As a upcoming tax professionals you must know about the procedure of assessments under GST Scenario and what are the procedures followed by the Assessing officers under GST scenario as per section from 59 to 64 of the CGST Act, 2017

What is the meaning of Assessment under GST Law?

As per Section 2(11) of CGST Act,2017,”Assessments” means determining the tax liability under This Act and includes self-assessment, re-assessment, provisional assessment, summary assessment and best judgment assessment.

1. Self –Assessment:

As per Section 59 of the CGST Act,2017, every registered person shall self-assess the taxes and payable under this Act and furnish a return for each tax period s specified under section 39.

2. Provisional Assessment:

As per Section 60 of CGST Act,2017 subject to the provisions of sub-section (2) , where the taxable person is unable to determine the value of goods or services or both or determine the rate of tax applicable thereto, he may request the proper officer in writing giving reasons for payment of tax on a provisional basis and the proper officer in writing giving reasons for pass an order, within a period not later than 90 days from the date of receipt of such request, allowing payment of tax on provisional basis at such rate or on such value as may be specified by him.

FROM GST ASMT-01: As per Rule 98(1) of the CGST Rules,2017, states that every registered person requesting for payment of tax on a provisional basis in accordance with the provisions of sub-section (1) of section 60 shall furnish an application along with the document in support of his request, electronically in FORM GST ASMT-01 on the Common Portal, either directly or through GST Practitioner .

FORM GST ASMT-02: Notice to appear in person or furnish additional information/documents, as per 98(2) of the CGST Act,2017,states that the proper officer may, on recipient of the application under sub-rule (1), issue a notice in FORM GST ASMT-02 requiring the registered person to furnish additional information or documents in support of his request and the applicant shall file a reply to the notice in FOR GST ASMT-03 and may appear in person before the said officer if he so desires.

What are the records and documents to be submit before GST Officer for completion of Assessment under GST Law:

(a) Verification of records by GST Officer at the time of take up assessment for prepare audit notes: The proper officer authorized to conduct of the records and books of account of the registered person shall with the assistance of the team of officers and officials accompanying him, verify the documents and statements furnished under the Act and rules made thereunder , to check the correctness of following:-

i. The turnover,

ii. Exemptions and deductions claimed,

iii. The rate of tax applied in respect of supply of goods or services,

iv. The input tax availed and utilized ,

v. Refund claimed, proper officer and his team will examine other relevant issued ad record the observations in is audit notes.

(b) To afford the necessary facility to verify the books of accounts or other documents he may require,

II. The taxable person submit these following records to GST officer:

i) Cash book for the audit period mentioned by the audit officer in said notice,

ii) Ledger of inward supply of goods , services,

iii) Ledger of out ward supply of goods, services,

iv) Returns forms like GST Form 3B, GSTR-1, GSTR-2 and GSTR-3 and GSTR-4 etc., maintained by the taxable person as per GST Act, Maintenance of Records Rules,

v) Payments challans,

vi) Ledger of Bank account,

vii) Details of E way bill for the audit period for inward and out ward supply of goods and services,

viii) GST registration certificate details like principle place of business, branch and other place of details whether incorporate or not,

ix) Ledger of stock maintained at Where house by the taxable person,

x) Trial Balance for the audit period and Profit and Loss Account,

xi) Copy and details of Trans-1, Trans-2 and 2A and Trans-3 etc., for the year 2017-18 along with stock register and copies of original invoice relating to ITC claimed in Trans-1 for the period prior to July’2017 as per Sec.143 of CGST Act,2017.

Form and manner of issuance of order:

As per Rule 98(3) of CGST Act,2017 ,that the proper officer shall issue an order in FORM GST ASMT-04 , allowing payment of tax on a provisional basis indicating the value or the rate or both on the basis of which the assessment is to be allowed on a provisional basis and the amount for which the bond is to be executed and security to be furnished not exceeding twenty five percent, of the amount covered under the bond.

Bond with security:

As per secc.60(2) of the CGST Act,2017, the payment of tax on provisional basis may be allowed, if the taxable person executes a bond in such form as may be prescribed and with such surety or security as the proper officer may deem fir, binding the taxable person for payment of the difference between the amount of tax as may be finally assessed and the amount of tax provisionally assessed.

Rule 98(4) of the CGST Act,2017, the registered person shall execute a bond in accordance with the provisions of sub-section (2) of section 60 in FORM GST ASMT-05 along with a security in the form of a bank guarantee for an amount as determined under sub-rule (3).

Provided that a bond furnished to the proper officer under the CGST SGST//UTGST/IGST Acts shall be deemed to be a bond furnished under the provisions of this Act and the rules made thereunder.

Explanation:- For the purpose of this rule, the term ”amount” shall include the amount of integrated tax, central tax, State tax, or Union territory tax and cess payable in respect of the transaction.

Time Limit for passing final order:

As per section 60(3) of the CGST Act,2017 the proper officer shall, within a period not exceeding six months from the date of the communication of the order issued under sub-section (1), pass the final assessment order after taking into account such information as may be required for finalizing the assessment.

Provided that the period specified in this sub-section may, on sufficient cause being shown and for reasons to be recorded in writing, be extended by the Joint Commissioner or Additional Commissioner for a further period not exceeding six months and by the Commissioner for such further period not exceeding four years.

As per Rule 98)5) of the CGST Act,2017, the proper officer shall issue a notice in FORM GST ASMT-06, calling for information and records required for finalization of assessment under sub-section (3) of section 60 and shall issue a final assessment order, specifying the amount payable by the registered person or the amount refundable, if any in FORM GST ASMT-07.

As per rule 98(6) of the CGST Act,2017, the applicant may file an application in FORM GST ASMT-08 for release of security furnished under sub-rule (4) after issue of order under sub-rule (5).

As per rule 98(7) of CGST Act,2017, the proper officer shall release the security furnished under sub-rule (4), after ensuring that the applicant has paid the amount specified in sub-rule (5) and issue an order in FORM GST SMT-09 within a period of seven working days from the date of receipt of the application under sub-rule(6).

