CA Puneet Mathur

Demand and Recovery procedures are basically for department to provide them a framework or methodology in order to raise a demand in the cases where any tax, interest or penalty are not paid and subsequent recovery in case of non-payment by the assessee.

Under GST Act, provisions relating to demand and recovery are quite similar to the provisions under Service Tax and Central Excise Act. Demand & Recovery provisions under GST are contained in Section 73 to 84 of Chapter XV of The CGST Bill, 2017.

Primarily demand and recovery provisions are categorized in two parts –

→ One without reason of fraud or wilful-misstatement or suppression of facts, and

→ Other one with reason of fraud or wilful-misstatement or suppression of facts.

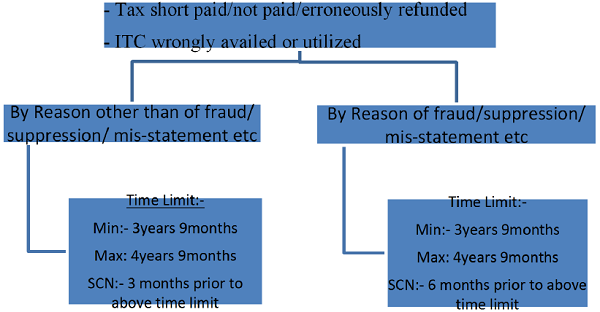

Section 73 deals with the cases where there is no invocation of fraud/suppression/mis-statement etc.

Time Limits for adjudication of cases under Section 73 are:-

→ 3 years from the duedate for filing of annual return for the relevant financial year in case of tax not paid or short paid or Input Tax Credit (ITC) wrongly availed or utilized.

In effect, time limit in this case will range between minimum 3 years 9 months to maximum 4 years 9 months.

→ 3 years from the date of erroneous refund.

{Sec.73 (10)}

Above time limits are for issue of order and Show Cause Notice (SCN) for this purpose is required to be issued at least three months prior to the time limit mentioned above.

{Sec.73 (2)}

For example:- Tax payer has not paid tax for the month of Oct-2017 then in normal cases department can pass order for recovery by 31st Dec 2021 and SCN for this purpose can be issued by 30th Sep 2021.

Section 74 deals with cases where the provisions related to fraud/suppression/mis-statement etc. are invoked.

Time Limit for adjudication of cases under Section 74 are:-

→ 5 years from the due date for filing of annual return for the relevant financial year in case of tax not paid or short paid or ITC wrongly availed or utilized.

In effect, time limit in this case will range between minimum 5 years 9 months to maximum 6 years 9 months

→ 3 years from the date of erroneous refund.

{Sec.74 (10)}

Above time limits are for issue of order and SCN for this purpose is required to be issued at least six months prior to the time limit mentioned above

{Sec.74 (2)}

For example:- Tax payer has not paid for the month of Oct-2017 and department contends it as case of fraud/suppression/mis-statement etc then department can pass order for recovery by 31st Dec 2023 and SCN for this purpose can be issued by 30th June 2023.

Here, it is pertinent to note that this extended period can be invoked only when there is a wilful misrepresentation/suppression with intention to evade tax. Supreme court also in the case of Tamil Nadu Housing Board Vs CCE 1995 Supp(1) SCC 50=74 ELT 9(SC) held that power to extend period from 1 year to 5 year are exceptional powers and have to be construed strictly.

Also it is important to mention that there is no suppression if all the facts have been disclosed to the department and hence extended period can’t be invoked.

To Summarize:-

Further, law also provided immunity to the person chargeable to tax if he pays:-

- In normal case: –Outstanding tax amount with interest before service of show cause notice under section 73(1) & inform to proper officer in writing. {Sec.73 (5)}

- In cases of fraud/suppression/mis-statement etc: –Outstanding tax amount with interest and penalty @ 15% of tax amount before service of show cause notice under section 74(1) & inform to proper officer in writing. {Sec.74 (5)}

Then, Proper officer will not serve any SCN under Section 73(1) & Section 74(1) as the case may be. {Sec.73 (6) & Sec.74 (6)}

However if person pays:-

- In normal case:-Tax along with interest within 30 days of issue of SCN under section 73(1).

- In cases of fraud/suppression/mis-statement etc: –Tax along with interest & penalty @ 25% within 30 days of issue of SCN under section 74(1).

- Further again, in cases of fraud/suppression/mis-statement etc: –Tax along with interest & penalty @ 50% within 30 days of communication of order.

Then, all proceedings in respect of the said notice {Sec 73(1)/Sec 74(1)} shall be deemed to be concluded. {Sec.73 (8) & Sec.74 (8)}

All proceedings, in respect of the said notice, shall not include proceeding under section 132 i.e punishable offences (Explanation to Sec 74).

