GEARING UP FOR GOODS AND SERVICES TAX-Vol I

(DRAFT LAW- AT A GLANCE)

“IMPACT AND IMPLICATIONS”

The article (Vol I) broadly covers the various specific provisions related to working and operation of Goods and Services Tax vis-à-vis the statutory requirements of Model Draft law released by Govt w.r.t. concept of Txable event under GST i.e. Supply of goods and services.

The article also brings out the clarity on the various issues addressed in the reports of registration and refund released by the Govt.

As a part of Vol II, other provisions and pending reports will be summarised and issues will be addressed as contemplated in the reports of payment and return issued by Govt.)

Goods and Service Tax-A dual tax system, proposed in the report submitted by the Joint Working Group of the Empowered Committee of the State Finance Ministers in November 2007, was to be implemented in April 2010,one for the Centre and other for the states replacing the state VAT and Cenvat. However the final decision on the time of its implementation is still pending as it is hanging between the ruling and opposition party due to certain undecided terms and conditions.

GST is a value added tax to be levied on both goods and services, except the exempted goods and services. The tax will be levied on the value of the product or service supplied. The taxes levied at the multiple stages such as CENVAT, Central sales tax, State Sales Tax, Octroi etc will be replaced by GST to be introduced at Central and State level.

Why GST- How GST will be better than existing tax structure

The single comprehensive tax is expected to give following advantages over and above the existing tax structure-

- Dual model GST under federal structure i.e. CGST & SGST,

- Elimination of cascading effects of the taxes,

- CGST & SGST to be charged on same price,

- Set-off relief fully captured,

- Destination based tax structure,

- Free movement of goods & service through out the country,

- Applicable to all transactions of Goods & Services with some exceptions,

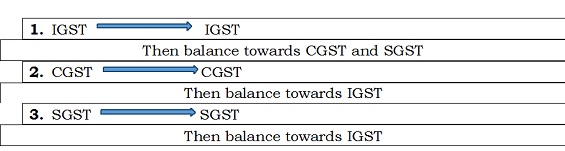

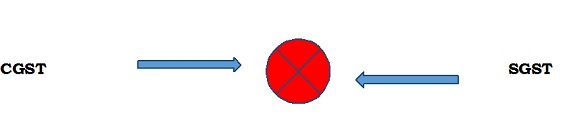

- Input tax credit (ITC) for the CGST/SGST and could be utilized for payment of CGST/SGST, but cross utilization not allowed, except IGST

- Inter State GST (IGST) –new model for Interstate transactions

- It will also improve the International cost competitiveness of native Goods and Services.

Government Has Released Model Draft of Proposed GST Act, 2016 and the 130 page report has been divided into 14 parts, 81 sections, 3 schedules and GST Valuation(Determination of the value of Supply of Goods and Services) Rules 2016.The issues covered in the report broadly covers the following

- Definition of 77 terms

- Meaning and scope of supply of goods and services

- Classes and powers of officers under the act

- Time of supply of goods and services

- Identifying the nature of Supply- interstate or intrastate

- Place of supply of goods and services

- Value of taxable supply

- Manner of taking input tax credit and utilisation thereof

- Remission of tax on supplies found deficient in quantity

- Recovery of tax not paid or short paid or erroneously refunded

- Interest on delayed payment of tax

- Refund of tax and interest on delayed refund

- Registration-amendment, cancellation, revocation

- Accounts and records –tax invoice, credit and debit notes, other records including period of retention

- Furnishing details of inward and outward supplies

- Payment of taxes, penalty, interest and other amounts.

- Offences and penalties.

1. GST applicable on ‘supply of goods and services’

Section 3- Meaning and Scope of Supply

- Supply includes supply of goods and services

- Includes all forms of supplies

- sale

- Transfer

- Barter

- Exchange

- License

- Rental

- Lease

- Disposal

- Importation of services

made or agreed to made For a consideration by a person in the course or furtherance of business

Matters to be treated as supply even without consideration– Schedule 1

- Permanent transfer/ disposal of business assets

- Temporary application of business assets to a private or non business use

- Services put to a private or non business use

- Self supply of goods and or services

- Assets retained after deregistration

Explanation to Schedule II

| Supply of goods | Supply of services |

| 1. Transfer of title of goods

2. Transfer of title of goods under an agreement of transferring property in goods at a future date 3. Transfer of Business Assets with or without any consideration – Which are no longer required By/ under directions of the person carrying on business 4. Transfer of goods included in business assets – Sold by other person who has the power to do – To recover any debt – Owed by taxable person |

