FAQs on Filing of Form GST ITC-02

Q 1. What are the pre-conditions for filing of ITC declaration in FORM GST ITC-02?

Ans: The following conditions must be met for being eligible to file the FORM GST ITC-02:

1. In case any registered entity undergoes sale, merger, de-merger, amalgamation, lease or transfer, the acquired entity must file ITC declaration for transfer of ITC in the FORM GST ITC-02.

2. The acquired or transferor entity must have matched Input Tax Credit available in the Electronic Credit Ledger, as on effective date of merger/ acquisition/ amalgamation / lease/ transfer.

3. The acquiring entity (transferee) and the acquired entity (transferor), both should be registered under the GST regime.

4. The acquired entity (transferor) must have validly filed all the returns for the past periods.

5. All transactions categorized as “Pending for action” of the merging entity should be either accepted, rejected or modified and any liabilities arising out of the returns filed by the transferor must be paid.

6. The transfer of business should be with specific provision of transfer of liabilities. It should be accompanied by a certificate issued by Chartered Accountant or Cost Accountant to that effect. Liabilities here would include stayed demands – of tax or in respect of litigation or recovery cases.

Q 2. Which ITC can be transferred by filing FORM GST ITC-02?

Ans: The following ITC can be transferred by filing the FORM GST ITC-02:

1. Matched ITC balance available in the transferor’s Electronic Credit Ledger;

2. Such ITC appearing under the major heads – Central tax, State / UT tax, Integrated tax, and CESS can be transferred by filing FORM GST ITC-02.

The amount of ITC that is provisional or un-matched, cannot be transferred by the Acquired Entity (transferor) using this process.

Q 3. As an acquiring /transferee Entity, can I change my decision once the ACCEPT / REJECT button has been pressed?

Ans: Upon filing of the FORM GST ITC-02 by the acquired entity (transferor), such details are notified to the acquiring (transferee) entity through the GST portal. On acceptance, the un-utilized credit specified in FORM GST ITC-02 will be credited to his Electronic Credit Ledger. The Transferee (acquiring) Entity can change its decision to accept or reject an ITC transfer request any number of times until it is finally submitted by the transferor at the GST portal.

Q 4. What happens to the Electronic Credit Ledgers of Acquired Entity (transferor) as well as the Acquiring Entity (transferee), if the ITC transfer request filed through FORM GST ITC-02 is accepted or rejected in the system?

Ans: If the ITC transfer request of an acquired Entity (transferor), filed through FORM GST ITC-02 is ACCEPTED by the acquiring Merged Entity (transferee), the ITC will be transferred to the transferee, and the Electronic Credit Ledger of the (transferee) Acquiring Entity will get updated.

However, if the ITC transfer request of an acquired entity (transferor), filed through the FORM GST ITC-02 is REJECTED by the acquiring entity (transferee), the ITC will not be transferred to the transferee, and the Electronic Credit Ledger of the acquired entity will receive back the ITC. The Electronic Credit Ledger of the acquiring entity (transferee) will not remain unchanged.

Q 5. In case of demerger how much of the ITC would be transferred to the demerged entity or entities?

Ans: In the case of demerger, the ITC shall be apportioned in the ratio of the value of assets of the new units as specified in the demerger scheme.

Q 6. Which certificate from a practicing Chartered Accountant / Cost Accountant is required for filing FORM GST ITC-02?

Ans: For filing the FORM GST ITC-02, the acquired (transferor) entity must submit and upload a copy of certificate issued by a practicing chartered account or cost accountant, certifying that sale / merger / amalgamation / lease or transfer of business has been done with specific provision for the transfer of liabilities. The FORM GST ITC-02 cannot be filed without such certificate.

How to transfer ITC and file Form GST ITC-02- Manual

How can I transfer the matched unutilized Input Tax Credit available in my Electronic Credit Ledger, in case of sale of business / merger / demerger, resulting in change of constitution of business?

A registered taxpayer can apply for transfer the matched Input Tax Credit available in the Electronic Credit Ledger to another business entity in case of transfer of business by way of sale of business / merger / demerger by filing of ITC declaration in FORM GST ITC-02.

However, there are certain pre-requisites for filing this form. These are:

1. In case any registered entity undergo sale, merger, de-merger, amalgamation, lease or transfer, the acquired entity must file ITC declaration for transfer of ITC in the FORM GST ITC-02.

2. The acquired / transferor entity must have matched Input Tax Credit available in the Electronic Credit Ledger, as on effective date of merger/ acquisition/ amalgamation / lease/ transfer.

