Several goods are taken out of India on consignment basis for exhibitions or other export promotion events. These goods are sold only when approved by the prospective customers abroad. The unsold goods are then brought back to India. This is a widespread practice in various sectors, including the gems and jewelry industry.

Exporters of these items were facing problems due to the lack of clarity on the procedure to be followed under GST at the time of taking these goods out of India and at the time of their subsequent sale or return to India. Taking cognizance of these problems and in order to help exporters, the Central Board of Indirect Taxes and Customs (CBIC) has now issued a comprehensive clarification in this regard vide Circular No. 108/27/2019-GST dated 18.07.2019.

Clarifications:

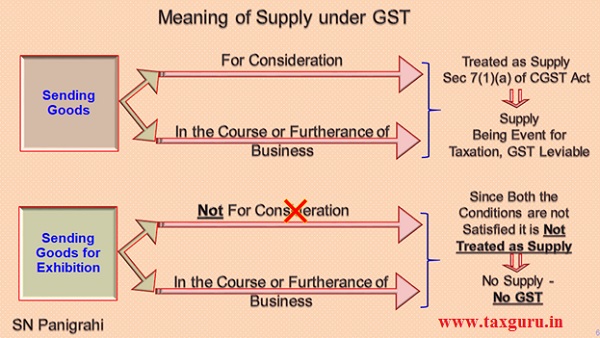

It is clarified that the activity of sending / taking the goods out of India for exhibition or on consignment basis for export promotion, except when such activity satisfy the tests laid down in Schedule I of the CGST Act (hereinafter referred to as the “specified goods”), do not constitute supply as the said activity does not fall within the scope of section 7 of the CGST Act as there is no consideration at that point in time. Since such activity is not a supply, the same cannot be considered as ‘Zero Rated Supply’ as per the provisions contained in section 16 of the IGST Act.

Understanding the applicability of ‘supply’ and ‘zero-rated supply’

In the circular, the Central Board of Indirect Taxes and Customs (CBEC) clarified that any activity/transaction would be treated as ‘supply’ only if the following two conditions are satisfied:

- Such activity/transaction should be done for consideration; and

- Such activity/transaction should be done in the course or furtherance of the business.

When the goods are sent/taken out of India for exhibition or on the consignment basis for export promotion, the same would not come within the ambit of ‘supply’ in as much as there is no consideration involved at any point of time.

With regard to the applicability of ‘zero-rated supply’, it has been clarified that only ‘supplies’ which are either export or are supply to Special Economic Zone unit/developer would qualify as zero-rated supply.

Since the goods sent/taken out of India does not qualify as ‘supply’, consequently, the same would also not qualify as ‘zero-rated supply’.

Further Clarifications

Since the activity of sending / taking specified goods out of India is not a supply, doubts have been raised by the trade and industry on issues relating to maintenance of records, issuance of delivery challan / tax invoice etc. These issues have been examined and the clarification on each of these points is as under: –

Issue : 1

Whether any records are required to be maintained by registered person for sending / taking specified goods out of India?

Clarification

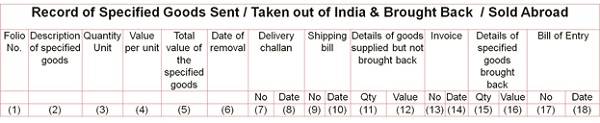

The registered person dealing in specified goods shall maintain a record of such goods as per the format at Annexure to this Circular.

Issue : 2

What is the documentation required for sending / taking the specified goods out of India?

Clarifications

a) As clarified above, the activity of sending / taking specified goods out of India is not a supply.

b) The said activity is in the nature of “sale on approval basis” wherein the goods are sent / taken outside India for the approval of the person located abroad and it is only when the said goods are approved that the actual supply from the exporter located in India to the importer located abroad takes place. The activity of sending / taking specified goods is covered under the provisions of sub-section (7) of section 31 of the CGST Act read with rule 55 of Central Goods & Services Tax Rules, 2017 (hereinafter referred to as the “CGST Rules”).

c) The specified goods shall be accompanied with a delivery challan issued in accordance with the provisions contained in rule 55 of the CGST Rules.

d) As clarified in paragraph 6 above, the activity of sending / taking specified goods out of India is not a zero-rated supply. That being the case, execution of a bond or L UT, as required under section 16 of the I GST Act, is not required.

