CA Shshank Saurav

Goods and Service Tax – Understanding the legal and procedural requirements

Background – Goods and Service Tax (GST) constitution amendment bill has received the assent of the president and constitution of GST Council has also been notified. Biggest ever indirect tax reform is expected to become reality from April 1, 2017.

Objective– To understand the reporting requirements under proposed legislation so that teams can start working on development of necessary IT infrastructure.

Federal structure of taxation

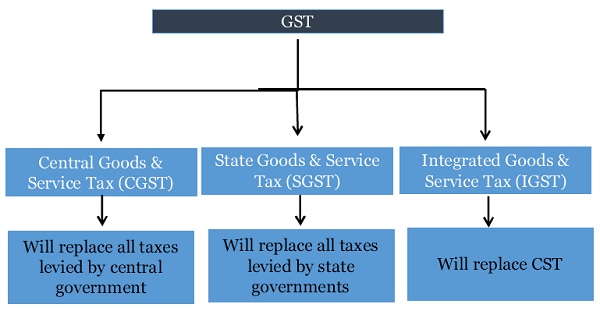

Taxes to be subsumed under GST and dual structure of GST

| CGST | SGST | IGST |

| Central excise duty | Sales tax/VAT | Taxes levied in the course of interstate trade (i.e. Central Sales Tax) and taxes levied in the course of import. |

| Additional excise duty | Entertainment tax (except levied by local authorities) | |

| The Excise Duty levied under the Medicinal and Toiletries Preparations (Excise Duties) Act 1955 | Luxury tax | |

| Service tax | Taxes on lottery, betting and gambling | |

| Countervailing Duty (CVD) | Octroi & entry tax | |

| Spl. Add. Duty – 4% | Purchase tax | |

| Surcharges & cess levied by central government | Surcharges & cess levied by state government |

Scheme of levy

1.GST is levied on Supply of goods or services. Concept of sale is not relevant in GST regime and definition of supply as given u/s 3 is inclusive under GST regime.

2.GST law also provides for tax on reverse charge.

3.Imported goods would be liable to custom duty along with IGST (equivalent to IGST on similar goods in India).

4.Small scale exemption is given person carrying business and having turnover of Rs. 10 lakh or less. This limit is not applicable in case of reverse charge.

5.Composition scheme is also provided in the law as an option to the dealer whose turnover doesn’t exceed Rs. 50 lakh. However this option is not available to person making inter-state supply. The person buying goods/services from a dealer who has opted composition scheme can’t take credit of taxes levied under the scheme.

6.Supply without consideration is also liable to GST. Amount on which tax will be charged will be determined as per valuation rules.

7.Transaction between principle-agent will be liable to tax.

8.Provisions relating to job work u/s 43A are almost similar to current regime (notification 214/86 dated 25 March 186).

9.Specific provision made for E-Commerce dealers (named aggregators in the GST law) under Chapter -XIB.

10. Tax liability under arises on supply of goods/services under GST. Section 12 and section 13 provides when supply of goods & services will be deemed as taken place.

| Goods u/s 12 | Reverse charge – Goods

u/s 12 |

Services u/s 13 | Reverse charge – Services u/s 13 |

| Earliest of the following- | Earliest of the following- | 1. Earlier of date of issue of invoice or receipt of payment (if invoice issued within prescribed period) | Earliest of the following- |

| 1. When goods are removed by supplier | 1. Receipt of goods | 2. Earlier of completion of service or receipt of payment (if invoice issued within prescribed period) | 1. Receipt of goods |

| 2. When goods are made available to the recipient | 2. Date of payment | 3. Date shown by recipient in his books | 2. Date of payment |

| 3. When supplier issues invoice | 3. Date of receipt of invoice | 4. Specific provisions made for continuous supply of services | 3. Date of receipt of invoice |

| 4. Supplier receives the payment | 4. Date of debit in books | 4. Date of debit in books | |

| 5. Recipient shows receipt in his books |

Classification of Goods Vs Services : Controversy is expected to end!

GST is expected to neutralize the difference of tax incidence between goods and services and currently there is ambiguity over classification of some transactions (practice vary from state to state). Some of the important aspects are-

1.Currently software is taxed as goods as well services and classification remains a controversial issues. Draft GST law has classified software as services [Section 5(d) of Schedule II].

2.Under the existing regime, both VAT & Service tax is charged on work contract. Some states provide for deduction of tax at source in case of work contract. Draft GST law provides that work contract will be classified as service [Section 5(f) of Schedule II].