1. Transfer of goods / transfer of rights in goods/ undivided share of goods without transferring title of goods.

2. Lease, tenancy, easement, license to occupy land 3. Lease or letting out of the building– commercial, industrial, residential for business/ commerce wholly or partly 4. Treatment/ process applied to another person’s goods 5. Goods held or used for the purposes of business – Put to any private use – Made available to any person for use – For any purpose other than the business purpose – With or without any consideration |

- 2. GST payable as per time of supply

- 3. Determining Place of Supply

- 4. Valuation of Taxable Supply

- 5. Sec 18- Input tax credit in GST- Manner of taking credit and utilisation thereof

- 6. An additional tax upto 1% will be levied by Centre on inter-State supply of goods(and not on services) made for consideration.

- 7. 33 GST laws in India

- 8. Time limit for show cause notices (SCN)

- (the time limit prescribed for issuance of SCN for generic cases is much more than the current time limit prescribe in excise law (i.e. 12 months) and service tax legislation (i.e. 18 months).

- 9. Rate of GST is not yet specified in the draft GST law

2. GST payable as per time of supply

The liability to pay CGST / SGST will arise at the time of supply as determined in the following provisions prescribed separately for Goods and Servoces.

Sec 11- Time of Supply of Goods

1. On the basis of the Movement of Goods

Goods required to be moved-Date on which the goods are removed by the supplier for supply to the buyer

Goods not required to be moved-Date on which goods are made available to the buyer.

2. On the basis of transactions- either of the following

a. Date of issue of invoice by supplier

b. Date of receipt of payment by supplier

c. Date of receipt of goods entered into books of accounts of buyer.

3. On the basis of continuous supply of goods

Successive statement of accounts and payments involved-Date of expiry of period to which it relates

Successive statement of accounts and payments not involved-Date of issue of invoice or Date of receipt of payment whichever is earlier

4. When goods are sent or taken on approval or sale or return or similar terms

In this goods are removed before it is known whether the supply will take place

- Time when it is known that supply has taken place or

- 12 months from the date of removal

Whichever is earlier

5. In any other case

Periodical return has to be filed- Date on which such return has to be filed

Periodical return no to be filed- Date of payment of CGST/ SGST

Sec 12- Time of Supply of Services

1. On the basis of issue of Invoice

- Invoice issued within the prescribed period-Date of issue of invoice or date of receipt of payment whichever is earlier

- Invoice not issued within the prescribed period- Date of completion of provision of service or the date of payment whichever is earlier

- In other case- Date on which the recipient shows the receipt of service in his books of accounts

2. On the basis of continuous supply of services

- If the due date is ascertainable- Date of liability of payment to service provider

- If the due date is not ascertainable- Date of receipt of payment or issue of an invoice whichever is earlier

3. In other situations

| -the payment is linked to the completion of an event | When the event gets completed |

| -if tax is paid on reverse charge basis | Earliest of-

– Date of receipt of services – Date of payment – Date of receipt of invoice – Date of debit in books of accounts |

| Supply ceases before completion of service | At the time of cessation |

4. In any other case

- Periodical return has to be filed- Date on which such return has to be filed

- Periodical return no to be filed- Date of payment of CGST/ SGST

(Sec 13 explains the various situations when there is a change in rate of tax in respect of supply of services)

3. Determining Place of Supply

Typically for ‘goods’ the place of supply would be location where the good are delivered. Whereas for ‘services’ the place of supply would be location of recipient.

Sec 15- Place of supply of Goods

| Distance supply+ Movement of goods | Place of delivery of goods |

| No movement of goods | Place of delivery of goods(handed over to receiver) |

| Assembly/ installation of goods at site | Place of such installation/ assembly |

| Supplied on board/ conveyance/ vessel | Such place |

| Other cases | As recommended by Govt |

Sec 16- Place of Supply of Services

| Immovable property

Restaurant and catering service Artistic/ sporting/scientific/ educational/ Entertainment Transportation of goods Passenger transportation service Board a conveyance/ vessel etc Telecommunication service Banking/ other financial service Insurance services Advertisement services |

Provided to registered person- Location of Service recipient

Not provided to registered person- Location of Service provider |

4. Valuation of Taxable Supply

- GST would be payable on the ‘transaction value’.

