The GST is likely to roll out on July 1, 2017. Given the cross-country experience and empirical evidence on efficiency gains from the Value Added Tax (VAT) in the Indian context, we conjecture that implementation of GST is likely to ensure higher tax buoyancy and an improvement in government finances over the medium term.

1. Introduction

3.1 The goods and services tax (GST) Bill was passed unanimously in the Parliament in August, 2016 reflecting cooperative fiscal federalism in the pursuit of reforms. After ratification by a majority of states and assent of the President, it was enacted as Constitution (One Hundred and First Amendment) Act, 20161.The GST is the largest tax reform in India, paving the way for a single national market by merging several central and state taxes2. It is also expected to make Indian products more competitive in both domestic and international markets and also attract large inflows of foreign direct investment than before in view of the stability it will impart to the tax regime. At the same time, it will be transparent and easier to administer. Thus, the GST has the potential to raise India’s growth trajectory over the medium-term.

3.2 The concept of the GST is not new to India. Earlier in 2005, value added tax (VAT) was introduced on the recommendation of the Report of the Indirect Taxation Enquiry Committee, 1978 (Chairman: L. K. Jha). The VAT proved to be inherently efficient relative to the sales tax or excise duty or any turnover tax as it minimized tax evasion with an in-built mechanism of multi-stage tax distribution and a cross-auditing practice.

3.3 The introduction of the GST is likely to have an enduring impact on state finances over the medium term for several reasons. First, with states being unable to rationalize their committed expenditure burden (viz., pension liabilities, interest obligations and administrative expenses) in the near term, revenue expansion through GST implementation is a prudent strategy in remaining committed to the path of fiscal consolidation. Second, the GST is likely to chart out a new course for cooperative federalism in India focusing on cooperation between the Centre and states in deciding on (i) tax rates, (ii) exemptions and (iii) commodities featuring in each category of tax rate/slab. Finally, GST implementation may result in augmenting the shareable pool of resources which would result in greater transfer of resources from the Center to the states. Cumulatively, these issues are likely to have a profound impact on state finances in the coming years (see Chapter IV for detailed discussion on each of these issues).

3.4 Against this backdrop, the rest of this chapter is organized into five sections. Section 2 explores the concept of GST and its advantages. Section 3 draws out the key lessons from a cross-country perspective. Section 4 sketches the evolution of GST– from ideas to legislation; the challenges and modalities of implementation. The experience of Indian states with regard to the VAT are empirically explored in Section 5. Concluding observations on the macroeconomic implications of the GST are set out in Section 6.

2. The Concept

3.5 The GST is a destination-based single tax on the supply of goods and services from the manufacturer to the consumer3 and is one indirect tax for the entire country. GST will replace multiple taxes such as central value added tax (CENVAT), central sales tax, state sales tax and octroi (Table III.1). A common base and common rates across goods and services and similar rates across states and between Center and states will facilitate better tax administration, improve tax compliance, alleviate cascading or double taxation while also ensuring adequate tax collection from inter-state sales.4

3.6 While the VAT is imposed at different stages of production of goods and services, the GST is levied at the national level on consumption of goods and services (Table III.2). Credits of input taxes paid at each stage will be available in subsequent stages of value addition, which makes GST essentially a tax on value addition at each stage. The final consumer will thus bear only the GST charged by the last dealer in the supply chain with set-off benefits against all previous stages. Consequently the benefits of GST are manifold spanning across business, government and the consumer (Box III.1).

Table III.1 : Taxes subsumed under GST

|

Central level |

State level |

| 1. Central Excise Duty

2. Duties of Excise (Medicinal and Toilet Preparations) 3. Additional Excise Duty 4. Service Tax 5. Additional Customs Duty commonly known as Countervailing Duty 6. Special Additional Duty of Customs 7. Cesses and surcharges in so far as they relate to supply of goods or services

|

1. State Value Added Tax

2. Entertainment Tax (other than the tax levied by the local bodies) 3. Central Sales Tax (levied by the Centre and collected by the States) 4. Octroi and Entry tax 5. Purchase Tax 6. Luxury tax 7. Taxes on lottery, betting and gambling 8 Taxes on advertisements 9. State Cesses and surcharges in so far as they relate to supply of goods and service |

Note: GST would apply to all goods and services (including tobacco and tobacco products), except Alcohol for human consumption. GST on five specified petroleum products (Crude, Petrol, Diesel, Aviation Turbine Fuel & Natural gas) would be applicable from a date to be recommended by the GST Council.

Table III.2: VAT and GST

| Major Features | Present VAT | Proposed GST | |

| 1 | Structure | Structure of VAT in different states differ; VAT rates also differ. | A dual tax with both Central GST and state GST will be levied on the same base. GST to have four rates. |

| 2 | Cascading effect | CENVAT and VAT have not yet been extended to include the chain of value addition and thus the benefits of a comprehensive input tax and service tax set-off remains out of the reach of manufacturers/dealers. | The introduction of GST will not only include more indirect Central taxes and integrate goods and services taxes for set-off relief, but will also capture value addition in distributive trade and a continuous chain of set-off from the original producer’s and service provider’s point upto the retailer’s level. This would eliminate the burden of all cascading effects. Also, major Central and state taxes will get subsumed into the GST, reducing the multiplicity of taxes. |

| 3 | Coverage | Relatively narrow base and separate service tax. | Wider base and applied on both goods and services. GST is a consumption based tax which will be collected by the states where the goods or services are actually consumed. |

| 4 | Procedures for collection of tax | It varies from state to state. | Likely to be uniform throughout the country. |

| 5 | Tax Administration | Complex due to number of taxes. | Intention is to make it simple, easy and tax-payer friendly. |

| 6 | Use of Information Technology | Not much. | Completely IT-based. Its success to a great extent will depend on IT for which the goods and services tax network (GSTN) – a separate company has been formed. |

Box III.1:

What GST implies for various economic agents

(i) Business

- Easy compliance: a robust and comprehensive information technology (IT) platform and seamless transfer of input tax credit from one stage to another in the value chain would incentivise tax compliance.

