R.K Rengaraj, Advocate

Introduction: As 30th June, 2019 is fast approaching the GST Practitioners, auditors and assessees are involving themselves in filing annual return GSTR 9 and 9C. Filling every table in the GSTR 9 is not that much easy as any wrong filling will result in remitting back the amount particularly on account of ITC mismatch in 2A and 3B by the Assessee or an account of debit notes, amendments, wrong utilisation of ITC, RCM etc.,. There is no revision option in GSTR 9, as of now, and the whole industry ise expecting some changes in the ensuing 35th GST council meeting slated on 20th June, 2019 headed by new union finance minister, Mrs.Nirmala Seetharaman. In this article let us see what is deemed exports under the GST Act and where such turnover is to be shown in the Annual Return GSTR 9.

Deemed exports under GST Act.

“Deemed exports” generally refer to those transactions under which supply of goods do not leave the country, and payment for such supplies is received in Indian Rupees shall be treated as ‘deemed exports’, provided that goods are manufactured or produced in India.

In other words, deemed export includes certain transactions which though do not qualify as export of goods but refund of GST is awarded to them. Certain supplies of goods which are manufactured in India and:

> where such goods do not leave India and

> payment of such supplies is received either in Indian rupees or in convertible foreign exchange,

to be treated as deemed supplies

– Sec. 2(39) of CGST Act 2017 read with Sec. 147 of CGST Act 2017.

Conditions for deemed ecports:

- Applicable only for the supply of goods (not applicable to services).

- Goods are not required to be taken outside India.

- Such supply of goods must be notified by the Central Government as Deemed exports under Section 147 of the Central Goods and Services Tax Act, 2017 (CGST Act).

- Goods must be manufactured or produced in India.

- Payment can be received in Indian Rupees or in convertible foreign exchange.

- Such supplies cannot be made under Bond / LUT.

- The tax must be paid at the time of supply. Refund of tax paid on such supplies can be claimed.

It is to be noted that deemed export supplies are not zero-rated supplies by default. All deemed export supplies will be subject to GST at the point of supply. Supplies cannot be made under Bond / LUT without payment of tax. Tax should be paid on such supply and then be claimed as refund.

Subject to certain conditions, Refund of tax paid can be claimed by either of the following persons:

1. Supplier of goods OR

2. Recipient of goods.

The recipient is not eligible to claim the input tax credit (ITC) in case refund of tax paid is being claimed by the supplier.

CBIC notified list under the category of Deemed Exports under GST regime. The notification and circular were issued by the CBIC on dated 18th October 2017 and 6th November 2017 respectively detailing the Deemed Export procedure.

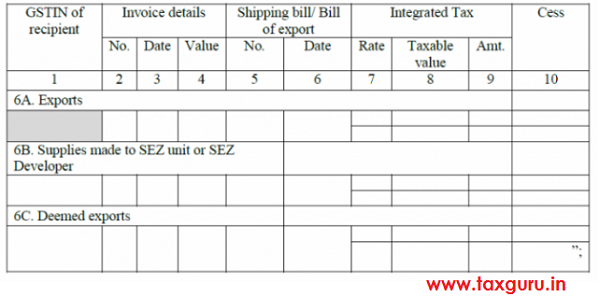

Return in GSTR1.

Return in GSTR1.

The outward supplies made to the above category should have been reported in Table 6C.

Return in GSTR 3B

The outward supply of deemed exports is to be reported in table 3.1 (b) with other zero-rated supplies.

Annual Return in GSTR 9

The sum total of the deemed exports value should be declared in Table No.4E i.e Table 6C of Form GSTR1 may be used for filling up these details.

Section 147 allows the Government to notify certain supplies of goods to be deemed exports. The deeming fiction of this kind of supply as deemed export allows a person to enjoy all the tax benefits as available in case of zero rated supply.

The author is a whole time director in Ms Lore Tax Professionals Private Ltd, Coimbatore and can be reached in renga42002@yahoo.co.in.

Author Bio

Sir, deemed export is to be in Table-4 (B2B) and not in table-6.

There is problem, if our deemed export in local then as per your view it is shown in 3B as zero rated which accept only IGST. Then how we can show under 3.1(B).

Export of service under LUT, how can we show in GSTR 9, table 17 (HSN details). It asks to match the tax amount with supply. But there is no payment of tax. how can we enter that outward supply.

Under gst, only spe4cified category vide Notification No. 48/2017 is treated as deemed exports.

is third party export called Deemed Export

Good topic selected. New things learned