GST Revenue for April 2021

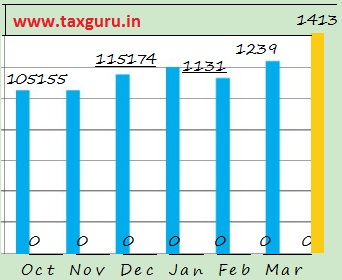

The gross GST revenue collected in the month of April, 2021 is at a record high of Rs. 1,41,384 crores, out of which, CGST is Rs. 27,837 crores, SGST is Rs. 35,621 crores, IGST is Rs 68,481 crores (including Rs. 29,599 crores collected on import of goods) and Cess is Rs. 9,445 crores (including Rs. 981 crores collected on import of goods). Despite the second wave of COVID-19 pandemic affecting several parts of the country, Indian businesses have once again shown remarkable resilience by not only complying with the return filing requirements but also paying their GST dues in a timely manner during the month.

The GST revenues during April 2021 are the highest since the introduction of GST, even surpassing collections in the last month. In line with the trend of recovery in the GST revenues over past six months, the revenues for the month of April 2021 are 14% higher than the GST revenues in the last month of March,2021. During the month, the revenues from domestic transaction (including import of services) are 21% higher than the revenues from these sources during the last month.

GST revenues have not only crossed the Rs. 1 lakh crore mark successively during the last seven months but have also shown a steady increase. These are clear indicators of sustained economic recovery during this period. Measures like closer monitoring against fake-billing, deep data analytics using data from multiple sources including GST, Income-tax and Customs IT systems and effective tax administration have also contributed to the steady increase in tax revenue. Quarterly return and monthly payment scheme has been successfully implemented bringing relief to the small taxpayers as they now file only one return every three months. Providing IT support to taxpayers in the form of pre-filled GSTR 2A and 3B returns and ramped up system capacity have also eased the return filing process.

During this month the government has settled Rs. 29,185 crores to CGST and Rs. 22,756 crores to SGST from IGST as regular settlement. The total revenue of Centre and the States after regular and ad-hoc settlements in the month of April’ 2021 is Rs. 57,022 crores for CGST and Rs. 58,377 crores for the SGST.

The chart below shows trends in monthly gross GST revenues during the October,20 to March,20 and April,2021. 160000 140000 120000 100000 80000 60000 40000

♦ GST Collection Year ‘2

♦ GST Collection Year ’21

Source: PIB Press Release dated 1.05.2021

GST Relief measures in view of COVID-19 pandemic

In view of the challenges faced by taxpayers in meeting the statutory and regulatory compliances under GST law due to the outbreak of the second wave of COVID-19 pandemic, the Government has issued notifications, all dated 1 May, 2021, providing various relief measures for taxpayers. These

st

measures are explained below:

1. Reduction in rate of interest:

Concessional rates of interest in lieu of the normal rate of interest of 18% per annum for delayed tax payments have been prescribed in the following cases.

a. For registered persons having aggregate turnover above Rs. 5 crore: A lower rate of interest of 9 per cent for the first 15 days from the due date of payment of tax and 18 per cent thereafter, for the tax payable for tax periods March 2021 and April 2021, payable in April 2021 and May 2021 respectively, has been notified.

b. For registered persons having aggregate turnover up to Rs. 5 crore: Nil rate of interest for the first 15 days from the due date of payment of tax, 9 per cent for the next 15 days, and 18 per cent thereafter, for both normal taxpayers and those under QRMP scheme, for the tax payable for the periods March 2021 and April 2021, payable in April 2021 and May 2021 respectively, has been notified.

c. For registered persons who have opted to pay tax under the Composition scheme: NIL rate of interest for first 15 days from the due date of payment of tax and 9 per cent for the next 15 days, and 18 per cent thereafter has been notified for the tax payable for the quarter ending 31st March, 2021, payable in April 2021.