- Uniformity of rates and structure: GST will ensure that tax rates and structure are common across the country, thereby increasing certainty and ease of doing

- Removal of cascading: seamless tax credits throughout the value-chain and across states would ensure minimal cascading of taxes, thus reducing hidden costs of doing

- Reducing compliance cost: The uniformity in tax rates and procedures across the country will economize on compliance cost.

- Gain to manufacturers and exporters: the subsuming of major taxes in GST and reduction in transaction costs would lower the cost of locally manufactured goods and services and increase India’s export competitiveness.

(ii) Government

- Improve tax administration: with a robust user-friendly IT system in the form of the Goods and Services Tax Network (GSTN) portal, GST would be simpler and easier to administer.

- Higher revenue: GST is expected to reduce the cost of collection of tax revenues and improve revenue buoyancy.

(iii) Consumer

- Single and transparent tax: there would be only one tax from the manufacturer to the consumer leading to greater tax transparency.

- Relief from tax burden: efficiency gains and prevention of leakages will benefit consumers with a reduction in the overall tax burden estimated to be around 25-30 per cent.

3. The Cross Country Experience

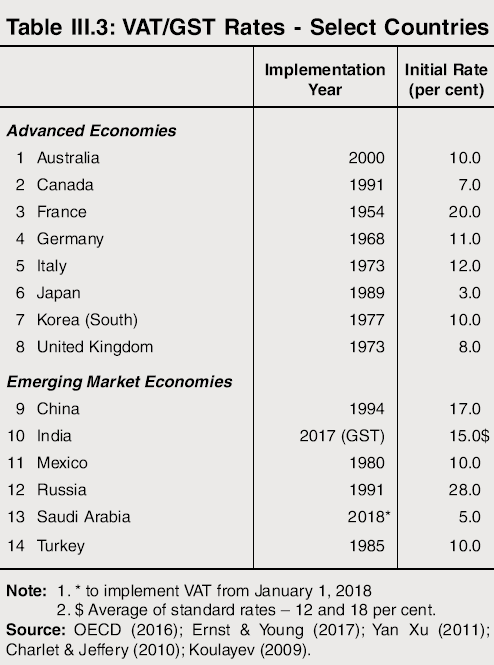

3.7 VAT/GST has been introduced over several decades, with France being the earliest entrant (Table III.3). Today, 160 countries have some form of VAT/GST, with the United States being a prominent absentee from this list. There are different models of VAT/GST currently in place. Singapore taxes virtually everything at a single rate, while many countries (France, Italy, UK) have multiple rates. In some countries (e.g., UK), a reduced rate on necessary items is applied with basic goods being exempted to minimize the regressive impact of the tax (Zhou, etal, 2013).

3.8 In most countries, introduction of the VAT/GST has been preceded by prolonged deliberations about its relative merits and demerits with fixing of the optimal rate being the most contentious issue (IMF, 2015b). GST rates vary widely among countries – the average VAT/GST rate in major OECD countries is higher than the rate proposed for India and those prevailing among other EMEs in 2016 (Chart III.1).

3.9 Diverse motives have been cited for the introduction of the VAT/GST, although the common element seems to be that of reforming the existing tax system and simplifying the tax structure. In this regard, a robust federal structure of government is particularly helpful for ensuring success of such reforms – Brazil, India and Canada being prominent examples. Discussion on tax reform to simplify federal and state indirect taxes is underway in Brazil with a proposal to

introduce a single integrated national VAT on both goods and services. India’s plan to have central GST (CGST) and state GST (SGST) has some resemblance to the structure of the system existing in the Canadian province of Quebec where independent federal (GST) and provincial (QST) VATs are operative simultaneously (Bird and Gendron, 1998).

3.10 A robust and fail-proof information technology (IT) framework is regarded as an essential prerequisite for the success of the GST, given the large volume of transactions involved. Besides, sensitising industry and public through information dissemination such as release of legislative documents and conducting outreach programmes/media interactions with the tax authorities are also critical. Furthermore, tax laws need to be simplified to avoid definitional issues and defray administrative costs. Drawing on lessons in the implementation experience of countries, a well-designed GST should ensure that (i) a single rate is levied on a comprehensive base (goods and services); (ii) no exemptions are given beyond standard ones; (iii) GST refunds are processed expeditiously; (iv) an adequate threshold is delineated to exclude small and micro business; and (v) initial rates are suitably calibrated to avoid disruptions to economic activity and macroeconomic stability (IMF, 2015b).

