CA Abhisek Tibrewal

The GST regime in India shall be a turnaround for the whole indirect tax schema in the country. The revamped taxation policies, altered levies and revised compliance methodologies shall affect businesses and commerce of all levels and categories. However, one the most significant and majorly impacted segment shall be the E – Commerce industry.

E – Commerce is somewhat new to the Indian economy and is undoubtedly one of the most prominently growing business segments in the country. So far as the taxation net is concerned, the frequently emerging innovative concepts and business models can be said to have not been tried and tested upon by the tax administrators till date. As the saying goes on ‘practice makes a man perfect’, the tax governing bodies of our country are yet practicing on the e-commerce front. The efforts to understand and generalize a broader taxation policy so as to bring under the tax net, all possible business models being practiced or evolving in the e-commerce segment can be sensed from the categorical coverage of the said segment in the Model GST Law as released by the Empowered Committee of the State Finance Ministers.

The Model GST Law has quite specifically dealt on the taxing policy of the e-commerce segment, which itself is quite significant since such attention has not been turned on to any other business segment or industry for that matter.

As of now, the general understanding that stands with a lay man as regards the e-commerce segment of business is the concept of ‘brand building’. The players in this whole segment seem to target upon the ‘Maximization (rather read as Capitalization) of Wealth Concept’ as against the traditional, attractive and easy to materialize concept of ‘Profit Maximization’.

However, under the GST Regime, the business models of the e-commerce operators might need a paradigm shift considering the involvement of extensive compliance obligations and at the same time, the inducement of tracing and tracking liability being casted upon such operators for better tax administration, reviewing, re-modeling and re-engineering of the Standard Operating Procedures may be required.

With this article, we aim to brief upon the major points as highlighted in the Model GST Law specifically in respect of the E – Commerce segment of business.

Electronic Commerce Operator

The first and foremost thing that needs to be understood is, who the target of this tax net is. The purpose fulfills with the definition of ‘Electronic Commerce Operator’ as envisaged in the Model GST Law itself. The prescribed definition of E – Commerce Operator is an inclusive one and has been defined to include:

– every person who, directly or indirectly, owns, operates or manages an electronic platform that is engaged in facilitating the supply of any goods and/or services or in providing any information or any other services incidental to or in connection there with, but

– does not include persons engaged in supply of such goods and/or services on their own behalf.

The scope of coverage of the aforesaid definition seems to be quite wide and seeks to bring into the tax net all player of the generally recognized, Online Market!

Some other terms as defined in the Model GST Law that need to be marked for reference are as under:

Aggregator

An aggregator means a person, who owns and manages an electronic platform, and by means of the application and a communication device, enables a potential customer to connect with the persons providing service of a particular kind under the brand name or trade name of the said aggregator.

Brand name or Trade name

It refers to a brand name or a trade name, whether registered or not, that is to say, a name or a mark, such as an invented word or writing, or a symbol, monogram, logo, label, signature, which is used for the purpose of indicating, or so as to indicate a connection, in the course of trade, between a service and some other person using the name or mark with or without any indication of the identity of that person.

Branded Services

Branded Services mean services which are supplied by an electronic commerce operator under its own brand name or trade name, whether registered or not.

Electronic Commerce

Electronic Commerce means the supply or receipt of goods and / or services, or transmitting of funds or data, over an electronic network, primarily the internet, by using any of the applications that rely on the internet, like but not limited to e-mail, instant messaging, shopping carts, Web services, Universal Description, Discovery and Integration (UDDI), File Transfer Protocol (FTP), and Electronic Data Interchange (EDI), whether or not the payment is conducted online and whether or not the ultimate delivery of the goods and/or services is done by the operator.

Registration

Registration is the identification of a taxable person before the tax administrators. Under the GST Regime, the primary registration obligation is attracted once the volume of supplies made by a person exceeds the prescribed threshold limit, barring the exceptions. E-Commerce segment is a prominent exception to this threshold limit relaxation. It has been prescribed that the following categories of persons shall be liable to get registered under the GST Regime, irrespective of the volume of supplies made by them, namely:

– persons who supply goods and/or services, other than branded services, through

electronic commerce operator; or

– every electronic commerce operator; or

– an aggregator who supplies services under his brand name or his trade name.

Collection of tax at source

The E-Commerce market is huge, growing and most importantly, intangible in practical terms. In order to put a track of transactions in the segment, the provision for tax deduction at source has been inculcated in the e-commerce taxing policy. The provision has been prescribed to be applicable beyond anything to the contrary contained in the Act itself or in any:

– contract,

– arrangement or

– memorandum of understanding.

It has been prescribed that,every electronic commerce operator shall;

– at the time of credit of any amount to the account of the supplier of goods and/or services or

– at the time of payment of any amount in cash or by any other mode

whichever is earlier, collect an amount, out of the amount payable or paid to the supplier, representing consideration towards the supply of goods and /or services made through it, calculated at a rate to be notified in this behalf by the Central/State Government on the recommendation of the Council.

