Why is E-way bill required?

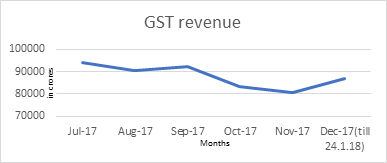

E-way bill had been introduced in VAT regime at the different time in different states with different nomenclature. The intention behind introducing the e-way bill was to check movement of goods. Similarly, e-way bill will be introduced from 1st of February mandatorily across the country for interstate movement of goods. Various communication with media suggests that e-way bill implementation process is expedited because various dealers are evading payment of tax, showing interstate transactions as intrastate transactions, amount of revenue[1] have constantly declined over the period of time and other administrative reason.

Power to introduce e-way bill

As per Central GST act, the government is empowered to make rules for carrying out provisions of the act. Through notification e-way bill rules and forms are notified vide notification 34/2017-Central Tax dated 15 September 2017.

However, vide notification 11/2018-Central Tax, dated, 2 February 2018 Central Board of Excise and Customs have postponed e-way bill provision for the obscure period.

Application and other administrative processes

Government have due to initial technical glitches extended trail phrase and will be mandatory from the date to be announced. Previously, Central Government has issued the notification to generate the e-way bill for inter-state supplies having monetary limit more than Rs.50,000. Further, to support central government step, 6 states have made e-way bill mandatory for intra-state supplies.

E-way bill is required to be filed by the registered person, the registered person can be consigner of the recipient of the supply of consignment, who causes movement of goods where the value of goods is more than Rs. 50,000. Monetary limit of Rs.50000 is mandatory for the registered person, if enrolled under composition scheme. However, the voluntarily e-way bill can be generated for supply without threshold limit of Rs.50,000. On the generation of the e-way bill on the common portal, the unique e-way bill shall be made available to the supplier, the recipient, and the transporter.

E-way bill is mandatory when movement of goods is done on account of –

a. In relation to supply

b. Reason other than supply.

c. Due to inwards supply from an unregistered person

However, specifically in 2 cases registered person is required to required to file e-way bill irrespective of monetary limit –

1. In case of movement of goods between different states where principal and Job worker are in different states

2. In case where handicraft goods are transported between different states and such person is specifically exempted from registration (under Section 23 of Central Goods and Service Tax Act, 2017)

Exemptions to generate e-way bill are also carved out by government, in following cases –

a. Goods specified in the annexure to rule 138(1) – List goods with chapter number along with the description of goods

b. When goods are transported by non-motorized conveyance

c. In case of internal transportation from the port, airport, air cargo complex and land customs station to inland container depot or container freight station for clearance by customs.

d. In case movement of goods within such area as notified by the government. — No such notification is issued.

e. Goods as specified in notification no.2/2017 – Central tax (Rate), part II, section 3, sub-section (i) other than de-oiled cake.

f. Where goods supplied are as mentioned in section 9(2) along with alcoholic liquor for human consumption – Petroleum crude, high-speed diesel, motor spirit, natural gas or aviation turbine fuel (semicolon) and

g. Where goods being transported are treated as no supply under schedule III of the Central Goods and Service Tax Act,

In the case where the e-way bill is generated for any state shall be valid for every state and union territory.

The registered person is required to file e-way bill whether goods are transported in his own conveyance or hired or by railways or by air or by vessel.

To avoid confusion of details used, the government have facilitated to accept/ reject consignment by the registered buyer and in case of inaction by the registered buyer, deemed acceptance will be granted.

Government have provided option to generate consolidated e-way bill in case where multiple consignment are required to be transported in one conveyance, than transporter may indicate the serial number electronically and generate consolidated e-way bill prior to movement of goods.

In case where goods are supplied by unregistered supplier to registered buyer than such movement of goods is deemed to have been caused by registered buyer and should file e-way.

Validity of e-way bill

Validity period of e-way bill or consolidated e-way bill will depend on distance required to be covered by medium of transportation –

| Distance | Validity period |

| Up to 100 kilometers (approx. 62.137 miles) | One day (24 hours) |

| For every 100 kilometers or part thereof thereafter | One additional day (24 hours) |

Such validity can be extended by the commissioner vide notification for certain categories of goods as may be specified.

In the case where the e-way bill is generated, but goods are either not transported or are not transported as per details furnished than the registered person himself or through facilitation center can cancel e-way bill within 24 hours of generation of the e-way bill. However, in case of cancellation will be invalid if the e-way bill is verified in transit under rule 138B.

In the case where goods are of exceptional nature and goods cannot be transported within valid period a transporter may generate another e-way bill after updating sufficient information in GST EWB 01.

Documentation

Following documents are required to be carried by person in charge of conveyance –

a. Invoice or Bill of Supply or delivery challan, as case and

b. Copy of e-way bill or e-way bill number physically or mapped on radio frequency identification device

However, circumstances warranted, commissioner may by notification require person in charge of conveyance to carry following documents –

a. Tax invoice or Bill of Supply or delivery challan and

b. Delivery challan

What is radio frequency identification device

As per Wikipedia, the radio frequency identification device (RFID) uses electromagnetic fields to automatically identify and track tags attached to objects. The tags contain electronically stored information. Further, there are two categories of tags for RFID. Passive tags collect energy from a nearby RFID reader’s interrogating radio waves. Active tags have a local power source (such as a battery) and may operate hundreds of meters from the RFID reader. Unlike a barcode, the tag need not be within the line of sight of the reader, so it may be embedded in the tracked object.

Information Technology preparedness

Government is required to have very smooth IT network to accept e-way bill details. Let’s have the rough estimate of e-way bill suppose to be generated on daily basis – As per data posted on 29 January 2018 on Press Information Bureau, there had been 9.8 million registered taxpayer. If we assume that out of total registered person, following will be number of transaction as per hypothesis –

| Particulars | Numbers |

| Total number of taxpayers | 9.80 million |

| Exclude – Input Service Distributor, service provider and other exclusions (40%) | (3.92 million) |

| Number of taxpayers require filing e-way bill | 5.88 million |

| Number of transaction entered by a supplier on weekly basis | 700 |

| Interstate transactions with respect to transaction entered (50%) | 350 |

| Number of e-way bill expected to generate on weekly basis (5.88 million x 350 transactions) | 2,058 million |

We can assume that number of e-way bills generated on weekly basis will be nearly 1800-2000 million. As across India registered person or transporter will upload details for the e-way bill from various band-with speed. The government should ensure that for all e-way bills get generated within the span of time. In case of the technological glitch or sluggish data fetch, the government should have fortified themselves with the alternative plan. However, they must increase trial period for the indefinite period.

Conclusion

The government was ardent to implement e-way bill for interstate supplies. Further, few states supported central government action to mandatorily generate of the e-way bill.

We appreciate the move of the government to implement e-way bill in phrase wise manner, to make tax evaders handicap. However, on the initial day itself at 7:56 PM government tweeted to rescind the notification for implementation of the e-way bill for indefinite period. Pursuant to this government should consider web server bandwidth, code density of the new site introduced (i.e. www.ewaybillgst.gov.in ), file request and various other technical matter. In case of failure on the government side, business would impact as e-way bill is required to be generated before movement of goods. So, it of paramount importance that next time e-way bill is introduced, rules should have either have the higher monetary limit or technological infrastructure should work favorably for trade and business.

[1] Figures are taken from pib.nic.in

Very informative article.