2. Waiver of late fee

a. For registered persons having aggregate turnover above Rs. 5 crore: Late fee waived for 15 days in respect of returns in FORM GSTR-3B furnished beyond the due date for tax periods March, 2021 and April, 2021, due in the April 2021 and May 2021 respectively;

b. For registered persons having aggregate turnover up to Rs. 5 crore: Late fee waived for 30 days in respect of the returns in FORM GSTR-3B furnished beyond the due date for tax periods March, 2021 and April, 2021 (for taxpayers filing monthly returns) due in April 2021 and May 2021 respectively / and for period Jan-March, 2021 (for taxpayers filing quarterly returns under QRMP scheme) due in April 2021.

3. Extension of due date of filing GSTR-1, IFF, GSTR-4 and ITC-04

a. Due date of filing FORM GSTR-1 and IFF for the month of April (due in May) has been extended by 15 days.

b. Due date of filing FORM GSTR-4 for FY 2020-21 has been extended from 30th April, 2021 to 31st May, 2021.

c. Due date of furnishing FORM ITC-04 for Jan-March, 2021 quarter has been extended from 25th April, 2021 to 31st May, 2021.

4. Certain amendments in CGST Rules:

a. Relaxation in availment of ITC: Rule 36(4) i.e. 105% cap on availment of ITC in FORM GSTR-3B to be applicable on cumulative basis for period April and May 2021, to be applied in the return for tax period May 2021. Otherwise, rule 36(4) is applicable for each tax period.

b. The filing of GSTR-3B and GSTR-1/ IFF by companies using electronic verification code has already been enabled for the period from the 27.04.2021 to 31.05.2021.

5. Extension in statutory time limits under section 168A of the CGST Act: Time limit for completion of various actions, by any authority or by any person, under the GST Act, which falls during the period from 15th April, 2021 to 30th May, 2021, has been extended up to 31st May, 2021, subject to some exceptions as specified in the notification.

Source: PIB Release dated 02.05.2021

Notifications

| Notification No. & Date | Subject |

| Notification No. 14/2021-Central Tax dated 01.05.2021 | Seeks to extend specified compliances falling between 15.04.2021 to 30.05.2021 till 31.05.2021 in exercise of powers under section 168A of CGST Act. |

| Notification No. 13/2021-Central Tax dated 01.05.2021 | Seeks to make third amendment (2021) to CGST Rules. |

| Notification No. 12/2021-Central Tax dated 01.05.2021 | Seeks to extend the due date of furnishing FORM GSTR-1 for April, 2021 |

| Notification No. 11/2021-Central Tax dated 01.05.2021 | Seeks to extend the due date for furnishing of FORM ITC-04 for the period Jan-March |

| Notification No. 10/2021-Central Tax dated 01.05.2021 | Seeks to extend the due date for filing FORM GSTR-4 for financial year 2020-21 |

| Notification No. 09/2021-Central Tax dated 01.05.2021 | Seeks to amend notification no. 76/2018-Central Tax in order to provide waiver of late fees for specified taxpayers and specified tax periods |

| Notification No. 08/2021-Central Tax dated 01.05.2021 | Seeks to provide relief by lowering of interest rate for the month of March and April, 2021 |

| Notification No. 07/2021Central Tax, dated 27.04.2021 | The facility of filing GSTR-3B and GSTR-1/ IFF, using EVC instead of DSC, for companies has been provided vide Notification No. 07/2021Central Tax, dated 27.04.2021 for period upto 31.05.2021. |

Source: https://www.cbic.gov.in/htdocs-cbec/gst/central-tax-notfns-2017

Changes made in Customs Duty in view of Covid-19

| Notification No. & Date | Subject |

| Notification No. 29/2021-Customs dated 30.04.2021 | Seeks to amend notification No. 27/2021-Customs to exempt customs duty on import of specified Inflammatory Diagnostic (markers) kits, up to 31st October, 2021. |

| Notification No. 28/2021-Customs dated 24.04.2021 | Seeks to exempt customs duty and health cess on import of oxygen, oxygen related equipment and COVID-19 vaccines, up to 31st July, 2021. |

| Notification No. 27/2021-Customs dated 20.04.2021 | Seeks to exempt customs duty on import of Remdesivir injection, Remdesivir API and Beta Cyclodextrin (SBEBCD) used in the manufacture of Remdesivir, up to 31st October, 2021. |