Penalty Percentages under different payment cases:-

| Possible case | Normal Case (Sec 73) | Fraud etc (Sec 74) |

| Before issue of SCN | Nil | 15% of Tax Amount |

| Within 30 days from issue of SCN | Nil | 25% of Tax Amount |

| Withtin 30 day from issue of order | Higher of 10% of Tax or INR 10,000 | 50% of Tax Amount |

| Any other case | 100% of Tax Amount |

Law has also imposed a control on the revenue to act timely and pass orders without much delay through provisions of Section 75 where it says that, in case proper officer issued a SCN but fails to pass order within the time limit prescribed under Section 73(10) and Section 74 (10), then adjudication proceedings shall deemed to be concluded. {Sec 75(10)}

Exclusion from Time limit {Sec.75 (1)}

Where the service of notice or issuance of order is stayed by an order of Court or Appellate Tribunal, the period of stay shall be excluded in computing the period specified in sub-section (2) and (10) of Section 73 or sub-section (2) and (10) of section 74 as the case may be.

Where any Appellate Authority or Appellate Tribunal or court concludes that the notice issued under section 74(1) is not sustainable for the reason that the charges of Fraud or wilful-misstatement or suppression of facts to evade tax has not been established, the proper officer shall determine the tax payable deeming as if the notice were issued under section 73(1). {Sec 75(2)}

General Provisions:-

1. Proper officer (with sufficient cause) grant time and adjourn the hearing for reasons to be recorded in writing. Provided that no adjournment shall be granted for more than three timesto a person during the proceedings. {Sec 75(5)}

2. Amount of tax, interest and penalty demanded in order shall not be more than the amount specified in notice and no demand shall be confirmed on the ground other than the ground specified in the notice.

As similar to present law viz Central Excise/Service tax, GST law also have provisions related to recovery of amount collected by a person as tax from another person but the same has not been deposited with Government. Here law says that it is mandatory to pay the amount collected from another person representing tax under this Act to the government regardless of whether the supplies in respect of which such amount collected is taxable or not. For any such amount not so paid, proper officer may issue SCN for recovery of such amount and penalty equivalent to such amount. {Sec 76(1&2)}

Though there is no time limit to issue SCN under Section 76(2) for the cases where taxes collected but not paid to Government but Proper office has to pass order after following principles of natural justice within one year of date of issue of such notice. {Sec 76(6)}

Period of stay by an order of the court or Appellate Tribunal shall be excluded in computing the period of one year. {Sec 76(7)}

Tax wrongly collected and paid to Central / State Government {Sec 77}:-

Law provides refund of tax wrongly paid as CGST/SGST or CGST/UTGST as the case may be, considering transactions as intra-state supply which subsequently held to be an interstate supply. {Sec 77(1)}

Also where registered person paid integrated tax on a transaction considering being an inter-State supply, but which is subsequently held to be an intra-State supply, shall not be required to pay any interest on the amount of CGST/SGST or CGST/UGGST as the case may be. {Sec 77(2)}

Issue: – Ideally there should be a mechanism of adjustment between Central and State Government in these cases. Since CGST & IGST both are with Central Government so these could have been made adjustable in these circumstances. Hope this issue will settle down as we progress in GST regime.

Provisions with respect to recovery, Charge, Attachment

Recovery of Tax {Sec 78 & 79}

Amount payable by taxable person, in pursuance of an order passed, shall be paid within 3 months from the date of service of such order. Proper officer, if consider it expedient in the interest of revenue, may with reasons to be recorded in writing, require the said person to make payment with in such reduced period as he may specify.

If demand is not paid within the time specified, then department can start recovery proceedings.

Section 79 (1) gives power to proper officer to recover the amount by one or more of following modes:-

(a) Proper officer may recover or require any other specified officer to recover by deducting the amount from the other amount payable to such person.

(b) Proper officer may recover or require any other specified officer to recover by detaining or selling any goods belonging to such person which are under his control.

(c) Proper officer may, by notice in writing, require any other person from whom money is due or may become due to such person or who holds or may subsequently hold money for or on account of such person, to pay to government. This amount will be payable forthwith upon the money becoming due or being held or within the time specified in the notice not being before the money becomes due or is held. (Garnishee Provisions)

(d) Proper officer may (Subject to rules) detain any movable or immovable property belonging to or under control of such person and detain the same until the amount payable (including cost of distress) is paid.

(e) Proper officer may prepare a certificate specifying amount due from such person and send it to collector of the relevant district and collector shall proceed to recover from such person the amount as if it were an arrear of land revenue.

(f) Notwithstanding anything contained in the Code of Criminal procedure, 1973, proper officer may file application to appropriate Magistrate and such Magistrate shall proceed to recover that amount as if it were the fine imposed by him.

