This article clarifies the applicability of e-invoicing on export supplies under GST, focusing on the nature of supply and the impact of filing a Letter of Undertaking (LUT). It explains that e-invoicing applies only to taxable supplies, whether domestic or export, while exempt, nil-rated, and non-taxable supplies remain outside its scope. The presence or absence of an LUT does not affect the obligation to generate an e-invoice; it only determines whether GST is payable. For taxable exports made with an LUT, GST is not payable, but the invoice must still reflect the applicable GST rate with the tax amount shown as zero. In contrast, taxable exports without an LUT attract GST, which must be charged and disclosed accordingly. The article further provides practical compliance guidance on invoice preparation, GST rate selection, and reporting on the GST portal, reinforcing that taxability of supply—not LUT status—is the decisive factor for e-invoice applicability.

1. Coverage of this article:

a. In this article, I am discussing the applicability of e invoicing in case of export supply. It may be taxable or exempt supplies.

b. I am also covering the scenario whether the supplier has filed a Letter of undertaking (LUT) & how it impacts the issuance of e invoices.

2. Applicability of E-invoice on different types of supplies:

All types of supplies not covered under e-invoicing. Supplies may be taxable, exempt or nil rated etc. Below mentioned supplies are covered under e-invoicing:

a. Taxable supplies are covered under e-invoicing

b. Exempt supplies are not covered under e-invoicing

c. Nil rated supplies are not covered under e-invoicing

d. Non-taxable supplies are not covered under e-invoicing

Conclusion: Supplier will generate the e-invoice only in case of taxable supplies. If a registered person supplying exempt goods or services then e-invoicing will not be applicable.

3. E invoice applicability in case of ZRS:

| S No | Nature of supplies | Applicability of e invoice |

| 1 | Taxable supplies outside India with LUT | Yes |

| 2 | Exempt supplies outside India with LUT | No |

| 3 | Nil rated supplies outside India with LUT | No |

| 4 | Non-Taxable supplies outside India with LUT | No |

| 5 | Taxable supplies outside India without LUT | Yes |

| 6 | Exempt supplies outside India without LUT | No |

| 7 | Nil rated supplies outside India without LUT | No |

| 8 | Non-Taxable supplies outside India without LUT | No |

4. Letter of undertaking:

a. If LUT is filed by the supplier then GST will not be levied on sale.

b. If no LUT is filed by the supplier then GST will be levied on sale.

5. When to generate the e invoice:

a. The supplier is required to generate the e invoice in case of taxable supplies under ZRS, irrespective of whether an LUT has been filed or not by the supplier.

b. Because e- invoicing is applicable in case of taxable supplies.

c. It does not matter whether you have filed the LUT or not.

6. Taxable supplies outside India with LUT:

a. In this case, there will be no GST liability if taxable goods are exported under an LUT.

b. At the time of preparation of invoice, you should select the actual rate of GST even though no GST is payable on sales. You should not select the 0% rate or show it under exempt supplies.

c. In the GST column, GST amount should be shown as zero.

7. Taxable supplies outside India without LUT:

a. In this case, there will be GST liability if taxable goods are exported without an LUT.

b. At the time of preparation of invoice, you should select the actual rate of GST since GST is payable on sales.

c. In the GST column, GST amount should be shown as per actual GST levied.

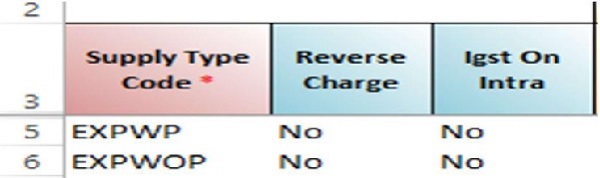

8. 1st Screenshot of e invoice sheet:

a. This screenshot has been taken from the e invoice sheet downloaded from the e invoice portal.

b. It clearly shows that e invoicing is applicable in both cases, whether an LUT has been filed or not.

9. Refer e-invoicing article for understanding:

In this article, I have covered the Provisions related to e-invoicing under GST.

https://taxguru.in/goods-and-service-tax/provisions-related-e-invoicing-gst.html

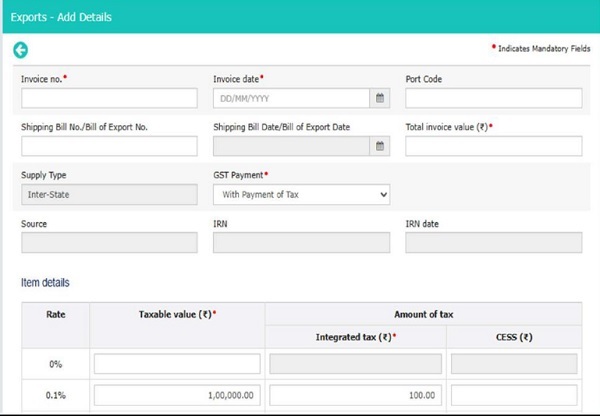

10. 1st Practical scenario without LUT:

a. If goods are exported without LUT, you need to pay the tax on supply.

b. At the time of disclosure in GST portal, you should select the actual rate of GST since GST is payable on sales.

c. In the GST column, GST amount should be shown based on the actual GST charged.

11. 2nd Practical scenario with LUT:

a. If goods are exported with LUT, you do not need to pay the tax on supply. IGST amount will be zero by default.

b. At the time of disclosure in GST portal, you should select the actual rate of GST even there is no tax liability.

c. In the GST column, GST amount should be shown as zero. The portal will automatically display the amount as zero in case an LUT has been filed.

12. E-invoicing on SEZ supplies with or without LUT will be covered in a separate article.

*******

If you have any queries, you can reach the author by email at caashishsingla878@gmail.com.

Disclaimer: The views and opinions expressed in this article are those of the author. This article is intended for general information purposes only and does not constitute professional advice. Readers are strongly advised to consult a qualified professional for guidance specific to their individual situation before making any financial, legal, or tax-related decisions. The author shall not be held liable for any loss or damage of any kind incurred as a result of the use of this information or for any actions taken based on the content of this article.

Author Bio

What is the threshold limit for e-invoicing for export supply of services? kindly reply me. thanks

Hi, There is no specific limit for export sales. General limit is 5 Crore. If your aggregate turnover exceeds 5 Cr. in any of the year from FY 17-18 to FY 24-25 then in the FY 25-26, e-invoicing will be applicable on taxable supplies.

Refer this article for understanding:

https://taxguru.in/goods-and-service-tax/provisions-related-e-invoicing-gst.html