Source: https://www.cbic.gov.in/Customs-Notifications

IGST Exemption on imports of COVID19 relief material donated from abroad

The Government has granted exemption from IGST vide ad hoc exemption Order 4/2021-Customs on imports of specified Covid-19 relief material received free of cost for free distribution for covid relief across the country. On such goods custom duty was already been exempted vide Notification (Customs) No. 27/2021 dated 20.04.2021, 28/2021 dated 24.04.2021 and 29/2021 dated 30.04.2021

The exemption order shall apply to all such consignments pending clearance from Customs as on date of issue of order. Thus, as BCD is already exempt, such imports will not attract any customs duty or IGST. The Chief Secretaries of states are being requested to appoint Nodal Agency and authorize relief agencies for the purpose. Necessary instructions also issued to field formations to expedite clearance of such cargo.

GST Portal Updates

> Auto-population of e-invoice details into GSTR-1

For the month of March, 2021, the auto-population of e-invoices into GSTR-1 is still in progress and is likely to take some more time. Hence, notified taxpayers who are reporting e-invoices, are hereby advised not to wait for the complete auto-population, and instead proceed with preparation and filing of GSTR-1 for March, 2021 (by the due date), based on actual data as per their records.

Portal updated on 06/04/2021

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders.

To view module wise functionalities deployed on the GST Portal and webinars conducted/ Videos posted on our YouTube channel, refer to table below:

Sl. No. |

Taxpayer functionalities deployed on the GST Portal during |

Click link below |

1. |

March, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalities_compilationmarch2021.pdf |

2. |

February, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalities_compilationfebruary2021.pdf |

3. |

January, 2021 |

https://tutorial.gst.gov.in/downloads/news/taxpayerfunctionalities_deployed _jan_2021.pdf |

4. |

October-December,2020 |

https://tutorial.gst.gov.in/downloads/news/functionalities_released_octtodec2020.pdf |

5. |

Compilation of GSTN YouTube Videos posted from January-December, 2020 |

https://tutorial.gst.gov.in/downloads/news/gstn_youtube_videos_posted_2020.pdf |

Portal updated on 06.04.2021

> Payment of Tax by Taxpayers under QRMP Scheme, for the month of March, 2021

1. All taxpayers having aggregate turnover up to Rs 5 crores, under QRMP Scheme (w.e.f. 01.01.2021), are required to furnish return on quarterly basis, along with payment of tax on monthly basis.

2. Persons availing QRMP Scheme are required to pay tax due, in each of the three months of the quarter, by depositing the due amount as discussed below.

3. Payment of Tax for first two months of a quarter (M1 & M2 i.e. for January and February month for Jan-March Quarter):

a. While generating the challan, taxpayers must select “Monthly payment for quarterly taxpayer” as reason for generating the challan.

b. They can choose either of the following two options to generate the Challan:

i. 35% Challan (Fixed Sum Method): For taxpayers opting for this method, portal will generate a pre-filled challan in Form GST PMT-06, for an amount equal to 35% of the tax paid in cash, in the preceding quarter, if the return was furnished quarterly or equal to the tax paid in cash in the last month of the immediately preceding quarter, if the return was furnished monthly.

ii. Challan on a self-assessment basis (Self-Assessment Method): These taxpayers can pay tax due by considering the tax liability on inward and outward supplies and the input tax credit as available, in FORM GST PMT-06.

Note: The aforesaid options are not available for payment of tax for third month (M3) of the quarter to persons availing QRMP Scheme.

c. Payment of Tax for third month of a quarter (M3 i.e. for March month for Jan-March Quarter): For third month of the quarter (M3), taxpayers can click button ‘Create Challan’ in Payment Table 6 of Form GSTR-3B and file GST-PMT-06 Challan, for depositing any amount towards their tax liability.

Portal updated on 08.04.2021

> Clarification on reporting 4-digit/6-digit HSNs

GST helpdesk is in receipt of some tickets at helpdesk wherein it was reported that certain 6-digit HSN codes are not available in HSN Master/not accepted on e-invoice/e-Way bill portals.