3.11 Notwithstanding the merits of GST implementation, international experience points out some likely risk relating to tax evasion and avoidance. These are (i) small businesses may not register; (ii) a trader may under-report actual sales; (iii) traders may reduce their liability by exaggerating the proportion in the lower tax slabs; (iv) tax authorities need to guard against traders who collected tax but were not remitted to the government; and (v) traders may make false claims for refunds (IMF 2015b).

3.12 It is perceived that by anchoring revenue to a more stable source, i.e., consumption, the government can have a credible plan to strengthen public finances which, in turn, would boost investor confidence in the economy and sustain growth (Zhou et al, 2013) especially if the introduction of the GST is supplemented by structural reforms (Bolton & Dollery, 2005; IMF, 2015b). Although the precise impact is difficult to measure accurately, average growth increased by about 0.7 percentage point following fiscal (including tax) reforms in some advanced economies (Danforth et al, 2015). As it promotes competitiveness, efficiency gains from GST is considered to be higher vis-a-vis other taxes, the benefits of which accrues to growth over the medium-term (IMF, 2006). In the short term, however, it may result in lower growth as households adjust their consumption after GST implementation. The evidence also suggests that implementation of GST may be inflationary under specific circumstances (Box III.2).

3.13 From a fiscal perspective, international evidence suggests that implementation of VAT/ GST have resulted in a higher government revenue-GDP ratio over time. An earlier study concluded that the tax-GDP ratio increased significantly after VAT implementation in twelve European countries (Aaron, 1981). Moreover, OECD data on member countries from Europe suggest an increase of 37 per cent in the VAT revenues-GDP ratio between 1975 and 2006 (OECD, 2008). While an increasing VAT revenue-GDP ratio is not necessarily correlated with a rising government spending- GDP ratio, critics have argued that an indirect (less visible) VAT may support higher levels of government spending compared to the use of direct taxes (eg. income tax) which are more visible (Carroll et al, 2010).

Box III.2:

Impact on Inflation

Cross country evidence suggests that the impact on inflation due to the introduction of a VAT/GST is not uniform. While the introduction of a VAT in UK resulted in no major impact on inflation, Canada experienced inflation pressures after introduction of the GST (Gelardi, 2014). One of the reason which might have helped UK escape inflation pressures is that the VAT replaced a concealed consumption tax; however, this contention is not supported by evidence from Canada where the GST replaced the manufacturer’s sales tax. In fact, inflation in Canada did not have any impact from the GST rate reductions of 2006 (7 to 6 per cent) and again in 2008 (to 5 per cent) which may be attributed to Canadian provinces being able to impose their own sales tax (Gelardi, 2014).

Singapore witnessed a sharp rise in inflation soon after introduction of the GST, mirroring the experience of many other countries. Malaysia was able to mitigate this risk as the price rise on account of GST was moderated by the Ministry of Domestic Trade and Consumer Affairs. Australia, and New Zealand saw one-off increases in inflation post GST implementation which normalized within a year. In Australia, GST had a significant but transitory impact on inflation with a lag of one quarter after its implementation in July 2000. During the quarter, inflation showed an average increase of 2.6 per cent which was on account of a spike in domestic consumption in the months prior to VAT/GST implementation as consumers purchased ahead of the new tax coming into effect. Domestic consumption and economic activity declined after VAT/GST implementation and resulted in the economy contracting during the first quarter of 2001, but returned to normalcy thereafter (Palil and Ibrahim, 2011).

From the British and German experiences, VAT/GST was found to be least disruptive in terms of inflation if introduced during a period of economic slowdown. In 1979, a wage price inflation spiral afflicted the British economy after VAT/GST was raised from 11 to 15 per cent as producers increased prices beyond what was necessary to cover the additional VAT/GST. In contrast, West Germany was able to minimize the inflationary impact by introducing VAT/GST during recession in 1968. All subsequent rate increases in Germany have since been successfully effected during periods of economic slack (Palil and Ibrahim, 2011).

In the context of 17 Euro zone countries, VAT pass-through to inflation during 1999 to 2013 were found to be sensitive to the type of VAT change and significantly different between durable and non-durable due to differences in storability and other features such as the salience of tax changes. For changes in the standard rate, the final pass through was about 100 per cent, while for reduced rates it was significantly lower at around 30 per cent (Benedek et al., 2015).

References

(i) Benedek, D., R. De Mooij, M. Keen, and P. Wingender (2015), “Estimating VAT Pass Through”, IMF Working Paper WP/15/214.

(ii) Gelardi, A. M. G (2014), “Value Added Tax and Inflation: A Graphical and Statistical Analysis”, Asian Journal of Finance & Accounting, Vol. 6, No. 1.

(iii) Palil, Mohd Rizal and Mohd Adha Ibrahim (2011), “The Impacts Of Goods And Services Tax (GST) On Middle Income Earners In Malaysia”, World Review of Business Research Vol. 1. No. 3. July.

Select Country Experiences

(i) New Zealand

The GST was introduced in 1986 as part of a comprehensive tax and welfare reform when the economy was in crisis. Initially, GST was introduced at a rate of 10 per cent which was subsequently raised to 12.5 per cent (1989) and further

to 15 per cent (2010) to mobilize higher revenue while removing distortions in the tax structure (IMF, 2015a). This eventually led to the adoption of GST at a single rate with almost no exemptions. Most notably, food was included in the GST base at the full rate, which broad-based the tax net and also reduced both compliance and administrative costs. With a standard rate lower than in most other OECD countries but without almost any exemptions, New Zealand is one of the highest tax productive nations (highest GST revenue GDP ratio) among the OECD countries (IMF, 2015a).

