ASSESSMENT

1. INTRODUCTION

1.1 GST law is a voluntary compliance-based taxation system. One of the key features of GST is its self-assessment system. The entire responsibility for assessment of tax liability has been entrusted upon with the taxable person or the Business entity in line and spirit of the GST laws.

1.2 The standard norm in tax laws is to make the supplier responsible for tax assessment, because the supplier alone is aware of the details of his supply and all elements of value that are relevant for arriving at taxable value.

This means that taxpayers are required to self-assess their tax liability and file their returns accordingly.

1.3 The provisions of the CGST Act, 2017 and CGST Rules, 2017, relevant to this Chapter of Assessment, are as under –

| Sr. No. | Section/Rule | Provision pertaining to | |

| 1 | Section 2(11) | Definition of Assessment | |

| 2 | Section 59 | Self-Assessment | |

| 3 | Section 60 and Rule 98 | Provisional assessment | |

| 4 | Section 61 and Rule 99 | Scrutiny of returns | |

| 5 | Section 62 and Rule 100 | Assessment of non-filers of returns | |

| 6 | Section 63 and Rule 100 | Assessment of unregistered persons | |

| 7 | Section 64 and Rule 100 | Summary assessment in certain special cases | |

| 8 | Section 65 and Rule 101 | Audit by tax authorities | |

| 9 | Section 66 and Rule 102 | Special audit. | |

| 10 | Section 67 and Rule 139 | Power of inspection, search and seizure. | |

| 11 | Section 16 and Rule 36 | Eligibility and conditions for taking input tax credit | |

| 12 | Rule 68 | Notice to non-filers of returns | |

| 13 | Rule 100 | Assessment in certain cases | |

1.4 Assessment under GST is a crucial process that helps to ensure that taxpayers are complying with the GST laws and regulations. The law has put onus of self-assessment on the taxpayers with a strong compliance verification mechanism in place to ensure that the tax liabilities are discharged appropriately and in time. The officer will step into the area of assessment of tax liabilities only in cases the legislation warrants him to do so in specified situations.

1.5 As per Section 2(11) of CGST Act, 2017 ‘assessment’ means determination of tax liability and includes self-assessment, re-assessment, provisional assessment, summary assessment and best judgment assessment. Such assessments are subject to proceedings involving observance of principles of natural justice. (Section 2(11) of CGST Act, 2017)

1.6 The word assessment is used in a comprehensive sense and includes all proceedings, starting with the filing of the return or issue of notice and ending with the determination of the tax payable by the taxpayer and its recovery by the proper officer.

2. IMPORTANCE OF ASSESSMENT UNDER GST

Assessment under GST is important for various reasons. It ensures that taxpayers are complying with the GST laws and regulations, which enables the taxpayer to run his business smoothly. Assessment also helps in detecting any errors or discrepancies in the returns filed by the taxpayers, thus, preventing tax evasion. Besides, assessment helps educate taxpayers on the correct procedures for calculating and paying their taxes and thus, improves GST compliance.

3. ERRORS COMMONLY COMMITTED WHILE DISCHARGING TAX LIABILITY

It is crucial to understand the common errors the taxpayers are making while filing the statutory returns. These errors can result in incorrect assessment which ultimately lead to short payment or non-payment of tax. Some of the common errors made while filing the returns are as under:

(i) Incorrect classification of goods and services: GST rates vary depending on the classification of goods and services. It has to be ensured from the returns that the supply of goods and services are correctly classified and the tax rate applied for determining the tax payable is correct.

(ii) Delayed filing of returns: The statutory GST returns should be filed on or before the due dates, failing which interest is attracted at prescribed rate and penal clauses are attracted.

(iii) Failure to report input tax credit: Taxpayers are allowed to claim the input tax credit on their purchases goods (inputs) and/or services (input services), which are utilised for discharging the tax liability on supply of goods and/or services. Failure to report input tax credit correctly can result in incorrect assessment and in case of wrong availment of the input tax credit, interest at prescribed rate and besides recovery of such wrongly availed input tax credit, penalty is also attracted.

(iv) Incorrect reporting of turnover: It has to be ensured that the taxpayers report their turnover correctly to avoid incorrect assessment.