3.Permit to use intellectual property (IPR) is now classified as service [Section 5(c) of Schedule II].

4.Activity of leasing of goods classified as service [Section 5(g) of Schedule II].

For definition Download Below file

https://taxguru.in/wp-content/uploads/2016/09/Definations-GST.pdf

Scheme of credit mechanism

1.CGST – Rates will be uniform across India for goods & services covered under GST.

2.SGST – Rates may vary for different states as the state government has authority to declare any particular good as “Declared Goods” in that particular state. However central government has shared the draft SGST law and rates will be decided by GST Council and therefore consistency across various geographies is expected.

3.IGST- It will be sum total of CGST & SGST .

Chronology of utilising credit

- GST was expected to facilitate seamless credit of inputs and input services however the draft law doesn’t provide so and there are certain technical aspects under Cenvat which have been carried in GST regime also. It may have cascading effect.

- Credit of capital goods can now be taken in one year as against 50-50 rule under Cenvat Credit. Definition of capital goods remains more or less same under GST also.

- Credit of Inputs and Input Services can be taken only when these are used or intended to be used by a supplier for making an outward supply in the course or furtherance of business. This condition can lead to denial of credit in various cases.

- Credit can be taken only when gods/services are received by the supplier. Condition for taking credit in case of goods is similar to existing Cenvat Rules but condition of receipt of service may pose practical challenges as services are intangible in nature.

- Credit is not available after one year from the date of issue of tax invoice. Additionally tax credit for any financial year can’t be taken after 30 September or date of filing of return whichever is earlier (due date for filing of annual return is 31st December of next FY) . Accordingly company management has to ensure that invoices are received and accounted in a timely manner.

- Inputs or input services which are used for personal consumption (e.g. canteen rent, medical insurance, outdoor catering etc.) will continue to be disallowed under GST regime also.

Transition of credit existing as at last date of existing scheme

Cenvat credit or VAT credit as per the last return would get transferred to “GST electronic credit ledger account” of the taxpayer. If any amount is not claimed in the last return then it can’t be claimed under GST regime.

Scheme of distribution of IGST credit among center and state

GST is a destination based consumption tax in which the state where goods/services are consumed will be the ultimate beneficiary for taxes paid by its residents. Transfer of credit among centre and states will happen through GSTN Let’s assume X of Uttar Pradesh sales goods to Y of Uttar Pradesh who in turns sales it to Z of Bihar and the applicable CGST is 12% and SGST is 14% then credit will be distributed in the following manner.

| X (UP) | Y (UP) | Z (Bihar) |

| X sales goods to Y for Rs. 10 lakh | Y sales goods to Z for Rs. 10.5 lakhs | Z sales goods to customer for Rs. 11 lakh (final customer) |

| CGST @12% = Rs. 1.2 lakh

SGST @14% = Rs. 1.4 lakh |

Output tax payable by Y-

IGST @26% = Rs. 2.73 Lakh |

Output tax payable by Z-

CGST @12% = Rs. 1.32 lakh SGST @14% = Rs. 1.54 lakh |

| Input credit taken by Y

CGST = Rs. 1.2 lakh SGST = Rs. 1.4 lakh |

Input credit taken by Z

IGST = Rs. 2.73 lakh |

|

| Amount payable in cash after adjusting the input credit Rs. 2.6 lakh = Rs. 13K | Amount payable in cash after adjusting the input credit Rs. 2.73 lakh = Rs. 13K | |

| State of Uttar Pradesh will transfer Rs. 1.2 lakh to Centre which is used as credit by Y for paying IGST.

GSTN will transfer the SGST of Rs. 1.26 lakh to Bihar which was used by seller in Bihar as input credit (IGST credit). |

||

Procedural aspects

1.Registration – Registration is mandatory for dealers having turnover over the specified limit. Dealers who are already registered with state VAT/sales tax authorities would be granted temporary registration number automatically under the GST regime and they have to get the permanent registration number within 6 months from the date GST becomes effective.

Dealers would be allotted PAN based 15 digit alpha numeric registration number and separate registration is required for each state in which dealer is having business.

2. Returns and their periodicity- Various returns are required to be filed with authorities (through GSTN) on prescribed frequency.

3. Payment of taxes- Payment over Rs. 10K will be made through online banking by accessing GSTN for challan generation.

4. Refund of taxes- It is recommended that option to procure duty free goods for exports to be discontinued and exporter should claim refund of taxes paid on inputs. Refund claim will be processed online and theoretically process & timeline of getting the refund is expected to streamlined.

