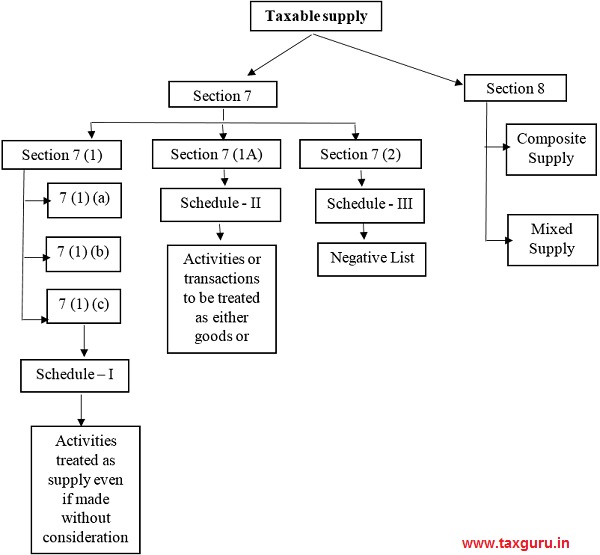

Chapter overview:

Section 7 (1) Meaning and Scope of supply

Section 7 (1) (a): Both Business and Consideration

> Any Supply of goods or services or both made or agreed to be made by a registered taxable person such as:

> Barter, Exchange, Lease, Transfer, Disposal, Sale, Licence, Rental (BELT DSLR)

> for a consideration,

> In the course or furtherance of business.

Section 7 (1) (b): Business/Business and Consideration

> Import of service: from a supplier located outside India who provides service in India to a registered/ unregistered recipient located in India.

> For consideration.

Section 7 (1) (c): Business and Consideration

> Schedule – I: Activities treated as supply even if made without consideration

(a) Permanent transfer or disposal of business assets:

i. Permanent transfer or disposal of the business asset without consideration, on which ITC was availed during purchase, will be treated as supply under 7 (1) (c) (a).

(b) Transaction between related persons [section 15 (5)]* or distinct persons specified under [section 25 (4)]**:

i. in the course or furtherance of business

ii. Provided gift not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as supply of goods or services or both.

* Explanation to Section 15(5): Two persons shall be a related person if:

- Such persons are officers of one another’s business,

- Such persons are employer and employee,

- They are legally recognized partners,

- One directly or indirectly controls the other,

- Any person directly or indirectly owns, controls or holds 25% or more of the voting stock or shares of both of them,

- Both are controlled by the third party,

- Together they control the third party,

- Members of the same family,

- Persons who are associated in the business of one another, where one is a sole agent/ distributor/ concessionaries, of the other, shall also be related.

** Distinct Person Section 25 (4): A person who has obtained or is required to obtain more than one registration, whether in one State or Union territory or more than one State or Union territory shall, in respect of each such registration, be treated as distinct persons for this Act.

Section 25 (5): Where a person who has obtained or is required to obtain registration in a State or Union territory in respect of an establishment, has an establishment in another State or Union territory, then such establishments shall be treated as establishments of distinct persons for this Act.

(c) Supply of Goods between principal and agent:

i. By a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

ii. By an agent to his principal where the agent undertakes to receive such goods on behalf of the principal.

(d) Import of Services:

i. By a taxable person in the course of business,

ii. From a related person, or

iii. From any other establishments outside India.

Section 7 (1A):

Schedule – II: Activities or transactions to be treated as supply of goods or supply of Services

Few transactions are treated as either good or services as per schedule – II.

(a) Activities Treated as Supply of Goods:

| Schedule II | Activities |

| 1 (a) | Transfer of title in goods |

| 1 (c) | Transfer of title is good at a future date upon payment of the entire consideration. |

| 4 (b) | Transfer or disposal of the business asset on the direction of the person carrying on the business whether or not for a consideration. |

| 4 (C) | Assets of the business carried on by any person who ceases to by a taxable person shall be deemed to be supplied before he ceases to be a taxable person unless:

|

| 7 | Goods supplied by unincorporated association or body of persons to a member thereof for a consideration. |

(b) Activities to be treated as Supply of Services:

| Schedule II | Activities |

| 1 (b) | Transfer of right in the undivided share without transferring the title. |

| 2 (a) | Letting out of the land. |

|

2 (b) |

Letting out of building either wholly or partly for business or commerce. |

|

3 |

Addition in goods, where the title belongs to another person. |

|

4 (b) |

The usage or making available of goods held or used for the business is put to private use, for any purpose other than business, whether or not for a consideration. |

|

5 (a) |

Renting of immovable property, |

|

5 (b) |

Construction of a complex, building, civil structure or a part thereof, including those intended to sell either wholly or partly. Except where the consideration is received after issuance of completion certificate or first occupation, whichever is earlier. |

|

5 (c)

|

Temporary or permanent transfer of right in any intellectual property. |

|

5 (d) |

Service relating to information technology software, |

|

5 (e)

|

Agreeing to the obligation to refrain from an act, or to tolerate an act or a the situation, or to do an act; and |

|

5 (f) |

Transfer of the right to use any goods for any purpose for a consideration. |

Section 7 (2): Negative List

> Activities or transactions specified in Schedule III, as may be notified by Government on the recommendation of the council.

> or such activities or transactions in which the Central Government, a State Government or any local authority are engaged as public authorities,

> Shall be treated neither as a supply of goods nor a supply of services.

Schedule III: Negative list

| Schedule III | Activities |

|

1 |

Services provided in the course of employment.

|

|

2 |

Judgement by any court or Tribunal established under any law for the time being in force,

|

|

3 (a) |

Functions performed by MPs, MLAs etc.

|

|

3 (b) |

Service provided by persons holding a constitutional post.

|

|

3 (c) |

Service provided by a person as an as a chairperson/ Member/ Director in a body established by Government. Provided such person should not be deemed as an employee before the commencement of this clause in such company. |

|

4 |

Funeral services. |

|

5

|

Sale of building & land where whole consideration is received after issuance of completion certificate. |

|

6

|

Actionable claims, other than lottery, betting and gambling |

|

7 |

Supply from one non-taxable territory (outside India) to another, without entering taxable territory (Inside India). |

|

8 (a) |

Supply of warehoused goods to any person before clearance for home consumption; |

|

8 (b) |

Endorsement of documents of title to the goods by the consignee to any other person after the goods have been dispatched from the port of origin located outside India but before clearance for home consumption. |

Section 8: Composite & Mixed Supply

| Basis | Composite supply | Mixed Supply |

|

Transaction |

A taxable person supplying two or more taxable supplies of goods or services or both, or a combination thereof.

|

A taxable person supplying two or more individual supplies of goods or services or both, or a combination thereof. |

|

Nature |

Naturally bundled in the ordinary course of business, one of which is a principal supply. E.g. Service provided by Packers and movers along with Moving Kits, Goods: Moving Kit, Services: packing, transportation of goods, dispatch etc. e.g. Warranty on purchase of any product Goods: product, Services: warranty given. |

These supplies are not naturally bundled in the ordinary course of business. E.g. pen drives given at modest rate on the purchase of a laptop. |

|

GST Payable |

The rate of Principal supply shall be considered as the rate of composite supply. | The rate of that individual supply which attracts the highest rate would be considered as the rate of mixed supply. |

Author Bio

BELT DSLR Excellent

The acronym of BELT DSLR mentioned u/ss 7 (1)(a) was the idea of Professor: P. Subbaraman..