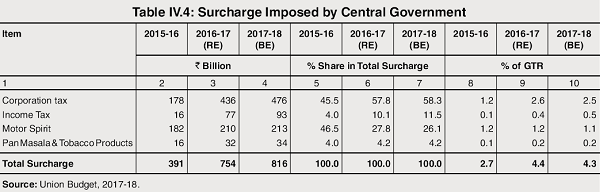

4.30 Besides cess, the Centre has imposed a surcharge of 10 per cent on tax payable for individual assessees in the ` 50 lakh-1 crore income bracket in the Union Budget 2017-18 while continuing with the existing surcharge of 15 per cent on assessees withincome higher than ` 1 crore, and a surcharge ranging between 2 per cent and 12 per cent on companies with total income of more than ` 1 crore. The share of surcharge in the Central Government’s GTR has increased from 2.5 per cent in 2013-14 to 4.4 per cent in 2016-17 (Table IV.4).

Implications for States

4.31 Despite increasing use of special levies, the benefits do not percolate down to state governments as special levies are not part of the divisible pool of taxes. Thus, the total divisible tax pool for states (as proportion to total tax revenue) has actually shrunk. Consequently, despite a sharp jump in the share of states in the divisible pool of resources from 32 per cent to 42 per cent from 2015-16 following the FC-XIV recommendations, the states’ share in the Centre’s GTR has de facto increased from 27.1 per cent in 2014-15 to 34.8 per cent in 2015-16 (Table IV.5).

4.32 In effect, such levies bring back the issue of vertical fiscal imbalance. While the Centre continues to get the larger share of revenues, the states make the bulk of disbursements, which is essentially contrary to the spirit of cooperative federalism. Although the Centre has been claiming that the enhanced share of states in tax revenues will allow them greater fiscal space even at the cost of lower revenue to support its own programmes and schemes, this has been sought to be offset by increasing the reliance on cesses and surcharges. It has simultaneously reduced the fiscal space for states by curtailing the total central assistance for state plans. Over the years, states have naturally been arguing against cesses, suggesting that either they be completely eliminated or, if continued beyond a specified period, should form a part of the divisible pool.

Implications for GST

4.33 The GST Council has finalised a fourtier GST structure. While the GST Council has decided that all the existing cesses would be subsumed under the GST except the clean energy cess levied on coal, it proposes to levy a cess on ultra-luxury goods (viz., high end cars) and demerit goods (viz., tobacco, pan masala, aerated drinks). Accordingly, luxury and de-merit goods will attract tax at 28 per cent as well as a cess. The GST Council has capped the proposed cess on aerated drinks and luxury automobiles at 15 per cent, pan masala at 135 per cent and cigarettes at 290 per cent. The cess would be used to create a Compensation Fund to help the states that sustain any loss of revenue due to introduction of the GST. In particular, states will be given full compensation for any shortfall in revenue on the basis of a formula that entails a secular revenue growth of 14 per cent for tax revenue of states (with 2015-16 as the base year) over the five years of compensation period. The cess will have a sunset clause of 5 years. It will be reviewed on a yearly basis and any surplus in the Fund will be distributed among the states. The GST Council will review the taxation structure once the cess is withdrawn.

4.34 Since most of the cesses will be subsumed into the GST, it will increase the size of the divisible pool of resources to the advantage of the states. Introduction of a new cess on luxury and demerit goods may be contrary to the spirit of the GST but the proceeds would be used to compensate the states; thus, the impact of GST would be beneficial overall. Nonetheless, from the point of view of implementation, it could be argued that GST is imposed on consumption while cess, which is typically applied at the stage of manufacturing, may be difficult to administer and could also lead to cascading effects.

8. Concluding Observations

4.35 The implementation of GST would be the single most important tax reform undertaken since the onset of economic reforms with far reaching fiscal consequences for the federal structure of the Indian government. In this regard, the key issue is the determination of the revenue neutral rate which would ensure that the Centre and states would not incur any loss of revenue post-GST implementation. While states are expected to forego fiscal autonomy in the levying of new taxes, changing the existing tax rate or giving tax exemptions with the implementation of the GST, it is expected to promote cooperative federalism and reduce competitive federalism.

4.36 Nevertheless, the amount of tax revenue raised by the Central Government in the recent period through special levies, the benefits of which are not shared with state governments, brings to the fore the issue of vertical fiscal imbalance. In the way ahead, thorny issues on implementation are sought to be addressed through a robust dispute resolution mechanism while GSTN would provide the necessary IT infrastructure to all stakeholders. Finally, the administrative arrangements of GST roll out have to be seamlessly coordinated among all stakeholders. From a medium-term perspective, greater devolution of resources to states would provide the flexibility to priorities their expenditure in sync with their development objectives. In this regard, the shift towards statutory transfers have led to an increase in untied funds at the disposal of states. Prudent choices of policies in public finances will help the states in realizing their developmental objectives and would also keep them solvent over the medium term.

Way Forward

5.1 The fiscal position of state governments in India improved significantly since 2004- 05 after the implementation of fiscal rules through the enactment of Fiscal Responsibility and Budget Management (FRBM) Acts / Fiscal Responsibility Legislation (FRLs) and introduction of debt and interest relief measures by the Central Government. These initiatives were also supported by a favorable macroeconomic environment following the high growth phase and a reversal of the interest rate cycle in the mid-2000s.

5.2 In the recent period, particularly during the last couple of years, signs of fiscal stress have re-emerged on the back

of poor performance of state public sector enterprises (SPSEs). The recent initiative by several state governments of assuming additional debt liabilities as part of financial and operational restructuring of state power distribution companies (through issuance of UDAY bonds) has led to deterioration in fiscal health of states. This has been reflected in the worsening of key fiscal indicators. It is expected that states will take necessary steps to renew their efforts towards fiscal consolidation and reduce their liabilities.