- Transaction value is the price actually paid or payable for the said supply of goods and/or services between un-related parties.

- The transaction value is also said to include all expenses in relation to sale such as packing, commission etc.

- Even subsidies linked to supply will be includable.

- As regards discounts/ incentives, it will form part of ‘transaction value’ if it is allowed aftersupply is effected.

- However, discounts/ incentives given before or at the time of supply will be permissible as deduction from transaction value.

Apart from this ,GST Valuation (Determination of the value of Supply of Goods and Services) Rules 2016 have also been provided in the draft law.

5. Sec 18- Input tax credit in GST- Manner of taking credit and utilisation thereof

- Disallows CENVAT Credit on various services such as motor vehicle related services, catering services, employee insurance, constructionof civil structure etc.

- Restrict input tax credit in respect of construction, motor vehicle etc.

- Further, credit is proposed to be denied on goods and/or services used for private or personal consumption, to the extent they are so consumed.

Utilisation of Input Tax Credit

Denial of Cross Utilisation of Input Tax Credit

6. An additional tax upto 1% will be levied by Centre on inter-State supply of goods(and not on services) made for consideration.

- Inter-State branch transfers will not attract this 1% additional Tax.

- Additional tax will be assigned to States from where the supply of goods originates.

- Will be applicable for a period of two years and could be extended further by GST Council.

- The credit of this additional levy will not be available as thus it will be a cost in the supply chain.

7. 33 GST laws in India

- One CGST law

- and 31 SGST law for each of the States including two Union Territories

- and one IGST law governing inter-State supplies of goods and services.

8. Time limit for show cause notices (SCN)

- Time limit for issuance of SCN in generic cases (i.e. other than fraud, suppression etc) would be three years

- and in fraud, suppression etc cases it would be five Years.

(the time limit prescribed for issuance of SCN for generic cases is much more than the current time limit prescribe in excise law (i.e. 12 months) and service tax legislation (i.e. 18 months).

9. Rate of GST is not yet specified in the draft GST law

The rate of GST is not specified in draft GST law. However, various News reports suggest that the Revenue Neutral Rate (RNR) as proposed by the Chief Economic Advisor Shri. Arvind Subramanian could be 17%-18%. Further, there could be lower rate (of 12%-14%) for concessional goods and higher rate (upto 40%) for luxury goods (such as luxury cars, tobacco products etc).

Highlights of the Executive Summary of the Report submitted by Committee headed by the Chief Economic Adviser Dr. Arvind Subramanian on Possible Tax rates under GST

- The term revenue neutral rate (RNR) will refer to that single rate, which preserves revenue at desired (current) levels

- The RNR should be distinguished from the “standard” rate defined as that rate in a GST regime which is applied to all goods and services whose taxation is not explicitly specified.

- On the RNR, the Committee’s view is that the range should between 15 percent and 15.5 percent (Centre and states combined)

- The Committee would recommend that lower rates be kept around 12 per cent (Centre plus states) with standard rates varying between 17 and 18 per cent.

- Demerit rates—other than for alcohol and petroleum (for the states) and tobacco and petroleum (for the Centre)—will have to be provided for within the structure of the GST.

- The Committee recommends that this sin/demerit rate be fixed at about 40 percent (Centre plus states) and apply to luxury cars, aerated beverages, paan masala, and tobacco and tobacco products (for the states).

- If policy objectives have to be met, instruments other than tax exemptions such as direct transfers could be deployed

- Eliminating all taxes on inter-state trade (including the 1 percent additional duty) and replacing them by one GST will be critical to achieving the objective of Make in India

- The proposed structure of tax rates will have minimal inflationary consequences.

- Bringing alcohol and real estate within the scope of the GST would further the government’s objectives of improving governance and reducing black money generation without compromising on states’ fiscal autonomy.