Issue : 3

When is the supply of specified goods sent / taken out of India said to take place?

Clarifications

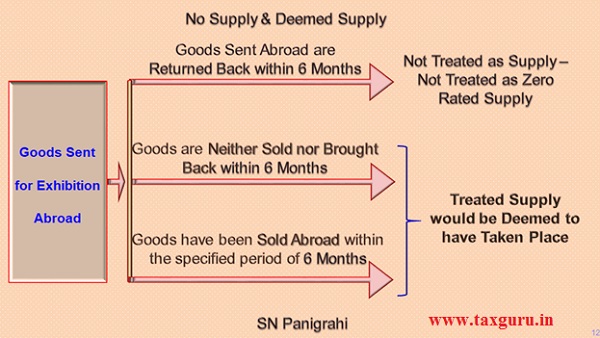

a) The specified goods sent / taken out of India are required to be either sold or brought back within the stipulated period of six months from the date of removal as per the provisions contained in sub‑ section (7) of section 31 of the CGST Act.

b) The supply would be deemed to have taken place, on the expiry of six months from the date of removal, if the specified goods are neither sold abroad nor brought back within the said period.

c) If the specified goods are sold abroad, fully or partially, within the specified period of six months, the supply is effected, in respect of quantity so sold, on the date of such sale.

Issue : 4

Whether invoice is required to be issued when the specified goods sent / taken out of India are not brought back, either fully or partially, within the stipulated period?

Clarifications

a) When the specified goods sent / taken out of India have been sold fully or partially, within the stipulated period of six months, as laid down in sub-section (7) of section 31 of the CGST Act, the sender shall issue a tax invoice in respect of such quantity of specified goods which has been sold abroad, in accordance with the provisions contained in section 12 and section 31 of the CGST Act read with rule 46 of the CGST Rules.

b) When the specified goods sent / taken out of India have neither been sold nor brought back, either fully or partially, within the stipulated period of six months, as laid down in sub-section (7) of section 31 of the CGST Act, the sender shall issue a tax invoice on the date of expiry of six months from the date of removal, in respect of such quantity of specified goods which have neither been sold nor brought back, in accordance with the provisions contained in section 12 and section 31 of the CGST Act read with rule 46 of the CGST Rules.

Issue : 5

Whether the refund claims can be preferred in respect of specified

goods sent / taken out of India but not brought back?

Clarifications

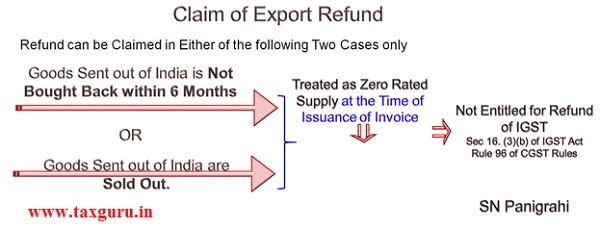

a) As clarified in para 5 above, the activity of sending /taking specified goods out of India is not a zero-rated supply. That being the case, the sender of goods cannot prefer any refund claim when the specified goods are sent / taken out of India

b) It has further been clarified in answer to question no. 3 above that the supply would be deemed to have taken place:

(i) on the date of expiry of six months from the date of removal, if the specified goods are neither sold nor brought back within the said period; or

(ii) on the date of sale, in respect of such quantity of specified goods which have been sold abroad within the specified period of six months

c) It is clarified accordingly that the sender can prefer refund claim even when the specified goods were sent / taken out of India without execution of a bond or LUT, if he is otherwise eligible for refund as per the provisions contained in sub-section (3) of section 54 the CGST Act read with sub-rule (4) of rule 89 of the CGST Rules, in respect of zero rated supply of goods after he has issued the tax invoice on the dates as has been clarified in answer to the question no. 4 above. It is further clarified that refund claim cannot be preferred under rule 96 of CGST Rules as supply is taking place at a time after the goods have already been sent / taken out of India earlier.