Payment of Interest:

As per section 60(4) of the CGST Act,2017, the registered person shall be liable to pay interest on any tax payable to pay interest on any tax payable on the supply of goods or services or both under provisional assessment but not paid on the due date specified under subsection (7) of section 39 or the rules made there under, at the rate specified under sub-section (1) of section 50 , from the first day after the due date of payment of tax in respect of the said supply of goods or services or both till the date of actual payment, whether such amount is paid before or after the issuance of order for final assessment.

Refund:

As per section 60(5) of the CGST Act,2017, where the registered person is entitled to a refund consequent to the order of final assessment under sub-section (3) , subject to the provisions of sub-section (8) of section 54 , interest shall be paid on such refund as provided in section 56.

Scrutiny of Returns:

As per sec.61 of the CGST Act, 2017, provides:-

(1) The proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform him of the discrepancies noticed if any, in such manner as may be prescribed ad seek his explanation thereto.

(2) In case the explanation is found acceptable , the registered person shall be informed accordingly and no further action shall be taken in this regard.

(3) In case no satisfactory explanation is furnished within a period of thirty days of being informed by the proper officer or such further period as may be permitted by him or where the registered person, after accepting the discrepancies , fails to take the corrective measure in his return for the month in which the discrepancy is accepted, the proper officer may initiate appropriate action including those under sec.65 or sec.66 or sec.67, or proceed to determine the tax and other dues under sec.73 or sec.74.

Manner of Scrutiny of Returns:

As per rule 99 of the CGST Rules, 2017 provides for the manner of scrutiny of returns:-

(1) Where any return furnished by a registered person is selected for scrutiny , the proper officer shall scrutinize the same in accordance with the provisions of section 61 with reference to the information available with him, and in case of any discrepancy, he shall issue a notice to the said person in FORM GST ASMT-10 , informing him of such discrepancy and seeking his explanation thereto within such time , not exceeding thirty days from the date of service of the notice or such further period as may be permitted by him and also , where possible , quantifying the amount of tax, interest and any other amount payable in relation to such discrepancy.

(2) The registered person may accept the discrepancy mentioned in the notice issued under sub-rule (1) , and pay the tax, interest and any other amount arising from such discrepancy and inform the same or furnish an explanation for the discrepancy in FORM GST ASMT-11 to the proper officer.

(3) Where the explanation furnished by the registered person or the information submitted under sub-rule (2) is found to be acceptable, the proper officer shall inform him accordingly in FORM GST ASMT-12.

Assessment of Non-Fillers of Return:

As per Section 62 of the CGST Act,2017 provides :-

(1) Notwithstanding anything to the contrary contained in sec.73 or sec.74, where a registered person fails to furnished the return under sec.39 or sec.45, ever after the service of a notice under sec.46, the proper officer may proceed to assess the tax liability of the said person to the best of his judgment taking into account all the relevant material which is available or which he has gathered and issue an assessment order within a period of five years from the date specified under sec.44 or furnishing of the annual return for the financial year to which the tax not paid relates.

(2) Where the registered person furnishes a valid return within thirty days of the service of the assessment order under sub-section (1), the said assessment order shall be deemed to have been withdrawn but the liability for payment of interest under subsection () of section 50 or for the payment of late fee under sec.47 shall continue.

(3) As per rule 100(1) of CGST Act,2017, The order of assessment made under subsection (1) of section 62 shall be issued in FORM GST ASMT-12.

Assessment of Unregistered Person:

As per section 63 of the CGST Act,2017, provides:-

Notwithstanding anything to the contrary contained in section 73 or sec.74, where a taxable person fails to obtain registration even though liable to do so or whose registration has been cancelled under sun-section (2) of section 29 but who was liable to pay tax, the proper officer may proceed to assess the tax liability of such taxable person to the best of his judgment for the relevant tax periods and issue an assessment order within a period of five years from the date specified under section 44 for furnishing of the annual return for the financial year to which the tax not paid relates:

Provided that no such assessment order shall passed without giving the person an opportunity of being heard.

As per Rule 100(2) of CGST Act,2017,the proper officer shall issue a notice to a taxable person in accordance with the provisions of sec.63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and after allowing a time of fifteen days o such person to furnish his reply if any, pass an order in FOR GST ASMT-15.

Summary of Assessment in Certain Cases:

As per sec.64(1) of CGST Act,2017, the proper officer may, on any evidence showing a tax liability of a person coming to his notice , with the previous permission of Additional Commissioner or Joint Commissioner, proceed to assess the tax liability of such person to protect the interest of revenue and issue an assessment order, if he has sufficient grounds to believe that any delay in doing so may adversely affect the interest of revenue.

Provided that where the taxable person to whom the liability pertains is not ascertainable and such liability pertains to supply of goods, the person in charge of such goods shall be deemed to be the taxable person liable to be assessed and liable to pay tax and any other amount due under this section.

As per Rule 100(3) of CGST Act,2017, The order of summary assessment under subsection (1) of section 64 shall be issued in FROM GST ASMT-16.

As per sec.64(2) of the CGST Act,2017, provides that on application made by the taxable person within thirty days from the date of receipt of order passed under sub-section (1) or on his own motion , if the Additional Commissioner or Joint Commissioner considers that such order is erroneous , he may withdraw such order and follow the procedure laid down in section 73 or section 74.

As per rule 100(5) of CGST Act,2017,The person referred to in sub-section (2) of section 64 may file an application for withdrawal of the summary or, as the case may be, rejection of the application under sub-section (2) of section 64 shall be issued in FORM GST ASMT-18.

Dear Professional colleagues, I have completed my notes on “ ASSESSMENTS “ under various sections under GST Law,2017.

Notes on DEMAND AND RECOVERY “ UNDER Sec.73 and 74 of CGST Act,2017.

Q.1 What are the applicable sections for the purpose of recovery of tax short paid or not paid or amount erroneously refunded or input tax wrongly availed or utilized?

Ans. Section 73 deals with the cases where there is no invocation of fraud/ suppression / mis-statement etc. Section 74 deals with cases where the provisions related to fraud/suppression/mis-statement etc., are invoked.

Q.2 What if person chargeable with tax , pays the amount along with interest before issue of show cause notice under Sec.73?

Ans. In such cases notice shall not be issued by the proper officer as per Sec73(3) of CGST Act.