- Bringing electricity and petroleum within the scope of the GST could make Indian manufacturing more competitive

- Eliminating the exemptions on health and education would make tax policy more consistent with social policy objectives

10. Registration Process- Summarised extract on the basis of the report of Empowered Committee

Preliminary

- For each State, the taxable person would have to take a separate registration. No separate registration is required for CGST and IGST. Each taxpayer would be allotted a State wise PAN based 15 digit Goods and Services Taxpayer Identification Number (GSTIN). The registration would be effective from the date of application. The application has to be filed within 30 days from the date of the liability to obtain registration.

- A business entity is allowed to take multiple registrations within a State for each business vertical.

- Input tax credit across Business Verticals is not allowed except for common inputs and input services.

Exemption from Registration

- Any person below the threshold limit will not be required to take registration

- Threshold exemption limit will be calculated based on Gross Annual Turnover on an all-India basis.

- Gross Annual Turnover would include exports and exempted supplies

- Any person having turnover below the threshold exemption limit may apply for voluntary registration.

- Threshold exemption limit would not apply to persons making inter-state supply and persons importing goods/services Individuals importing goods or services for personal consumption need not take registration.

Compounding Scheme

- The registered person can opt to pay GST at a specified percentage of the compounding turnover, without entering the credit chain. Such person can neither claim credit on input nor recover GST from the customers.

- A registered person can switch from this scheme to the normal scheme any time during the year but not during the middle of the financial year.

Application process

- The Goods and Services Tax Network (GSTN) will develop and maintain a GST Common Portal which will serve as the online front end for obtaining registration under the GST regime.

11. Refund Process- Summarised extract on the basis of report of Empowered Committee

Situations where refunds would arise under Central Excise, Service Tax, VAT, CST, etc

- Excess payment of tax due to mistake or inadvertence.

- Export (including deemed export) of goods / services under claim of rebate or Refund of accumulated input credit of duty / tax when goods / services are exported.

- Finalization of provisional assessment.

- Refund of Pre – deposit for filing appeal including refund arising in pursuance of an appellate authority’s order (when the appeal is decided in favor of the appellant).

- Payment of duty / tax during investigation but no/ less liability arises at the time of finalization of investigation / adjudication.

- Refund of tax payment on purchases made by Embassies or UN bodies.

- Credit accumulation due to output being tax exempt or nil-rated.

- Credit accumulation due to inverted duty structure i.e. due to tax rate differential between output and inputs.

- Year-end or volume based incentives provided by the supplier through credit notes.

- Tax Refund for International Tourists

REFUND FORMS

- 4 different types of refund forms are made available for different assesses and cases.

Dates of filing of refund

| Type of refund | Relevant date |

| -Excess payment of tax due to mistake or inadvertence. | Date of payment of GST |

| Export (including deemed export) of goods under claim of rebate or Refund of accumulated input credit of duty / tax when goods are exported. | Date on which proper officer under the Customs Act gives an order for export |

| Finalization of provisional assessment. | Date of finalization of order |

| Export (including deemed export) of services under claim of rebate or Refund of accumulated input credit of duty / tax when services are exported. | Date of BRC |

| Refund of Pre – deposit for filing appeal including refund arising in pursuance of an appellate authority’s order (when the appeal is decided in favor of the appellant). | Date of communication of the order. |

| Payment of duty / tax during investigation but no/ less liability arises at the time of finalization of investigation / adjudication. | Date of communication of adjudication order or order relating to completion of investigation |

| Refund of tax payment on purchases made by Embassies or UN bodies. | Date of payment of GST |

| Credit accumulation in case of liability to pay service tax on partial reverse charge basis. | Date of providing of service(normally the date of invoice) |

| Accumulated ITC on account of inverted duty structure. | Last day of the financial year |

Supporting Documents

- Copy of TR-6 / GAR-7/ PLA / copy of return evidencing payment of duty.

- Copy of invoices (in original) (for the purpose of evidencing the supply of goods and the fact that duty is not reflected in the same).

- Documents evidencing that the tax burden has not been passed on to the buyer.

- Any other document as prescribed by the refund sanctioning authority

Procedure for Refund

– the State Tax authorities shall deal with the SGST refund

– Central Tax authorities shall deal with refund of CGST and IGST.

– The following procedure is proposed in this regard

- Applicant may be given the option of filing refund application either through the GSTN portal or through the respective State / Central Tax portal.