Deposit the Tax

The amount so deducted and collected by the E-Commerce Operator shall have be paid to the credit of the appropriate Government by the operator within ten days after the end of the month in which such collection is made.

Furnish Return

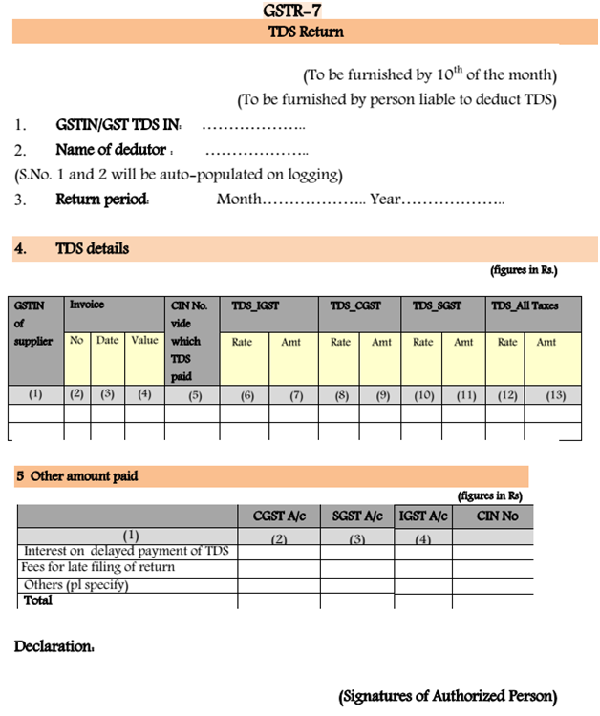

Every operator shall, furnish a statement, electronically, of all amounts collected towards outward supplies of goods and/or services effected through it, during a calendar month, in Form GSTR – 7, within ten days after the end of such calendar month.

The statement shall containthe details of the amount collected on behalf of each supplier in respect of all supplies of goods and/or services effected through the operator and the details of such supplies during the said calendar month. A snapshot of the prescribed format of return in this regards is produced hereunder so as to bring out an understanding as regards the details that shall be required to be furnished (and for that matter, be maintained as records) by the E-Commerce Operators.

Input Credit to the Supplier

The amounts collected by the E – Commerce Operator as discussed above and paid to the credit of the appropriate Government shall be deemed to be a payment of tax on behalf of the concerned supplier and the supplier shall claim credit, in his electronic cash ledger, of the tax collected and reflected in the statement of the operator filed.

Matching of records with Supplier

The details of supplies and the amount collected during a calendar month, and furnished by every operator shallbe matched with the corresponding details of outward supplies furnished by the concerned supplier in his valid return for the same calendar month or any preceding calendar month.

Where the details of outward supply, on which the tax has been collected, as declared by the operator do not match with the corresponding details declared by the supplier, the discrepancy shall be communicated to both persons in within prescribed time.

The value of a supply relating to any payment in respect of which any discrepancy is communicated and which is not rectified by the supplier in his valid return for the month in which discrepancy is communicated, shall be added to his output liability for the calendar month succeeding the calendar month in which the discrepancy is communicated.

The concerned supplier in whose output tax liability any amount is added shall be liable to pay the tax payable in respect of such supply along with interest on the amount so added from the date such tax was due till the date of its payment.

Calling of records from E-Commerce Operator

Any authority not below the rank of Joint Commissioner may, by notice, either before or during the course of any proceeding under this Act, require the operator to furnish such details relating to:

– supplies of goods and/or services effected through such operator during any period, or

– stock of goods held by the suppliers making supplies through such operator in the godowns or warehouses, by whatever name called, managed by such operators and declared as additional places of business by such suppliers – as may be specified in the notice.

Every operator on whom a notice has been served shall furnish the required information within five working days of the date of service of such notice.

Any person who fails to furnish the information required by the notice served shall, without prejudice to any action that is or may be taken be liable to a penalty which may extend to rupees twenty-five thousand. Here, the expression ‘concerned supplier’ shall mean the supplier of goods and/or services making supplies through the operator.

Food for Thought!

The E-Commerce market is the future and seems to be target audience of the tax administrators also. As of now the tax levies, especially the indirect taxes, are uneven and even bypassed in some cases. The model provisions under the GST Regime seem to be requiring the players in this segment to be more organized, transparent and record savvy rather than just being tech savvy.

The Newton’s Law of Motion here fits in that ‘Every Action has an Equal and Opposite Reaction’. The action is made, reaction is awaited. The efforts on both sides now needs to be equalized and hence, its time to gear up, review, re-model and be ready!

(Author can be reached at tibrewalca@gmail.com)

The E-commerce return format is GSTR-8 and not GSTR7.

I note that article refers TDS returns instead of TCS returns

Thanks