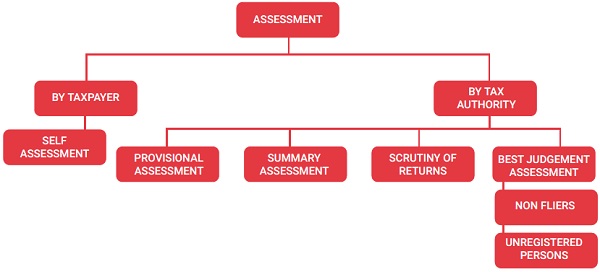

4. TYPES OF ASSESSMENT UNDER GST

The following are the types of assessment under GST:

5. SELF-ASSESSMENT

5.1 Section 59 of the CGST Act, 2017, provides that every registered person shall self-assess the taxes payable and furnish the prescribed return for each tax period. This is the first level of assessment, which is done by the taxpayers themselves. In self-assessment, the taxpayer calculates and declares his tax liability in the returns filed and pays his tax liability at the time of filing the return. This is done on a monthly, quarterly or annual basis, depending on the turnover of the taxpayer. (Section 59 of CGST Act, 2017)

5.2 Self-Assessment does not confer authority of an assessing officer on the taxpayer. A taxpayer is required to exercise this liberty to assess tax liability voluntarily with the risk of interest and penalty for any miscalculations or misinterpretations without usurping the role of proper officer.

5.3 If the taxpayer discovers any omission or incorrect particulars in the returns furnished by him, other than the omissions or commissions pointed out by the proper officer consequent to scrutiny of return or audit or inspection or incorrect particulars, then the taxpayer has to rectify such omissions or incorrect particulars and pay the differential tax, if any, along with interest.

5.4 The rectification mentioned above is allowed to be carried out only till the 30th day of November following the end of financial year to which such omissions or incorrect particulars pertain to or the actual date of filing of the Annual Return of the relevant financial year, whichever is earlier.

6. PROVISIONAL ASSESSMENT

6.1 General features of Provisional Assessment:

(i) The major factors for determining the tax liability are generally the applicable tax rate and the value. There may be situations when these factors might not be readily ascertainable and may be subject to the outcome of a process that requires deliberation and time. In such scenario it may not be possible for the taxpayer to carry out the self-assessment and determine the exact duty liability.

(ii) To deal with such scenario, Section 60 of the CGST Act, 2017 provides for provisional assessment in two possible situations (Section 60 of CGST Act, 2017)–

(a) when the taxpayer is unable to determine the value of supply; and

(b) when the taxpayer is unable to determine the rate of tax.

Apart from the above two scenarios, provisional assessment cannot be applied by the taxpayer for any other purpose.

(iii) The taxpayer has to make request in writing, along with the relevant documents and giving reasons for payment of tax on provisional basis.

(iv) The proper officer shall pass an order, allowing payment of tax on a provisional basis at such rate or on such value, as may be specified by him, if the taxpayer executes a bond in the prescribed form with surety or security as determined by the proper officer, binding himself for payment of the differential tax amount on finalization of the assessment.

(v) The final assessment order should be passed by the proper officer within six months from the date of communication of provisional assessment order. The period of six months can be extended by the Joint Commissioner or Additional Commissioner for further period not exceeding six months and by the Commissioner for further period not exceeding four years, if sufficient cause is shown and reasons are recorded in writing.

(vi) On finalization of the provisional assessment, any amount that has been paid on the basis of such assessment is to be adjusted against the amount that has been finally determined as payable. In case of short payment, the same has to be paid with interest from the first day after the due date of payment of tax in respect of the supplies subjected to provisional assessment till the date of actual payment.

(vii) The taxpayer is entitled for refund of tax paid in excess consequent to the order of final assessment and interest is payable to the taxpayer on such refund in terms of Section 56 of the CGST Act, 2017. (Section 56 of the CGST Act, 2017)

6.2 Procedure for Provisional Assessment:

(i) The procedure for provisional assessment is laid down in Rule 98 of the CGST Rules, 2017. (Rule 98 of CGST Rules, 2017)

(ii) As per Rule 98(1) of the CGST Rules, 2017 the taxpayer has to make request to the proper officer, i.e. the jurisdictional Assistant/ Deputy Commissioner of Central Tax, electronically in FORM GST ASMT-01 on common portal, along with the relevant documents and giving reasons for payment of tax on provisional basis.