All the above aspects are discussed in detail in subsequent Paragraphs

| Activity | Remarks | Format |

| Registration | i.Registration number will be of 15 digits

ii.State wise registration to be taken iii.Multiple registrations within a state for business verticals is allowed iv.Auto registration for already registered dealers which shall be valid for 6 months |

Annexure III Application for registration under GST.pdf |

| v. Various digits of PAN based registration denote the following-

-First two: State code -Next ten: PAN of the person -Thirteenth: Entity code -Fourteenth: Blank -Fifteenth: Check digit |

Structure of GST Registration No. | |

| vi. If there are change in the particulars of entity subsequent to registration then intimation to be sent to department | Annexure VII Application for Amendment in GST Registration |

–

| Return/Ledger | Purpose | Due date | Format |

| GSTR1 | Outward supplies made by taxpayer

(other than compounding taxpayer and ISD) [as per section 25] |

10th of next month | GSTR-1 Outward Supplies Made by the Taxpayer |

| GSTR Z | Inward supplies received by a taxpayer (other than a compounding taxpayer and ISD) [as per section 26] | 15th of next month | GSTR Z Inward supplies received by a taxpayer |

| GSTR 3 | Monthly return (other than compounding taxpayer and ISD) [as per section 27] | 20th of next month | GSTR 3 Monthly return.pdf |

| GSTR 4 | Quarterly return for compounding

Taxpayer |

18thof the month next to quarter | Applicable for small entities opting for compounding option |

| GSTR 5 | Periodic return by Non-Resident Foreign Taxpayer | Last day of registration | Not applicable for resident taxpayers |

| GSTR 6 | Return for Input Service Distributor (ISD) | 15th of the next month | ISD is very uncommon |

| GSTR 7 | Return for Tax Deducted at Source [as per section 37] | 10th of the next month | GSTR 7 TDS Return |

| GSTR 8 | Annual Return | By 31st December of next FY | GSTR 8 Annual Return |

| ITC Ledger of taxpayer | Running ledgers (in the nature of PLA existing under excise laws) | Continuous | ITC , CASH and Tax Ledger of taxpayer |

| Cash Ledger of taxpayer | |||

| Tax ledger of taxpayer |

Note:

- A reconciliation in the prescribed format is required to be submitted for value of supplies declared in the return furnished for the year with the audited annual financial statement. This reconciliation statement has to be verified by a chartered accountant.

- As per section 29 of the GST law, input credit claimed by the dealer will be matched with the return filed by other dealer.

Payment of taxes- Payment over Rs. 10K will be made through online banking by accessing GSTN for challan generation. Following process will be followed for payment of taxes-

1.Visit the GSTN and create draft challan

2.Upon creation of the draft challan, the taxpayer will fill in the details of the taxes that are to be paid. The challan page will have sets of mandatory fields, which the user has to provide. The tax payer will have the option to pay CGST, IGST, Additional Tax and SGST concurrently. Generate the final challan after filling all the details.

3.The challan so generated will have a 14-digit (yymm followed by 10-digit) Unique Common Portal Identification Number (CPIN).

4.Select the bank for making the payment. GSTN will share the relevant details (like GSTIN, CPIN, challan amount, relevant state etc.) on a real time basis with bank.

5.After successful payment, challan identification number (CIN) will be generated against CPIN.

Download Format of Annexure IV GST Payment challan

https://taxguru.in/wp-content/uploads/2016/09/Annexure-IV-GST-Challan.pdf.

Refund of taxes- It is recommended that option to procure duty free goods for exports to be discontinued and exporter should claim refund of taxes paid on inputs. Refund claim will be processed online and theoretically process & timeline of getting the refund is expected to streamlined.

Refund will be given in cases like export, unutilized credit, completion of assessment etc. In case of refund relating to input/input services used for export, the time limit for filing refund claim is one year from the date of export and the refund claim has to be certified by a chartered accountant. Principle of unjust enrichment is applicable in case of all refunds.

Download Format of refund application

https://taxguru.in/wp-content/uploads/2016/09/Refund-Claim-Form-Under-GST.pdf

Download Format of refund order

https://taxguru.in/wp-content/uploads/2016/09/Refund-Order-Under-GST.pdf

(Author can be reached at shshanksaurav@gmail.com)