5.3 The Central Government accepted the recommendations of the Fourteenth Finance Commission (FC-XIV) to increase the states’ share in the divisible pool of taxes to 42 per cent (earlier 32 per cent) from 2015- 16 on wards. This did lead to greater predictability and certainty in the quantum of funds being transferred to the states; additionally, there has been an overall increase in untied funds. As a result, the share of states in central taxes increased by 1.1 percentage points of GDP in 2015-16 (RE) over the previous year. The increasing use of special levies (viz., cess, surcharge and other additional/special duties) by the Central Government, however, resulted in a reduction in the divisible pool of taxes as these levies are not shared with state governments, although they did boost the Central Government’s tax revenue. As a result, despite increase in the share of states in the divisible pool of resources from 2015-16 by 10 per cent following the FC-XIV’s recommendation, the states’ share in Centre’s gross tax revenue has de facto increased by only 7.7 per cent – from 27.1 per cent in 2014-15 to 34.8 per cent in 2015-16. It is expected that most of the cesses will be subsumed in the GST, which will increase the size of the divisible pool of resources to the advantage of the states.

5.4 While conventional debt sustainability analysis reveals that state governments’ debt is sustainable in the long run, several related developments which have a bearing on the debt/fiscal sustainability of states over the medium term need to be taken into account for a balanced assessment. First, the guarantee commitments of state governments in respect of SPSEs have recently emerged as a major source of potential risk to debt sustainability. Unbridled growth in these guarantees constitutes a major fiscal risk given the SPSEs large outstanding debt and losses (particularly those in the power sector) (IMF, 2016; Kaur et al., 2014). Second, the interest liabilities of states that have participated in financial restructuring of DISCOMs (through UDAY) would increase, going forward. Moreover, additional provisions are required to be made by the state governments for extending financial support to these utilities in case they continue to incur losses in future. Third, the committed liabilities of states may increase in case they decide to implement the recommendations of their own pay commissions in 2017-18. Since their own tax revenue is inadequate to finance the additional burden, states may take recourse to market borrowing for additional funds, with implications for debt sustainability. Fourth, many states (particularly the fiscally prudent ones), which were earlier refraining from seeking additional funds through market borrowing, may now borrow as per the criteria of additional borrowing indicated by the FC-XIV.

5.5 Yet another dimension is the ad hoc nature of various types of loan waivers announced from time to time by state

governments. Such initiatives could add to their fiscal burden and affect their finances over the medium term. While these loan waivers could alleviate the immediate debt burden of financially distressed farmers, it is essentially a transfer from tax payers to borrowers with an adverse bearing on the fiscal viability of states. Moreover, it impacts credit discipline, vitiates credit culture and dis-incentivizes borrowers from repayment, thus engendering moral hazard with expectations of future bailouts. Furthermore, if overall government borrowings increase, as is likely due to issuance of debt relief bonds by state governments, yields on state development loans (SDL) may firm up posing a higher interest burden in the future. Concomitantly, it can also crowd out private borrowers, given the finite pool of investible resources in the economy.

5.6 The consolidated GFD-GSDP ratio of25 states is budgeted at 2.6 per cent for 2017-18, lower than the Central Government’s budgeted gross fiscal deficit to GDP ratio at 3.2 per cent. Even as the Central Government makes significant efforts toward fiscal consolidation, the accumulation of liabilities could result in higher debt burden of the states unless immediate steps are taken to contain them. A rising general government debt-GDP ratio is also detrimental from a sovereign rating perspective. The recently released FRBM Review Committee Report, 2017 (Chairman: N. K. Singh) has recommended that a sustainable debt path must be the principle macro-economic anchor of fiscal policy, consisting of 40 per cent of debt-GDP ratio for the Central Government and 20 per cent for state governments by 2022-23. The states will have to considerably tighten their finances to reach this benchmark, given that their outstanding liabilities to GDP ratio stood at 23.9 per cent at end-March 2017.

5.7 In this context, introduction of the GST is expected to have significant macroeconomic implications in terms of growth, inflation, export competitiveness and the fiscal balance in the years ahead. The successful implementation of GST will result in additional revenue through simpler and easier tax administration, supported by robust and user-friendly IT systems. The GST is expected to reduce administrative costs for collection of tax revenue and improve revenue efficiency. Moreover, uniformity in tax rates and procedures across the country will economize on compliance cost. It will also lead to increase in the shareable pool of resources, resulting in larger central transfer to the states which, in turn, will enable them to undertake much needed developmental expenditure. Such an outcome would ensure debt sustainability for states in the long term. In fact, the GST is likely to set a new course for cooperative federalism in India by strengthening Centrestate partnership.

1. In practice, there will be a structure of rates but for the sake of clarity it is appropriate to think of a single rate.

2. The Subramanian Committee (2015) had discussed about three approaches to arrive at RNR – the macro, indirect tax turnover (ITT) and the direct tax turnover approaches.

3. Along with this rate, 10 per cent non-rebatable excises on passenger cars and multi-utility vehicles, petroleum products and tobacco products, would help in realising the revenue target.

4. Report of the Select Committee on the Constitution (One Hundred and Twenty-Second Amendment) Bill, 2014, Parliament of India.

5. The Union List contains items of national importance (eg. defence, railway etc.), the State List contains items of state and local interest (eg. public health, agriculture etc.) while the Concurrent List contains items having mutual jurisdiction of the Center and states on areas on mutual interest (eg. education, forest etc.).

6. Central Government transfers to states comprise of tax devolution and grants.

7. The ratio of net additional expenditure on account of pay revision between the Center and states is 1:1.49 indicating higher net additional liability on account of pay revision for states (FC XIII).

Source- RBI