The introduction of the Goods and Services Tax requires a fundamental re-examination of the approach of the Commercial Taxes Department to the enforcement of tax laws. This circular prescribes the new approach to be followed with effect from 1st June 2019.

Circular No. 10/2019

Q1/17253/2019

Office of the Commissioner of

Commercial Taxes, Chepauk,

Chennai – 5.

Dated : 31-05-2019

Present: Dr T.V. Somanathan, I.A.S.,

Additional Chief Secretary / Commissioner of Commercial Taxes,

Sub : Intelligence wing – Power, Roles and Responsibilities.

Ref : Government letter No.758/B1/2019 dated 19.02.2019.

******

The introduction of the Goods and Services Tax requires a fundamental re-examination of the approach of the Commercial Taxes Department to the enforcement of tax laws. This circular prescribes the new approach to be followed with effect from 1st June 2019.

BACKGROUND

Activities related to enforcement of tax law are distinct from the activities related to voluntary compliance. Intelligence gathering, interception & inspection of vehicles and inspection of premises are (inter alia) various methods which may, as per law, be adopted for enforcing the law in cases where tax evasion has, or is believed to have, occurred. In the past, the Department has followed an approach to enforcement which relies considerably on physical interception of the movement of goods. This approach can no longer continue in the same manner with the removal of inter-state movement controls and check posts. Other enforcement activities, including inspections, had been authorized at decentralized levels. The past track record of the actual collection from such activities shows that the amount actually collected as revenue is a tiny fraction of the amount initially shown as ‘detected’. Enforcement activities have also witnessed numerous vigilance and anti-corruption inquiries over the years. The Government has emphasized that intelligence-based enforcement activities shall be carried out in an unobtrusive and efficient manner with senior officials under proper authorization and overall supervision and control of the Commissioner. The need to avoid indiscriminate investigation and to avoid any disrepute to the Department has been stressed.

By their nature, enforcement activities involve some degree of risk and uncertainty. Enforcement activities can have three possible outcomes:

i) Evasion has taken place and enforcement action is taken- this represents correct enforcement activity.

ii) Evasion has taken place but no enforcement action is taken-this represents an error of omission where a tax evader escapes.

iii) Evasion has not taken place and enforcement action is taken-this represents an error of commission wherein an innocent taxpayer is confronted with unpleasant and unfriendly actions of the Department, with attendant risk of corruption.

The challenge for the Department is to maximize the cases under (i) and minimize the cases under (ii) and (iii) above. However, unless special care is taken efforts to reduce cases under the error under (ii) above by intensifying the enforcement activity carry a risk of increasing the harassment of taxpayers under (iii) above, which is harmful to the economy and to the image of the Department and contrary to the Citizens Charter of the Department. Hence a careful balance is necessary. Reducing errors under (ii) without increase in errors under (iii) requires much more attention to intelligence-gathering, proper risk-based analysis and due authorization of inspections. This circular prescribes the procedures and activities to be followed towards this end.

INTELLIGENCE WING AND ITS FUNCTIONS

The existing Enforcement wing shall hereby be renamed the “Intelligence wing”, with effect from 01.06.2019 in pursuance of G.O.Ms.No.30 CT&R (A2) dated 04.03.2019, reflecting the change in the manner of enforcing tax compliance. The activities shall be focussed on tax evaders on the basis of reports prepared with diligence, from relevant data and information gathered in a scientific manner, and without resort to widespread inspection, or random inspection without adequate data or information ……………….

The term “inspection” used in section 67 and 68 of Tamil Nadu Goods and Services Act (and corresponding provision of even number in the Central GST Act) is a mechanism which enables officers to access any place of business of a taxable person or person engaged in transporting goods or a person who is an owner or an operator of a warehouse or godown. According to section 67, inspections can be carried out by an officer of CGST/SGST only upon a written authorization given by an officer of the rank of Joint Commissioner or any proper officer superior to the Joint Commissioner. The Join’, Commissioner or taxguru.in any proper officer superior to him can authorize any proper officer to conduct inspection only if he has reasons to believe that:-

(a) A taxable person has suppressed any transaction relating to supply of goods or services or stock in hand or

(b) A taxable person has claimed excess input tax credit or

(c) A taxable person has contravened any of provisions of the Act or the Rules to evade tax and

(d) Any person engaged in the business of transporting or storing goods or is keeping goods which have escaped payment of tax or is manipulating accounts or stocks which may cause evasion of tax.

