In a greater relaxation the facility of furnishing LUT extended to all exporters. Exporters were facing difficulties in submission of bonds / Letter of Undertaking (LUT for short) for exporting goods or services or both without payment of integrated tax. Especially small exporters were facing problems as most of them were not eligible for furnishing LUT. As per Notification No. 16/2017-Central Tax dated 7th July, 2017 which extended the facility of export under LUT to status holder as specified in paragraph 5 of the Foreign Trade Policy 2015-2020 and to persons receiving a minimum foreign inward remittance of 10% of the export turnover in the preceding financial year which was not less than Rs. one crore. Alternatively these small exporters either to execute Bond backed by Bank Guarantee or export on payment of IGST.

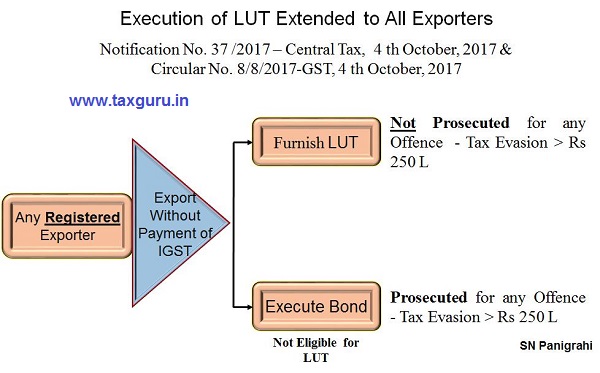

Now in supersession of Notification No. 16/2017 – Central Tax dated 7th July, 2017, a fresh Notification No. 37/2017 – Central Tax dated 4th October, 2017 has been issued which extends the facility of LUT to all exporters under rule 96A of the Central Goods and Services Tax Rules, 2017.

Also in line with the above new notification a Circular No. 8/8/2017-GST, 4 th October, 2017 is also issued by rescinding Circular No. 2/2/2017 – GST dated 5th July, 2017, Circular No. 4/4/2017 – GST dated 7th July, 2017 and Circular No. 5/5/2017 – GST dated 11th August, 2017.

Let us now discuss the Salient features of Notification No. 37/2017 & Notification No. 37/2017

Eligibility to Export under LUT:

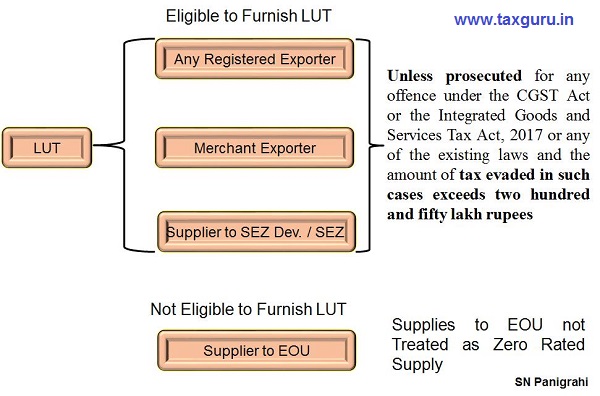

The facility of export under LUT has been now extended to all registered persons who intend to supply goods or services for export without payment of integrated tax except those who have been prosecuted for any offence under the CGST Act or the Integrated Goods and Services Tax Act, 2017 or any of the existing laws and the amount of tax evaded in such cases exceeds two hundred and fifty lakh rupees.

Validity of LUT:

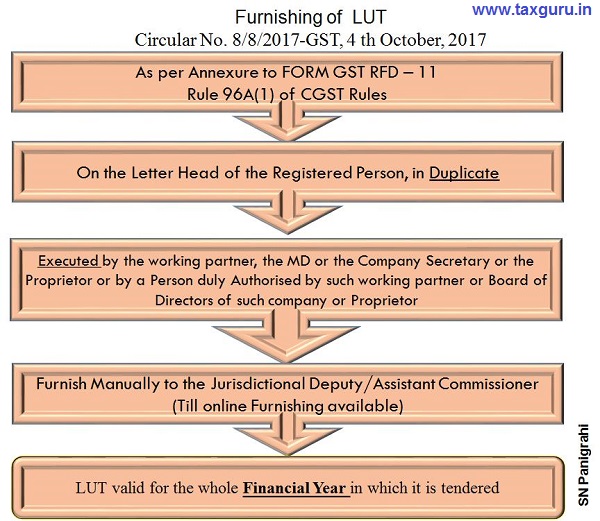

The LUT shall be valid for the whole financial year in which it is tendered.

Withdrawal of LUT Facility :

In case the goods are not exported within the time specified in sub-rule (1) of rule 96A of the CGST Rules and the registered person fails to pay the amount mentioned in the said sub-rule, the facility of export under LUT will be deemed to have been withdrawn.

Restoring the LUT Facility :

If the amount mentioned in the said sub-rule is paid subsequently, the facility of export under LUT shall be restored. As a result, exports, during the period from when the facility to export under LUT is withdrawn till the time the same is restored, shall be either on payment of the applicable integrated tax or under bond with bank guarantee.

