Introduction

Of the many reforms introduced in the Modi regime, Goods and Services Tax (GST) has been the center of attraction, inviting reactions fromeconomic stalwarts to the local farmers. It is a consumption-based tax system. While it’s a new and evolving law, it has been the government’s effort to try and keep it out of the target of political propaganda.[1]I feel instead of criticising GST altogether, it is imperative to analyse the law and draw comparisons with the erstwhile regime, to see why it has been brought and what has changed for the better or worse. GST has been instrumental in addressing some vital problems of the previous tax structure and has positively affected the middle class and people belonging to the lower strata of the society.[2]

Therefore,I have tried to shed light upon some important aspects of GST, listing out its pros and cons, giving information as to why it was needed, the problems it aims to tackle and also mentioning some of the salient features. Later, I have also suggested some reforms required to be made in GST for it to be more structured and systematic. I believe that the introduction of GST is an extremely progressive stance taken by the Indian government that should make a more integrated and effective indirect tax structure in India.

Why GST in India?

In pre-GST regime there were several indirect taxes levied like excise, custom, central sales tax, service tax, value added tax and so on. But GST is a system where almost all these separate taxes have been subsumed into one. Thiseases and smoothens the tax compliance as now only one tax, i.e., GST to be levied. The four GST slabs are currently set at 5%, 12%, 18% and 28%. The various goods and services are placed among these slabs and are taxed according to their slab rates. Lowest rates for the most essential commodities and the higher rates for luxuries. There are also NIL rated things, i.e., 0% tax on them such as basic necessities. The export sector gets a big boost too as the supplies there are ‘zero-rated’ meaning no GST on exports, thus, booming the economy. This integrated law is supposed to reduce the tax burdenwhen compared to the erstwhile system where the burden was excessive.[3] Previously, the tax was at two points i.e., whilst the product moves out of factory and other on the retail outlet. However, GST is to be charged at final destination of consumption and no longer at various factors. This brings transparency and corruption free tax administration.[4]

Another motivation behind bringing in GST was to broaden the tax base by doing away or reducing the compliances and processes involved,including more economic activities on a wider scale and an overall reduction of taxpayer’s burden on goods and services through the ‘level playing field process’by obliterating the cascading tax effect and doing away with multiple tax statues that governed the pre-GST era. Thus, as a result the domestic industry is expected to boomwith healthy competition and an expected rise in GDP by 2%.[5]

Issues GST Tried to Address

GST finds its roots in Germany where German Economists in the late 18thCentury asserted that there is a unique kind of sales tax that doesn’t impact the manufacturing and distribution cost, but is collected with respect to the final price that was charged to the consumer. Consequently, irrespective of the number of hand changing transactions taking place from the point of manufacture of the good to the sale to the consumer, the tax rate was always set at the final price.[6]Thus, making GST a destination based consumption tax mechanism, where even though there can be multiple transactions in the process of manufacture and distribution; with respect to the goods or services, these transactional taxes are all taxed against the output.[7]

Hence, it is vital to know that GST has tried to address many issues that existed in the previous regime like that of cascading tax effect, intricate filing procedures, cumbersome tax registration process, etc. that majorly caused distress among the middle-class people of India that form the backbone of India’s economy. Some of the issues are discussed as below:-

(i) ‘Cascading Tax Effect’ –

One daunting issue of the erstwhile regime was the plethora of indirect taxes that existed.The initial tax structure was complex and intricate where payment had to be made for the overlapping of taxes,which was eventually borne by the customer. This overlapping was called the ‘cascading tax effect’.In laymen terminology this meant paying ‘tax on tax’.[8] Thecause of this was primarily based on ‘input tax credit’.ITC was basically the tax that one paid on material purchases but could not be reduced from tax payable on output.[9] This can be explainedwith the example of a commodity like a Phone.The erstwhile structure would practically involve tax levy at every stage. For instance, the first step would be the procurement of raw materials where VAT is added. In the next process, the manufacturer process would involve another tax called Excise tax. The next tax would be at retailers’ level which would be VAT after the manufacturing process. This would include that tax that has been already added to the value at the initial level. While in this case the VAT would be at the state level, the Excise tax would be at the central level. Also, the Central tax cannot be claimed against the State tax, i.e., Excise and VAT cannot be claimed against each other. At the state level,any other state tax cannot be claimed against other state tax i.e. VAT cannot be claimed against another state tax.