Q.3 If show cause notice is issued under Section 73 and thereafter the noticee makes payment along with applicable interest , is there any need to adjudicate the case?

Ans. If the person pays the tax along with interest within 30 days of issue of notice, no penalty shall be payable and all proceedings in respect of such notice shall be deemed to be concluded as per Sec.73(8) of CGST Act,2017.

Q.4 What is the relevant date for issue of show cause notice?

Ans. (I). In case of section 73 ( cases other than fraud/suppression of facts/ willful misstatement), the relevant date shall be counted from the due date for filing of annual return for the financial year to which demand relates to the Show Cause Notice has to be adjudicated within at a period of three years from the due date of filing of annual return. The Show Cause Notice is required to be issued at least three months prior to the time limit set for adjudication as per Sec. 73(2&10).

(ii). In case of Section 74 ( cases involving fraud/suppression of facts/willful misstatement), the relevant date shall be counted from the due date for filing of annual return for the financial year to which demand relates to. The Show Cause Notice has to be adjudicated within at period of five years from the due date of filling of annual return. The Show Cause Notice is required to be issued at least ix months prior to the time limit set for adjudication as per Sec.74(2 & 10) of CGST Act,2017.

Q.5 Is there any time limit for adjudication the case?

Ans. (1). In case of Sec.73 ( cases involving fraud/suppression of facts/willful misstatement), the time limit for adjudication of cases is 3 years from the due date for filing of annual return for the financial year to which demand relates to or the date of erroneous refund/ITC wrongly availed as per Sec.73(10) of CGST Act,2017.

(2). In case of Sec.74 ( cases involving fraud/suppression of facts/willful mis-statement), the time limit for adjudication of cases is 5 years from the due date for filing of annual return for the financial year to which demand relates to or the date of erroneous refund/ITC wrongly availed as per Sec.74(10) of CGST Act,2017.

Q.6 Is there any immunity to a person chargeable with tax in case of fraud/suppression of facts/ willful mis- statement, who pays the amount of demand along-with interest before issue of notice?

Ans. Yes. Person chargeable with tax, shall have an option to pay the tax amount of tax along with interest and penalty equal to 15% percent of the tax involved, as ascertained either on his own or ascertained by the proper officer, and on such payment, no notice shall be issued with respect to the tax paid as per Sec.74(6) of the CGST Act,2017.

Q.7 If notice is issued under Section.74 and thereafter the noticee makes payment is there any need to adjudicate the case?

Ans. Where the person to whom a notice has been issued under sub-section 7(1) of Section 74 , pays the tax along with interest with penalty equal to 25% of such tax within 30 days of issue of notice, all proceedings in respect of such notice shall be deemed to be concluded as per Sec.74(8) of CGST Act,2017.

Q.8 In case a notice is adjudicated under 74 and order issued confirming tax demand and penalty, does the notice have any option to pay reduced penalty?

Ans. Yes, If any person pays the tax determined by the order along with interest and penalty equivalent to 50% of such tax within thirty days of the communication of order, all proceedings in respect of the said tax shall be deemed to be concluded as per Sec.74(11) of CGST Act,2017.

Q.9 What will happen in cases where notice is issued but order has not been passed under Sec.73 & 74 within time specified for adjudication under these sections?

Ans. Section 75(10) provides for deemed conclusion of the adjudication proceedings if the order is not passed within time limit prescribed under these sections.

Q.10 What happens if a person collects tax from another person but does not deposit the same with Government?

Ans. It is mandatory to pay amount, collected from other person representing tax under this act, to the government. For any such amount not so paid , proper officer may issue Show Cause Notice for recovery of such amount and penalty equivalent to such amount as per Sec.77(1&2) of CGST Act,2017.

Q.11 In case the person does not deposit tax collected in contravention of Section 76(1), what is the proper course of action to be taken?

Ans. Show Cause Notice may be issued and if so, an order shall be passed following Principles of natural justice within one year of date of issue of such notice as per Sec.76(2 to6) of the CGST Act,2017.

Q.12. What is the time limit to issue notice in case under Section 76 i.e. taxes collected but not paid to Government?

Ans. There is n time limit. Notice can be issued on detection of such cases without any time limit.

Q..13. What are the modes of recovery of tax available to the proper officer?

Ans. The Proper officer may recover the dues in following manner:-

- Deduction of dues form the amount owned by the tax authorities payable to such person,

- Recovery by way of detaining and selling any goods belonging to such person,

- Recovery from other person, from whom money is due or ay become due to such person or who holds or may subsequently hold money for or on account of such person, to pay to the credit of the Central or a State Government.

- Distrain any movable property belonging to such person , until the amount payable is paid. If the dues not paid within 30 days, the said property is to be sold and with the proceeds of such sale the amount payable and cost of sale shall be recovered.

- Through the Collector of the district in which such person owns any property or resides or carries on his business , as if it was an arrear of land recovery,

- By way of an application to the appropriate Magistrate who in turn shall proceed to recover the amount as if it were a fine imposed by him.

- Through enforcing the bond/ instrument executed under this Act or any rules or regulations made there under,

- CGST arrears can be recovered as an arrear of SGST and vice versa as per Sec.79(1,2,3,and 4) of CGST Act.

Q.14 Whether the payment of tax dues can be made in installments?

Ans. On receipt of any such request, Commissioner/Chief Commissioner may extend the time for payment or allow payment of any amount due under the Act, other than the amount due as per the liability self-assessed in any return, by such person in monthly installments not exceeding twenty-four, subject to payment of interest under section 50 with such limitations and conditions as may be prescribed . However, where there is default in payment of any one installment on its due date , the whole outstanding balance payable on such date shall become payable and recovered without any further notice as per Sec.80 of CGST Act.

Q.15 What is the course of recovery in cases where the tax demand confirmed is enhanced in appeal/revision proceedings?

Ans. The notice of demand is required to be observed only in respect of the enhanced dues. In so far as the amount already confirmed prior to disposal of appeal/revision, the recovery proceedings may be continued from the stage at which such proceedings stood immediately before such disposal of appeal / revision as per Sec84(a) of CGST Act.

Q.16 If a taxable person with pending tax dues, transfers his business to another erson, what would happen to the tax dues?

