RETURNS & SCRUTINY THEREOF

1. INTRODUCTION

1.1 In every taxation system the liability of tax payable by a person has to be determined and assessed. The GST law provides for various kinds of assessment. Self-assessment of the tax liability is one of them. Every registered taxable person is required to himself assess his liability of taxes payable and furnish a return for each tax period.

1.2 The provisions of CGST Act, 2017 and CGST Rules, 2017 relevant to this Chapter are as under –

| Sr. No. Section/Rule Provision pertaining to | ||

| 1 | Section 37 and Rule 59 | Furnishing details of outward supplies |

| 2 | Section 38 and Rule 60 | Furnishing details of inward supplies |

| 3 | Section 39 and Rule 61 | Furnishing of returns |

| 4 | Section 10 | Annual return filed by Composition Scheme taxpayers |

| 5 | Section 40 | First return |

| 6 | Section 44 and Rule 80 | Filing annual returns |

| 7 | Section 45 and Rule 81 | Filing of return by taxpayers whose registration is cancelled |

| 8 | Section 46 and Rule 68 | Notice to return defaulters |

| 9 | Section 47 | Levy of late fee |

| 10 | Section 50 | Interest on delayed payment of tax |

| 11 | Section 61 | Scrutiny of returns |

| 12 | Section 62 | Assessment of Non-Filers of returns |

| 13 | Section 83 | Provisional attachment to protect revenue in certain cases |

| 14 | Rule 63 | Submission of return by non-resident taxable person |

| 15 | Rule 64 | Submission of return by persons providing online information and database access or retrieval services |

| 16 | Rule 65 | Submission of return by Input Service Distributor |

| 17 | Rule 67 | Form and manner of submission of statement of supplies through an e-commerce operator |

| 18 | Rule 67A | Manner of furnishing of return or details of outward supplies by SMS facility |

| 19 | Rule 68 | Notice to Non-Filer |

| 20 | Section 125 | Delay in filing GSTR-9C attracts general penalty |

| 21 | Rule 82 | Details of inward supplies of persons having UIN |

| 22 | Rule 99 | Scrutiny of returns |

1.3 A GST return is a document containing details of all purchases, sales, taxes paid on purchases (input tax) and taxes collected on sales (output tax). A GST Taxpayer (every taxpayer holding GSTIN) is required to file the return electronically on the GST Common Portal. Return is the basis for assessment and an important aspect under GST law, as all control over the tax paid and input tax credit availed is on the basis of return filed by the Taxpayer.

1.4 There are a whole lot of activities that form a part of the process of Returns under GST. These include:

- Filing different types of GST returns electronically.

- Uploading invoice wise details.

- Auto-population of details with regards to input tax credit from returns filed by suppliers to return filed by recipients.

- Matching of invoice information.

- Automatic reversal of ITC in the event of mismatch of the invoice information.

1.5 The returns filed by the Taxpayer are scrutinised by the proper officer to verify the correctness of the tax liability discharged on the supplies made by such Taxpayer. If any discrepancies are observed, then the officer may ask for an explanation from the Taxpayer and if the explanation is not found satisfactory then he may initiate further proceedings, as provided under the CGST Act, 2017 and the rules made thereunder for recovery of the tax short-paid or not paid or input tax credit wrongly availed.

1.6 In GST the basic features of the return mechanism includes electronic filing of returns, uploading of invoice level information, auto-population of information relating to input tax credit from returns of supplier to that of recipient, invoice level information matching and auto-reversal of input tax credit in case of mismatch. The returns mechanism is designed to assist the taxpayer to file returns and avail ITC.

1.7 The provisions under Section 37 to Section 40 of the CGST Act, 2017 stipulate the various types of Returns to be filed under the GST law. The type (Form) and manner of furnishing the returns by various class of Taxpayers is provided under Rule 59 to 67A of the CGST Rules, 2017.

1.8 A regular Taxpayer has to furnish monthly returns and one annual return. The GST law also provides a facility called Quarterly Return Monthly Payment (QRMP), for the Taxpayers with turnover less than Rs. 5 Crore during the preceding financial year and current financial year, under which the returns in FORM GSTR-3B and FORM GSTR-01 are required to be filed on Quarterly basis with monthly payment of tax. As per Notification No. 84/2020-Central Tax, dated 10.11.2020, a registered person who is required to furnish a return in FORM GSTR-3B and has an aggregate turnover upto Rs. 5 Crore in the preceding financial year, is eligible for the QRMP scheme, whereunder such person can opt to file the return on Quarterly basis. However, the tax payment shall be on monthly basis. Circular No. 143/13/2020-GST, dated 10.11.2020, issued by CBIC provides the details of the QRMP Scheme and the clarifications thereof.

1.9 Taxpayers are mandatorily required to file returns, depending on the activities they undertake. There are separate returns for the Taxpayer registered under the Composition Scheme, Non-resident Taxpayer, Taxpayer registered as an Input Service Distributor, a person liable to deduct or collect the tax (TDS/TCS), a person granted Unique Identification Number, etc.

