The GST law is stabilizing with the passage of time. However, the increasing activity of fake invoicing and fraudulent ITC claiming has resulted in the Government initiating several checks and mechanisms on GSTN portal. These actions are aimed at ensuring that genuine and accurate numbers are reported on GSTN portal, reduce the number of litigations, and increase efficient compliance by taxpayers.

In this long list of actions, the government has introduced another feature in the form of “electronic credit reversal and re-claimed statement”. This article summarizes the salient features of this new functionality on the GSTN portal and the possible interpretation of few unclarified points.

1. Statement Overview: Through this statement, starting with August 2023, the GSTN portal will maintain a record of reversal of ITC and re-claimed amount on a tax return period basis to ensure accurate reporting and to curtail the excess ITC re-availment by the taxpayer.

2.Tracking ITC Reversal and Re-claimed Amounts: It will allow easy tracking of ITC that has been reversed in Table 4B(2) – “Others” and thereafter re-claimed in 4A(5) – “All other ITC” and reported in Table 4D(1) – “ITC reclaimed which was reversed under Table 4(B)(2) in earlier tax period” for each return period.

3. Reporting and Amendment of Opening ITC Reversal Balance: This reporting will start from August 2023 GSTR-3B return for monthly taxpayer and from July – September GSTR-3B for quarterly taxpayer.

4. Reporting of “Opening ITC reversal balance” pending to be reclaimed –

- Taxpayer can report their cumulative ITC reversal (ITC that has been reversed in earlier GSTR-3B returns and has not yet been reclaimed) as opening balance on GSTN portal.

- The last date to report same is 30th November 2023.

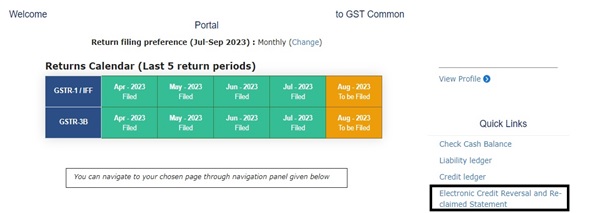

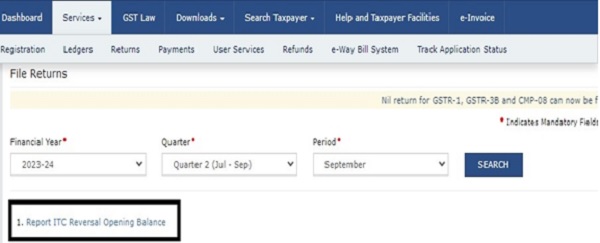

- The opening reversal balance can be reported using the following navigation on GSTN portal –

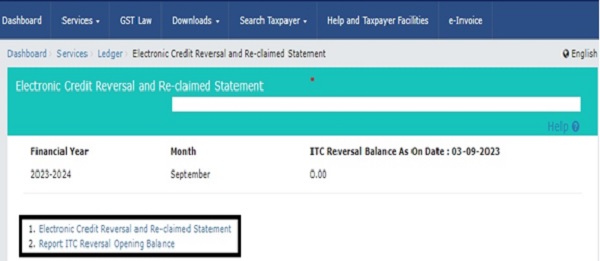

Login >> Electronic Credit Reversal and Re-claimed Statement >> Report ITC Reversal Opening Balance

OR

Login >> Returns >> Return Dashboard >> Report ITC Reversal Opening Balance.

OR

Services >> Ledger >> Electronic Credit Reversal and Re-claimed Statement >> Report ITC Reversal Opening Balance

- For monthly taxpayers, this opening balance shall be reported considering reversal done in the GSTR-3B filed upto July 2023. Similarly, for quarterly taxpayers, this balance shall be considered basis GSTR-3B filed for April-June 2023 quarter.

- The taxpayer will also have option to amend the opening balance upto 3 times. This facility of amendment will be available upto 31st December 2023.