(ii) Canada

The GST was introduced in the form of a multi-level VAT in 1991 replacing manufacturers’ sales tax. GST was levied on supplies of goods or services purchased in Canada and included most products, except certain essentials such as groceries, residential rent, medical services, financial services and exports. The system of input tax credit ensures that the value added at each stage of the supply chain is taxed only once thus avoiding cascading. The introduction of GST led to new processing operations and techniques to verify the accuracy of the returns submitted by small entrepreneurs and multinational corporations (Sherman, 2009). Since some of the Canadian provinces impose their own sales tax besides the GST, it creates price distortions in the economy (IMF, 2015a).

(iii) Singapore

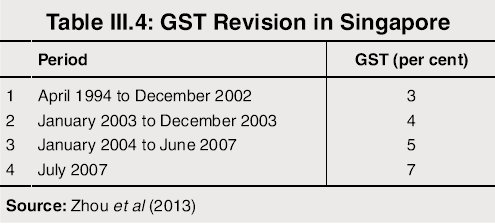

The GST was introduced in April 1994 at 3 per cent, along with a reduction of direct and other indirect taxes (Zhou, et al, 2013) to make it acceptable to the public and to minimize the inflation impact. Additionally, the government committed not to raise the tax for the next 5 years which was an important step in reviving consumer spending. Thereafter, rates were raised gradually, although it remains one of the lowest rate globally with favourable implications for trade competitiveness (Yin, 2003) (Table III.4). The motives for GST implementation were (i) broadening the indirect tax base; (ii) offsetting the loss in revenue as a result of the reduction in direct taxes; and (iii) making the tax base more resilient in the long term in view of an aging population (Zhou, et al, 2013). To compensate for the regressive nature of GST, Singapore has introduced a GST compensation scheme which provides support to the needy and underprivileged.

(iv) Australia

Although first mooted in 1975, GST was implemented in Australia 25 years later on July 1, 2000 through the passing of the Goods and Services Tax Act, 1999 (Zhou, et al, 2013). Australia imposed a 10 per cent tax on goods and services and replaced a range of existing taxes – the wholesale sales tax (WST), debit tax, financial institutions duty, and stamp duty on shares, leases, mortgages and cheques. The GST is collected by the federal government and redistributed to the six states and two territories according to the amount recommended by the Commonwealth Grants Commission (CGC) on the basis of the principle of horizontal fiscal equalization (HFE). The aim is to achieve equality in the provision of services and infrastructure; however, it often causes friction between the states when the GST revenue is divided (Zhou, et al, 2013). The effective veto that Australian states and the commonwealth enjoys makes any GST reform difficult to achieve (IMF, 2015a). In order to increase the acceptability of GST, Australia introduced a range of measures to soften the extra financial burden of GST. Several exemptions (viz., basic foods, some education and health services, childcare, and religious and charitable activities) and low standard GST rate at 10 per cent have, however, led to low GST revenue productivity from a tax collection standpoint (IMF, 2015a).

(v) Malaysia

One common reason for implementation of GST in both Singapore and Malaysia is the large expatriate work force in these countries who benefit from economic growth but are exempt from income tax. Furthermore, Malaysia’s shadow economy was estimated at 30 per cent which represents a vast scope for tax revenue (Zhou et al, 2013). Although the idea of introducing a consumption based GST has been on the table since 1989, it was introduced only in 2015 after intensive debate on its potential merits and shortcomings. Lingering doubts on the country’s preparedness for the introduction of GST led to some delay in its implementation even though the standard rate (at 6 per cent) is relatively low compared to the VAT rates in other ASEAN countries. After introduction of GST, the cost of doing business in Malaysia has reduced as the tax burden as been transferred from manufacturers to consumers. A generous list of exemptions and very low rates, however, lowers revenue productivity in terms of tax collection (IMF, 2015b).

4. The Indian Context – Overview and Status

3.14 The concept of the GST was first introduced by the report on “Reform of Domestic Trade Taxes in India: Issues and Options” (Chairman: A. Bagchi; 1994). 5 In fact, the VAT was adopted as a stop-gap arrangement for implementation of the GST in future. In 2000, the Government initiated discussions on the GST by constituting an Empowered Committee (Chairman: Dr Asim Dasgupta) with a mandate to design the GST model and oversee the IT back-end preparedness for its rollout. The Task Force on “Implementation of the Fiscal Responsibility and Budget Management Act, 2003” (Chairman: Vijay Kelkar) noted that although the indirect tax policy has been steadily progressing in the direction of VAT since 1986, the existing system of taxation of goods and services in India still suffers from many problems and suggested the introduction of a comprehensive GST based on the VAT principle.

3.15 In the Union Budget 2006-07, a proposal was made to introduce a national level GST by April 1, 2010. Since the proposal involved reform/restructuring of indirect taxes levied by the Centre and by the states, the responsibility of preparing a design and road map for the implementation of GST was assigned to the Empowered Committee (EC) of State Finance Ministers. In April, 2008, the EC submitted a report titled “A Model and Road map for Goods and Services Tax (GST) in India” and the first discussion paper on GST was presented by the EC of State Finance Ministers on November 10, 2009.