2. TYPES OF RETURNS UNDER GST LAW

2.1 FORM GSTR-1 for furnishing details of outward supplies:

(i) FORM GSTR-1 is the return prescribed under Section 37(1) of the CGST Act, 2017 for reporting details of all outward supplies of goods and services made during the relevant period of the return, in the manner prescribed under Rule 59 of the CGST Rules, 2017. (Section 37(1) of the CGST Act, 2017) (Rule 59 of CGST Rules, 2017)

(ii) As per Section 37(1) of the CGST Act, 2017, every registered Taxpayer (other than an input service distributor, a non-¬resident taxable person and a person paying tax under Composition Scheme in terms of the provisions of Section 10, persons registered as ‘deductor of tax’ (TDS) in terms of Section 51 or the e-commerce Operator collecting tax at source (TCS) in terms of Section 52 of the CGST Act, 2017) has to file the GSTR-1 return in the prescribed manner and time and shall be communicated to the recipient of the said supplies. (Section 10, 51 and

52 of CGST Act, 2017)

(iii) The frequency of filing the return is monthly. However, the class of Taxpayers who have opted for filing of return on Quarterly basis in terms of the proviso to Section 39(1) of the CGST Act, 2017 under the Quarterly Return Monthly Payment Scheme (QRMP), can furnish the return in FORM GSTR-1 on Quarterly basis. (Section 39(1) of CGST Act, 2017)

(iv) Details of outward supplies include details of invoices, debit notes, credit notes and revised invoices issued in relation to outward supplies during any tax period.

(v) GSTR-1 is to be filed by all normal taxpayers who are registered under GST, including casual taxable persons. Delay in filing the return attracts penalty, as applicable.

(vi) ‘Nil’ return is mandatory even if there are no transactions in a month/quarter.

(vii) Any amendment to sales invoices made, even pertaining to previous tax periods, must be reported in the GSTR-1 return by all the suppliers or sellers registered under GST.

(viii) The due date for filing GSTR-1 return is:

(a) For Monthly return filers, by 11th of every month.

(b) For Quarterly return filers under the QRMP scheme, by 13th of the month following every quarter.

2.2. FORM GSTR-2A containing details of all inward supplies:

(I) Section 38 of the CGST Act, 2017, stipulates that the details of outward supplies furnished by the registered persons in GSTR-1 return and of such other supplies, containing the details of input tax credit, shall be made available electronically by an auto-generated statement through the common portal, to the recipients of such supplies. (Section 37 and 38 of CGST Act, 2017)

(II) Rule 60 of the CGST Rules, 2017 prescribes that the details of the inward supplies is required to be made available to the recipient in FORM GSTR-2A. (Rule 60 of CGST Rules, 2017)

(III) GSTR-2A is relevant for the recipient or buyer of goods and services and is a read only document. This document gets auto-populated once the corresponding supplier uploads the details in GSTR-1. In other words, GSTR-2A enables the recipient to verify the details uploaded by the supplier in GSTR 1.

(IV) GSTR-2A contains the details of all inward supplies of goods and services i.e., purchases made from GST registered suppliers during a tax period.

(V) Data filed in the Invoice Furnishing Facility (IFF) by the QRMP Taxpayer, also get auto-filled.

(VI) Since GSTR-2A is a read-only return, no action can be taken in it. However, it is referred by the buyers to claim an accurate Input Tax Credit (ITC) for every financial year, across multiple tax periods.

(VII) The data made available in GSTR-2A enables the recipient to accept, reject, modify or keep the invoices pending using the said details. In case any invoice is missing, the buyer can communicate with the seller to upload it in their GSTR-1 on a timely basis.

(VIII) GSTR-2B was introduced w.e.f. July, 2020 on trial basis and has been statutorily provided w.e.f. 1-1-2021.

(IX) Besides the details of outward supplies provided by the registered supplier in FORM GSTR-1, Rule 60 of CGST Rules, 2017, also provides as under – (Rule 60 of CGST Rules, 2017)

(i) The details of invoices furnished in FORM GSTR-5 by the non-resident Taxpayer shall be made available to the recipient electronically in Part A of FORM GSTR-2A;

(ii) The details of invoices furnished by Input Service Distributor in his return in FORM GSTR-6 shall be made available to the recipient electronically in Part B of GSTR-2A;

(iii) The details of TDS furnished by the deductor in FORM GSTR-7 shall be made available to the concerned person electronically in Part C of FORM GSTR-2A;

(iv) The details of the TCS furnished by an e-commerce operator in FORM GSTR-8 shall be made available to the concerned person in Part C of GSTR-2A.

(v) The details of the IGST paid on the import of goods or goods brought in Domestic Tariff Area (DTA) from Special Economic Zone (SEZ) unit or a SEZ Developer, on a Bill of Entry, shall be made available in Part D of GSTR-2A.

2.3 FORM GSTR-2B containing details of all inward supplies:

(I) Rule 60(7) of the CGST Rules, 2017 prescribes that an auto-generated statement containing the details of input tax credit shall be made available electronically through the common portal, to the registered Taxpayer in FORM GSTR-2B every month. (Rule 60(7) of CGST Rules, 2017)

(II) GSTR-2B is a static auto-drafted statement for regular taxpayers. It is available month wise and was introduced on the GST portal from the August 2020 tax period onwards.

(III) ITC details covered in the return is from the date of filing GSTR-1 for the preceding month up to the date of filing GSTR-1 for the current month.

(IV) The details of ITC in this return do not get altered for a particular tax period, even if the seller makes revisions. Hence, the taxpayers can refer to the ITC appearing in this return for eligible ITC claims in GSTR-3B for a tax period.

(V) The return is made available to the registered Taxpayer on the 12th of every month, giving sufficient time before filing GSTR-3B, where the ITC is declared.