Background:

Notification No. 12/2017-Central Tax dated June 28, 2017, as amended vide Notification No. 78/2020 Central Tax, dated October 15, 2020, mandates taxpayers to declare specified digits, as follows, of Harmonised System of Nomenclature (HSN) / Service Accounting Code (SAC) Code on raising of tax invoices, w.e.f. April 1, 2021.

| Sl. No. | Aggregate Turnover in the preceding Financial Year | Number of Digits of HSN Code |

| 1. | Upto INR 5 crores | 4 |

| 2. | More than INR 5 crores | 6 |

It may be noted that specific 6-digit HSNs, as available in the HSN/Customs Tariff (with corresponding description of goods) are allowed in the system. It also follows that the declaration of HSN at 4/6 Digits has to be out of valid HSN codes only.

However, there are instances that some taxpayers are trying to report truncated first 6-digits out of an otherwise valid 8-digit HSN; which are actually not available in Tariff at 6-digit level and with no corresponding description of goods; these are invalid and hence not being allowed in the System.

Taxpayers may, therefore note that based on the harmonious interpretation of the Notifications, as referred above, read with Customs Tariff Act, 1975, as made applicable to GST; the number of digits of HSN, as specified vide Notifications No. 12/2017 & 78/2020 (Central Tax), are the minimum number of digits of HSN to be mentioned on the invoice.

Example: Where HSN 6 digits are specified to be reported in invoice, valid HSN codes as available in tariff, at both 6-digits and 8-digits can be mentioned. Similarly, where HSN at 4-digits are specified, valid HSN codes as available in tariff, at 4-digit, 6-digit and 8-digit can be mentioned. However, the 4/6 Digit HSN Codes, which are not available in the tariff;

along with specific description, Unit and GST Rate; are not allowed to be mentioned.

Portal updated on 12.04.2021

> New features of Form GSTR-2B & GSTR-3B made available to taxpayers under QRMP Scheme

The new features related to filing of Statement/ Returns by taxpayers under QRMP Scheme, for the quarter of Jan-Mar., 2021, which has been made available to them are summarized below:

1. Auto Generation of Form GSTR-2B, for the QRMP taxpayers

a) Form GSTR-2B contains details of filed IFFs (for Month M1 & M2) & filed Form GSTR 1 (for Month M3).

b) Form GSTR 2B has two sections of ITC i.e. ITC available and ITC not available (which flows from the supplier’s filed IFF & Form GSTR-1, imports etc.). It also contains tax liability of the taxpayer (which flows from the taxpayers own filed IFF & Form GSTR-1).

c) Taxpayers can view and download their system generated Quarterly Form GSTR-2B for Jan-March, 2021 quarter, by clicking on Auto- drafted ITC statement for the quarter on 14th April, 2021, by selecting the last month of the quarter (M3)

d) The default view of Form GSTR-2B is quarterly. However to view Form GSTR-2B of a particular month (M1, M2 or M3), taxpayer has an option to select appropriate month, from the view drop-down to view that month’s data.

e) A hyperlink ‘View advisory’ has also been provided, which on clicking displays the criteria/ cut-off dates considered for quarterly GSTR-2B as a pop-up, with details of Supplies from/type e. Monthly taxpayer, Taxpayer in QRMP Scheme, NRTP, ISD & Import from Overseas/SEZs, and ‘From date’ and ‘To date’ based on which Form GSTR-2B has been generated.

2. Auto-population of ITC in Form GSTR-3B for the QRMP taxpayers

a) Figures of ITC available and ITC to be reversed will now be auto-populated in Table 4 of Form GSTR-3B, for the QRMP taxpayers, from their system generated quarterly Form GSTR-2B.

b) On the GSTR-3B dashboard page, an additional button ‘System computed GSTR-3B’ has also been provided, by clicking which system computed Form GSTR-3B can be downloaded in PDF format.

c) Taxpayer can edit the auto-drafted values as per their records and save the updated details.

d) The system will show a warning message to taxpayers in case ITC available is increased by more than 5% or ITC to be reversed is reduced even partially, by them. However, the system will not stop the filing of Form GSTR-3B in such cases.