Inspection of goods in movement and conveyances carrying consignment of goods may also be done by proper officers as per the provisions of section 68 of the GST Act to prevent evasion of tax.

Though section 67 and 68 provide ample power to proper officers to inspect any places of business of the taxable persons or the persons engaged in the business of transporting goods or the owners or the operators of warehouse or godown or any other place or inspection of goods in movement or conveyance carrying goods to control tax evasion, such power shall be exercised prudently minimizing room for complaint from genuine tax payers. The power given under these sections is not absolute, but, according to sub-section (1) of section 5 of the SGST Act, the proper officer shall exercise such powers and discharge the duties conferred or imposed on him under this Act subject to such conditions and limitations as the Commissioner of Commercial Taxes may impose.

Therefore, the undersigned is of the view that it is imperative to frame certain protocols to maintain discipline and uniformity in respect of the functions assigned to the Intelligence Wing. Accordingly, the undersigned as Commissioner of Commercial Taxes, under the power vested by sub-section (1) of section 5 of the State Goods and Services Tax Act, 2017 frames the following protocol in respect of taxguru.in the Intelligence wing:

A- CENTRAL INTELLIGENCE WING:

1. The Investigation unit of the Central Intelligence Wing shall, as appropriate, utilize the services of the Technical cell, Data cell and Survey cell to prepare investigation files in respect of such taxpayers as may be ordered by the Commissioner of Commercial Taxes or other taxpayers after getting prior approval from the Commissioner of Commercial Taxes.

2. The Investigation Unit shall examine the complaints received on tax evasion and prepare investigation files based on the complaint or may refer the issue to the Divisional Intelligence Wing for necessary action.

3. The investigation file prepared by the Investigation Unit shall be examined and forwarded by the Joint Commissioner (Central Intelligence) to the Commissioner through the Additional Commissioner (Intelligence) for approval. The Additional Commissioner (Intelligence) shall also examine the investigation file before submitting it to the Commissioner of Commercial Taxes for approval.

4. The Coordination Unit functioning under the Central Intelligence Wing, on approval of the investigation file, shall forward the investigation file to the Joint Commissioner (Intelligence) concerned for inspection through E-mail id exclusively created for this purpose or through physical delivery, wherever necessary.

5. The Coordination Unit shall examine the investigation files

6. The Coordination Unit shall collate data from MIS for the whole State in respect of functioning of the Intelligence Wing and prepare such reports or statistics as may be prescribed or ordered by the Commissioner.

B- INTELLIGENCE DIVISION:

1. The Data cell and the Survey cell shall function under the control of the Deputy Commissioner (Investigation) or the Assistant Commissioner (Investigation), as the case may be. These cells shall gather data or details in respect of such taxpayers as may be ordered by the Commissioner of Commercial taxes or by the Joint Commissioner (Intelligence) concerned or other taxpayers after getting permission from the Joint Commissioner (Intelligence) and provide the required data or details to the Investigation Unit.

2. The Investigation Unit, based on the data gathered from the Data Cell and Survey Cell or inputs from other officers, shall prepare the investigation file and submit the same to the Joint Commissioner (Intelligence).

3. The Joint Commissioner (Intelligence) shall examine the investigation file submitted by the Investigation Unit and if he is satisfied, he may submit it to the Central Intelligence Wing for getting the approval of the Commissioner of Commercial Taxes. I f he is not satisfied with the investigation file, he may direct the Investigation Unit to furnish further particulars or may close the files for reasons to be recorded in writing.

4. The Investigation unit shall examine complaints received by the Intelligence Division or received from the Central Intelligence Wing and prepare investigation file, if deemed fit and shall forward the same to the Central Intelligence Wing for the approval of the Commissioner of Commercial Taxes or may close the issue for reasons to be recorded in writing.