Refund Claim

Question of refund claim arises only in the following two cases:

- Goods sent out of India is not bought back within the stipulated time of 6 months; or

- Goods sent out of India are sold out.

As seen above, goods sent / taken out of India is not covered within the scope of ‘zero-rated supply’ and hence accordingly execution of a bond or LUT is not required.

With regard to the refund claim it has been clarified that, even if the sender has not executed bond or LUT, he would be eligible for refund claim as per provisions of section 54(3) read with rule 89(4) of the CGST Rules.

However, refund claim cannot be filed under rule 96 of the CGST Rules reason being the supply has taken place at a time after the goods have already been sent / taken out of India.

Illustrations

Case – 1

i) M/s ABC sends 100 units of specified goods out of India. The activity of merely sending / taking such specified goods out of India is not a supply.

ii) No tax invoice is required to be issued in this case but the specified goods shall be accompanied with a delivery challan issued in accordance with the provisions contained in rule 55 of the CGST Rules.

iii) In case the entire quantity of specified goods is brought back within the stipulated period of six months from the date of removal, no tax invoice is required to be issued as no supply has taken place in such a case.

iv) In case, however, the entire quantity of specified goods is neither sold nor brought back within six months from the date of removal, a tax invoice would be required to be issued for entire 100 units of specified goods in accordance with the provisions contained in section 12 and section 31 of the CGST Act read with rule 46 of the CGST Rules within the time period stipulated under sub-section (7) of section 31 of the CGST Act.

Case – 2

M/s ABC sends 100 units of specified goods out of India. The activity of sending / taking such specified goods out of India is not a supply.

No tax invoice is required to be issued in this case but the specified goods shall be accompanied with a delivery challan issued in accordance with the provisions contained in rule 55 of the CGST Rules. If 10 units of specified goods are sold abroad say after one month of sending / taking out and another 50 units are sold say after two months of sending / taking out, a tax invoice would be required to be issued for 10 units and 50 units, as the case may be, at the time of each of such sale in accordance with the provisions contained in section 12 and section 31 of the CGST Act read with rule 46 of the CGST Rules.

If the remaining 40 units are not brought back within the stipulated period of six months from the date of removal, a tax invoice would be required to be issued for 40 units in accordance with the provisions contained in section 12 and section 31 of the CGST Act read with rule 46 of the CGST Rules.

Further, M/s ABC may claim refund of accumulated input tax credit in accordance with the provisions contained in subsection (3) of section 54 of the CGST Act read with sub-rule (4) of rule 89 of the CGST Rules in respect of zero-rated supply of 60 units.

Summary of The key points clarified in the Circular are as following:

a) The activity of taking goods out of India on consignment basis for exhibition would not in itself constitute a supply under GST since there is no consideration received at this time.

b) The movement of these goods out of India shall be accompanied by a delivery challan issued in accordance with the provisions contained in rule 55 of the CGST Rules.

c) Since taking such goods out of India is not a supply, it necessarily follows that it is also not a zero-rated supply. Therefore, execution of a bond or LUT, as required under section 16 of the IGST Act, is not required.

d) The goods taken out of India in this manner are required to be either sold or brought back within a period of six months from the date of removal.

e) The supply would be deemed to have taken place if the goods are neither sold abroad nor brought back within the period of six months. In this case, the sender shall issue a tax invoice on the date of expiry of six months from the date of removal, in respect of the quantity of goods which have neither been sold nor brought back. The benefit of zero-rating, including refund, shall not be available in respect of such supplies.

f) If the specified goods are sold abroad, fully or partially, within the period of six months, the supply shall be held to have been effected, in respect of the quantity so sold, on the date of such sale. In this case, the sender shall issue a tax invoice in respect of such quantity of goods which has been sold. These supplies shall become zero-rated supplies at the time of issuance of invoice. However, refund in relation to such supplies shall be available only as refund of unutilized ITC and not as refund of IGST.

g) No tax invoice is required to be issued in respect of goods which are brought back to India within the period of six months.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, Corporate Trainer & Author.

Available for Corporate Trainings & Consultancy

Can be reached @ snpanigrahi1963@gmail.com