(iii) The proper officer will scrutinize the application of the taxpayer made in FORM GST ASMT-01. In case additional information or documents in support is required to decide the case, then in terms of Rule 98(2) of the CGST Rules, 2017 the proper officer shall issue notice in FORM GST ASMT-02 to the taxpayer requesting for submission of the As provided under Rule 98(2) of the CGST Rules, 2017 the taxpayer may file a reply to the notice in FORM GST ASMT–03, and can also appear in person before the said proper officer, if he so desires, to explain his case.

(iv) As per Rule 98(3) of the CGST Rules, 2017, the proper officer, on being satisfied with the reasons given by the taxpayer for seeking provisional assessment, will issue an order in FORM GST ASMT-04 within a period of ninety days from the date of receipt of the request, allowing the payment of tax on a provisional basis. The order should indicate the value or the rate or both on the basis of which the assessment is to be allowed on a provisional basis and the amount (including the amount of Integrated tax, Central tax, State tax or Union territory tax and cess payable in respect of the transaction), for which the bond is to be executed along with the security to be furnished. The security will not exceed twenty-five percent of the amount covered under the bond. (Rule 98(3) of the CGST Rules, 2017)

(v) In terms of Rule 98(4) of the CGST Rules, 2017 the taxpayer has to execute the bond in FORM GST ASMT-05 along with a security in the form of a bank guarantee for an amount, as mentioned in FORM GST ASMT-04. The bond furnished to the proper officer under the State Goods and Services Tax Act or Integrated Goods and Services Tax Act shall be deemed to be a bond furnished under Central Goods and Services Tax Act 2017. (Rule 98(4) of CGST Rules, 2017)

(vi) On executing the bond, the process of the provisional assessment is complete and the supplier can supply the goods or services or both and pay the tax at the rate or on the value that has been indicated in the order in FORM GST ASMT-04.

6.3 Finalisation of provisional assessment:

(i) The provisional assessment will be finalized within a period of six months from the date of issuance of FORM GST ASMT-04. The time limit for finalization of provisional assessment can be extended by the Joint Commissioner or Additional Commissioner for a further period not exceeding six months and by the Commissioner for such further period not exceeding four years, if sufficient cause is shown and reasons are recorded in writing.

(ii) As per Rule 98(5) of the CGST Rules, 2017, the proper officer, i.e. the jurisdictional Asst. Commissioner/Dy. Commissioner of Central Tax will issue a notice in FORM GST ASMT-06, calling for information and records required for finalization of assessment. He shall issue a final assessment order, specifying the amount payable by the taxpayer or the amount refundable, if any, in FORM GST ASMT-07. (Rule 98(5) of the CGST Rules, 2017)

6.4 Interest liability:

(i) In case any tax amount becomes payable subsequent to finalization of the provisional assessment, then interest at the specified rate will also be payable by the taxpayer from the first day after the due date of payment of the tax till the date of actual payment, whether such amount is paid before or after the issuance of order for final assessment.

(ii) In case any tax amount becomes refundable subsequent to finalization of the provisional assessment, then interest at the specified rate will be payable to the taxpayer, subject to the eligibility of refund and absence of unjust enrichment.

6.5 Release of Security:

(i) Rule 98(6) of the CGST Rules, 2017 provides that after issuance of the order in FORM GST ASMT-07 mentioned above, the taxpayer has to file an application in FORM GST ASMT- 08 for the release of the security furnished. (Rule 98(6) of the CGST Rules, 2017)

(ii) On receipt of the application in FORM GST ASMT-08, the proper officer shall issue an order in FORM GST ASMT– 09 prescribed in Rule 98(7) of the CGST Rules, 2017 within a period of seven working days from the date of the receipt of the application, releasing the security after the amount payable as per the order, if any, as specified in FORM GST ASMT-07, has been paid. (Rule 98(7) of the CGST Rules, 2017)

7. SCRUTINY ASSESSMENT BY PROPER OFFICER

7.1 Scrutiny assessment is a cross check and verification done by the proper officer to verify the correctness of the returns filed by taxpayers. This is applicable for only registered persons and not to unregistered persons.