5. The Joint Commissioner (Intelligence), based on the Investigation file approved by the Commissioner of Commercial Taxes, shall authorize officers not below the rank of Deputy State Tax Officer to conduct inspection under section 67 subject to such conditions and restrictions as may be prescribed, from time to time, by the Commissioner of Commercial Taxes as per the powers vested under Section 5(1) of Tamil Nadu Goods and Services Tax Act. 2017. The authorization for inspections and search shall be issued in FORM GST INS-01.

6. The proper officer authorized to conduct the inspection shall scrupulously follow the law and rules governing inspections and connected matter.

7. The inspection team may, as for as possible, comprise of officers having adequate knowledge of the trade and GST law and the size of the team shall be decided depending upon the size of industry. nature of trade, turnover and number of branches.

8. Routine inspection and preparation of investigation file on trivial issues shall be avoided. The investigation file should be based on sound data and legal backing.

9. Officers conducting the inspection should show high degree of honesty and detect cases which would stand the test of law.

10. The Joint Commissioner (Intelligence) shall intimate the commencement of each inspection to the Commissioner by email within 30 minutes of commencement. Further he shall also, at the closure of inspection for the day, submit a daily report containing the names of the officers, starting 136 closing time of the inspection and a brief note on the progress made on each day, which shall include details about the documents seized, findings and the fact whether statement of the day has been recorded or not, to the Central Intelligence Wing through e-mail as in annexure or through portal, in format prescribed, for the notice of Commissioner of Commercial Taxes.

11. The head of the inspecting team or any such other officer not below the rank of State Tax Officer as may be authorized by the Joint Commissioner (Intelligence) shall with a period not inspection, pass the final assessment or adjudication order on the basis of the findings made during the inspection and available records. However, the period of 30 days may, on sufficient cause being shown and for reasons to be recorded in writing, be extended by the Joint Commissioner (Intelligence) for a further period not exceeding 30 days and further extension of time shall be granted with the approval of the Commissioner of Commercial Taxes. Where the proceeding is stayed by an order of the court or Appellate Tribunal or by any competent authority, the period of such stay shall be excluded in computing the above specified period:

12. The proper officer notified as adjudicating authority shall finalize the adjudication in respect of cases not finalized by the Roving squad during their duty hours and which were handed over to them by the Roving squad, at the earliest to the extent possible, but not later than 30 days from the date of completion of inspection or occurrence of the offence. However, the period of 30 days may, on sufficient cause being shown and for reasons to be recorded in writing, be extended by the Joint Commissioner (Intelligence) for a further period not exceeding 30 days and further extension of time shall be granted with the approval of the Commissioner of Commercial Taxes. Where the proceeding is stayed by an order of the court or Appellate Tribunal or by any competent authority, the period of such stay shall be excluded in computing the above specified period.

13. Orders or decisions passed by the Roving Squad or Adjudicating Cell or Inspection Cell or Central Intelligence Cell, along with the relevant records shall be handed over to the Review Cell within two days of passing such orders or decisions.

14. The Deputy Commissioner (Inspection) shall ensure that the Review Cell has examined the said orders or decisions passed by the various units/cells functioning under the Intelligence Division and take a decision to file or not to file appeal before the First Appellate Authority well within the time prescribed. Though section 107(2) provides a period of 6 months for filing appeal before the First Appellate Authority, the Deputy Commissioners (Inspection) shall ensure that such decisions by the Review Cell are taken within ninety days from the date of receipt of the decision and appeals are filed within fifteen days from the expiry of the above said ninety days. Stay of proceedings or orders or decisions of the proper officer concerned by any legal forum or by any competent authority shall be excluded in determining the time limit specified herein.

15. The Joint Commissioner (Intelligence) shall ensure that the Review Cell examines the record of any order or decision passed by the Appellate Authority or the Revision Authority for the purpose of satisfying himself as to the legality or propriety of the said order. In this regard, the Review Cell shall submit a report to the Joint Commissioner as to whether appeal can be preferred before the Tribunal against any order or decision passed by the Appellate Authority or the Revision Authority or not and based on the report, he may cause filing of an appeal before the Tribunal. Though section 112(3) provides a period of 6 months for filing appeal before the Tribunal, such decisions to file or not to file appeal before the Tribunal shall be taken by the Review Cell, within ninety days from the date of receipt of the order or decision and appeals shall be filed within fifteen days from the expiry of the above said ninety days. Stay of proceedings or orders or decisions of the proper officer concerned by any legal forum or by any competent authority shall be excluded in determining the time limit specified herein.