(VI) The GSTR-2B provides the action to be taken against every invoice reported, such as, to be reversed, ineligible, subject to reverse charge, references to the table numbers in GSTR-3B.

(VII) ITC cannot be claimed if it is restricted in GSTR-2B.

2.4 GSTR-3B return –Details of outward supplies, inward supplies, tax liability, tax paid:

(i) Section 39(1) of the CGST Act, 2017 states that every registered person (other than an Input Service Distributor or a non-resident taxable person or a person paying tax under Composition Scheme or a person deducting tax at source or a person collecting tax at source) is required to furnish a return electronically through the common portal, consisting details of inward and outward supplies of goods or services or both, input tax credit availed, tax payable, tax paid and such other particulars. (Section 39(1) of CGST Act, 2017)

(ii) Rule 61 of the CGST Rules, 2017 prescribes the manner in which the details are to be provided in FORM GSTR-3B. (Rule 61 of CGST Rules, 2017)

(iii) GSTR-3B is a monthly self-declaration to be filed, for furnishing summarised details of all outward supplies made, inward supplies received, input tax credit claimed, tax liability ascertained and taxes paid.

(iv) Proviso to Section 39(1) of CGST Act, 2017 read with Rule 61(1)(ii) of the CGST Rules, 2017 prescribes filing of return in FORM GSTR-3B on Quarterly basis for taxable persons with turnover of less than Rs. 5 Crore during the last and current financial year and who have opted for the QRMP Scheme. (Rule 61(1)(ii) of CGST Rules, 2017) (Section 39(1) of CGST Act, 2017)

(v) Facility to avail the QRMP Scheme on the common portal would be available throughout the year. The facility for opting out of the QRMP Scheme for a quarter is also available in the prescribed manner. (CBIC Circular No. 143/13/2020-GST dated 10-11-2020).

(vi) GSTR-3B is to be filed mandatorily by all normal Taxpayers registered under GST.

(vii) Taxpayers registered under the Composition Scheme, as Input service distributors, as Non-resident suppliers of OIDAR service and as Non-resident taxable persons are not required to file return in FORM GSTR-3B, as separate FORMS of Return have been prescribed for these type of Taxpayers.

(viii) The sales and input tax credit details must be reconciled with GSTR-1 and GSTR-2B every tax period before filing GSTR-3B. Reconciliation is crucial to identify mismatches in data.

(ix) A separate GSTR-3B must be filed for every GSTIN.

(x) The filing frequency of GSTR-3B is as follows:

(a) For Taxpayers with an aggregate turnover in the previous financial year of more than Rs. 5 Crore or have been otherwise eligible but still opted out of the QRMP scheme the filing frequency is Monthly, by 20th of the succeeding month.

(b) For the taxpayers with aggregate turnover equal to or below Rs.5 crore, eligible and remain opted into the QRMP scheme, the due date is 22nd of the month following the quarter for ‘X’ category of States and 24th of the month following the quarter for ‘Y’ category of States

‘x’ category States/UT – Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana or Andhra Pradesh or the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands and Lakshadweep.

‘y’ category States/UT- Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha or the Union Territories of Jammu and Kashmir, Ladakh, Chandigarh and New Delhi.

(xi) The registered Taxpayer shall not be eligible for the QRMP Scheme of filing quarterly return, unless he has furnished the return for a complete tax period of preceding month in which he has opted for the said scheme. (Notification No. 84/2020-CT dated 10.11.2020)

(xii) The liability of tax, interest and penalty, if any, as calculated in the return, must be paid on or before the date of filing GSTR-3B return, by debiting the tax payable in the Electronic Cash Ledger or Electronic Credit Ledger. The GSTR-3B for a particular period return cannot be filed without discharging the entire liability, as calculated in the return.

(xiii) The registered Taxpayer under the QRMP Scheme is required to pay the tax due in each of the first two months of the quarter, by depositing the due amount in FORM GST PMT-06, by the twenty fifth day of the month succeeding such month. While generating the challan, taxpayers should select “Monthly payment for quarterly taxpayer” as reason for generating the challan (CBIC Circular No. 143/ 13/2020-GST dated 10.11.2020).

(xiv) The GSTR-3B return once filed cannot be revised.

(xv) GSTR-3B must be compulsorily filed even in case of a zero liability for any tax period.

(xvi) The late filing of GSTR-3B attracts a late fee and interest at 18% per annum.

(xvii) In case the tax was paid within the due date but the GSTR-3B was filed after the deadline, both late fees and interest will apply.

(xviii) CBIC has issued a detailed Circular No. 26/26/2017-GST dated 29.12.2017 giving instructions to correct errors made in filing GSTR-3B. The error may be Liability under reported, Liability over reported, Liability wrongly reported, Input Tax Credit under reported, Input tax credit over reported, Input tax credit of wrong tax taken and Cash Ledger wrongly updated. The adjustment can be made only in return of next month, as there is no provision to amend the GSTR-3B return after filing.

(xix) As per Rule 67A of CGST Rules, 2017, ‘Nil’ GSTR-3B return can be filed by the Taxpayer registered as Normal taxpayer/Casual taxpayer/SEZ Unit/ SEZ Developer through SMS, anytime on or after the 1st of the subsequent month for which the return is being filed for. (Rule 67A of CGST Rules, 2017)

(xx) The common portal does not allow filing of GSTR-1 and GSTR-3B returns for the subsequent period if these returns for the earlier period are not filed.