Illustration:

| ACTION | COST | 10% Tax | Total |

| Buys raw material | 200 | 20 | 220 |

| Manufacturer adds value of 30 | 250 | 25 | 275 |

| Another value addition of 25 | 300 | 30 | 330 |

| Retailer adds value of 20 | 350 | 35 | 385 |

| Total | 275 | 110 | 385 |

Therefore, the 10% tax at every level is added to the cost and the final amount adds up to 275 (actual cost) + 110 (10% tax) = 385

Comparing the same with GST where the tax that is added at every level is deducted and the actual liability is added to the total.

| ACTION | COST | 10% Tax | Actual Liability | Total |

| Buys raw material | 200 | 20 | 20 | 220 |

| Manufacturer adds value of 30 | 250 | 25 | 5 | 255

|

| Another value addition of 25 | 280 | 28 | 3 | 283 |

| Retailer adds value of 20 | 303 | 30.3 | 2.3 | 305.3

|

| Total | 275 | 30.3 | 30.3 | 305.3 |

Therefore, the 10% tax is reduced by the tax that has been earlier charged (ITC). In this way it only calculates the extra amount that has been added. The final amount would then be 275 (actual cost) + 30.3 (10% tax after reducing ITC) = 303.3

The above example iterates how tax on tax is taken care of in GST. This reduces the amount of tax liability the consumer has to pay.

(ii) ‘Problems of Small Traders & Businessmen’ –

The generic criticism of GST, that it is anti-middle class and does not cater to needs of small traders and businessmen, is farce. The agenda being pushed that GSTfavours the rich capitalists is wrong and flawed.[10]For example, the threshold limit earlier was at Rs.5 lakhs in most of the states.The GST regime has increased this threshold to Rs.40 lakhs which exempts many small traders and service providers. Adding to this, the inclusion of the composition scheme clarifies in a certain way that, GST being for the elite argument, is baseless. The Composition Scheme was categorically brought into place to bring relief to small businessesto free them from the complex legal mandates. This scheme benefits small businesses with turnovers up to Rs.1.5cr.[11]Thus, GST provides for a level playing field for all. Further, the products and services being allowed to move freely through the country provides a conducive environment to general growth of the trade and commerce in the country.

(iii) ‘Consumer Friendly’ –

The tax structure has been made more people friendly by makingthe entire process of GSTonline. This directly benefits the people who have been progressively using the online platform and would also be advantageous for the startups.[12]Also, the number of compliances has been lowered, making the process easier as, when multiple taxes existed the different time periods for the filing of returns of the taxes made the process more burdensome and strenuous for a layman.[13]This in turn brings a certain amount of uniformity. The simpler process for tax refunds too has brought greater alacrity.

Salient Features

GST came into effect with the 101st Constitutional Amendment Act, that gave legal validity to the law through Articles 269A and 279A. Given below are some of its essential features: –

(i) ‘Basic Structure’ –

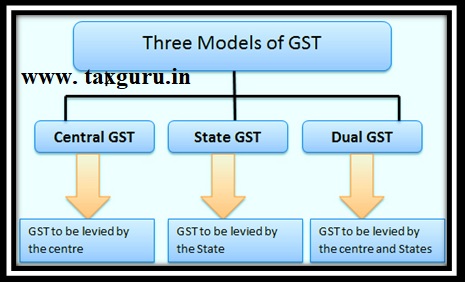

Since India has a federal structure, GST also has been brought in with a similar layout, i.e., GST on Intra-State Transactions and GST on Inter-State Transaction. These are the following components of GST:

CGST: The Central Goods and Service Tax is levied by the Central Government on Intra-State supplies of goods and services, governed by the CGST Act.