3.16 The Constitution (One Hundred and Fifteenth Amendment) Bill, 2011 was introduced in the Lok Sabha to enable the levy of GST; the Bill, however, lapsed with the dissolution of the 15th Lok Sabha. Subsequently, the Constitution (One Hundred and Twenty Second Amendment) Bill, 2014 was introduced in the Lok Sabha in December 2014 and passed in May 2015, finally culminating into an Act – the Constitution (One Hundred and First Amendment) Act, 2016 which, after receiving the assent of the President of India on September 8, 2016, will come into force once the Central Government notifies through the official gazette.

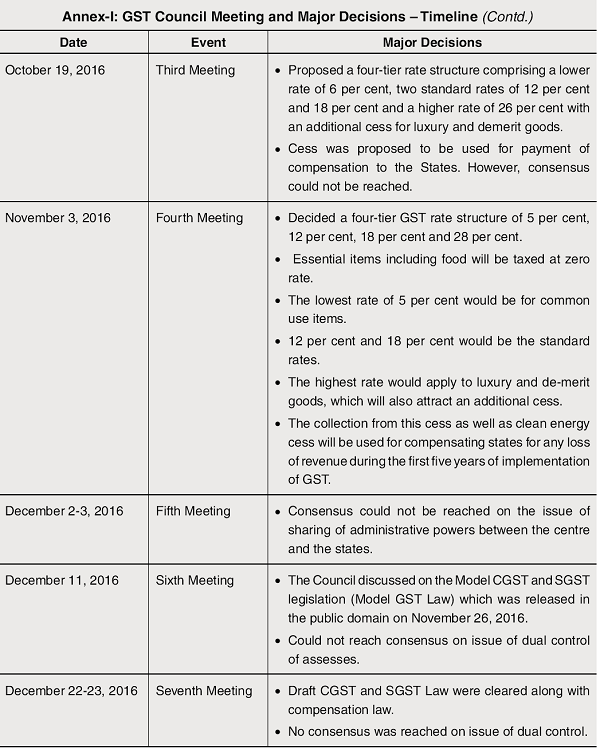

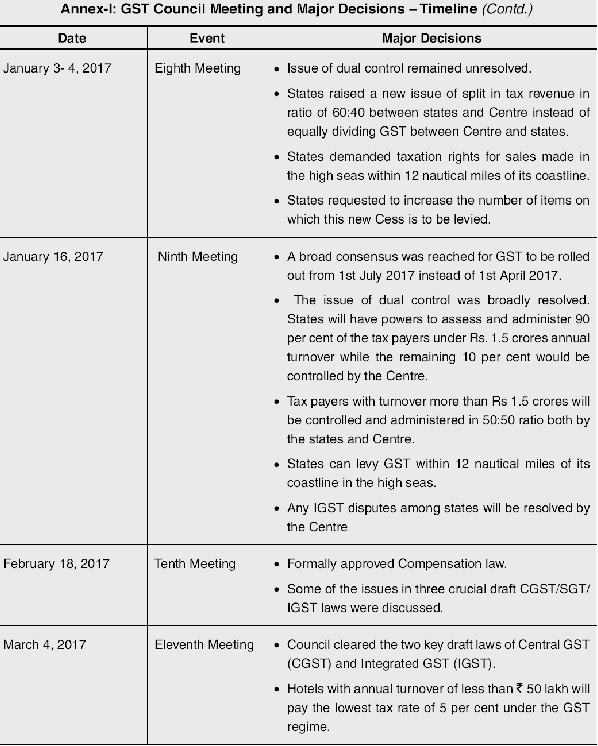

3.17 In compliance with Article 279A of the Constitution, the Union Cabinet constituted the GST Council and announced the formation of the GST Council Secretariat in its meeting of September 12, 2016. The GST Council is a joint forum comprising a) the Union Finance Minister as Chairperson; b) the Union Minister of State in-charge of Revenue as Member; c) the Minister in-charge of finance or taxation or any other Minister nominated by each state government as Members6 . In the Council, state government representatives enjoy two-third voting share while the remaining one-third is with the Central Government; decisions are to be taken with a three-fourth majority. The Council’s mandate include recommendations on (i) the goods and services that are subjected or exempted from GST; (ii) model GST Laws; (iii) principles that govern place of supply; (iv) threshold limits for exemptions; (iv) GST rates including the floor rates with bands; (v) special rates for raising additional resources during natural calamities/disasters; and (vi) special provisions for certain states. The GST Council held 13 meetings till March 31, 2017 (Annex-I).

3.18 Keeping in mind India’s federal structure, there will be one Central goods and services tax (CGST), 31 state goods and services tax (SGST) including two Union Territories with legislatures, one Union Territory goods and services tax (UTGST) without legislature, and one integrated goods and services tax (IGST) law governing inter-state supplies of goods and services. Both the Centre and states will simultaneously levy GST across the value chain on supply of goods and services. The Center would levy and collect CGST, while states would levy and collect SGST on all transactions within their geographical frontiers. The input tax credit under the CGST and the SGST would be available for discharging the liability on the output at each stage; however, no cross utilization of credit is permitted. The additional duty of excise/countervailing duty (CVD) and the special additional duty (SAD) currently being levied on imports will be subsumed under the GST. The IGST will be levied on all imports into the territory of India;states where imported goods are consumed will now gain from additional tax revenue (Box III.3).