16. The Deputy Commissioner (Inspection) shall ensure that the demand raised during any of the adjudication or assessment proceedings is collected within the due date and if not collected, arrear action shall be taken immediately by the Demand Collection Cell to realize the arrear.

17. The Legal Cell shall coordinate with the Legal wing in the office of the Commissioner of Commercial Taxes and Government Law officers in respect of cases pending before any legal fora and shall also ensure filing of appeal before any legal forum wherever decisions have been taken to file appeal.

18. The Joint Commissioner (Intelligence) shall have control over the entire Intelligence Division and shall exercise the powers and discharge the duties conferred or imposed on him under the Act subject to such conditions and limitations as the Commissioner may impose as per the provisions of sub-section (1) of section 5 of TNGST Act.

19. In cases of any deviation from the protocol stated supra, prior approval shall be obtained and in exceptional cases such deviation shall’ be brought to the notice of Commissioner of Commercial Taxes for ratification.

C- PROTOCOL FOR ROVING SQUAD:

Instances were brought to the notice of the Commissioner of Commercial Taxes where the Roving squad officers are levying maximum penalty in a routine manner even for minor breaches of tax regulations and procedural requirements without adhering to the general disciplines relating to penalty as envisaged under section 126 of CGST/SGST Act. According to section 126 of the said act, no officer under this Act shall impose any penalty for minor breaches of tax regulations or procedural requirements and in particular, any omission or mistake in documentation which is easily rectifiable and made without fraudulent intent or gross negligence, and the Act also provides that the penalty imposed under this Act shall depend on the facts and circumstances of each case and shall be commensurate with the degree and severity of the breach.

Keeping in mind the hardship experienced by genuine taxpayers, the Commissioner of Commercial Taxes issues the following protocol in respect of the functions envisaged under section 129 under the power vested by sub-section(1) of section 5 of the Tamil Nadu Goods and Services Tax Act, 2017.

1. Vehicle check shall be conducted only at such places as may be ordered by the Joint Commissioner and only during the hours of duty prescribed for the concerned squad.

2. No e-way bill is required in respect of those commodities or circumstances specified in sub-rule (14) of Rule 138, and in such cases vehicle shall not be detained.

3. The Commissioner of Commercial Taxes, in certain circumstances, may, by notification, require the person-in-charge of the conveyance to carry (i) tax invoice or bill of supply or bill of entry; or (ii) a delivery challan, where the goods are transported for reasons other than by way of supply, instead of the e-way bill. In such circumstances, the conveyance shall not be detained for not possessing e-way bill.

4. Where the physical verification of goods being transported on any conveyance has been done during transit at one place within the State or Union territory or in any other State or Union territory, no further physical verification of the said conveyance shall be carried out again in the State or Union territory, unless a specific information relating to evasion of tax is made available subsequently, as mandated by sub-rule (2) of rule 138C of the GST Rules.

5. A summary report of every inspection of goods in transit shall be recorded online by the proper officer in Part A of FORM GST EWE-03 within twenty four hours of inspection and the final report in Part B of FORM GST EWB-03 shall be recorded within three days of such inspection.

6. The Roving Squad Officers, in respect of those cases where no decision has been taken by them during their duty hours, shall hand over the detained goods and conveyance along with the documents to the adjudicating unit immediately on completion of Orders or decisions passed by the Roving Squad officers, along with the relevant records shall be handed over to the Review Cell within two days of passing such orders or decisions.

7. It shall be the duty of the Roving Squad to record the name of the consignor and consignee GSTN and address in the relevant reports regardless on whom the penalty is being levied.

8. In cases of any deviation from the protocol stated supra, prior approval shall be obtained and in exceptional cases such deviation shall be brought to the notice of Commissioner of Commercial Taxes for ratification.