(xxi) Detailed instruction on various aspects for filing the GSTR-3B return is provided in CBIC Circular No. 170/02/2022-GST dated 06.07.2022.

2.5 FORM GSTR-4– Annual Return to be filed by the Taxpayers paying tax under Composition Levy:

(i) Taxpayer involved in intra-state trade and having turnover less than the stipulated limit, are only entitled to opt for payment of tax under Composition Levy scheme. The tax rate under the Composition Levy scheme is 1% of turnover for traders and manufacturers and 5% for restaurants.

(ii) Section 39(2) of the CGST Act, 2017 stipulates that a registered Taxpayer paying tax under the Composition Levy scheme in terms of the provisions of Section 10 ibid, shall furnish a return electronically in the prescribed manner for each financial year or part thereof, declaring the turnover in the State or Union territory, inward supplies of goods or services or both, import of services, supplies attracting reverse charge, tax payable, tax paid and other particulars. (Section 39(2) of CGST Act, 2017)

(iii) The Composition Levy is a scheme in which Taxpayers dealing with goods and having a turnover up to Rs.1.5 Crore can opt and pay taxes at a fixed rate on the turnover declared. The service providers too can avail a similar scheme as per CGST (Rate) Notification No. 02/2019 dated 7th March 2019, if their turnover is up to Rs.50 lakhs.

(iv) As per Rule 62(1)(i) of the CGST Rules, 2017, the Taxpayer under the Composition Levy scheme is required to furnish a statement, every quarter of the year or part thereof declaring the details of payment of self-assessed tax in FORM GST CMP-08, till the 18th day of the month succeeding such quarter. (Rule 62(1)(i) of CGST Act, 2017)

(v) As per Rule 62(1)(ii) of the CGST Rules, 2017, the Taxpayer under the Composition Levy scheme shall furnish the return in FORM GSTR-4, by 30th April following the end of the financial year, electronically. It has replaced the erstwhile GSTR-9A (Annual Return) for the taxpayers under Composition Levy Scheme from FY 2019-20 onwards. (Rule 62(1)(ii) of CGST Act, 2017)

(vi) Prior to FY 2019-20, this return had to be filed on a quarterly basis. Thereafter, a simple challan in FORM CMP-08 filed by 18th of the month succeeding every quarter replaced it.

(vii) Annual return in Form GSTR-4 cannot be filed without filing Form CMP-08, for the applicable period/periods, of the relevant financial year.

(viii) Filing of GSTR-4 is mandatory and even a ‘Nil’ return has to be filed mandatorily. Failure to file the return on or before the due date will attract Late Fees, as applicable.

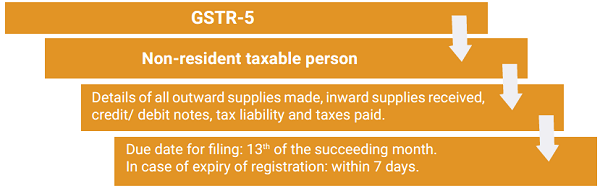

2.6 FORM GSTR-5 –Return for Non-Resident Taxpayer:

(i) Non-resident Taxpayers are the suppliers who do not have a business establishment in India and have come for a short period to make supplies in India.

(ii) The registration issued to a Non-resident Taxpayer is temporary and is valid for the period specified in the application or 90 days from the effective date of registration, whichever is earlier. Such a person can make taxable supplies only after the issuance of the certificate of registration.

(iii) Section 39(5) of the CGST Act, 2017 states that every registered non-resident taxpayer shall furnish a return for every calendar month or part thereof electronically within thirteen days after the end of a calendar month or within seven days after the last day of the period of registration, whichever is earlier. (Section 39(5) of CGST Act, 2017)

(iv) Rule 63 of the CGST Rules, 2017 prescribes that the return is to be filed by registered Non-resident Taxpayer in FORM GSTR-5, electronically through the common portal, which should include therein the details of outward supplies and inward supplies credit/debit notes, tax liability and taxes paid. The Non-resident Taxpayer should pay the tax, interest, penalty, fees or any other amount payable under the Act within twenty days after the end of a tax period or within seven days after the last day of the validity period of registration, whichever is earlier. (Rule 63 of CGST Rules, 2017)

(v) The GSTR-5 return is required to be filed on or before 20th of the following month and within seven days after the last date of validity of the registration. Delay in filing the return attracts Late Fees.

(vi) If GSTR-5 for a particular month is not filed then the return for the subsequent month cannot be filed.

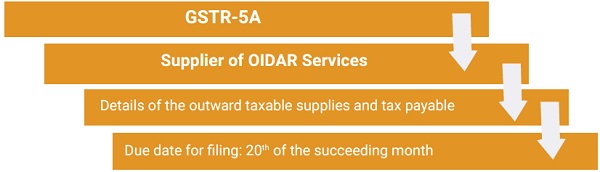

2.7. GSTR-5A – Summary return of tax payable by Non-Resident Online Information and Database Access or Retrieval (OIDAR) Services provider:

(i) Online Information and Database Access or Retrieval services (OIDAR) are primarily a category of services, provided by using the internet as a medium. These services are even received by the service recipient without having a physical interface with the service provider.

(ii) The taxes on services received by a registered Taxpayer are imposed through a reverse charge mechanism, i.e., the recipient of services is liable to pay GST. In respect of the OIDAR services received by unregistered persons or Government or Local Authority, the OIDAR service providers are liable to pay GST.