Box III.3:

Integrated Goods and Services Tax (IGST)

The integrated goods and services tax (IGST) Act, 2017 applies to movements of goods and services from one state to another. It is not a separate tax but a sum of CGST and SGST. The major advantages of IGST model are (i) maintenance of uninterrupted input tax credit (ITC) chain on inter-state transactions; (ii) no upfront payment of tax or substantial blockage of funds for the inter-state seller or buyer; and (iii) no refund claim in exporting state as ITC is used up while paying the tax. It will facilitate the seamless flow of ITC across states as it is a destination based tax, i.e., the IGST amount will be apportioned between the Center and states although the power to levy and collect IGST lies with the Center to ensure that a single coordinating agency administers it.

Collections under the IGST are to be deposited into an IGST account administered by the Central Government and will be distributed between the Central Government and the consuming states on a mutually agreed formula epitomizing the spirit of cooperative federalism. The IGST will also apply to imports and exports of goods and services into/from India and any import/export of goods or services into/from Indian territory shall be deemed to be supply of goods and services as inter-state trade or commerce.

The IGST will be governed by the Central Government under the administrative control of CBEC. Although states also want to control the IGST mechanism, the Center is of the view that it should have sole administrative authority over IGST. By a special provision in the law, however, states can be empowered to collect IGST. In case of any dispute between states over the place of supply, the Center will have the power to administer those assesses and collect taxes. The levy of IGST, however, can commence only after the GST law has been enacted by all the legislatures, as it would have to be synchronized through the simultaneous participation of the Center and all the states.

References

(i) Model GST Law, GST Council Secretariat, November, 2016 at http://www.cbec.gov.in

(ii) FAQ-Indirect Tax at https://home.kpmg.com

(iii) Goods and Services Tax at http://www.icra.in

5. Experience of Indian States with VAT

3.19 During the last decade, a major initiative on the revenue side was the introduction of VAT by state Governments over a span of four years (2003-04 to 2007-08). Concurrently, existing general sales tax laws were replaced with the VAT Act (2005) and other associated rules. While a few states opted to stay out of VAT during the initial years, all states adopted it by 2008. Among the states, Uttar Pradesh was the last state to introduce VAT in January 2008, while Haryana was the first in April 2003.

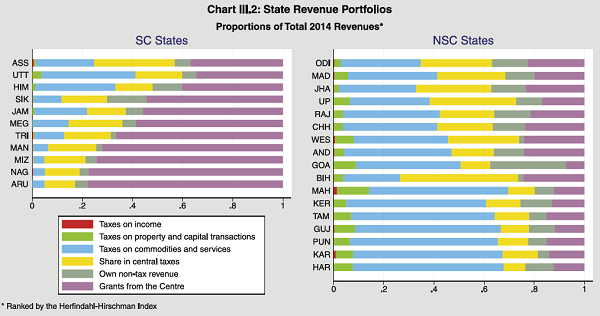

3.20 Indian states have gained revenue efficiency after the introduction of VAT although their revenue structure differ significantly – non-special category (NSC) states depending more on their own tax revenue while the special category (SC) states relying mostly on Central transfers (Chart III.2).7

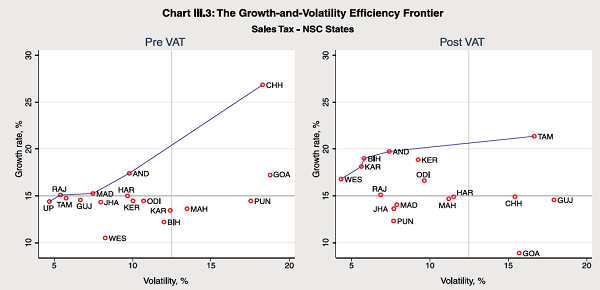

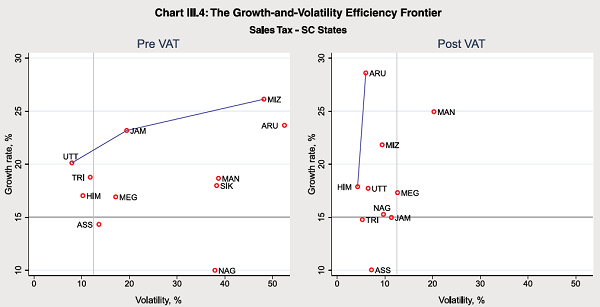

3.21 The introduction of VAT has led to significant revenue efficiency gains for the NSC states whose revenue source are primarily taxation of commodities and properties. The estimated growth and volatility efficiency frontier8 of their sales tax revenue after the introduction of VAT reveal that there has been a distinct migration of states from the south-west (low growth-low volatility) to the north-west quadrant (high growth low volatility) (Chart III.3). 9 Illustratively, the average volatility10 in their sales tax receipts has declined – from 9.8 per cent (pre-VAT) to 9.2 per cent (post-VAT) – while the median growth of tax collections improved to around 15 per cent (post-VAT) from around 14 per cent (pre-VAT).

3.22 SC states, dependent mainly on grants and tax devolution from the Centre, also experienced significant efficiency gains in terms of much lower volatility after introduction of VAT despite their small bases of sales tax revenue. While the median growth in tax revenue has marginally declined (from around 19 to about 18 per cent), average volatility has

declined significantly – to about 9 per cent from around 19 per cent after the introduction of VAT (Chart III.4).