3. The acquiring entity (transferee) and acquired entity (transferor), both should be registered under the GST regime.

4. The acquired entity (transferor) must have validly filed all the returns for the past periods.

5. All transactions categorized as pending for action of merging entity should be either accepted / rejected / modified, and any liabilities arising out of the returns filed by the transferor must be paid.

6. The transfer of business should be with specific provision of transfer of liabilities which will be the stayed demands of tax, or in respect of litigation /recovery cases. It should be accompanied by the certificate issued by Chartered Accountant or Cost Accountant.

The process of transferring matched unutilized ITC by filing the FORM GST ITC-02 is broadly divided into two steps:

1. The acquired entity (transferor) files declaration in FORM GST ITC-02 in the GST portal, specifying the available matched ITC in each major head.

2. The acquiring entity (transferee) accepts / rejects the same in GST portal.

This user manual covers both aspects of the whole process.

Steps to be taken by the Acquired Entity (Transferor):

To transfer the matched unutilized ITC by filing the FORM GST ITC-02, please follow the below steps:

1. Access the GST Portal. The GST Home page gets displayed.

2. Using your valid credentials, login to the GST Portal. The Taxpayer’s Dashboard (transferor) gets displayed.

3. Navigate to the Services> Returns > ITC Forms option. The GST ITC Forms page gets displayed.

4. Click the Prepare Online button on the GST ITC-02 tile.

Notes:

- The FORM GST ITC-02 opens-up.

- The amounts of matched unused ITC get auto-filled from the transferor’s Electronic Credit Ledger.

- Transferor may choose to transfer all or partial ITC, as desired. For each major head, the Amount of matched ITC to be transferred needs to be filled by the transferor.

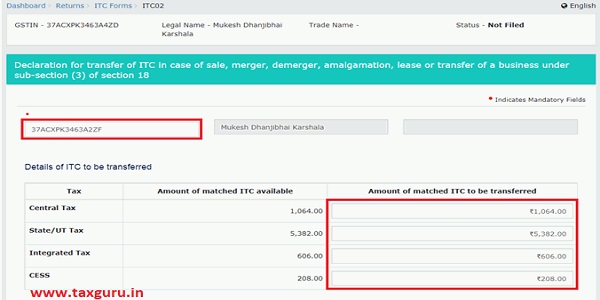

5. Enter the GSTIN of the transferee.

6. Enter the Amount of matched ITC to be transferred for each major head under the Details of ITC to be transferred section. The entered amount must be less than or equal to the amount of ITC that is shown as available in the Electronic Credit Ledger.

7. Under the section on Particulars of certifying Chartered Accountant or Cost Accountant, the acquired entity (transferor) needs to specify the details of a certificate from a practicing chartered accountant or cost accountant, certifying that the sale / merger / amalgamation / lease or transfer of business has been done with specific provision of the Act and Rules. Enter the following details:

a) Name of the certifying accounting firm.

b) Name of the certifying Chartered Accountant / Cost Accountant in the certifying firm.

c) Membership number of the certifying firm.

d) Date of certificate issued by the certifying accounting firm.

8. Attach a scanned copy of the certificate.

Notes:

- The attachment should either be in JPEG / PDF format.

- File size of attachment should not exceed 500 KB.

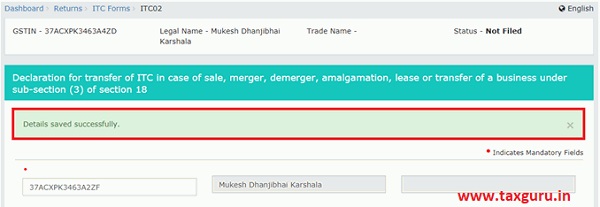

9. Click SAVE to upload the entered data and the attachment to the GST Portal.

Notes:

- The system will display a confirmation upon saving.

- You can save your application at any time.

- After saving the FORM GST ITC-02, if you return to this form at a later point in time, all the line items will get auto-populated as they were saved.

- You can also retrieve the saved FORM GST ITC-02 by navigating to Services à User Services à My Saved Applications.

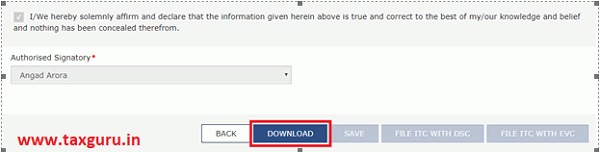

10. Check the statement box to declare that the furnished information is true and correct.

11. Select an Authorised Signatory from the drop-down, containing a list of authorised signatories that you have configured in the system.