(iii) Section 39(1) of the CGST Act, 2017 read with Rule 64 of the CGST Rules, 2017 provides for filing of a monthly return in FORM GSTR-5A, by the Taxpayer providing Online Information and Database Access or Retrieval services, from a place outside India to a person, other than a registered Taxpayer, located in India. (Section 39(1) of CGST Act, 2017) (Rule 64 of CGST Rules, 2017)

(iv) GSTR-5A is a summary return for reporting the outward taxable supplies and tax payable by OIDAR Service provider under GST.

(v) The due date to file GSTR-5A is the 20th of the following month. Delay for non-filing of GSTR-5A return attracts interest, Late Fees and penalty, as applicable.

(vi) If there are no transactions of supply of OIDAR services during a particular period even then filing of a ‘Nil’ return is mandatory. Failure to file the ‘Nil’ return attracts Late Fees.

(vii) The OIDAR service providers located overseas can have their authorized representatives to make payment of tax and to file GSTR 5A return on their behalf as their agents.

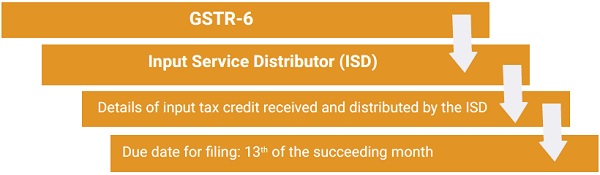

2.8 GSTR-6 – Return to be filed by an Input Service Distributor (ISD):

(i) An Input Service Distributor (ISD) is a taxpayer who receives invoices for services used by its branches.

(ii) ISD distributes the Input Tax Credit (ITC) to their branches on a proportional basis by issuing ISD invoices.

(iii) Section 39(4) of CGST Act, 2017 provides that every Taxpayer registered as an Input Service Distributor shall furnish a return for every calendar month or part thereof, electronically, within thirteen days after the end of such month. (Section 39(4) of CGST Act, 2017)

(iv) Rule 65 of the CGST Rules, 2017 prescribes that the return is to be filed by ISD in FORM GSTR-6, containing the details of tax invoices on which input tax credit has been received and those issued to their branches. (Rule 65 of CGST Rules, 2017)

(v) Most of the details in GSTR 6 are auto-populated from the details approved in GSTR-6A generated from the details provided by the suppliers of an ISD in their GSTR 1.

(vi) The due date to file GSTR-6 is the 13th of succeeding month. GSTR 6 has to be filed by every ISD even if it is a ‘Nil’ return.

(vii) Failure to file GSTR-6 within the due date attracts late fees at the prescribed rates.

(viii) There is no provision for revising the GSTR 6 return. Any errors made in the return can be corrected while filing GSTR 6 of the following month.

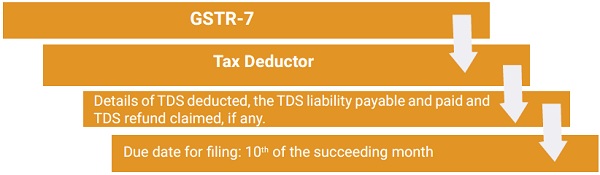

2.9. GSTR-7 – Return to be filed by persons required to deduct Tax at source (TDS) under GST:

(i) The provisions under GST provides for deduction of TDS (Tax Deducted at Source) at the time of making/crediting payment to suppliers towards the inward supplies received, at the prescribed rate, by the notified persons under GST.

(ii) Section 39(3) of the CGST Act, 2017 read with Rule 66 of the CGST Rules, 2017 stipulate that every registered taxpayer required to deduct tax at source (deductor) shall furnish a return in FORM GSTR-7, electronically through the common portal, for the month in which such deductions have been made, within ten days after the end of such month. (Section 39(3) of CGST Act, 2017) (Rule 66 of CGST Rules, 2017)

(iii) The GSTR-7 return contains details of TDS deducted, the TDS liability payable and paid and TDS refund claimed, if any.

(iv) The details furnished by the deductor in FORM GSTR-7 shall be made available electronically on the common portal to each of the deductee in FORM GSTR-7A (System generated TDS Certificate), for claiming the amount of tax deducted in his Electronic Cash Ledger.

(v) GSTR-7 is required to be filed every month within 10 days after the end of a particular month. Late fees is applicable for the delay in filing the return.

2.10 GSTR-8 – Monthly return for e-commerce operators, required to collect tax at source (TCS) under GST:

(i) Tax Collected at Source (TCS) is the tax collected by the e-commerce operator when a supplier supplies some goods or services through its portal and the payment for that supply is collected by the e-commerce operator.

(ii) On placing the order for a particular product/service, the actual supplier supplies the selected product/ service to the consumer but the price/consideration for the product/service is collected by the e-commerce operator from the consumer and passed on to the actual supplier after deducting the commission by the Operator. The e-commerce operator collects the tax at the prescribed rate from the supplier and deposited in the Government Account.

(iii) Section 39(1) of CGST Act, 2017 read with Rule 67 of the CGST Rules, 2017 stipulates that every e-commerce operator required to collect tax at source shall furnish a statement in FORM GSTR-8, electronically on the common portal, containing details of supplies effected, the amount of tax collected and tax paid. (Section 39(1) of CGST Act, 2017) (Rule 67 of CGST Rules, 2017)

(iv) The details furnished by the e-commerce operator in FORM GSTR-8 shall be made available electronically in Part C of FORM GSTR-2A, to each of the suppliers on the common portal, for claiming the amount of tax collected in his Electronic Cash Ledger.