Form for bond/LUT:

Till the time FORM GST RFD-11 is available on the common portal, the registered person (exporters) may download the FORM GST RFD-11 from the website of the Central Board of Excise and Customs (www.cbec.gov.in) and furnish the duly filled form to the jurisdictional Deputy/Assistant Commissioner having jurisdiction over their principal place of business.

Self-declaration :

Self-declaration to the effect that the conditions of LUT have been fulfilled shall be accepted unless there is specific information otherwise. That is, self-declaration by the exporter to the effect that he has not been prosecuted should suffice for the purposes of Notification No. 37/2017- Central Tax dated 4 th October, 2017. Verification, if any, may be done on post-facto basis.

Time for acceptance of LUT/Bond:

As LUT/Bond is a priori requirement for export, including exports to a SEZ developer or a SEZ unit, the LUT/bond should be processed on top most priority. It is clarified that LUT/bond should be accepted within a period of three working days of its receipt along with the self-declaration as stated in para 2(d) above by the exporter. If the LUT / bond is not accepted within a period of three working days from the date of submission, it shall deemed to be accepted.

Bank guarantee:

Since the facility of export under LUT has been extended to all registered persons, bond will be required to be furnished by those persons who have been prosecuted for cases involving an amount exceeding Rupees two hundred and fifty lakhs. A bond, in all cases, shall be accompanied by a bank guarantee of 15% of the bond amount.

Payments Made in Indian Currency :

It is clarified that the acceptance of LUT for supplies of goods to Nepal or Bhutan or SEZ developer or SEZ unit will be permissible irrespective of whether the payments are made in Indian currency or convertible foreign exchange as long as they are in accordance with the applicable RBI guidelines. It may also be noted that the supply of services to SEZ developer or SEZ unit under LUT will also be permissible on the same lines. The supply of services, however, to Nepal or Bhutan will be deemed to be export of services only if the payment for such services is received by the supplier in convertible foreign exchange.

Jurisdictional officer:

In exercise of the powers conferred by sub-section (3) of section 5 of the CGST Act, it is hereby stated that the LUT/Bond shall be accepted by the jurisdictional Deputy/Assistant Commissioner having jurisdiction over the principal place Page 5 of 5 of business of the exporter. The exporter is at liberty to furnish the LUT/bond before either the Central Tax Authority or the State Tax Authority till the administrative mechanism for assigning of taxpayers to the respective authority is implemented.

Same Treatment for Supplies to Special Economic Zone developer or Special Economic Zone unit

The provisions of this notification shall mutatis mutandis apply in respect of zero-rated supply of goods or services or both made by a registered person (including a Special Economic Zone developer or Special Economic Zone unit) to a Special Economic Zone developer or Special Economic Zone unit without payment of integrated tax.

Merchant Exporters also Eligible for LUT :

It is clarified that there is no provision for issuance of CT-1 form which enables merchant exporters to purchase goods from a manufacturer without payment of tax under the GST regime. The transaction between a manufacturer and a merchant exporter is in the nature of supply and the same would be subject to GST.

Transactions with EOUs:

Zero rating is not applicable to supplies to EOUs and there is no special dispensation for them under GST regime. Therefore, supplies to EOUs are taxable like any other taxable supplies. EOUs, to the extent of exports, are eligible for zero rating like any other exporter

Comments:

It is in fact a welcome measure in lines of Trust based treatment allowing the facility of LUT for all types of Registered Exporters including Merchant Exporters and suppliers to SEZ Developers & SEZ Units.

It is further suggested to make the facility of furnishing LUT one time instead of furnishing every financial year wise, unless disqualified under the said provisions.

Author : SN Panigrahi, GST Consultant, Practitioner & Trainer

Can be reached @ snpanigrahi1963@gmail.com

Author Bio

What is the effect of decision taken by the GST council on 6th October, 17 as far as waiver of execution of bond/LUT is concerned?

Can we presume that when the requirement of furnishing of bond/LUT has been waived for clearance of goods for export, the exporter is neither required to charge IGST nor he is obliged to furnish bond/LUT?

Dear Panigrahi sir

We are exporting services from long back. LUT is applicable from Jul’17 however we have applied for LUT in Sept’17 . so is there any remedy for us towards the export made in Jul & Aug?

your prompt reply will greatly appreciated.

Sir,

What about company which exports Software.

People say that just including text of

“SUPPLY MEANT FOR EXPORT UNDER BOND OR UNDER LETTER OF UNDERTAKING WITHOUT PAYMENT OF INTEGRATED TAX”

is enough.

Should companies which export softwares apply for LUT or Bond ?

Dear Shri Panigrahi

A very useful and timely article .Please keep posting such good articles.

CA H Venkatesh Rao, Coimbatore

CMA Bhargavi Venkatesh

We have been issued the LUT but all our suppliers have refused to supply goods for export under LUT without payment of IGST.

They have said that their consultants have advised that this is not yet started and so thay cannot supply without paying IGST.

Please advise how to proceed.

Good article.

Sir,

Is this applicable for export of service also?