Section 2(37)

‘credit note’ means a document issued by a registered person under sub-section (1) of section 34.

Section 2(38)

‘debit note’ means a document issued by a registered person under sub-section (3) of section 34.

Definition of Credit Note as per CGST Act– Section 34(1)

Where a tax invoice has been issued for supply of any goods or services or both and the taxable value or tax charged in that tax invoice is found to exceed the taxable value or tax payable in respect of such supply, or where the goods supplied are returned by the recipient, or where goods or services or both supplied are found to be deficient, the registered person, who has supplied such goods or services or both, may issue to the recipient a credit note containing such particulars as may be prescribed

Definition of Debit Note as per CGST Act – Section 34(3)

Where a tax invoice has been issued for supply of any goods or services or both and the taxable value or tax charged in that tax invoice is found to be less than the taxable value or tax payable in respect of such supply, the registered person, who has supplied such goods or services or both, shall issue to the recipient a debit note containing such particulars as may be prescribed

Journal Entries for Debit and Credit Notes under GST

| Dr. Notes | Cr. Notes | ||

| 1. When Purchases is Made | 1. When Sales is Made | ||

| Pur | 100 | Debtor | 118 |

| Input CGST | 9 | To Sales | 100 |

| Input SGST | 9 | To Output CGST | 9 |

| To Creditor | 118 | To Output SGST | 9 |

–

| Dr. Notes | Cr. Notes | |||||

| BUYER’S POINT OF VIEW | BUYER’S POINT OF VIEW | |||||

| Creditor | 118 | Pur | 100 | |||

| To Pur Return | 100 | Input CGST | 9 | |||

| To Input CGST | 9 | Input SGST | 9 | |||

| To Input SGST | 9 | To Creditor | 118 | |||

| SELLERS’S POINT OF VIEW | SELLERS’S POINT OF VIEW | |||||

| Debtor | 118 | Sales Return | 100 | |||

| To Sales | 100 | Output CGST | 9 | |||

| To Output CGST | 9 | Output SGST | 9 | |||

| To Output SGST | 9 | To Debtor | 118 | |||

–

| Reasons for Issue of Dr. Note | Reasons for Issue of Cr. Note |

| BUYER’S POINT OF VIEW | BUYER’S POINT OF VIEW |

| Purchase Return To Decrease Purchases

Ex- More Goods Recd, More Tax Charged by the Supplier |

To Increase Original Purchase

Ex- Less Goods Purchased, Less Tax Charged by the us from the Buyer |

| SELLERS’S POINT OF VIEW | SELLERS’S POINT OF VIEW |

| To Increase Original Sales Ex- Less Goods Sold,Less Tax Charged by the Us

*If the supplier charges a penalty for the delayed payment of consideration , the supplier would issue a debit note for the amount of Penalty . Ex- Less Goods Sold, Less Tax Charged by the Us |

Sales Return

*Cash Discount *If Goods on Sale are Found deficient by the buyer Ex- More Goods Sold, More Tax Charged by the Us |

Note

1. Debit Note will benefit the government in terms of Tax Collection but Credit Note will cause to reduce the tax liability So, Government has specified the time limit for issuing a Credit Note but has not specified the time limit for issuing a debit note.

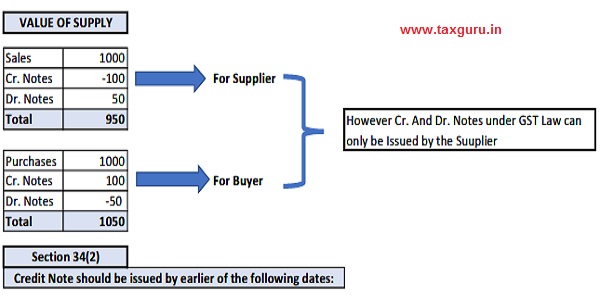

2. A Credit Note and Debit Note for the purpose of GST Law, can be Issued by the Registered Person who has issued the tax Invoice i.e. The Supplier.

3. Any Such Document, by whatever name called (Debit Note or credit Note) when issued by the recipient to the registered supplier, will not be considered any document under GST Law. ⇒Not Valid as per GST

VALUE OF SUPPLY

1. Date Of Filling Of Annual Return In Which The Original Tax Invoice Was Issued; Or

2. 30th September of the FY immediately succeeding the FY in which the original Tax Invoice was issued.

Note: The Credit Note so issued must be declared in the returns for the month in which they are issued, by the supplier and by the recipient both (Means by Buyer and Seller Both) as per the above mentioned date.

Author Bio

Purchase [ Supplier ] Good Shortage Debit Note Entry send supplier how we are send credit note Please Send with Gst-Input/Output ?

Good article thank you