(v) GSTR-8 is a monthly return and the due date for filing the return for a particular month is 10th of the following month. Delay in filing the return attracts Late Fees at the applicable rate, besides the interest payable towards late deposit of tax amount into the Government account.

(vi) GSTR-8 once filed, cannot be revised. Mistakes, if any, can be revised in the next month’s return.

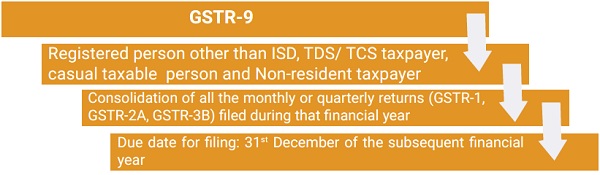

2.11 GSTR-9–Annual Return

(i) GSTR 9 is an annual return to be filed yearly by regular taxpayers registered under GST, including SEZ units and SEZ developers. The return consists of details of the outward supplies made, inward supplies received and their HSN codes, under different tax heads i.e. CGST, SGST & IGST, for the relevant financial year

(ii) Section 44 of the CGST Act, 2017 read with Rule 80 of the CGST Rules, 2017, outline the provisions for furnishing annual return. Section 44 of the CGST Act, 2017 stipulates the provisions of filing annual returns by every registered person, which may include a self-certified reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year with the audited annual financial statement for every financial year. Rule 80 of the CGST Rules, 2017 prescribes FORM GSTR-9 as the form of Annual Return for a registered Taxpayer. (Section 44 of CGST Act, 2017) (Rule 80 of CGST Rules, 2017)

(iii) Taxpayers who have opted for the Composition scheme, Casual taxable persons, Input Service Distributors, nonresident taxable persons and persons paying TDS under Section 51 of the CGST Act, 2017 and person collecting TCS under Section 52 ibid are not required to file the Annual Return. Further, to ease the compliance burden for small businesses, exemption is given from filing of GSTR-9 for businesses with turnover up to Rs 2 Crore from FY 17-18 onwards. (Section 51 and 52 of CGST Act, 2017)

(iv) Filing of annual returns is also not applicable in the case of any department of the Central Government, State Government or a local authority, whose books of account are subject to audit by the Comptroller and Auditor-General of India or an auditor appointed to audit the accounts of local authorities.

(v) The Annual Return needs to be filed if the taxpayer was registered for even a single day in a particular financial year.

(vi) If a Taxpayer has obtained multiple GST registrations, under the same PAN, whether in the same State or different States, he is required to file the Annual Return for each registration separately, where the GSTIN was registered as a normal taxpayer for some time during the financial year or for the whole of the financial year.

(vii) GSTR-9 is a consolidation of all the monthly/quarterly returns (GSTR-1, GSTR-2A, GSTR-3B) filed in the relevant year. This return is a complete document that summarises information on outward supplies made, inward supplies received, Input tax credits availed, and tax payments made during the financial year and helps in extensive reconciliation of data.

(viii) The common portal allows the Taxpayers to obtain a system-computed consolidated summary of GSTR-9, GSTR-1 and GSTR-3B. This summary is based on the monthly returns filed by the registered person and includes details like, the taxable value, liabilities paid through ITC and cash, ITC claims and reverse charge. GSTR-9 is auto-populated based on GSTR-1 & 3B and is for reference purpose only. It provides with an option to edit the auto-populated data with certain exceptions, so as to enable the Taxpayer to report the correct figures of liability in GSTR-9, which is matching with the accounts and other records.

(ix) The Taxpayer can report additional liability that was not reported in GSTR-1 or GSTR-3B and pay such liability through FORM DRC-03. However, the Taxpayer is not allowed to avail additional ITC through GSTR-9.

(x) The GSTR-9 return has to be filed electronically on the GST common portal by 31st December, following the end of the financial year. Delay in filing the Annual Return attracts Late Fees at the applicable rate.

(xi) No revision of the GSTR-9 return filed is permissible.

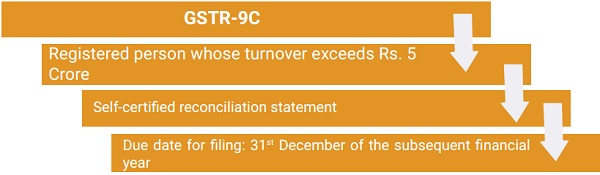

2.12 GSTR-9C – Self Certified Reconciliation Statement:

(i) GSTR-9C is a self-certified reconciliation statement between the books of account and the GSTR-9 return to be filed by every registered Taxpayer under GST, whose turnover during a financial year exceeds the prescribed limit of Rs. 5 Crore. Besides the category of Taxpayers exempt from filing GSTR-9 Annual Return, all foreign companies which are in the airline business and compliant with the relevant provisions and rules of the Companies Act 2013, are exempted from the GSTR-9C requirement.