9. CIRCUMSTANCES WHERE NO PENALTY SHALL BE LEVIED BY THE ROVING SQUAD:

i) Where the amount involved in the offense is less than Rupees Five thousand.

ii) Where a mistake or omission in documentation is easily rectifiable and has been committed without fraudulent intent or gross negligence or is not backed up with any sort of malicious intent to evade taxes.

iii) Where the issue relates to rate of tax, classification of goods, place of supply disputes, valuation of goods etc: Instead of levying tax and penalty on the spot, these types of cases shall be referred to the assessment circle concerned for further action, without detaining the goods and conveyance. However, in respect of newly registered taxpayers where the roving squad officers are able to establish that the taxpayer had failed to file returns for two or more tax periods this instruction would not apply and the vehicles of such tax payers may be detained for further action, wherever appropriate.

10. CIRCUMSTANCES WHERE PENALTY UPTO Rs. 5000/- PER ACT SHALL BE LEVIED:

Where the movement of goods is accompanied by any one of the basic documents such as invoice or bill of supply or delivery challan or E-way bill as prescribed in Rule 55 A and 138 A of the TNGST Rules 2018, and in such cases where at least one of the basic documents, manifestly showing sufferance of tax in the particular transaction is available, a penalty of upto Rs.5000/- per act shall be levied so as to deter the recurrence of offence. The following are examples in this context:

Example 1: Vehicles meant for a vehicle distributor are delivered at the stock yard / godown / branch; the transporter possesses the necessary tax invoice, but the E-way bill was generated for principal place of business/different place of business.

In this case the CGST / SGST / IGST (if interstate supply) would have been suffered at the hands of manufacturer or distributor. Mere delivery of the goods at a place other than those mentioned in the documents would not render the transaction as an evasion or abetment of evasion. Being a B 2 B transaction, trail of transaction would now be available in GSTR1 for the department.

Example 2: A conveyance carrying the goods from a factory of fertilizers is delivering the same at various locations as directed by the department of Agriculture. The goods are accompanied by invoice or invoice with delivery challan and E-way bill. The E-way bill has expired due to delay in making delivery at various locations. The expiry of E-way bill does not create any scope for evasion.

In cases as in the examples, penalty of upto Rs.5000/- per act shall be levied.

11. CIRCUMSTANCES WHERE PENALTY of Rs. 25000/- SHALL BE LEVIED:

i) In the circumstances described in Sl.No. 10 if any person repeatedly indulges in the same violation, a penalty of Rs.25,000/- per act shall be levied to deter the recurrence of such offence. For this consignee who commits a violation more than once in a calendar month or twice in a calendar quarter or thrice in a financial year.

ii) In all other circumstances, other than the ones falling under Sl.No.9, 10 and 12 a penalty of Rs.25,000/- per act shall be levied.

12. CIRCUMSTANCES WHERE MAXIMUM PENALTY SHALL BE LEVIED:

Where goods are transported without any of the prescribed documents like invoice, delivery challan, e-way bill, it is presumed that there is an intention to evade tax and maximum penalty shall be levied, provided the tax amount exceeds Rupees five thousand.

Sd /- T.V.Somanathan,

Commissioner of Commercial Taxes

To

All Joint Commissioners (ST) (Territorial)-

All Joint Commissioners (ST) (Intelligence)

All the Deputy Commissioners

(Territorial and Intelligence)

Copy to:

1. All Additional Commissioners, 0/o. the CCT, Chepauk, Chennai -5.

2. The Joint Commissioner (Admin), 0/o. the CCT, Chepauk, Chennai -5.

3. The Deputy Commissioner (General Service), 0/o.CCT, Chepauk, Chennai – 5.

4. All the Joint Commissioners (ST), Deputy Commissioners (ST) & Assistant Commissioners(ST), 0/o. the CCT, Chepauk, Chennai – 5.

5. The Joint Commissioner (Computer Systems), Chennai -6 (for uploading in the intranet websites).

6. The Director, Commercial Taxes Staff Training Institute, Chennai-6.

7. All Administrative Officers, O/o. the CCT, Chepauk, O/o. the CCT, Chepauk,

8. Stock File/Spare

//Forwarded by Order//

Superintendent

31/5/19

Annexure

POTENTIAL AREAS FOR TAX EVASION

(This list is indicative and not exhaustive)

(1).Non-disclosure or suppression of purchases made from un-organized sector or from below threshold and corresponding sales to avoid tax payable on output.