7.2 Section 61 (1) of the CGST Act, 2017 provides that the proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform him of the discrepancies noticed, if any, in the prescribed manner and seek explanation on the same. (Section 61(1) of CGST Act, 2017)

7.3 Section 61(2) of the CGST Act, 2017 provides that in case the explanation is found acceptable, the registered person shall be informed accordingly and no further action shall be taken in this regard. However, if no satisfactory explanation is furnished within the stipulated time of thirty days or where the registered person, after accepting the discrepancies, fails to take the corrective measure in his return for the month in which the discrepancy is accepted, the tax authorities may initiate the following actions- (Section 61(2) of CGST Act, 2017)

- Conduct a tax audit under Section 65 of CGST Act, 2017; or (Section 65 of CGST Act, 2017)

- Start a special audit under Section 66 of CGST Act, 2017; or (Section 66 of CGST Act, 2017)

- Inspect and search the places of the taxpayer’s business under Section 67 of CGST Act, 2017; or

- Initiate demand and recovery provisions; or

- Send notices under Section 73 of CGST Act, 2017 for outstanding demand or shortfall of tax, when there is no wilful intention of doing fraud or suppression of facts or wilful misstatement of facts; or (Section 73 of CGST Act, 2017)

- Send notices under Section 74 of CGST Act, 2017 for outstanding demand or shortfall of tax when there is wilful intention of fraud or suppression of facts or wilful misstatement of facts. (Section 74 of CGST Act, 2017)

7.4 Procedure for Scrutiny Assessment:

(i) A Scrutiny Module for online scrutiny of returns is available for scrutiny of returns filed in FY 2019-20 onwards.

(ii) The Superintendent of Central Tax is assigned as a proper officer for performing functions, as stated under section 61 of the CGST Act, 2017. (Section 61 of CGST Act, 2017)

(iii) Central Board of Indirect Taxes and Customs (CBIC) has issued two SOPs (Standard Operating Procedures), Instruction No. 02/2022-GST dated 22.03.2022 and Instruction No. 02/2023-GST dated 26.05.2023, to ensure uniformity in selecting returns for scrutiny in 2022 for FY 2017-18 and FY 2018-19 as well as in 2023 for FY 201920 onwards. The details of the said SOP have been discussed at length in the later part of this CHAPTER.

(iv) As per Rule 99 of the CGST Rules, 2017, when a return is selected for scrutiny, the proper officer shall scrutinise the same as per Section 61 based on information available to him. The discrepancies shall be intimated to the taxpayer via Form GST ASMT-10 and seek his explanation within 30 days from the date of service of notice (Rule 99 of CGST Rules, 2017)

(v) If the discrepancies pointed out in FORM GST ASMT-10 is not acceptable to the taxpayer then he has to submit his explanation electronically through common portal vide FORM GST ASMT-11 [Rule 99(2)].

(vi) If the reply of the taxpayer is found to be satisfactory and acceptable, then the proper officer may inform the taxpayer electronically in FORM GST ASMT-12 [Rule 99(3)].

(vii) If no explanation is provided by the taxpayer or if he fails to pay tax within 30 days of intimation, the proper officer may proceed to determine the tax and other dues as per Section 73 or Section 74 of CGST Act, 2017. The officer may refer the matter to the Jurisdictional Principal Commissioner or Commissioner, if he believes that an audit or investigation is required to determine the correct amount of liability. The Principal Commissioner or Commissioner can decide the appropriate action, like audit by the tax officers under Section 65, special audit by a Chartered Accountant or a Cost Accountant nominated by Commissioner under Section 66 or inspection, search and seizure in terms of Section 67 to be referred to the Audit Commissionerate or Anti Evasion Wing. (Section 73 & 74 of CGST Act, 2017) (Section 65, 66 & 67 of CGST Act, 2017)

(viii) No order can be passed under scrutiny assessment as it is not a legal or judicial proceeding.