5. Monitoring ITC Reclaimed vs. Reversal Balance: Going forward, the GSTN portal will start tracking that total ITC reclaimed as per Table 4D(1) of GSTR-3B does not exceed the ITC reversal balance in the statement + ITC reversal made in the current tax period GSTR-3B in Table 4B(2).

6. Warning Message for Excessive Reclaimed ITC: If the ITC reclaimed exceeds the balance as stated in Serial No 5 above, the GSTN portal will show a warning message. The taxpayer will still have the option to proceed with the return filing by ignoring the message.

Points for consideration:

1. Determination of opening balance of ITC reversal:

The option to report “opening ITC reversal balance” does not specify the tax period that shall be taken into consideration for reporting such ITC reversal amount. The same is open to interpretation of GST law by the taxpayer.

It may be noted that there is no time limit specified in GST law for re-claiming the previously claimed and reversed ITC. Hence, the taxpayers may interpret the same to include all ITC previously claimed and reversed in GSTR-3B returns but pending for reclaiming in the GSTR-3B.

2. Reporting of credit notes in Table 4 of GSTR-3B:

As per the clarification, the warning message will be reflected if the total ITC reclaimed exceed the carried forward reversal balance + ITC reversed in Table 4B(2).

However, it may be noted that Table 4B(2) of the GSTR-3B includes all ITC reversal other than those pertaining to Rule 38 (ITC by banking or financial institution), Rule 42 (Proportionate ITC reversal for inputs and Input services), Rule 43 (Capital goods related ITC reversal) and Section 17(5) of CGST Act (Blocked ITC). This includes ITC such as reversal of ITC incorrectly claimed, ITC reversal due to non-payment to vendor within 180 days and any other ITC reversed to be re-claimed in future etc. Further, certain taxpayers tend to report credit notes data also in Table 4B(2).

In such scenario, the total ITC reversal as per Table 4B(2) is expected to be higher than the ITC reclaimed in 4D(1). Thus, their will be no warning message even when the total ITC reclaimed by the taxpayer is exceeding the amount eligible for re-claim. Thus, it is necessary that taxpayers stop reporting of credit notes in Table 4B(2) of GSTR-3B and consider their impact in Table 4A(5) itself only i.e., in “All other ITC”.

3. Section 16 conditions and contradiction between books and GSTR-3B in method of recording of ITC:

As per the earlier advisory of CBIC, the taxpayers are required to report the ITC reversal on account of non-fulfilment of conditions prescribed in Section 16 such as non-receipt of tax paying document, non-receipt of goods and/or services or non-payment of tax by supplier to government in Table 4B(2) of the GSTR-3B. Thus, when the taxpayer claim such ITC in GSTR-3B of subsequent months, it will become a re-claim of credit and consequently required to be reported in Table 4D(1).

However, this is contrary to the recording of purchases in the books by certain taxpayers. This is because the taxpayers have inbuilt system restrictions on ITC availment until and unless the Section 16 conditions are satisfied. Thus, when such credit is claimed in the books upon fulfilment of Section 16 conditions, it is recorded as ITC availment and not ITC re-availment.

This creates a difference in ITC re-availment numbers between books and GST returns.

To avoid this reconciliation difference, taxpayer may reduce in Table 4A(5) of GSTR-3B, the amount of credit pertaining to such invoices wherein Section 16 conditions are not satisfied but ITC is auto-reflected in GSTR-3B basis the GSTR-2B.

Comments:

It is advisable to ensure that this new functionality is read together in alignment with previous reporting changes in Table 4 of GSTR-3B and the recording of purchases in the books of accounts to ensure that there is no discrepancy between auto-populated GSTR-3B, actual figures filed in GSTR-3B and the books of the taxpayer.

******

Disclaimer: The above article is based on the author’s understanding and view of the tax laws, tax rules, the relevant circulars, and notifications. Please refer to the latest law and consult the author before forming any opinion based on the information provided above as tax laws are subject to frequent changes. The author is not responsible for any issues arising because of opinion based on the above article without consultation. In any manner whatsoever, the views expressed in this article should not be construed as the views of the firm that the author is associated with. The author can be contacted at gauravmittal756@gmail.com.

Author Bio