(2). Showing lower turnover with meager profit than the actuals to avoid more tax payment.

(3). In B2C transaction, normally the customers are not insisting bills or invoices. In such situation, the taxpayers report sales turnover in such way not to pay any tax and all the time the output tax gets adjusted against the input tax credit on the pretext that the good purchased are in stock.

(4). Normally consumers in B2C transactions do not insist for proper invoices, if they are not charged with any tax and is such circumstances, the taxpayer issues the customer an estimation slip or some other paper as a proof for having sold the goods to such customer. The input tax credit which accrued in respect of these goods would be transferred to another taxpayer through an invoice to make the other taxpayer claim input tax credit for certain percentage of commission without actual sale of goods.

(5). Wherever, the markets is driven by brands and if the sale is from a business to a customer (B2C) , evasion will be more in the form of un-reported sale of duplicate or spurious parts at a lower price and it is more happen in auto parts.

(6). There is a general tendency among the taxpayers dealing in precious metals and stones not to issue invoices to the extent possible to un-report sales made out of goods bought from unknown source or brought from outside the country through illegal means.

(7). Goods supplied to taxpayers involved in operation where black money plays the vital role needs special attention for investigation and inspection. For example, much evasion took place in real estate and construction segment and this may be reason as to why the percentage of tax evasion is higher in Electrical Goods, Marbles, Tiles, Sanitarywares, Steel, Blue metal, bricks and other building materials: and also in services offered to this sector.

(8). Claiming input tax credit against fake invoices and ineligible claim of input tax credit.

(9).Multiple tax rates on the same goods make it an easy way for many taxpayers to evade taxes. In case of garments, a number of smaller players are billing one shirt that costs Rs 1,000 above as two pieces of around Rs 600 each to pay only 5% instead of 12% which is applicable for shirts which costs Rs.1000/ and above.

(10).Goods transported through railways, as it mostly moves unnoticed by the tax officials.

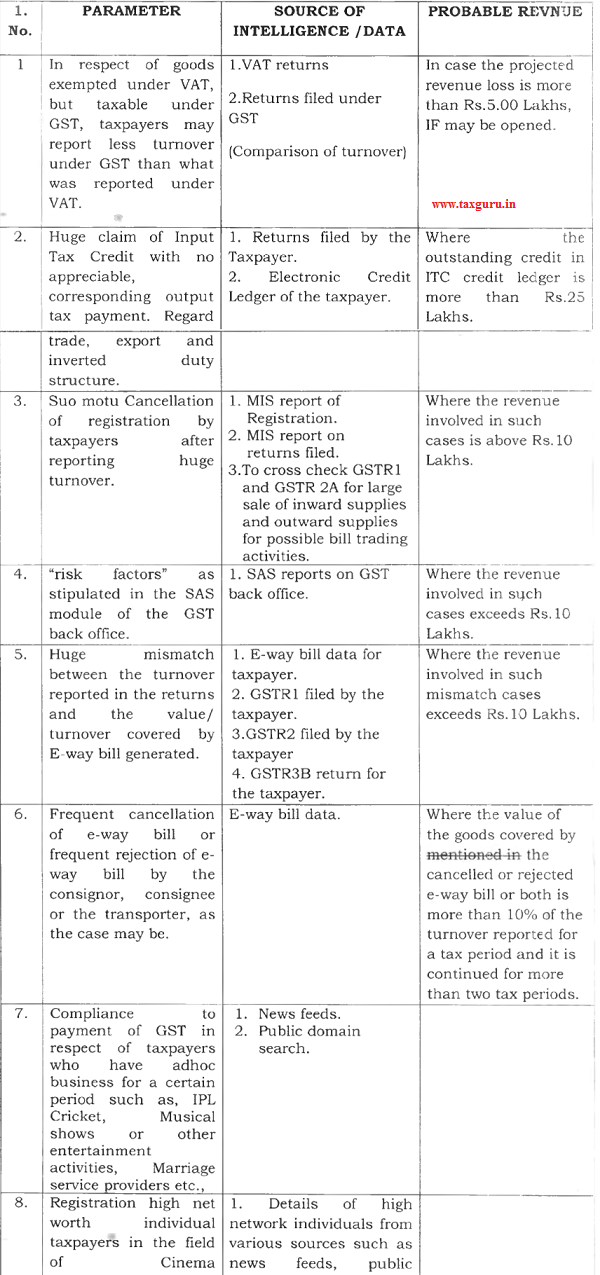

PARAMETERS FOR OPENING INVESTIGATION FILE FOR CONDUCTING AUDIT OR INSPECTION

Note : The parameters in the table below are only prima facie indicators and not conclusive. Proper study and analysis should be done before proposing Inspection / Audit.