(ix) Presently the Directorate General of Analytics and Risk Management (DGARM) selects the GSTIN whose returns are to be scrutinised and communicates the same to the field formations through the DDM portal. The DGARM will make the list of GSTINs available through the DG systems on the scrutiny dashboard of the officers on the ACES-GST application.

(x) The list of parameters for selection of GST returns for scrutiny are as follows-

(a) The tax liability in Tables 3.1(a) and (b) of GSTR-3B must match with tax liability in Tables 4, 5, 6. 7A(1), 7B(1), 11A and 11B of GSTR-1 [Net of amendments in Tables 9, 10, and 11(II)].

(b) Advances adjusted are accurately reflected by reporting the same in Table 11B and Tables 4, 5, 6 and 7 of GSTR-1.

(c) Reporting and paying in cash the exact tax liability under the reverse charge mechanism using Tables 3.1(d) for tax liability and 4(A)(2) and 4(A)(3) for ITC claimed on it in GSTR-3B. The value in GSTR-3B should be more than the eligible ITC in Tables 3, 4, 5 and 6 of GSTR-2A.

(d) ITC claimed in Table 4(A)(4) of GSTR-3B should match with amounts marked as eligible ITC in Table 7 of GSTR-2A (Net of amendments in Table 8).

(e) Sales subjected to TCS or TDS under GST in GSTR-3B should match the TDS and TCS credit reflected under Column 6 of Table 9 of the GSTR-2A.

(f) In Table 3.1(a) and (b) of the GSTR-3B the tax liability should match with the corresponding e-way bills.

(g) ITC is ineligible for claims for the period after the effective date of cancellation of the supplier’s GST registrations, especially in case of retrospective cancellation of GST registrations.

(h) The GSTR-3B filing status of respective vendors must not be ‘No’ while claiming ITC of such invoice or debit note in the GST returns, despite it appearing in the GSTR-2A.

(i) No ITC should be claimed if the relevant period’s GSTR-3B is filed after the last date allowed under Section 16(4) of the CGST Act, 2017, i.e. 30th November of the year following the financial year in which such invoice/debit note is raised or date of filing annual returns, whichever is earlier. (Section 16(4) of CGST Act, 2017)

(j) ITC on import of goods in Table 4(A)(1) of GSTR-3B should match with amounts in Tables 10 and 11 of GSTR-2A and data on ICEGATE.

(k) Adherence to Rule 42 and 43 of CGST Rules, 2017 for accurate reversals of ITC in Table 4(B) of GSTR-3B. (Rule 42 & 43 of CGST Rule, 2017)

(l) Computation and payment of late fee/interest as per Sections 47 and 50 of the CGST Act, 2017, wherever return filing/tax payment is delayed. (Section 47 & 50 of CGST Act, 2017)

(xi) The CGST department has introduced the automated return scrutiny module for returns from FY 2019-20 onwards. It ensures minimal manual intervention in the adjudication process, making it more transparent, efficient and bridges any gaps leading to tax evasion.

(xii) A month-wise schedule shall be prepared by the proper officer for scrutiny regarding all GSTINs selected. The priority may be based on the revenue implication involved. GSTINs with a higher revenue implication shall be prioritised.

(xiii) The proper officer scrutinises the return for its correctness based on the information available on the system in various forms and statements filed by the registered taxpayer and other sources, such as, DGARM, ADVAIT, E-way Bill portal, etc.

(xiv) The proper officer is expected to depend on the information available to the Department itself. He should have a minimal interface with the taxpayer and normally should not ask for documents from the taxpayer before the issuance of FORM GST ASMT-10.

(xv) The proper officer shall issue a notice to the taxpayer indicating all the discrepancies noticed and seek his explanation thereon in FORM GST ASMT-10. He shall quantify the tax, interest, and other such sums payable regarding the discrepancies noticed. If the registered taxpayer has already made the additional tax payment through FORM GST DRC-03, then the same should be considered while communicating discrepancies to the taxpayer in FORM GST ASMT-10.

(xvi) For each selected GSTIN, the proper officer must scrutinize all the returns of the corresponding financial year and issue a single notice via FORM GST ASMT-10.