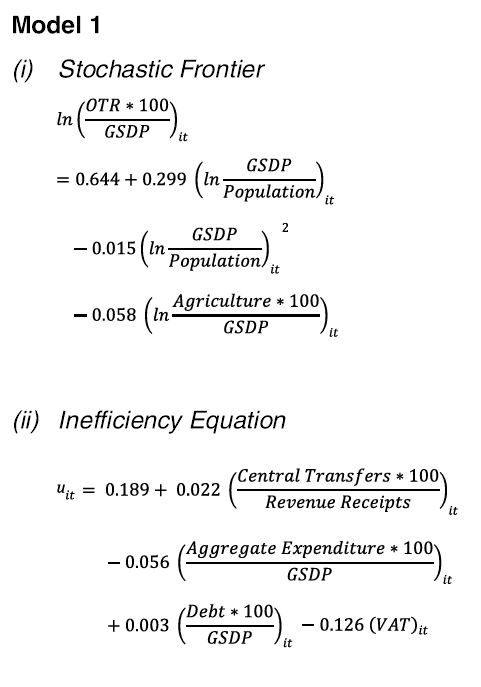

Stochastic Frontier Analysis

3.23 Stochastic frontier analysis (SFA) is used to assess revenue efficiency, analogous to the production function in which the production frontier measures the maximum output (tax revenue) based on inputs (tax base i.e., GSDP per capita and other determinants of tax revenue).

3.24 In order to study tax efficiency, two SFA models are estimated for the period 1990-91 to 2014-15 covering 17 NSC states following the standard methodology (Battese and Coelli, 1995) adapted to the Indian context (see methodology in Annex-II). 11 The model incorporates per capita GSDP (proxy for tax base), square of per capita GSDP (representative of non-linearity in the tax-GDP relationship), share of agriculture in GSDP (a higher share is expected to lower own tax revenue) as the factors that determine (i) own tax revenue of states as proportion of GSDP in Model 1 and (ii) taxes on commodities and services as proportion of GSDP in Model 2. The ratio of transfers to revenue receipts, aggregate expenditure to GSDP, debt-GSDP ratio and dummies for statewise VAT implementation dates are taken as determinants of variation in efficiency across the states.

3.25 The estimates of the equation (see Annex-II, Table 1 and Table 2 for diagnostics) are:

3.26 Equation (i) and (iii) specifies the stochastic frontier production functions for Model 1 and Model 2, respectively for the ith state in time period t. It represents a linearised version of the logarithmic transformation of the Cobb-Douglas production function in which per capita GSDP and share of agriculture in GSDP are taken as inputs. From equation (i) and (iii), it can be seen that one percentage point increase in per capita GSDP increases the own tax revenue- GSDP ratio by 0.3 percentage point in Model 1 and taxes on commodities and services-GSDP ratio by around 0.28 percentage point in Model 2. Similarly, one percentage point increase in the share of agriculture in GSDP reduces own tax revenue-GSDP ratio and taxes on commodities and services-GSDP ratio by about 0.6 percentage point in both Model 1 and Model 2.

3.27 As evident from the statistically significant estimates of the inefficiency equation [(ii) and (iv)], one percentage point increase in the ratio of transfers to revenue receipts leads to increase in inefficiency by 0.02 percentage point in both the models while introduction of VAT reduces inefficiency by 0.13/0.11 percentage point in Model 1/ Model 2, which is in conformity with other studies in the Indian context (Garg et.al, 2014). 12

Sigma Convergence of Tax Efficiency

3.28 To ascertain whether the disparity in tax efficiency across states is declining over time, efficiency scores and the standard deviations for each state are worked out for each year. We undertake “Sigma convergence analysis” in which the standard deviation thus obtained is regressed on time (year) and the squared term of time. A positive and significant coefficient for time suggests divergence across states in tax efficiency scores, although it is increasing at a decreasing rate as given by the negative coefficient of the squared term of time. This implies that less efficient states are not catching up with the more efficient ones (Annex-II – Table 2).

3.29 The ideal GST implementation should ensure a uniform rate structure across states, reduction in compliance cost, removal of cascading, and enhance transparency in tax administration, all of which may significantly improve tax efficiency while reducing its divergence among states.

6. Concluding Observations

3.30 The macroeconomic impact of introduction of the GST could turn out to be significant in the years ahead, given the dominance of the services sector in India. Besides giving a major boost to tax revenue, the larger impact on the fiscal health would be from reduction in the administrative compliance cost. GST is likely to be supportive of fiscal consolidation without compromising capital expenditure.

3.31 Under the prevailing tax structure in India, investment is discouraged through the application of excise duties and VAT on capital goods, for which no set off or input tax credit is provided. For example, input tax credits are not allowed for union excise duties on capital equipment acquired for non manufacturing sectors; similarly, no credit is allowed for the state VAT on capital goods acquired by the services sector. Moreover, GST implementation is likely to boost the small and medium scale enterprises (SME) sector by (i) improving their ease of doing business; (ii) lowering logistical costs; (iii) extending outreach beyond state borders; and (iv) aiding SMEs dealing in sales and services. Furthermore, economic activity would also benefit from exports becoming more competitive as the GST regime will eliminate the cascading impact of taxes.