Daily Report Format

| IF No. | : | |

| Date | : | |

| Trade name of the Tax Payer | : | |

| GSTIN | : | |

| Name of the Goods/ Service | : | |

| Name of the inspecting officers | : | |

| Starting Time of inspection | : | |

| Closing Time of inspection | : | |

| Brief note on today’s progress | : |

Note: The brief note should contain the details of documents or goods detained during the time of inspection and the details of daily statement recorded from the person in charge of the business place under inspection or the authorized person, as the case may. Statement

Investigation File (IF) NUMBER FORMAT

a) Code – 3 alpha letters to identify the divisions.

CH1 -Intelligence I Chennai

CH2 -Intelligence II Chennai

TVL – Intelligence Tirunelveli

VLR – Intelligence Vellore

MDU – Intelligence Madurai

TRY – Intelligence Trichy

ERD – Intelligence Erode

SLM – Intelligence Salem

CBE – Intelligence Coimbatore

b) Division-wise running Number – 3 digits from 001 to 999

c) YYYY- Year format (4 digits)

d) MM- Month Format (2 digits)

e) DD – Day Format (2 digits)

Example: SLM -001-20190513.

The IF Number will be allocated by Commissioner of Commercial Taxes on approval. All the communications in respect of the inspection related activities carried out by the officials are to be communicated to the Commissioner of Commercial Taxes from hereon, through the subject tag mentioning the aforesaid metadata format, for easy identification and further follow up to the actions taken on each inspection by the Officials.

The following email ids have been created

TABLE-A

| cct.inspapproval@ctd.tn.gov.in | IF details are to be sent to this email id for getting the approval of Commissioner of Commercial Taxes. |

| cct.inspfollowup@ctd.tn.gov.in | Further communication regarding the activities of the IFs are to be sent to this email id from the respective enforcement wing email id created for this purpose as detailed in table B |

TABLE -B

| Sl. No. |

Email id |

| 1. | ch 1 .inspa,ctd.tn. gov. in |

| 2. | ch2.insractd.tn.gov.in |

| 3. | tvl.inspactd.tn.gov.in |

| 4. | vlr.inspactd.tn.gov.in |

| 5. | mdu.inso@ctd.tn.g0v.in |

| 6. | try.insica,ctd.tn.gov.in |

| 7. | erd.insoctd.tn.gov.in |

| 8. | slm.inspactd.tn.gov.in |

| 9. | cbe.insp(e)cctd.tn.gov.in |

Sd /- T.V.Somanathan,

Commissioner of Commercial Taxes

To

All Joint Commissioners (ST) (Territorial)-

All Joint Commissioners (ST) (Intelligence)

All the Deputy Commissioners

(Territorial and Intelligence)

Copy to:

1. All Additional Commissioners, O/o. the CCT, Chepauk, Chennai -5.

2. The Joint Commissioner (Admin), 0/o. the CCT, Chepauk, Chennai -5.

3. The Deputy Commissioner (General Service), 0/o.CCT, Chepauk, Chennai – 5.

4. All the Joint Commissioners (ST), Deputy Commissioners (ST) & Assistant Commissioners(ST), 0/o. the CCT, Chepauk, Chennai – 5.

5. The Joint Commissioner (Computer Systems), Chennai -6 for uploading in the intranet websites.

6. The Director, Commercial Taxes Staff Training Institute, Chennai-6.

7. All Administrative Officers, O/o. the CCT, Chepauk, O/o. the CCT, Chepauk,

8. Stock File/Spare

/ / Forwarded by Order/ /

Superintendent

31/05/2019