Portal updated on 13.04.2021

> Updates in Forms GSTR-1, GSTR-3B and Matching Offline Tool for taxpayers in QRMP Scheme

With effect from 1st January, 2021, all taxpayers with Annual Aggregate Turnover up to Rs 5 Crore have been given an option to file their Form GSTR-1 Statement and Form GSTR-3B return on a quarterly basis. They also have an option to file B2B invoice details in Invoice Furnishing Facility (IFF) for months 1 and 2 (ex. Jan and Feb) of the quarter in order to pass on the credit, whereas the remaining invoices have to be declared in the Quarterly Form GSTR-1 of Month 3 (e.g. March).

I. The salient points related to filing of Form GSTR-1 Statement & auto-population of liability in Form GSTR-3B for taxpayers under QRMP Scheme for the quarter Jan-Mar., 2021, are summarized below:

a) Before filing Form GSTR-1, taxpayers may note the following:

| Period | Type of Statement | If in saved state | If in submitted state | After filing |

| Jan. & Feb., 2021 | IFF | RESET to delete the saved records and then add these details in Form GSTR-1 (Quarterly) before filing |

File IFF before filing Form GSTR-1 (Quarterly) | Invoices filed in IFF in Jan and Feb need not be entered again in Form GSTR-1. If these are entered again, portal will give an error at save stage itself. |

b)Liability in Table-3 [except 3.1(d)] of Form GSTR-3B, for the taxpayers under QRMP Scheme, will be auto-populated on the basis of IFF filed, if any, for the Jan and Feb months and quarterly Form GSTR-1 for the Quarter. Liability on account of inward supplies attracting reverse charge in Table 3.1 (d) is auto-populated from the taxpayer’s FORM GSTR 2B. The System computed liability will also be made available in PDF format on taxpayer’s GSTR-3B (Quarterly) dashboard.

II. Matching Offline Tools:

a) The Matching Offline Tool has been updated for taxpayers under QRMP Scheme. In the Matching tool dashboard page, an option to select the quarter has been provided and in the purchase register, quarters Apr-Jun, Jul-Sep, Oct-Dec and Jan-Mar have been added to the tax periods.

b) The system generated Form GSTR-2B JSON file can be used for matching details with their purchase register, using the updated Matching Offline Tool. Taxpayers can now navigate Services > Returns > Returns Dashboard, select the Financial Year and Return Filing Period > SEARCH and click on Download button on Auto drafted ITC Statement GSTR -2B tile to download system generated Form GSTR-2B JSON file.

Portal updated on 13.04.2021

> Due dates for filing of Form GSTR-3B from the Tax Period of January, 2021

Government of India, Ministry of Finance (Department of Revenue), CBIC, vide Notification No 82/2020 Central Tax, dated 10th Nov., 2020, has revised Rule 61 of the Central Goods and Services Tax Rules, 2017, to provide for staggered filing of Form GSTR-3B, for the tax periods from January, 2021, onwards, as under:

| Sl. No. | Class of registered persons who have Opted for | Having principal place of business in the State/ UT of | Due date of filing of Form GSTR-3B, from January, 2021, onwards |

| 1 | Monthly filing of Form GSTR-3B | All States and UTs | 20th of the following month |

| 2 | Quarterly filing of Form GSTR-3B | States of Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana and Andhra Pradesh, the Union territories of Daman and Diu, Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands and Lakshadweep | 22nd of the month following the quarter |

| States of Himachal Pradesh, Punjab, Uttarakhand,

Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand and Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh and Delhi |

24th of the month following the quarter |

Portal updated on 16.04.2021

******

Printed & Published by GST COUNCIL SECRETARIAT | 5th Floor, Tower-II, Jeevan Bharati Building, Connaught Place, New Delhi 110 001, Ph: 011-23762656, www.gstcouncil.gov

DISCLAIMER: This newsletter is in-house efforts ofthe GST Council Secretariat. The contents ofthis newsletter do not represent the views ofGST Council and are for reference purpose only.