(ii) Rule 80(3) read with Notification No 49/2018-CT, dated 13-9-2018, substituted vide Notification No 74/2018-Central Tax dated 31-12-2018, has notified the FORM GSTR-9C under Section 44 of CGST Act, 2017, for filing a self-certified reconciliation statement by a registered taxpayer filing Annual Return in FORM GSTR-9. For the financial year 2022-23, the Annual return forms have been notified vide Notification No. 38/2023-Central Tax dated 04.08.2023. (Rule 80(3) of CGST Rules, 2017) (Section 44 of CGST Act, 2017)

(iii) The certification by a Cost Accountant or Chartered Accountant has been done away vide Notification No. 56/2019- CT dated 14-11-2019 and self-certification has been introduced.

(iv) GSTR-9C is to be filed along with the GSTR-9 and audited Financial Statement, by 31st December following the end of the financial year. Delay in filing GSTR-9C attracts general penalty under Section 125 of the CGST Act, 2017. (Section 125 of CGST Act, 2017)

(v) GSTR-9C is a self-certified reconciliation statement that reconciles the value of supplies declared in the return furnished for the financial year with the audited Annual Financial Statement and GSTR-9 return. In GSTR-9C a registered Taxpayer is required to reconcile turnover, tax paid, and ITC availed as per books of accounts with GSTR-9 and provide reasons for the difference. Differential tax, if any, has to be paid vide FORM GST DRC-03.

(vi) GSTR-9C is to be filed for every GSTIN with one PAN, registered in different States or Union Territory.

(vii) GSTR-9C acts as a base for the Proper Officer to verify the correctness of the GST returns filed by the taxpayers after a self-certification.

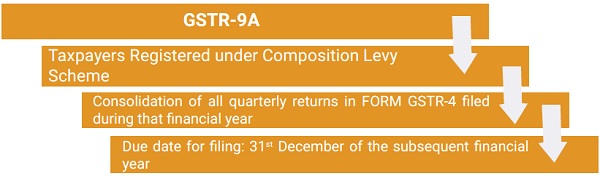

2.13. GSTR-9A – Annual Return for Taxpayers under Composition Scheme:

(i) GSTR-9A is the Annual Return and was filed once in a financial year by taxpayers opting for the Composition Scheme under Section 10 of CGST Act, 2017, for a specific fiscal year. (Section 10 of CGST Act, 2017)

(ii) GSTR-9A is consolidation of all the Quarterly returns filed in FORM GSTR-4 or CMP-08 upto FY 2018-19 and included all the data furnished within the quarterly returns filed by the Composition taxpayers during a financial year.

(iii) GSTR-9A form has been scrapped with effect from FY 2019-20 after being replaced by Annual Return in revised FORM GSTR-4.

(iv) Filing of GSTR-9A was made optional for the financial years 2017-18 and 2018-19.

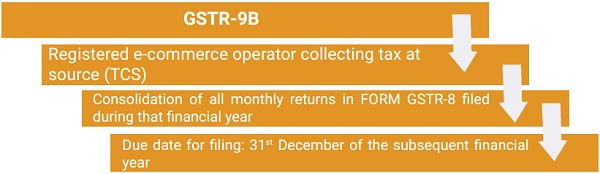

2.14. GSTR-9B – Annual Return to be filed by e-commerce operator collecting tax at source (TCS):

(i) GSTR-9B is an annual return to be filed by every E-commerce operator who is required to collect tax at source as per Section 52 (5) of the CGST Act, 2017. (Section 52(5) of CGST Act, 2017)

(ii) GSTR-9B contains the details of outward supplies of goods and services, returns if any, and the amount collected during the financial year. It summarises the details filed in the monthly return GSTR-8 to be filed by E-Commerce operators.

(iii) Section 44 of CGST Act, 2017 stipulates that every e-commerce operator required to collect tax at source shall furnish annual statement electronically through common portal, in FORM GSTR -9B, prescribed in Rule 80 of CGST Rules, 2017. (Section 44 of CGST Act, 2017) (Rule 80 of CGST Rules, 2017)

(iv) However, the format of FORM GSTR-9B is yet to be released.

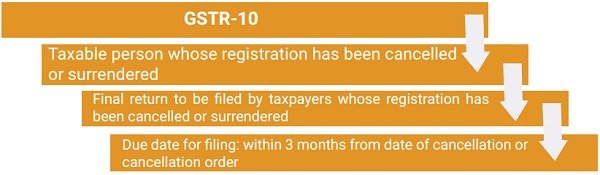

2.15. GSTR-10 – Return to be filed by a taxpayer whose registration is cancelled or surrendered:

(i) GSTR-10 is the Final Return to be filed by the registered taxpayers who have opted for the cancellation or surrender of the GST registration.

(ii) Section 45 of CGST Act, 2017 states that every registered person who is required to furnish a return under Section 39(1) and whose registration has been cancelled, shall furnish a final return in FORM GSTR-10 prescribed in Rule 81 of the CGST Rules, 2017, within three months of the date of cancellation or date of order of cancellation, whichever is later. (Section 45 of CGST Act, 2017) (Rule 81 of CGST Rules, 2017) (Section 39(1) of CGST Act, 2017)

(iii) GSTR-10 is a statement of stocks held by the taxpayer, whose registration has been cancelled or ordered to be cancelled, on day immediately preceding the date from which cancellation is made effective.

(iv) In case if invoices are not present for the declared stock of inputs and inputs contained in semi-finished or finished goods, then the amount must be estimated differently and must be certified by a practising Chartered Accountant or Cost Accountant and uploaded along with GSTR-10.

