A registered supplier is not allowed to avail of the Input Tax Credit of GST paid in respect of motor vehicles. The Act is silent on the allowability of Input Tax Credit of GST paid on insurance, repair and maintenance of motor vehicles. So, the taxpayers were in dilemma whether such ITC should be claimed or not? Even Department is not sure about the treatment of such ITC.

Government has replied to FAQ on 28.12.2017 , Question no 14 and has given clarification on this aspect. The clarification given is as follows:-

Question No. 14: Whether GST paid on insurance and Repairs on Vehicles is allowed, when vehicles is used for Business purpose only??

Answer: ITC is available

But in the (FAQs) ON GOODS AND SERVICES TAX (GST) 3rd Edition: 15th December, 2018, Department has taken U-turn regarding ITC on Motor Vehicle services. The text of the same is reproduce here:

Q 41. Whether tax paid on repairs, maintenance and insurance of Motor Vehicles used for the purpose of business is eligible for ITC?

Ans. The ITC on repairs, maintenance and general insurance of those motor vehicles is blocked if the ITC is blocked under Section 17(5)(a) of the CGST Act 2017.

Motor Vehicles for transportation of persons: Thus, ITC on repairing, maintenance and insurance of motor vehicles for transportation of persons carrying more than 13 persons will be admissible. However, for motor vehicles for transportation of persons carrying up to 13 persons will be admissible only if it is used for transportation of passengers, further supply of such motor vehicles and imparting training on driving. [ Section 17(5) (ab) as substituted vide the CGST (Amendment) Act, 2018]

Motor Vehicles for transportation of Goods: ITC on repairing, maintenance and insurance of motor vehicles for transportation of goods is admissible with no restrictions.

Department has come with different views in different platform. Even once in Twitter they have clarified that the input tax credit on repair and maintenance of the vehicle is not admissible. So this created lot of incertitude in the mind of people regarding ITC on Such services.

Now let us Understand , what act says about ITC on Motor Vehicle

As per provisions contained under section 17(5) of CGST Act, input tax credit (ITC) is not available for certain supplies under GST. These supplies are also named as blocked credit. The relevant provision of section 17 (5) are explained hereunder;

As per section 17 (5) input tax credit shall not be available in respect of the motor vehicles and other conveyances, however, following are the exceptional to the same –

(a) motor vehicles and other conveyances except when they are used––

(i) for making the following taxable supplies, namely:—

(A) further supply of such vehicles or conveyances ; or

(B) transportation of passengers; or

(C) imparting training on driving, flying, navigating such vehicles or conveyances;

(ii) for transportation of goods;

“motor vehicle” shall have the same meaning as assigned to it in clause (28) of section 2 of the Motor Vehicles Act, 1988;

“motor vehicle” or “vehicle” means any mechanically propelled vehicle adapted for use upon roads whether the power of 1 Subs. & ins. by Act. propulsion is transmitted thereto from an external or internal source and includes a chassis to which a body has not been attached and a trailer; but does not include a vehicle running upon fixed rails or a vehicle of a special type adapted for use only in a factory or in any other enclosed premises or a vehicle having less than four wheels fitted with engine capacity of not exceeding thirty-five cubic centimetres;

As per the provisions, we can conclude that the input tax credit shall not be available in respect of the motor vehicles and other conveyances, except when they are used for making further supply of such vehicles or conveyances or transportation of passengers or imparting training on driving, flying, navigating such vehicles or conveyances and for transportation of goods.

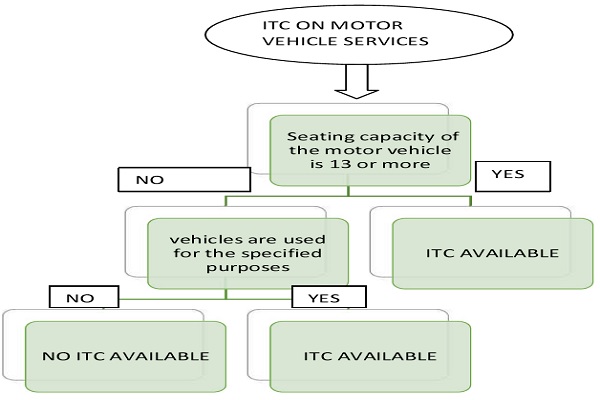

However On August 9, 2018 the Lok Sabha has passed the GST Amendment Bill, 2018 The recent amendment now provides that the Input Tax Credit shall be available in every situation, if the seating capacity of the motor vehicle is 13 or more (including driver). For other vehicles, the ITC shall be available only if these vehicles are used for the specified purposes as mentioned above. Further, the words ‘Other conveyances’ have been removed. Therefore, input tax credit would now be available in respect of dumpers, work-trucks, fork-lift trucks and other special purpose motor vehicles.

Therefore, the input tax credit can be available for motor vehicle services only in two cases :

- if the seating capacity of the motor vehicle is 13 or more or

- if these vehicles are used for the specified purposes.

Author Bio

Can I get the reply to FAQ date 28th December 2017.

Was not able to find it anywhere

Can we availed ITC on insurance premium paid to General Insurance company(United India Insurance Co. Ltd.) for vehicle is used to transportation of Children for school.

I KNOW IF PURCHASES ANY CAR FOR OWNER USED SO WE TAKE GST INPUT TAX CREDIT (OWNER OR CO USE BOTH CONDITION)

Hi Sir

can you help me on domestic transportation insurance claims. Are claims taxable? if yes then how much is maximum limit

now iam going to purchase new car, can you tell me shall take itc input (company a/c)

Sir

What about the JCB used in Construction work. is ITC is available on its Purchase or repair as the same is not used in passenger lifting.

Articulated vehicles like Trailor itc is available?

Deepak sir,

I am following your article from last 3 years

I found your aricle very informative, useful and easy to understand as you use flow chart in most of the cases.

Keep writing keep sharing

Eagerly waiting for your next article.

Very well explained, First time able to understand input regarding ITC on Motor Vehicle

Thank you so much

Keeping writing such useful article

Thanks for Sharing Such Valuable Blog.