Ans. The person, to whom the business is transferred , shall jointly and severally be liable to pay the tax, interest or penalty due form the taxable person up to the time of such transfer, whether such dues has been determined before such transfer, but has remained unpaid or is determined thereafter as per Sec.85(1) of CGST Act,2017.

Q.17 What happens to tax dues where the Company (taxable person) goes into liquidation?

Ans. When any company is wound up, every appointed receiver of assets(“Liquidator”) shall give intimation of his appointment to Commissioner within 30 days. On receipt of such intimation Commissioner may notify amount sufficient to recover tax liabilities/dues to the liquidator within 3 months as per Sec88(1,2) as per CGST Act,2017.

Q.18 What is the liability of director of the Company ( taxable person) under liquidation?

Ans. When ay private company is wound u and any tax or other dues determined whether before or after liquidation that remains unrecovered, every person who was a director of the company during the period for which the tax was due, shall jointly and severally be liable for payment of dues unless he proves to the satisfaction of the Commissioner that such non-recovery is not attributed to any gross neglect, misfeasance or breach of duties on his part in relation to the affairs of the Company as per Sec.88(3),89 of CGST Act,2017.

Q.19 What is the liability of partners of a partnership firm(Taxable person) to pay outstanding tax?

Ans. Partners of any firm shall jointly and severally be liable for payment of any tax, interest or penalty. Firm/partner shall intimate the retirement of any partner to the Commissioner by a notice in writing. Liability to pay tax, interest or penalty up to the date of such retirement, whether determined on that date or subsequently, shall be on such partner.

If no intimation is given within one month from the date of retirement, the liability of such partner shall, continue until the date on which such intimation is received by the Commissioner as per Section 90 of CGST Act,2017.

Q.20 What happens to the tax liability of a taxable person, whose business is carried on by any guardian/trustee or agent of a minor?

Ans. Where the business in respect of which any tax is payable is carried on by any guardian/ trustee/agent of a minor or other incapacitated person on behalf of and for the benefit of such minor / incapacitated person, the tax, interest or penalty shall be levied upon and recoverable from such guardian /trustee/agent as Sec.91 of CGST Act,2017.

Q.21 What happens when the estate of a taxable person is under the control of Court of Wards?

Ans. Where the estate of a taxable person owning a business in respect of which any tax, interest or penalty is payable is under the control of the Court of Wards/ Administrator General/ Official Trustee/ Receiver or Manager appointed under any order of a Court, the tax, interest or penalty shall be levied and recoverable from such Court of Wards/Administrator General/ Official Trustee/ Receiver or Manager to the same text as it would be determined and recoverable from a taxable person as per Sec92 of CGST Act,2017.

Here with I am providing my notes on what is the procedure you have to follow to file reply in Form GST DRC-06 in practical manner under Sec.73 &74 under GST Law,2017, to know by our tax professionals in their day to day profession.

Filing Form GST DRC-06 against Proceedings initiated by tax officer U/s.73 and 74 related to determination of Tax.

A).How Can I file Form GST DRC-06 against proceedings initiated against me, by tax officer, U/s.73 and 74 related to determination of tax?

To file Form GST DRC-06 against proceedings initiated against you, by Tax Officer, u/s 73 and 74 related to determination of tax, perform following steps:

i) Navigate to view additional Notices/Orders page to view Notices and orders issued against you by Adjudicating or Assessing Authority (A/A) .

ii) Take action using Notices tax of Case Details screen: View issued Notices.

iii) Take action using Replies tax of Case Details screen: View/Add your reply (Form GST DRC-06) to the issued Notice.

iv) Take action using Orders tab of Case Details screen: View issued Order.

Click each hyperlink above to know more.

> Take action using Notices tab of Case Details screen: View Issued Notices.

To view issued Notices, perform following steps:

> On the Case Details page of that particular Case ID, select the NOTICES tab, if it is not selected by default. This tab displays all the notices (SCN/Statement/Reminder/Adjournment) issued by A/A to you.

Click the document name(s) in the Attachments section of the table to download into your machine and view them.

> Take action using Replies tax of Case Details screen: View/Add your reply (Form GST DRC-06) to the issued Notice.

To view or add your reply (Form GST DRC-06) to the issued Notice, perform following steps:

Note: Once the Tax Officer has issued SCN against your case and you are unable to make payment within 30 days of SCN, you must file your Reply in Form GST DRC-06.

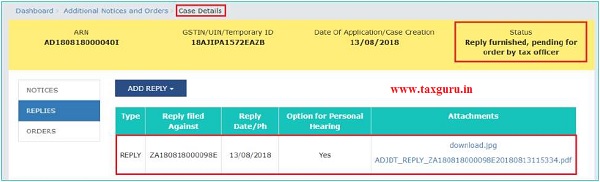

B.On the Case Details page of that particular taxpayer, select the REPLIES tab. This tab will display the replies you will file against the Notices issued by A/A. To add a reply, click ADD REPLY and select REPLY.

Note: Current Status as displayed is “Pending for reply by taxpayer”. It will change once you add your reply.

C.REPLY page is displayed. Type, Date of SCN, SCN Ref No, Financial Year fields are auto-populated. Enter details in the other fields as mentioned in the following steps. To go to the previous page, click BACK.

> In the Personal Hearing Required? field, select Yes or No.

Note: This button is visible to only those taxpayers where the A/A has not called for a personal hearing in the issued notice.

> In Reply field, enter details of your reply to the issued notice.

> Click Choose File to upload the document(s) related to your reply, if any. This is not a mandatory field.

> Enter Verification details. Select the declaration check-box and select the name of the authorized signatory. Based on your selection, the fields Designation/Status and Date (current date) gets auto-populated. Enter the name of the place where you are filing this reply.

Click PREVIEW to download and review your reply. Once you are satisfied, click FILE.

> Submit Application page is displayed. Click ISSUE WITH DSC or ISSUE WITH EVC.

> Notices and Orders page is displayed with the generated Reference number. To download the filed reply, click the Click here hyperlink. Then, click OK.

> The updated REPLIES tab is displayed, with the record of the filed reply in a table and with the Status updated to “Reply furnished, Pending for order by tax officer”. You can also click the documents in the Attachments section of the table to download them.