(xvii) The scrutiny of returns shall be completed in a specified period to safeguard revenue. Below are some of the timelines:

| Sr. No. | Process | Time Line |

| 1 | Communicating the list of GSTINs selected for scrutiny by the DGARM to the nodal officer | From time to time |

| 2 | Communicating the list of GSTINs selected for scrutiny by the nodal officer to the proper officer | Within 3 working days from the date of receipt of the list of GSTINs from the DGARM (not applicable for online scrutiny from FY 2019-20 onwards) |

| 3 | Finalisation of scrutiny schedule with the Assistant/ Deputy Commissioner | Within 7 working days of receipt of the list of GSTINs from the nodal officer (from FY 19-20 scrutiny onwards, it is available online on ACES portal) |

| 4 | Sharing the scrutiny schedule with the DGGST | Within 30 days of receipt of the list of GSTINs from DGARM |

| 5 | Issue of notice in Form GST ASMT-10 | Within a month as specified in the scrutiny schedule |

| 6 | Issue of response in GST ASMT-11 | Within 30 days of service of notice under GST ASMT-10 |

| 7 | Issue of order in Form GST ASMT-12 | Within 30 days of receipt of response in Form GST ASMT-11 |

| 8 | Initiating action for determining tax under section 73 and section 74 | If the reply is received: Within 30 days from receipt of reply in GST ASMT-11.

If the reply is not received: Within 15 days of completion of 30 days of service of notice in GST ASMT-10 or further period as may be notified by the proper officer. |

| 9 | Reference to Commissioner for taking appropriate action under section 65, section 66 or section 67 | If the reply is received: Within 30 days from receipt of reply in GST ASMT-11.

If the reply is not received: Within 45 days of service of notice in GST ASMT-10. |

(xviii) A Scrutiny Register shall be maintained by the proper officer for all the GSTINs allotted for scrutiny in the format prescribed in Instruction No. 2/2022-GST, dated 22.03.2022, issued by GST Policy Wing of CBIC. For scrutiny from the FY 2019-20 onwards, MIS report of scrutiny register along with the ‘Monthly Scrutiny Progress Report’ is available on the dashboard of the officer over the ACES portal.

(xix) The progress of the scrutiny shall be monitored by the jurisdictional Principal Commissioner every month. The proper officer shall prepare a scrutiny progress report at the end of every month in the prescribed format in Instruction No. 2/2022-GST, dated 22.03.2022, issued in GST Policy Wing of CBIC. This report shall be forwarded to the Director General of Goods and Service Tax by the Principal Chief Commissioner of the concerned zone by the 10th of the succeeding month. The DGGST shall submit this report to the Board by the 20th of the corresponding month.

(xx) Instruction No. 02/2022-GST issued by GST Policy Wing of CBIC on 22.03.2022 shall be followed for the scrutiny of returns for the financial years 2017-18 and 2018-19 whereas the Instruction No. 02/2023-GST issued on 05.2023 will be followed along with the previous instruction for FY 2019-20 onwards.

8. BEST JUDGMENT ASSESSMENT IN RESPECT OF NON-FILERS

8.1 Assessment in respect of the non-filers of statutory returns is vital for maintaining compliance and identifying taxpayers who haven’t met their filing responsibilities. To tackle non-compliance, the GST law has instituted diverse measures while aiming to prompt regular filing among taxpayers.

8.2 Continuous vigil is maintained on the GST portal to pinpoint registered taxpayers who fail to submit their returns by the specified deadlines. Through the GST system, reports and alerts are automatically generated for non-filers, aligned with the frequency of return filing, whether it’s on a monthly, quarterly, or annual basis.

8.3 Intimations are sent to non-filers, outlining their failure to submit returns within the set timeframe. If the taxpayer disregards the intimation or fails to file the necessary returns within the specified duration after receiving the intimation/ notice, assessment proceedings can be initiated.

8.4 In case of absence of any of the essential points required for regular assessment, i.e., non-submission of documents and records by taxable person, proper officer not satisfied with the correctness of records submitted by taxable person or taxable person not co-operating with proper officer for enabling him to complete the regular assessment, in such cases, the proper officer will determine the tax liability of the taxable person to the best of his judgement on the basis of records, documents or any other information in possession of such proper officer.