SGST: The State Goods and Service Tax is levied by the State Government on Intra-State supplies of goods and services, governed by the SGST Act.

Thus, in Intra-State supplies of goods and services there is revenue sharing between the Central and the State Government in the form of CGST and SGST.[14]

IGST: The GST mechanism has a provision for Integrated Goods and Service Tax, levied on Inter-State supply of goods and services, governed by the IGST Act. This also deals with export and import in and from India.[15]

Examples of CGST, SGST and IGST

a) Rao, dealer in electrical insulators from Maharashtra sold goods worth Rs.10,000 to Mr. Raut in Maharashtra itself. The GST rate of this good is presently 18%, hence, CGST and SGST is 9% each. Thus, Mr. Rao would collect a sum of Rs.1,800 from Mr. Raut, out of which Rs.900 will be paid to the Central Government and Rs.900 would be paid to the Maharashtra State Government.

b) Rao of Maharashtra sells goods worth Rs.2,00,000 to Mr. Banerjee in West Bengal. The GST rate being 18% is composed of 18% IGST,it being an inter-state transaction. Thus,Mr. Rao will charge Rs.36,000 from Mr. Banerjee in the form of IGST which will go to the Centre. Afterwards, the Centre will distribute the half amount, i.e., Rs.18,000 to the West Bengal State Government.

(ii) ‘GST Council’ –

It’s the governing body that regulates all aspects of GST like administration, rates, rules, implementation, etc. GST Council compromises of representatives from both Centre and State. Adequate representation has been given to State Governments as well. It has the Union Finance Minister as the Chairman, Union MoS of Finance from the Centre and then respective Finance Ministers from each State/UT from the States[16], thus, giving a wholistic and balanced representation to provide point of views from every region. Hence, inputs from all over India can help make the functioning of GST as efficient as possible.

(iii) ‘Compensation Cess’ –

Pre-GST all the States levied their own indirect taxes and generated revenue from the economic activities going on in their respective territories. But with GST in picture, one central tax was imposed throughout the territory of India, the revenue of which was to be shared between Centre and State equally. This gave the States a sense of insecurity as now they would have to share a large proportion of their revenue with the Central Government and thus, fearing revenue loss. Hence, to absolve the States of this fear and to ensure smooth implementation of GST pan India, the Central Government while announcing GST came up with ‘Compensation Cess’, that was supposed to be levied on certain goods and services, the revenue of which is to be shared with the respective State Governments in lieu of the supposed loss of revenue, so that the States do not fall short of funds. However, such cess has been levied only for the initial 5 years. It has been imposed on certain products like tobacco, certain petroleum goods, particular motor vehicles, etc. that account for a major chunk of revenue for the States. Such cess is levied over and above the GST rate[17]. Therefore, any shortfall in revenue of the States due to GST is aimed to be compensated for the given time period through Compensation Cess. The money is to be distributed by the Centre to the States bi-monthly[18].

But its also important to note that still, alcohol and petroleum products have been kept out of the ambit of GST as these two are the biggest revenue generators for the States, thus not disturbing their revenue generation capacity. However, talks are underway on how to incorporate these things too under GST so that there is uniformity, and no one stands at a loss.

(iv) ‘Input Tax Credit’ (ITC) –

This is the most advantageous and beneficial aspect of GST. ITC enables the price of goods/services to go down. This has benefitted both the consumers and the traders/manufacturers. ITC is basically the difference between the tax paid on inputs and the tax paid on outputs. It can be availed by a registered person, who takes supply of goods/services and further uses them in course of furtherance of business. It’s a seamless credit system that serves as a set-off against the tax payable. Hence, by this the businessman can mitigate its tax liability and ends paying a lesser amount of tax. Consequently, the consumer ends up paying up less as compared to what he was paying earlier.