Note: Once you file your reply successfully, following actions take place on the GST Portal:

You will receive acknowledgement intimation via your registered email and SMS, along with the generated RFN.

Your Reply will be available on A/A’s dash board.

Go back to the Main Menu:

> Take action using Orders tab of Case Details screen. View Order Issued against your case.

> To download order issued against your case, perform following steps:

> On the Case Details page of that particular Case ID, click the ORDERS tab. This tab provides you an option to view the issued order, with all its attached documents, in PDF mode.

> Click the document(s) in the Attachments section of the table to download and view them.

What are the records to be verified by the GST Audit Team of CGST or SGST Department.

Dear Colleagues, if you have received notice from the authorized person of CGST or SGST authority for conduct audit under Sec.73 & 74 under GST Law,2017, you have to submit these following documents to the authorized person for complete audit under GST Law,2017.

1. Cash Book/ or Day Book (from 1’st July,2017 to date of notice received from the audit officer),

2. General Ledger (from 1’st July,2017 to date of notice received from the audit officer),

3. Purchase Ledger (from 1’st July,2017 to date of notice received from the audit officer),

4. Sale Ledger (from 1’st July,2017 to date of notice received from the audit officer),

5. Details of Capital goods purchased and claim of ITC details and sale of any capital goods and output tax paid challan etc., from 1’st July,2017 to date of notice received from the audit officer,

6. Bank Statement for the period from 1’st July,2017 to date of notice received from the audit officer,

7. If works contractor, copies of agreements for the tax period from 1’st July,2017 to date of notice received from the audit officer,

8. Details of R.A. Bills (M.Book copies)and Tax Invoices for the tax period from 1’st July,2017 to date of notice received from the audit officer),

9. Copies of GST GSTR-3B returns for the tax period from 1’st July,2017 to date of notice received from the audit officer,

10. Copies of GSTR-1 returns for the tax period from 1’st July,2017 to date of notice received from the audit officer.

11. Copies of GSTR-2A returns for the tax period from 1’st July,2017 to date of notice received from the audit officer,

12. Details with documentary evidence of RCM payments for the tax period from 1’st July,2017 to date of notice received from the audit officer)

13. Copies of Income Tax Returns for the financial year 2017-18 &2018-19.

14. Copies of TDS returns for the tax period from 1’st July,2017 to date of notice received from the audit officer ( In case of works contractors),

15. Copy of the GST registration certificate along with additional place of business , Branch, Godown etc.,with the State and Out of State,

16. Copies of E –Way bills along with statement for the tax period from 1’st July,2017 to date of notice received from the audit officer,

17. Copies of Delivery Challans and Tax Invoices for the tax period from 1’st July,2017 to date of notice received from the audit officer),

18. Copies of export documents along with Bill of Lading, Bill of Entries for the tax period from 1’st July,2017 to date of notice received from the audit officer,

19. Copies of Tran-I & Tran II returns along with details of workings filed for the audit period.

20. Details of vacant site or godown and commercial complex has given on lease bases/rental basis for commercial purposes for the tax period from 1’st July,2017 to date of notice received from the audit officer,

21. Details of land given for lease for cultivation of commercial crop for the tax period from 1’st July,2017 to date of notice received from the audit officer),

22. Details of any amendments in registration or authorized person or natural of business in registration certificate for the tax period from 1’st July,2017 to date of notice received from the audit officer),

How to verify the documents by the authorized person for completion of audit.

(1) Important Documents:

(i) Copy of the GST Registration Certificate: They have to refer about incorporation of Business Addresses, Godown addresses, Branch addresses within the State and Out of States which belongs to same PAN number holder and cross check details of application form uploaded at the time of migration or applied for fresh registration from GSTIN Site with your clients user i. d. and password of regular taxable persons.

(ii) If your client is a composition dealer they have to verify GST registration certificate and application for composition.

(iii) They have verified Copy of Income Tax Return for the financial year 2016-17 &2018-19 filed before I.T. Authority along with Annexures.

(iv) Copy of Bank account /Accounts and cross check with PAN Number about to know how many bank accounts has been maintained through Indian Bank site.

(v) They have verified Books of accounts either manual, computer etc., along with other records like branch accounts with in the State and Out of States, Goodown registers etc.,

(vi) They have to verify copies of “TAX INVOICES” along with Purchase Orders ( In case of Companies, Partnership firms). If it is a company obtain copy of the Memorandum and Articles of Association, If it is a partnership firm obtain copy of the Partnership Deed.

(vii) They have verified copies of other State GSTIN certificates and verify such certificate details with GSTIN about whether he has incorporated all the branches or not within the State and out of State.

(viii) They to verify Copies of VAT Returns, CST Returns, Services Tax Returns and Central Excise Returns for the tax periods April,2017 to June’2017 of H.O and Branch offices etc.,

(ix) They have to verify Copies of GSTR-3B, GSTR-1, GSTR-2A, GSTR-4 and GSTR-6, etc., for the tax periods from July’2017 to March’2019 or as on date of notice issued..

(x) They have verified list of salaried employees for the above mentioned period along with Labour registration certificate, salary slips etc., ,if any out source employees salaries is their,then verified whether they have paid RCM or not.

(xi) They have verified copy of the “ Rental Agreement/s of Principal Place of business premises, Goodowns, Branches etc., verify with GSTIN registration certificate whether they shown all the business addresses in GSTIN Registration Certificate of places of business of your client.

(xii) They have verified details about immovable properties shown in balance sheet for the financial year 2017-18 and 2018-19 or up to date of notice issued and also ask them about if any assets omitted in Balance Sheet for the above mentioned period.

(xiii) They have verified details about if he has any other part time business like LIC agent, Real-estate commission business, Photo stat business, Sim card agencies , collection agent business, or worked as an agent or Commission agent to any taxable person or company etc.,

(xiv) They have verified details about vehicles like travel car business, Tour operator business, Lorry transport business etc., for the above period and also check with Aadhar Card/ PAN Card through Transport Department site.

(xv) They have verified import and export licenses and verify what are the commodities that are incorporated in DGFT application and what are the commodities that are imported or exported or check whether import or export of goods or services.