12. File the FORM GST ITC-02 either using the DSC or EVC option.

Notes:

- If you choose the DSC option, make sure to sign with the DSC of selected authorised signatory.

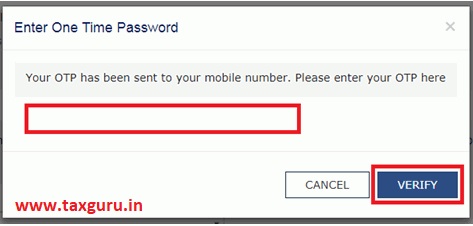

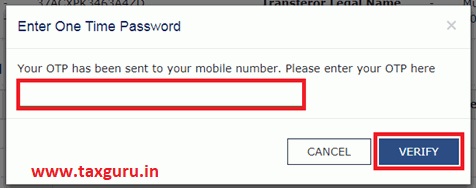

- If you choose the EVC option, the system will send an OTP on the authorised signatory’s registered mobile phone number, which you’ll be required to enter in a pop-up that appears after selecting this option.

- This user manual has assumed the EVC path for simplicity.

13. Click PROCEED on the Warning pop-up message.

14. Enter the OTP as received.

15. Click VERIFY.

Notes:

- The system will display a confirmation message on successful filing of the FORM GST ITC-02.

- The confirmation message will also contain the system-generated ARN.

- You can download an offline copy of the filed FORM GST ITC-02 in PDF version by clicking the DOWNLOAD button.

- In the next stage, the transferee (acquiring unit) of the ITC needs to take an action on your filed FORM GST ITC-02.

Steps to be taken by the Acquiring Entity (Transferee):

After the transferor (or the acquired entity) has filed the FORM GST ITC-02 to transfer the matched unutilized ITC, the transferee (or the acquiring entity) needs to login to the GST Portal and either accept or reject the ITC transfer. To take an action on the transferor’s initiated process of ITC transfer, please follow the below steps:

16. Access the GST Portal and login with your valid credentials.

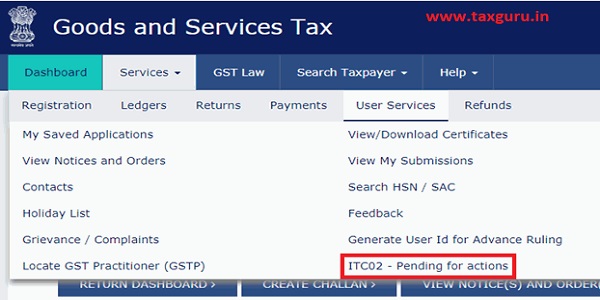

17. Navigate to the Services> User Services> ITC02 – Pending for actions option.

Notes:

- The page, listing the FORM GST ITC-02 will open, requiring you to take action.

- The displayed listing shows:

- A clickable link in the form of ARN.

- The transferor’s GSTIN and Trade Name.

- Date of filing.

- Status.

18. Click the ARN.

Notes:

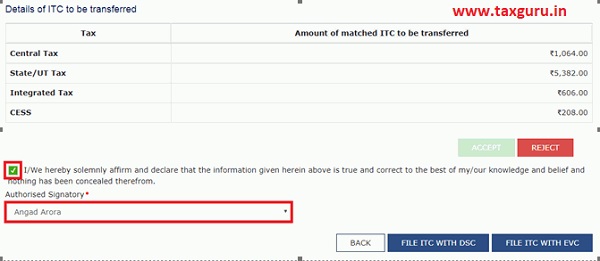

- The filed details of ITC to be transferred corresponding to the selected ARN get displayed.

- The details include the amount of matched ITC to be transferred against each of the major heads – Central Tax, State / UT Tax, Integrated Tax, and CESS.

19. Click either ACCEPT or REJECT based upon the decision that you want to exercise as the transferee.

Notes:

- On ACCEPT: The ITC will be transferred to the transferee, and the Electronic Credit Ledger of the acquiring entity (transferee) will get updated.

- On REJECT: The ITC will not be transferred to the transferee, and the Electronic Credit Ledger of the acquired entity will receive back the ITC. The Electronic Credit Ledger of the merged entity (transferee) will not get affected.

- After clicking ACCEPT / REJECT on this screen, the transferee needs to file his response in the system to complete the process. Simply clicking the ACEEPT / REJECT button without completing the filing steps does not make any changes to Electronic Credit Ledgers of either transferor or transferee.

- This user manual assumes the acceptance of ITC transfer to show the successful completion of the ITC transfer process.