But ITC is not available for certain products/services like immovable products, inputs used for construction, long term lease deeds, etc. and this leaves a large impact on such sector and the benefits available to them under GST. ITC cannot be availed for work contract services supplied for construction of immovable property (except plant and machinery), except where the supply is for further work contracts. If goods/services are received for construction of immovable property (except plant and machinery) for self or even in course of business, then also ITC cannot be availed.[19] A big twist came in via the Odisha High Court judgement in ‘M/S. Safari Retreats Private Limited v Chief Commissioner of CGST’[20], that laid that ITC can be availed by the person when constructing a building that has been built for the purpose of letting out. It said that restriction as to availing ITC was set for construction for ‘own account’, which is quite different when compared to ‘letting out/lease’ and hence, should be allowed in these cases. The reason being that the assessee not getting benefit of ITC would be contrary to the purpose of GST as the person would be double-taxed, as paying taxes on inputs used for construction as well as paying taxes on the rental income received from such investments.

Similar burden exists for people dealing in leasing business as it is considered as a service and hence, charged high rate of GST, but cannot avail ITC. There have been few rulings and judgements at the state level that tend to favour availing of ITC by reading S.17(5) of CGST Act differently. But no precedent and clarity is there given the lack of any Supreme Court judgement. Hence, this remains a highly debated issue.

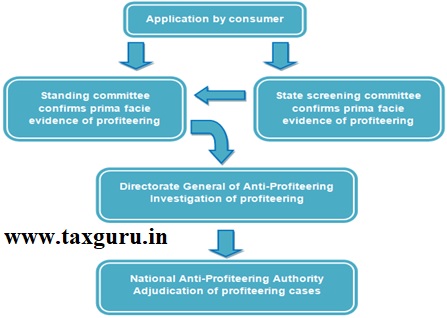

(v) ‘Anti-Profiteering under GST’ –

Primary motive of GST was to bring down the expenditure of the consumers. To ensure that the benefit of the law reaches the consumers, and the manufacturers and service providers pass on the benefit of ITC as reduced prices, ‘anti-profiteering’ provision was made under the law via S.171 of CGST Act. However, this clause did spark up a lot of debates among the stakeholders, it being perceived as restrictive on trade and violating the Fundamental Right to Free Trade.

This clause was brought in to prevent excessive and unfair profit making by entities in an illicit manner. This rule mandates the manufacturers and service providers to rally on the benefits they received because of the reduced tax rates or ITC, in form of reduced prices to the consumers.[21]S.171(2) of CGST Act enables the central government to set up an Authority to monitor and enforce compliance with the requirements of the provision. The GST Council also issued the Anti-profiteering Rules 2017 (‘APR2017’) to induce implementation of the above law.

If the Authority finds a business guilty of having committed anti-profiteering practices, as per Rule 14 of‘APR 2017’, it can penalise the entity by either cancelling the registration, imposing a penalty, order a reduction in prices, order the company to refund the customer an amount equal to what it has earned by not passing on the price benefits from the time the GST took effect, or in case the buyer is not identifiable, order the company to deposit the refund amount in the Consumer Welfare Fund. The Authority even has power to take suo motu action.The process for filing an anti-profiteering complaint is explained as follows:

Hence, it aims at protecting the interests of consumers without hurting the rights of the industry and keeping the retail inflation at check. This provision is still a work-in-progress and hopefully will not harm the businesses, without raising uncertainties.

(vi) ‘eWay Bill’ –

It’s an electronic bill that needs to be generated for facilitating movement of goods. It is mandatory to generate such when the supply is above Rs.50,000, and irrespective of the value of supply if it is an inter-state supply.For certain supplies it is mandatory to always generate it like handicraft goods, e-commerce operators, etc. There is a whole list of supplies which are exempt from this clause like supply of alcohol, petroleum products, etc. as per the rules. The onus is on the registered person, transporter or the recipient of supply to generate such bill, where a unique number is generated for each such supply.[22] This assists in movement of goods throughout the nation. This has reduced the compliance burden of maintaining several documents as it can be used country wide, at different check-posts, also reducing the harassment and time wastage caused via such checking at different borders.