(xvi) They have verified if your client is having manufacturing activity then check with about Job work issues and such job worker is having GSTIN registration or not. If job worker is not having registration under GST Law, you have to check whether he has incorporated such Job work addresses in your client GSTIN registration certificate.

(xvii) If your client is having import or export of goods or services or both , then you have to obtain Import invoice, Bill of Entry, IGST paid or not and obtain LUT copy . If he is having export activities of goods or services then obtain Export Invoice, other documents like Bill of Lading, BRC copy etc.,

(xviii) If your client is having export activities of goods or services obtain the details of refund claim details for the tax periods from July’2017 to March’2018 and 2018-19 or up to date of notice issued along with copies of RFD-01,2,3,4, etc., and work about total eligible refund out of which how much refund he has received and how much refund is due form the department for the above period. If any variations are identified during the audit, note in audit report and discuss with your client.

(xix) If your client is having branches with in the State or out of State then check whether he is having registration as Input Service Distributor under GST Law. If he is having branches, then check about distribution of ITC branch wise transaction and relevant ITC claim and expenses etc ., and also check about passing the entries in the respective branch books of accounts and GSTR 3B and GSTR-1 etc., for the above period.

(2) Verification Part from the records:

(a) TAX INVOICES/ Bill of Supply :

(i) Place of Supply: You have to verify “ PLACE OF SUPPLY” on the Tax Invoices. Because most of the taxpayers are not following to fill up place of supply coloum in the TAX INVOICE. As per GST Law,2017 Place of supply is most important aspect to fix appropriate tax rate under appropriate Act (IGST,CGST,SGST/UTGST/CESS Laws).

(ii) Time of Supply: You have to verify “ Time of Supply” on the TaxInvoice” Because most of the tax payers are not followed to fill up “TIME OF SUPPLY” coloum in the TAX INVOICE. As per GST Law,2017 Time of Supply also important aspect to claim of ITC as per Sec.16 ,17 and 18 of CGST Law,2017.

(iii) Classification of goods or services: You have to check about classification aspect. Because it is also most important area for verification. Most of the tax payers are not having knowledge about ‘Classification of goods or services. Whatever transactions made by them whether such transaction comes either supply of goods or supply of services under GST Law. Most of the accountants are not verifying ‘tax Invoice”about what is the rate of tax applied by his client on such supply and also not having knowledge on theory of Classification and not verified before preparation of books of accounts about what is the rate of tax attract on such supply of goods or services under GST Law,2017. Classification of Goods or Services is most important aspect because the rate of tax on such transaction is depending upon the classification. Normally dealers and accountants both are not having an experience in classification because GST Law is new act.

So, we have to verify each and every transaction of your client with Tax Invoice and relevant documents like E way bill, Delivery Challan, Bill of Lading etc., (Here with I am providing my notes on theory of classification for better understanding as per law).

(iv) Advances received against supply of services: This is also an important area for verification under GST Law, Because such advances are taxable under section 9(4) of GST Law,2017. In my observation most of the tax payers are not paying tax on advances received “against supply of Services”. They are having an impression that section 9(4) of CGST Law suspended from 13.10.2017. But Sec.9 (4) suspended on advances received against supply of goods only not services. Especially works contractors are not paying taxes on advances received against supply of services. Especially Works Contract services, they are not paid GST Tax on the above mentioned receipts under RCM under GST aw,2017.

(v) Tax payable under Reverse Charge Mechanism as per Sec.9(3) of CGST Act,2017: This area is also an most important under GST Law. Because as per Sec.9 (3) of CGST Law,2017. GST Tax is applicable on inward supply of goods from unregistered persons by registered taxable person as per Notification No. 12/2017 Dated. 28.06.2017 like GTA, Legal charges paid to an advocate, Sponsorship services, Director Services, Insurance Agent Services, Recovery Agent Services, transfer or pertaining the use or enjoyment of a copy right. Further Notification No.4/2017 dt. 28th June ‘2017, these following inward supply of goods (Purchase from URD) made from un-registered taxable persons are liable to tax under Sec.9(3) of GST Law,2017. Like Cashew nuts(not shell or peeled), Tobacco leaves, Silk Yarn, Raw Cotton, Supply of Lottery and nay used, Seized and confiscated goods, vehicles , waste and scrap etc .,purchased form the Government department.

(vi) Rental Income received on any commercial immovable property : This chapter is most important because it is new concept under GST law. So, you have to check your clients bank account, Postal Pass books etc,. about any income received on commercial properties, vacant land , Any flats were given to run Government offices, Private offices, Educational Institutions from Degree and above, Agricultural land given for commercial crop and received yearly income etc.,

(vii) Form Tran-1,Tran-II under GST Law: You have to verify the details relating to closing stock as on date of 30.06.2017 as per books of accounts and compare with TRAN-1 filed by your client. You have to verify opening stock as on date of 01.04.2017 as per Income Tax Return filed before I.T Authorities along with Books of accounts closed as on 31.03.2017. Prepare closing stock statement as per below formula:

Opening Stock of goods as on 01.04.2017 as per I.T. return : XXXXX

Add: Purchases from 1’st April,2017 to 30th June’2017 as per books : XXXXX

Total Stock as on 30.06.2017 : XXXXXX

Less: Put to sale : XXXXXX

Closing Stock Value as on 30.06.2017 : XXXXXX

Sales from 01.04.2017 to 30.06.2017 : XXXXXXXXXXXXXXX

Less: Latest G.P . as per Latest I.T. return: XXXXXXXXXXXXXXX

(Formula: Total Sales*Rate of G.P.

100+ Rate of G.P ________________

Put to Sale will be arrive based on the above formula: XXXXXXXXXXXXXXX

So, Now they have to verify stock value as per books of accounts and compare with TRAN-1 filed by your client.

Profit & Loss Account Items:

1. Opening Stock: They have to obtain previously filed Income Tax Return and verify the closing stock value adopted in Profit and Loss Account and Balance Sheet as on 31.3.2017 and compare with “ Physical Stock Register” and General Ledger, observe if there is any difference and rectify in the books of accounts and GSTR-1 and GSTR 3B on or before Sept’2018 and prepare in excel sheet such omissions and additions for the period 01.07.2017 to 31.03.2018 but rectified in subsequently tax period or Sept’2018 GSTR-1,GSTR-3B mention it in your notes on accounts and discuss with management and report in appropriate coloum in GSTR-9 and 9C .