8.5 In such cases either no documents or records are furnished/claims are not substantiated or the records and/ or evidence produced before the proper officer are rejected as being unreliable or incomplete/incorrect, either wholly or in part.

8.6 Section 62 of the CGST Act, 2017 provides for best judgement assessment in respect of such non-filers of returns prescribed under Section 39 or Section 45 ibid. (Section 62, 39 & 45 of the CGST Act, 2017)

8.7 Section 46 of the CGST Act, 2017 read with Rule 68 of CGST Rules, 2017 provides for issuance of notice in FORM GSTR-3A to the person who fails to file the statutory returns, viz, GSTR-3B return and GSTR-10 (Final Return), prescribed under Section 39 and 45, respectively. Issuance of notice under Section 46 operates as a precondition for initiating proceedings under Section 62 of the said Act. (Rule 68 of the CGST Rules, 2017)

8.8 Section 62 of the CGST Act, 2017 states that if a registered taxable person fails to furnish the return under Section 39 or Section 45 even after the service of a notice under Section 46, which provides for issuance of notice to the non-filers, the proper officer may assess the tax liability of such person to the best of his judgement taking into account all the relevant material available or which he has gathered and issue an assessment order within a period of five years from the due date for furnishing of the annual returns for the financial year to which the tax not paid relates. (Section 62, 39 45, 46 of the CGST Act, 2017)

8.9 The provisions of Section 62 can be invoked only in case of registered taxable persons who have failed to file returns, as required, under Section 39 or final return on cancellation of registration under Section 45 of the Act. Section 62 cannot be invoked for non-filing of GSTR-1 or GSTR-9 Annual Return.

8.10 If the taxpayer fails to furnish the return within 15 days of issue of notice under Section 46 then the proper officer may assess the tax liability in accordance with the provisions of Rule 100 of the CGST Rules, 2017. (Rule 100 of the CGST Rules, 2017)

8.11 The Best Judgement Assessment has to be made on the basis of the material available on record and the information gathered by the proper officer and the circumstances of each case.

8.12 In terms of Rule 100 of the CGST Rules, 2017, the order of assessment made under Section 62(1) has to be issued in FORM GST ASMT-13 and a summary thereof shall be uploaded electronically in FORM GST DRC-07. (Section 62(1) of the CGST Act, 2017)

8.13 If the taxpayer furnishes a valid return within 30 days of the service of the above said assessment order in FORM GST ASMT-13, the said assessment order shall be deemed to have been withdrawn but the liability for payment of interest under Section 50(1) or for the payment of late fee under Section 47 shall continue. However, if the taxpayer fails to furnish a valid return within sixty days of the service of the said assessment order, he may furnish the same within a further period of sixty days on payment of an additional late fee of one hundred rupees for each day of delay ‘beyond sixty days of the service of the said assessment order and in case he furnishes valid return within such extended period, the said assessment order shall be deemed to have been withdrawn, but the liability to pay interest or to pay late fee will remain. (Section 47 & 50(1) of the CGST Act, 2017)

8.14 In case returns are not filed within 30 days even after the order of best judgement is passed under Section 62, the order becomes final and even if returns are filed subsequently, the order cannot be withdrawn. (Section 62 of the CGST Act, 2017)

8.15 Since FORM GST DRC-07 will also be issued, best judgement assessment under section 62 will lead to recovery of tax assessed and demand made in order in FORM GST ASMT-13.

8.16 CBIC, vide its Circular No. 129/48/2019, dated 24-12-2019 has issued Standard Operating Procedure in respect of the assessment of non-filers.

9. ASSESSMENT OF UNREGISTERED PERSONS

9.1 Section 63 of the CGST Act, 2017 provides that when a taxable person fails to obtain registration even though liable to do so or whose registration has been cancelled under sub section (2) of Section 29 but who was liable to pay tax, the proper officer may proceed to assess the tax liability of such taxable person to the best of his judgement for the relevant tax periods. (Section 63 & 29(2) of the CGST Act, 2017)

9.2 Under Section 63 of the CGST Act, 2017, even when a taxable person is ‘unregistered’, the proper officer is vested with jurisdiction to not only identify taxable transactions but also pass an order of assessment on best judgement basis and fasten an enforceable demand. However, once registration is obtained, use of best judgement method permitted in case of unregistered persons cannot be applied against registered persons even for the period prior to their date of registration.