It is generated through an online portal where the details of supply, such as value, address, recipient, etc. is filled in the different forms mandated.[23] There are penalties in place if someone fails to provide eWay Bill or has incorrect information. The same can also be cancelled within 24 hours if the supply is not made.[24]

Bright Side of GST

Many positives can be seen after the onset of GST. Some of them can be listed as follows: –

(i) GST is levied only when there is supply, unlike the erstwhile regime where tax was levied on the manufacture of goods, sale of goods and/or on provision of services.

(ii) It creates a single market in India by removing the plethora of multiple taxes into a single uniform tax process and removes tax difference bias because of the uniform rates.

(iii) It forms an undisrupted credit chain, where all tax is collected by the Centre and distributed to the States.

(iv) The reduced tax burden of the companies will result in reduced production cost, making India more competitive in the export market too.

(v) GST uses minimum human interface as it is mostly software based (GSTN) which will help in curbing corrupt practices that occurred in the past by keeping minimum interaction with the administration.

(vi) Such lucrative tax rates will widen the tax base and as a result tax collection would be better and effective.

(vii) Compliances and filing returns are easier as now it is to be done for only one law instead of multiple statutes, bringing down compliance cost too. This also leads to increased ease of doing business.

(viii) GST leads to ‘one nation, one market’, increasing competition among national and international businesses and promoting the ‘Make in India’ campaign.

Proposed Reforms

GST being so young is not perfect and requires amendments to make it effective and efficient. The following are a few changes that I feel could go a long way in fulfilling this purpose: –

(i) Widening the ambit of the GST should take place. Currently, petroleum, electricity, alcohol, land, buildings, etc. have been kept outside the ambit of GST. These products are important as they form basic input for several industries. The cascading tax effect still continues for these as the credit of GST charged in the supply of these goods cannot be set off and older tax laws cannot be set off against GST.[25] It should apply to unorganised transport sector too as it will result in reduction of time wastage and less harassment at inter-state borders.[26]

(ii) The online system that has huge potential of making the tax regime more people friendly and easy, has been unusually structured and made problematic. Stringent compliance systems have made the system difficult to work on.[27]The issue of inefficacy of the officers managing the GST compliances and regulation continues. It has been seen that the efficacy of these officers largely affects the performance of the tax regimes.[28]

(iii) A few shortcomings in the anti-profiteering clause can also be removed. The current provision seems a bit confusing to the industry and they feel that a sword is always looming over their heads given the power under this clause. Hence, to address this, a margin can be kept so that if the price is fixed between this limit, then the businesses do not face any consequences. A threshold can also be put up where individuals upto a certain turnover are exempt from this clause, to motivate trade and prevent losses to small businessmen. Further, steps can be taken to minimise the discretion with the authority to avoid any harassment of the taxpayer.

(iv) There should be a change in the restrictions on availing ITC for construction purposes by bifurcating and analysing the construction works to allot them into categories for which ITC may be claimed and not. Thus, a broad view should be taken to assess the inputs. The nature, function, use, utility and relation of the input should be thoroughly looked before denying benefit of ITC.

Conclusion

GST has been the biggest change in India’s tax regime, rejigging the whole indirect tax structure. It is imperative to understand that the economic boom that the country has gotten post the 2010s has massively affected the position of India as an economic powerhouse. India is seen by the international community as a lucrative potential market for investment, and favourable and attractive tax laws contribute a big way in making India such an investment friendly nation. The funding of developmental and welfare policies depends a lot on the regulation and collection of taxes. I believe GST will prove beneficial for this. Taxes are the pillars to any nation’s solid infrastructure.Therefore, it is important that GST caters to need of citizens and fulfills the purpose of requisite tax collection. A simpler, comprehensive and integrated tax system like GST will solve all these needs and set India upon a path of growth and development. But because the system is so new, it is developing as we go, addressing all the issues that crop up, solving the practicality in its implementation and making it more efficient and effective. Therefore, some of the reforms mentioned above can go a long way in addressing the longstanding non-payment and wastage of tax.