2. Purchases (a): They have to obtain Original Tax Invoices and verify 100% Tax Invoices for the tax periods from April’2017 to June’2017 for claim of ITC and compare with VAT 200 returns and Ledger of the VAT department. (Available in APVAT official Site) and confirm about ITC credit balance for the month of June’2017 and compare with TRANS-1 filed by your client and also noted date of filing of TRAN-1,TRAN-2 and whether passed entries in the books of accounts are not, if passed kidney verify TRAN-1.

3. Inward Supply of goods (Purchases) (b) : They have to obtain 100% tax invoices and verify Place of Supply, Time of Supply, Classification of HSN Code and whether he can apply correct rate of tax or not and under concerned Acts based on place of supply , like IGST,CGST,SGST and UTGST Acts or not for the tax period from 1st July,2017 to 31st March,2018.

If any mistake is observed mention in your notes on accounts and discuss with the management and rectify and correct it before prepare Profit & Loss Account.

4. Inward supply of Goods Return (Purchase Returns): They have to verify books of accounts and observe that your client’s return. Some of the goods to the supplier and whether he received any Credit note or Tax Invoice with GST or not and mention in your notes on accounts and discuss with management and rectify such mistakes and pass necessary entries in the books of accounts and finalize Profit and Loss Account. You have to verify whether your client is reversed ITC claim on such goods returned or not and also verify whether he has received TAX Invoice for such return goods because as per GST Law TAX invoice shall be raised by supplier only , recipient has no right to raise any TAX invoice for such return goods.

5. Claim of Input Tax on inward supply of Goods (Purchases): They have to obtain and verify 100% Tax Invoices and whether he can claim ITC as per Law or not and whether he can revert ITC as per Sec.17& 18 of the CGST Act,2017 with GSTR-3B return for the tax periods from July’2017 to March’2018 and 2018-19 or up to notice issued and also with the books of accounts about passing of respective entries or not.

6. Credit and Debit Notes: They have to obtain 100% original Credit and Debit Notes from 01.07.2017 to 31.03.2018 and verify narration of the credit note and debit notes and purpose of the raising of credit and debit notes by supplier and obtain any written agreement or document regarding Discounts, Incentives etc., Because some of the discounts and incentives are taxable under GST and liable to GST Tax if they are not paid .

7. Advance Received or Advance payments from 01.07.2017 to12.10.2017,against supply of goods: They have to verify books of accounts with bank accounts and Advance Voucher or P.O. copies and whether any advance is received against supply of goods or services from 01.07.2017 to 12.10.2017 because your client is liable to pay GST Tax on advances received against supply of goods or services under GST Law and verify whether he applied correct rate of Tax or not on advances received as per appropriate Acts, like IGST,CGST,SGST and UTGST . If they are not paid, mention the same in your notes and inform to management and try to make payment along with Interest.

8. Advance Received by Works Contractor : They have to verify books of accounts with bank accounts about any advances received towards mobilization advance or advance for payment against R A R Bill from 01.07.2017 to 31.03.2018 because your client is liable to pay GST tax on advances received against RA Bill or mobilization advance etc., and verify whether he applied correct rate of tax r not on such advances received as per appropriate Acts, like IGST,CGST,SGST and UTGST Acts. If he is not paid, mention the same in your notes and inform to management and try to make payment along with interest.

9. Loading and Unloading Charges: They have to verify 100% vouchers with GSTR-3B and GSTR-1 returns in this regard because RCM is applicable under Sec.9(4) of the CGST Act,2017 from 01.07.2017 to 12.10.2017. If he is not paid you have to mentioned in your notes on accounts and inform to the management and make payment along with Interest and mention it in

“ Annual Return”.

10. Fright Charges paid on inward supply of goods : They have to obtain LR’s ,RR and Consignment notes and verify 100% voucher with GSTR-3B and GSTR-1 returns in this regard because RCM is applicable under Sec.9(3) of the CGST Act,2017 verify from 01.07.2017 to 31.03.2018 . If he is not paid you have to mention in your notes on accounts and inform to the management and make payment along with Interest and mentioned in “ Annual Return”.

11. Out ward Supply of goods (Sales) : They have to obtain 100% “ Tax Invoices” in respect of Place of Supply, Time of Supply, Whether he has mentioned appropriate classification HSN Code for goods or services or both and he has to apply correct rate of Tax as per concerned Acts based on place of supply as per GST Law,2017 or not. If any mistake is observed mention in your notes and discuss with the management and pay the tax to the government under concerned Acts, like IGST,CGST,SGST and UTGST Acts . Verify if your client has received any interest from his recipients for late payment of amounts against supply of goods or services. Because as per GST Law, Such Interest amount will be considered as part of consideration ( part of Value of supply) and liable to GST Tax. Regarding rate of tax , Your client on which invoice he has received interest and what is the rate of tax applied in that TAX INVOICE, such rate is applicable on interest component and also supplier has to raise invoice along with Interest and mentioned full details. So, you have to note such issues in your report.

12. Handling Charges paid on inward supply of goods : They have to verify books of accounts and 100% vouchers regarding payment of handling charges for the period 01.07.2017 to 12.10.2017 because RCM is applicable on such expenses under Sec.9(4) of the CGST Act,2017 , If he is not paid tax for the above mentioned period you have to mentioned in your notes on accounts and inform to the management and try to make payment along with Interest .

13. Supply of good on credit basis: They have to verify 100% tax invoices with books of accounts and bank accounts and find whether your client has received consideration on his supplies from the recipient with 180 days from the date of invoices. If not received whether he has to inform to recipient to reversal of ITC on particular Tax Invoice and also he can reverse of Tax payment made under appropriate GST Acts after 181 days in GSTR-3B and GSTR-1 and whether he has uploaded or not. If he is not reversed you have to mention in your notes and inform to the management and try to pass reversal entries and if any interest is liable try to remit to the government authorities along with Interest.