- On filing of the electronic application, a receipt/ acknowledgement number may be generated and communicated to the applicant via SMS and email for future reference.

- A provision may be made to display the application for refund in dealer’s online dashboard when he logs into the system.

- The “carry forward input tax credit” in the return and the cash ledger should get reduced automatically, if the application is filed at GSTN portal itself.

- In case the application is filed at the tax department portal, suitable integration of that portal with GSTN portal should be established to reduce/block the amount before taking up the refund processing.

- It should be clearly mentioned / highlighted that generation of this number does not in any way affirm the legality, correctness or completeness of the refund application

- Since the application for refund is expected to be filed electronically, the application form should have a print option along with the option for the applicant to download the same so that he can store the same for future reference and record.

- it is recommended that the preliminary scrutiny may be carried out within 30 common working days and deficiency, if any, should be communicated to the applicant directly from the respective tax portal.

– every refund application should be examined in light of the principle of “unjust enrichment” and the appropriate provisions may be incorporated in the GST law.

– It is recommended that a Chartered Accountant’s Certificate certifying the fact of non-passing of the GST burden by the taxpayer, being claimed as refund should be called for.

– it is recommended that an amount in the range of Rs. 500-1000/- may be fixed below which refund shall not be granted. This limit should be uniform for both CGST/IGST and SGST.

– It is recommended that looking at the higher level of compliance and self regulating mechanism in the form of system based ITC verification, uploading of sales and purchase invoices, reconciliation, compliance rating etc. post audit of refund application (and not of the accounts of the taxpayer)can be dispensed with if so decided by the respective Tax Jurisdiction for refunds upto Rs. One lakh for normal taxpayers and for refund upto Rs. 2 lakhs for certain prescribed categories of applicants (like public sector undertakings, applicants having the AEO Status, etc.) but the process of review of refund may be provided in the GST Law.

– for refund amounts exceeding a pre-determined amount a provision for pre-audit of refund application (and not of the accounts of the taxpayer) before the sanction of the refund may be provided for.

Interest on Refund

- It is recommended that the GST Law may provide for a prescribed time limit of 90 days from the date of the system generated acknowledgment of refund application within which refund has to be paid. It may also be provided in the GST law that, interest clause will start automatically once the prescribed time limit for sanctioning of refund has been breached.

- It is recommended that the rate of interest for delayed payment of refund and that in case of default in payment of GST should be different.

- The Committee recommends that the rate of interest in case of refund may be around 6% and that in case of default in payment of interest may be around 18%.

Adjustment

- The GST Law may provide for adjusting the refund claim against any amount of un-stayed confirmed demand lying beyond the appeal period.

Challenges ahead

Majority of the parties and co-operation from state government are the biggest challenges in front of the present Govt for implementing the GST as the proposed legislation needs to be passed by a two-third’s majority in both houses of parliament and ratified by more than half of the state assemblies.

Other challenges

- Inclusion of tax rate in the Constitution of India.

- The differences in the structure of the economy and sales tax revenue

- Central Government’s refusal to compensate the states for the loss of revenue arising from reduction in the rate of CST.

- Reluctancy of states to bring certain taxes(such as tax on motor spirit and high speed diesel oil etc) under the ambit of GST.

- Revenue neutral rates of GST at central and state level both.

- Consensus on the exemption list of goods and services considering revenue neutrality and consumer benefit as well.

- Treatment of taxes on services with inter state coverage(such as services related to transportation of passengers or goods in railways or telecom etc)

- Harmonisation of administrative processes with uniform systems, forms and procedures.

“Hope sustains life”

However we should not forget that India has always proved her as a golden region for investments and with economic reforms gaining momentum, prospects for growth and sustainable development in the long term remains bright. For fulfilling the agenda set for reforms, India needs to continue making progress on its domestic front and subsequently encourage investments.

(the figures/ data presented in the article have been taken from the information available on the respective websites of the bodies, the statements given if any, have been produced as given in the press.the extracts of the reports have been taken from the original reports of the empowered committee and the summary of CEA report is totally based on the provisions of the report given by Chief Economic Adviser of India)

Disclaimer- The summary mentioned below has been compiled on the basis of the draft law available on various websites such as www.gstindia.com etc.