Note

[1]Gireesh Chandra Prasad, ‘Jaitley signals further GST rate cuts, hits out against politicizing tax reform’(Livemint, 13thNovember, 2017) https://www.livemint.com/Politics/E3xJWwyYUTTgvxRU2jom8I/Arun-Jaitley-rules-out-single-GST-rate-says-rationalisation.html

[2]‘GST effect: 5 things that changed after the new tax regime’(BusinessToday, 11thJuly, 2017) https://www.businesstoday.in/current/economy-politics/gst-effect-5-things-that-changed-after-the-new-tax-regime/story/256269.html

[3]id

[4] id

[5]id

[6] id

[7] id

[8] Mahadev. R, ‘Cascading Effect of Tax in India’(Hiregange And Associates, 14thApril, 2014) https://hiregange.com/assets/articles/14-04-22_cascading_effect_of_taxes.pdf

[9]id

[10] ‘GST to benefit lower, lower-middle income class’ (BusinessLine, 22nd August, 2017) https://www.thehindubusinessline.com/economy/gst-to-benefit-lower-lowermiddle-income-class-adb-blog/article9826674.ece

[11]‘GST Composition Scheme’(ClearTax, 10th May, 2020) https://cleartax.in/s/gst-composition-scheme

[12] Prakash Chawla, ‘GST – A game changer for India’(Press Information Bureau, 4thAugust, 2016) http://pib.nic.in/newsite/mbErel.aspx?relid=148344

[13]id

[14] ‘What is SGST CGST and IGST’ (ClearTax, 6th March, 2020)https://cleartax.in/s/what-is-sgst-cgst-igst

[15] id

[16] ‘GST Council: All you need to know about GST Council & Meetings’ (3rd January, 2020) https://margcompusoft.com/m/gst-council/

[17] ‘What is GST Compensation Cess?’ (PaisaBazaar, 19th April, 2020) https://www.paisabazaar.com/tax/gst-compensation-cess/

[18] Satya Sontanam, ‘All you wanted to know about compensation cess’ (BusinessLine, 17th December, 2019) https://www.thehindubusinessline.com/opinion/columns/slate/all-you-wanted-to-know-about-compensation-cess/article30321925.ece

[19]Central Goods and Services Act 2017, S.17(5)

[20] M/S. Safari Retreats Private Limited v Chief Commissioner Of Central Goods & Service Tax (2019) (5) TMI 1278 (Orissa HC)

[21]Central Goods and Services Act 2017, S.171(1)

[22] ‘What is e Way Bill? E Waybill Rules & Generation Process Explained’ (ClearTax, 6th March, 2020) https://cleartax.in/s/eway-bill-gst-rules-compliance

[23]id

[24] Pramit P Ghosh, ‘E-Way Bill under GST- Format and Rules’ (Tally, 21st November, 2019) https://tallysolutions.com/gst/e-way-bill-under-gst/

[25] Indira Rajaraman, ‘Further reforms are needed for the GST to succeed’ (Livemint, 3rdNovember, 2017) https://www.livemint.com/Opinion/YR10H8ALBpr8R6diidIv4N/Further-reforms-are-needed-for-the-GST-to-succeed.html

[26] Rajat Arora, ‘GST provided much-needed reform to the logistics sector’(The Economic Times, 2ndJuly, 2018) https://economictimes.indiatimes.com/industry/transportation/shipping-/-transport/gst-provided-much-needed-reform-to-the-logistics-sector/articleshow/64821263.cms

[27]‘GST a much-needed reform, but has issues that need to be addressed’ (The Hindu, 22ndOctober, 2017) https://www.thehindu.com/news/cities/Tiruchirapalli/gst-a-much-needed-reform-but-has-issues-that-need-to-be-addressed/article19900295.ece

[28]id

not so impressive, it is only the story but not in practical.

in the market traders are selling at MRP inclusive of GST.

Even the govt is cheats the customer on diesel /petrol