20. Assuming that we have clicked ACCEPT, the system will display a confirmation message, and will prompt the user to proceed with filing the response.

21. Check the declaration to state that the given information is true and correct.

22. Select an Authorised Signatory from the drop-down, containing a list of authorised signatories that you have configured in the system.

23. File the form either using the DSC or EVC option.

Notes:

- If you choose the DSC option, make sure to sign with the DSC of selected authorised signatory.

- If you choose the EVC option, the system will send an OTP on the authorised signatory’s registered mobile phone number, which you’ll be required to enter in a pop-up that appears after selecting this option.

- This user manual has assumed the EVC path for simplicity.

24. Click PROCEED on the Warning pop-up message.

25. Enter the OTP as received.

26. Click VERIFY.

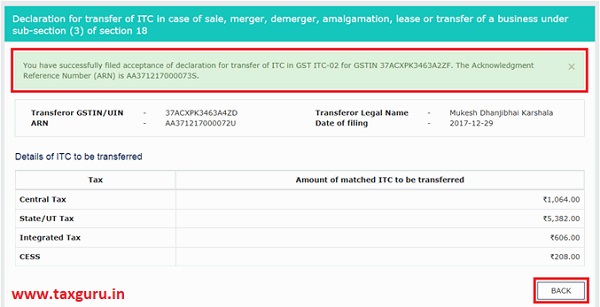

Notes:

- The system will display a confirmation message on successfully completing the ITC transfer process.

- The confirmation message will also contain the system-generated ARN.

27. Click BACK to return to the ITC–02 – Pending for actions screen.

28. Notice the status changes to Accepted.

please share format for CA Certificate for ITC 02.

UNDER GST : HOW TO CHANGE PARTNERSHIP TO PROP.RIETORSHIP AND TRANSFER STOCK AND UNCLAIMED ITC TO NEW PROP.CONCERN.

KINDLY ADVICE HOW TO PROCEED STEP BY STEP.

How many times one could file ITC 02 form to transfer the ITC of existing entity to succeeding entity. Whether there is any chance to file it more than once?

After filing itc 02, stock in gstr 10 is shown nil or with values of stock transferred?

HOW can legal heir file GST ITC 02 for transfer of ITC to his GSTN because he will have to become authorised signatory first. Deptt.is silent on this

Some ITC is taken on the basis of GSTR-2B .In case some supplier filed there GSTR _1 after due date of the month of tranfer,how the ITC will be taken and tranfer?

CA certificate is mandatory or not …if tranfor ITC less than 2 lakh

Yes ca certificate requirement compulsory

We have a similar issue please tell us how to transfer stock in new GSTIN.

I AM GETTTING AN ERROR DOCUMENT EXPIRED. WHAT SHOULD WE DO RECTIFY THAT ERROR?

I am getting the error Certificate has expired in 2 of my clients. Has anyone got any solutions for this?

I am trying to accept but it shows the certificate has expired

Thanks to the author for this very useful article.

1. After filing ITC-02, when can the transferor surrender his GSTIN?

2. Is there any format for the CA certificate regarding the liabilities?

very and knowledgeable article.

at the time of filling Form -02 after verification through evc massage display “Certificate Expired.” please help

As per my knowledge the Rule 41A of CGST which allows the transfer of ITC from existing unit to newly registered business vertical is being effective from 01.02.2019. So please guide what about the units registered prior to this period .

For e.g. , My one unit registered on 01.07.2017 and another unit registered on 27.07.2017 as Business vertical within same state, can I transfer ITC from one unit to another unit through form

ITC-02A.

at the time of filling Form -02 after verification through evc massage display “Certificate Expired.” please help

We are experiencing the same problem. if you got the solution please call me on 9912047744

I GOT The final solution and the above mentioned is my office number. getting many calls on that num. if any one’s case really emergency ping me on 9052020220

On transfer of a ongoing business, there is no IPT for transfer. There is only stock of goods and furniture. Whether the ITC 02 has to be filed?

Is this form ITC02 is it available online or has to be filed in hard copy with the GST authorities

sir is there any time limit for filling itc 02

Proprietor ki death kai baad 30 gst no cancellation karna hote hai us se pehla app us firm ki jitni bi libities or itc or stock wo new firm transfer kar lo but act kahi pr itc2 ki tme limit mention nahi hai

Proprietor ki death kai baad 30 gst no cancellation karna hote hai us se pehla app us firm ki jitni bi libities or itc or stock wo new firm transfer kar lo but act mai kahi pr itc2 ki tme limit mention nahi hai