Recovery under Bond:- {Sec 79(2)}

Any bond or other instrument was executed under this act or rules or regulation there under and that bond or instrument provides that any amount due under such instrument may be recovered in the manner laid down in Sec 79(1) as above, then the amount without prejudice to the other mode of recovery will be recovered as per Sec 79(1).

Recovery by State/Union Territory:- {Sec 79(3)/(4)}

Proper officer of State Government or UT during the course of recovery of SGST/UTGST arrears from any person may recover unpaid amount of tax, interest, penalty payable to Central Government by such person. Such amount will be recovered as if it were arrear of SGST/UTGST and credit the amount so recovered to the account of Central Government. {Sec 79(3)}

In case amount recovered as above is less than the amount due, then such amount will be apportioned among Central Government, State Government & UT in proportion of the amount due to each authority. {Sec 79(4)}

Amount in Instalments: – {Sec 80}

Commissioner, on application filed by the taxable person and with reasons recorded in writing, may extend the time for payment or allow the payment of amount due under CGST in monthly instalment not exceeding 24 months with payment of interest under Section 50.

This facility will not be available for payment of amount due as per the liability self assessed in any return.

In the event of failure of payment of even one instalment, whole of the outstanding balance will become due and payable forthwith and shall be liable for recovery without any further notice.

Interest to be paid from the date of tax became due till the date of actual payment.

For Example: – Mr X required to pay tax on 15th Oct 2017 for which he requested commissioner to grant him benefit to pay tax of INR 4,00,000 in 8 installments.

Interest will be payable for below mentioned days:-

| Installment no. | Installment Amount | Due Date | Payment date | Interest Days |

| 1. | 50,000 | 15-Oct-17 | 1-Jul-18 | 260 |

| 2. | 50,000 | 15-Oct-17 | 1-Aug-18 | 291 |

| 3. | 50,000 | 15-Oct-17 | 1-Sep-18 | 322 |

| 4. | 50,000 | 15-Oct-17 | 1-Oct-18 | 352 |

| 5. | 50,000 | 15-Oct-17 | 1-Nov-18 | 383 |

| 6. | 50,000 | 15-Oct-17 | 1-Dec-18 | 413 |

| 7. | 50,000 | 15-Oct-17 | 1-Jan-19 | 444 |

| 8. | 50,000 | 15-Oct-17 | 1-Feb-19 | 475 |

Void Property transactions: – {Sec 81}

If a person after any amount has become due from him –

→ creates a charge

→ or part with

the property belonging to him by way of –

→ Sale

→ Mortgage

→ Exchange

→ Or any other way of transfer

Of any of his property in favour of any other person with the intention of defrauding the Government revenue

Then, such charge or transfer shall be void as against any claim with respect to any tax, interest, or any other sum payable by the said person.

However if such charge or transfer is made –

→ with adequate consideration,

→ in good faith and

→ Without notice of pendency of such proceedings under the act

Or

→ Without notice of such tax or other sum payable by said person.

Or

→ With previous permission of the proper officer.

Amount payable to be first charge {Sec 82}

Amount payable as tax, interest, penalty by the taxable person or any other person shall be first charge on the property of such taxable or other person, notwithstanding any thing contrary contained in any other law for the time being in force, except Insolvency and Bankruptcy code 2016.

Provisional Attachment:- {Sec 83}

During the pendency of any proceeding under:-

→ Section 62 i.e. Assessment of non-filers of returns

→ Section 63 i.e. Assessment of unregistered persons

→ Section 64 i.e. Summary Assessment in some special cases with sufficient grounds

→ Section 67 i.e. Inspection, Search & Seizure

→ Section 74 i.e. Determination of Tax, Interest, penalty in case of fraud etc.

Commissioner may, if necessary in the interest of Government revenue, by order in writing, attach provisionally any property belonging to the taxable person.

Such provisional attachment shall be ceased to have effect after expiry of one year from the date of order mentioned above.

Continuation and validation of certain recovery proceedings {Sec 84}

Where any notice of demand in relation to Government dues viz Tax, Penalty, Interest or any other amount payable under the act, is served upon the taxable person and any appeal, revision application is filed or any other proceeding is initiated in respect of such Government dues then if:-

→ Government dues are enhanced in appeal, revision or other proceedings then commissioner shall serve notice of demand in respect of enhance amount. Recovery proceeding shall be continued from the stage at which such proceedings stood immediately before such disposal.

→ Government dues are reduced in appeal, revision or other proceedings then fresh notice of demand is not needed and only reduced demand will be liable for recovery. Recovery proceeding shall be continued with the reduced amount from the stage at which such proceedings stood immediately before such disposal.