14. Rent paid on business premises or godown : They have to verify from the books of account about payment of rent on business premises or godown to the owner (Supplier ) whether he has raised invoice for rent on business premises or godown with GST tax or not . If supplier has not raised invoice with GST Tax, recipient has to prepare tax invoice for rent paid and GST tax under RCM from 01.07.2017 to 12.10.2017 as per Sec.9(4) of the CGST Act,2017. You have to mention it in notes on accounts and inform to the management and try to make payment for that period along with Interest.

15. Advertisement Charges: They have to verify from the books of accounts about payment of any advertisement charges , if he is having advertisement charges invoice without GST ,under that circumstances he has to pay GST Tax on RCM under Sec.9(4) of CGST Act ,2017 from 01.07.2017 to 12.10.2017 and raise tax invoice for that expenses and make payment along with Interest to the government in appropriate Acts like IGST, CGST, SGST and UTGST Acts.

16. Salaries to out sourcing employees: They have to verify from the books of accounts about this expense , if he paid any salaries to out sourcing employees with out labour rolls then he has to pay GST Tax on that payments under RCM as per Sec.9(4) of CGST Act,2017 from 01.07.2017 to 12.102017. Under that circumstances you have to mention in your notes on accounts and inform to the management and raise tax invoice for that payments and pay tax along with Interest to the Government under appropriate Acts like IGST,CGST,SGST and UTGST Acts.

17. ITC claim on capital goods: They have to verify books of accounts about depreciation charged with or without tax component. If he has claimed ITC on that capital goods then verify depreciation account in the Balance Sheet whether depreciation calculated on tax component or not. If he has to calculate depreciation on tax component then you have to advice to revert ITC claim and pay ITC claim amount along with Interest to the government under appropriate acts like IGST,CGST,SGST and UTGST Acts.

18. Inputs purchased and used in manufactured of exempted goods , On Free Supplies and taxable goods: They have to verify in the books of accounts along with manufacturing accounts or production accounts and verify ITC claim and observe that ITC relating to exempted goods reversed or not.

If he has claimed total ITC on purchase of Inputs then you have to instruct to reversal of ITC to the extent of exempted goods and mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate acts like IGST,CGST,SGST and UTGST Acts.

19. Vehicles, Computers, Laptops etc., purchased and booked in business accounts but used for personal: They have to verify in the books of accounts and ITC account and if observed any ITC claim in the books of accounts then you have to instruct him for reversal of ITC to the extent of personal use and pass accounting entries in the books of accounts and make the payment to the government along with Interest under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

20. Convenience charges paid: They have to verify about this payments in the books of accounts and observed if any expenses incurred under this head of account then verify whether he has paid GST on RCM or not for the period 01.07.2017 to 12.10.2017. If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

21. Job Work and Labour charges: : They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST on RCM or not for the period 01.07.2017 to 12.10.2017under GST Law.. If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

22. Sales promotion and business promotion expenses: They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST are not under RCM as per Sec.9(4) of the CGST Act,2017 for the period 01.07.2017 to 12.10.2017.. If he is not paid then mention it in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

23. Bank charges and Service charges recovered by the bank: They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST under RCM or not for the period 01.07.2017 to 12.10.2017 under Sec9(4) of the GST Law.. If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

24. Payment to advocate fee: They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST TAX on Payment to advocate under RCM or not under Sec.9(3) of the GST Law. If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

25. Commission paid : They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST on RCM or not for the period 01.07.2017 to 12.10.2017 under Sec.9(4). If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

26. Payment to sponsorship fee: They have to verify about this payments in the books of accounts and observe if any expenses incurred under this head of account then verify whether he has paid GST on RCM under Sec.9(3) of the GST Law or not for the period 01.07.2017 to 31.03.2018.If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

27. Free Gifts to employees or partners etc., They have to verify about this payments in the books of accounts and observed if any expenses incurred under this head of account then verify whether he has paid GST under Sec.9(4) of the GST Law as RCM or not for the period 01.07.2017 to 12.10.2017. If he is not paid then mention in your notes on accounts and inform to the management and try to make payment along with Interest to the government under appropriate Acts like IGST,CGST, SGST and UTGST Acts.

28. Penalties or Interest on delayed payment of taxes: They have to verify about this expenditure in the books of accounts and deny as an expenditure as per Income tax Act,1962 because any penalty or interest paid on violation of act is not permitted as business expenditure.

29. Obtain creditors and debtors ledger accounts relating business or profession taxable person : They have to obtain ledger copies of creditors and debtors relating to business and compare with books of accounts and observe if there is any difference then mention in your notes on accounts and inform to the management and rectify such omissions and finalize profit & loss account.

30. Verification of E way Bills for movement of goods: They have to verify E way Bills generation for movement of goods for Intra-State and Inter-State Movement of goods with quantity details, taxable value and tax component , GSTIN numbers of Supplier and Recipient etc., with inward and out ward details etc., with ledger accounts of the client. Verify during the period of July’2017 to March’2018 whether your client has paid any penalties against violation of Act on the above subject ,such penalties are reported in your GSTR- 9 and 9C.

31. If the client is a service provider like Contractor for Civil works, Repair and maintains etc.,: They have to verify the terms and conditions of the agreement, P.O copies and verify RA bills raised by your client and supply of goods or services and verify classification of SC codes and applicable rate of taxes and eligibility of ITC claim on Capital Goods like machinery, earth moving equipment etc., and inputs purchased etc. Verify if invoices rose in the month as per terms and conditions of the contract and whether he has received any mobilization advances from the recipient for the period from 01.07.2017 to 31.03.2018 and charged GST tax on such advances and paid to the appropriate department as per GST Law. Verify invoices details for place of supply, time of supply and classification SAC code and applicable rate of tax etc., properly as per GST Law.

Author Bio

INNOCENT ARE DECLARED FRAUD IT IS DEFAMATORY

Can recovery proceedings be initiated for late filling of GSTR-10 with a late fine of Rs. 10,000/- who is a NIL Return filler for the F.Y. 2017-18. Doesn’t it unfair to levy such huge amount just for the delay and that too for a case where no transactions were carried out in the books of accounts for the whole year.

Thanks explained very well

Thank you 🤝

very valuable and to the point information. I personally appreciate your commitment for the welfare and well wishes of the tax society in the form of sharing knowledge with our tax practitioners.