9.3 For assessment of unregistered person, the proper officer has to resort to third party sources like information shared with Income Tax, ROC, etc. Information can also be gathered by initiating search and seizure proceedings after taking necessary approvals of the Competent Authority.

9.4 The proper officer will issue an assessment order within a period of five years from the due date for furnishing of the annual return for the financial year to which the tax not paid relates.

9.5 No such assessment order shall be passed without giving the person an opportunity of being heard.

9.6 Rule 100(2) of the CGST Rules, 2017 prescribes that the proper officer shall issue a notice to a taxable person in accordance with the provisions of Section 63 in FORM GST ASMT-14 containing the grounds on which the assessment is proposed to be made on best judgment basis and shall also serve a summary thereof electronically in FORM GST DRC-01. (Rule 100 (2) of the CGST Rules, 2017)

9.7 After allowing a time of fifteen days to furnish reply, if any, the proper officer shall pass an order in FORM GST ASMT-15 and summary thereof shall be uploaded electronically in FORM GST DRC-07.

10. SUMMARY ASSESSMENT

10.1 Summary assessment means a fast-track assessment based on the return filed by the taxpayer and is done in certain special cases to protect the interest of revenue. Summary assessment is usually done in cases of defaulting or absconding taxpayers when the tax authorities believe that the taxpayer is trying to evade tax or when there is a threat to revenue.

10.2 Before initiation of Summary Assessment, there must be evidence of tax liability and the proper officer should have sufficient ground that delay in assessment may adversely affect the interest of revenue. Therefore, the assessment is required to be completed on priority basis without the presence of the taxpayer.

10.3 Section 64 of the CGST Act, 2017 empowers the proper officer to carry out Summary Assessment with prior permission of the Additional Commissioner or Joint Commissioner, if he has evidence that the taxpayer has incurred a liability to pay tax and has sufficient ground to believe that delay in passing order will adversely affect the interest of revenue. That means, Summary Assessment cannot be initiated by the proper officer suo moto. (Section 64 of the CGST Act, 2017)

10.4 Summary assessments are often carried out in situations where it is not possible to identify the taxable person concerned in a case of supply of goods. If some person comes forward to claim the ownership of the unaccounted goods and to pay tax thereon, then for that he will be the taxable person. When the taxable person is not ascertainable then as per proviso to Section 64(1) of the CGST Act, 2017, in such cases the person incharge of such goods at that relevant time shall be deemed to be the taxable person and the tax liability is fastened on such person.

10.5 The procedure to be followed in respect of Summary Assessment is provided in Rule 100 of the CGST Rules, 2017.

10.6 There is no provision to issue any notice before passing the assessment order. However, opportunity to produce documents showing details of goods and to prove that such goods are accounted is given during the course of the Summary Assessment proceedings.

10.7 Rule 100(3) CGST Rules, 2017 provides for issuance of order of assessment in FORM GST ASMT-16 and the summary of the order shall be uploaded electronically in FORM GST DRC-07. (Rule 100(3) of the CGST Rules, 2017)

10.8 No time limit has been prescribed for passing the above said order. It is necessary to pass a speaking order containing introduction, discussion and finding, conclusion, amount of all applicable taxes (CGST/SGST/IGST) assessed, interest and penalty payable.

10.9 Section 64(2) of the CGST Act, 2017 provides that the taxable person against whom the Summary Assessment order is passed, can apply to the Additional Commissioner or Joint Commissioner electronically in FORM GST ASMT-17 [Rule 100(4)]. for withdrawal of said order, within 30 days from the date of receipt of the order. The Additional Commissioner after considering the grounds made by such taxable person in his application, shall either withdraw the Summary Assessment order if the same is found erroneous or reject the application if the grounds are not legally acceptable. The order of withdrawal of Summary Order or rejection of the application of taxable person, has to be issued in FORM GST ASMT-18 [Rule 100(5)].

*****

Source: Handbook of GST Law and Procedures for Departmental Officers issued by Ministry of Finance