3.32 The Subramanian Committee (2015) assumed an elasticity of investment demand with respect to price at (-) 0.5 and an incremental capital output ratio of 4 and inferred that GST could increase investment by 2 per cent which could propel growth by an incremental 0.5 per cent although an earlier study had projected GDP growth to increase by 1.7 per cent (NCAER, 2009). A recent study, however, posits a much higher incremental growth impact of 3.1 – 4.2 per cent based on alternative scenarios of the likely aggregated GST rate due to surge in manufacturing activity and trade (Leemput and Wiencek, 2017). The implementation of the GST should also boost domestic business confidence, including among foreign investors by assuring a stable and transparent tax system, free of cascades and distortions.

3.33 As evident from the cross-country experience, one-off effects on inflation dissipated after a year of GST/VAT implementation in most countries. In this context, the short-term effects on inflation depend upon a host of factors including the initial rate at which GST is implemented, the tax base and the efficiency of tax administration. In the Indian context, the implementation of GST is likely to have a pass-through impact lasting 12-18 months on the inflation trajectory (RBI, 2016). This would eventually be moderated by reduction in supply chain rigidities, transportation and production costs which would accrue from the creation of a unified goods and services market post-GST.

3.34 The impact of GST on CPI inflation would largely depend on the four-tier standard rate (5, 12, 18 and 28 per cent) that has been decided by the GST Council although almost 50 per cent of the CPI basket is expected to be exempted. A GST structure with a standard rate of 18 per cent and a low rate of 12 per cent (consistent with a RNR of about 15-15.5 per cent) is expected to have a minimal impact on inflation (Subramanian Committee, 2015). If the standard rate is increased, the impact on aggregate inflation would be higher, concentrated in select groups like healthcare (excluding medicines) (RBI, 2016). As the standard rate increases to 28 per cent, the impact on CPI would further increase. The general consensus is that the impact on consumer price inflation is likely to be moderate if the standard GST rate is at 18 per cent – in fact, overall price levels may actually go down due to more efficient allocation of factors of production in the long run (NCAER, 2009).

3.35 The immediate impact of GST on government finances is deemed to be negligible given that the GST rate structure emphasises a RNR. In the medium to long term, however, GST is likely to increase the tax buoyancy of the Central and state governments by 0.6 per cent which is likely to reduce the gross fiscal deficit by 0.7-1.2 per cent of GDP if disinvestment receipts and non-tax revenues remain unchanged from the trend of the previous 5 years (CRISIL, 2014).

1. As per the Constitution (One Hundred and Twenty Second Amendment) Bill, it has to be ratified by not less than 50 per cent of the states.

2. The origin of VAT/GST can be traced far back to the writings of German businessman Wilhelm Von Siemens in 1920s who proposed it as a substitute for the German turnover tax. VAT/GST has since become an important component in the overall fiscal framework of nearly all industrialised countries and in a large number of Latin American, Asian and African countries.

3. As per the definition under sub-clause 12A of Article 366 of the constitution, GST pertains to any tax on supply of goods or services or both except taxes on supply of alcoholic liquor for human consumption; further, services are defined to mean anything other than goods.

4. The Finance Minister had noted that “GST will streamline the tax administration, avoid harassment of business and result in higher revenue collection, both for the Centre and states” (Union Budget Speech, 2014-15).

5. The report observed “This would be possible if the modified value added tax (MODVAT) now operating through excise tax system is made into a full-fledged manufacturers VAT and the states also adopt a destination based harmonized system of VAT in place of the chaotic sales taxes operating now.”

6. During the meeting, decisions were taken for (a) appointment of the Secretary (Revenue) as the ex-officio Secretary to the GST Council; (b) inclusion of the Chairperson, Central Board of Excise and Customs (CBEC) as a permanent invitee (non-voting) to all proceedings of the GST Council; and (c) creation of one post of Additional Secretary to the GST Council and four posts of Commissioner in the GST Council Secretariat. The GST Council Secretariat are manned by officers on deputation from both the Central and state governments.

7. See footnote in chapter III for list of NSC and SC states

8. See Cornia and Nelson (2010).

9. The labels in Charts III.2, III.3 and III.4 are: AND = Andhra Pradesh; ARU = Arunachal Pradesh; ASS = Assam; BIH = Bihar; CHH = Chhattisgarh; GOA = Goa; GUJ = Gujarat; HAR = Haryana; HIM = Himachal Pradesh; JAM = Jammu and Kashmir; JHA = Jharkhand; KAR = Karnataka; KER = Kerala; MAD = Madhya Pradesh; MAH = Maharashtra; MAN = Manipur; MEG = Meghalaya; MIZ = Mizoram; NAG = Nagaland; ODI = Odisha; PUN = Punjab; RAJ = Rajasthan; SIK = Sikkim; TAM = Tamil Nadu; TRI = Tripura; UP = Uttar Pradesh; UTT = Uttarakhand; WES = West Bengal.

10. Volatility derived from inter-quartile range of growth rates.

11. Model 1 and Model 2 are estimated with data for the period 1990-91 to 2012-13 and 1990-91 to 2014-15, respectively.

12. A stochastic frontier of own tax revenue of 14 Indian states was earlier estimated for the period 1992-93 to 2009-10 (Garg et.al, 2014).

Source- RBI