(v) If GSTR-10 is not filed within the due date, a notice will be sent to the taxpayer. If the person still fails to file the Final Return then the proper officer will pass the final order for the cancellation and the amount of tax payable along with interest or penalty.

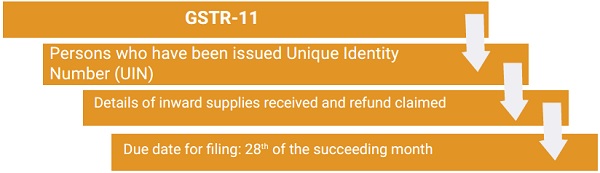

2.16. GSTR-11 – Return for persons having Unique Identity Number (UIN):

(i) Unique Identity Number (UIN) is a special classification made for foreign diplomatic missions and embassies like, specialized agency of the United Nations Organization, Multilateral Financial Institution and Organization notified under the United Nations (Privileges and Immunities) Act, 1947, Consulate or Embassy of foreign countries, who are not liable to taxes in Indian territory.

(ii) The purpose of issuing UIN is to claim refund of the tax collected from the organisation/person holding UIN.

(iii) Rule 82 of CGST Rules, 2017 stipulates that every person holding a Unique Identity Number and claiming refund of the taxes paid on his taxable inward supplies, shall furnish the details of such supplies, electronically on common portal, in FORM GSTR-11, along with application for the refund claim in FORM GST RFD-10. The Rule also provides that the person holding Unique Identity Number for purposes other than refund of the taxes paid, shall furnish the details of inward supplies of taxable goods or services or both in FORM GSTR-11.(Rule 82 of CGST Rules, 2017)

(iv) Deputy/Assistant Commissioner of Central Tax has been designated as ‘proper officer’ for the purpose of specifying the details of inward supplies (Circular No. 3/3/2017-GST dated 05.07.2017).

(v) GSTR-11 is required to be filed by 28th of the month following the month in which inward supply is received by the UIN holder. Thus GSTR-11 filing is not a monthly process, but a case-to-case basis filing, depending on supplies received by the UIN holders.

(vi) The GSTR-11 return is auto populated based on GSTR-1/5 filed by the suppliers of goods and services to the UIN

3. NON-FILERS OF RETURNS

(i) Return is an important aspect of GST and is the base for the authority to keep track over the tax paid and input tax credit availed. Tax is said to have been paid only when the return is filed after making debits in the Electronic Credit Ledger and/or Electronic Cash Ledger, as the case may be.

(ii) A Non-filer is a person who is registered and is liable to file the GST return or statement periodically but has failed to do so within the due dates prescribed. There are chances that the non-filer has some liability of tax to pay, which he has not paid.

(iii) Section 46 of the CGST Act, 2017 read with Rule 68 of the CGST Rules, 2017 stipulates issuance of a notice in FORM GSTR-3A to a registered taxpayer, who fails to furnish return under Section 39 or Section 44 or Section 45 of CGST Act, 2017 (GSTR-3B, GSTR-4, GSTR-5, GSTR-6, GSTR-7, GSTR-8, GSTR-9 and GSTR-10) asking him to furnish such return within fifteen days. (Section 46 of CGST Act, 2017) (Rule 68 of CGST Rules, 2017)

(iv) If the registered person fails to furnish return even after notice in FORM GSTR-3A is issued then for such cases, Section 62 of CGST Act, 2017 provides for assessment of non-filers of return on best judgement basis. (Section 62 of CGST Act)

(v) CBIC has issued Circular No. 129/48/2019 dated 24.12.2019 laying down the guidelines to deal with the cases of non-filers and for the purpose of maintaining uniformity. The said Circular prescribes the following guidelines on the issue of non-filers-

(i) A system generated message would be sent to all the registered taxpayers 3 days before the due date to remind them about filing of the return for the tax period by the due date.

(ii) Once the due date for furnishing the return under Section 39 is over, a system generated mail / message would be sent to the authorized signatory as well as the proprietor/partner/director/karta, etc. of all the defaulters immediately after the due date to the effect that he has not furnished his return for the said tax period.

(iii) Five days after the due date of furnishing the return, a notice in FORM GSTR-3A in terms of Section 46 of the CGST Act, 2017 read with Rule 68 of the CGST Rules, 2017, shall be issued electronically through common portal to such registered taxpayer who fails to furnish return under section 39, asking him to furnish such return within fifteen days.

(iv) In case the return is still not filed by the defaulter within 15 days of the notice, the proper officer may proceed to assess the tax liability of the said person under Section 62 of the CGST Act, 2017, to the best of his judgement taking into account all the relevant material which is available or which he has gathered and will issue order under Rule 100 of the CGST Rules, 2017 in FORM GST ASMT-13. (Section 62 of CGST Act) and (Rule 100 of the CGST Rules, 2017)

(v) The proper officer has to upload the summary thereof in FORM GST DRC-07.

(vi) For the purpose of assessment of tax liability, the proper officer may take into account the details of outward supplies available in the statement furnished under Section 37, i.e. FORM GSTR-1, details of supplies auto populated in FORM GSTR-2A, information available from e-way bills, or any other information available from any other source, including from inspection under Section 71. (Section 71 of CGST Act) (Section 37 of CGST Act)

(vii) In case the defaulter furnishes a valid return within thirty days of the service of assessment order in FORM GST ASMT-13, the said assessment order shall be deemed to have been withdrawn in terms of provision of sub-section (2) of Section 62 of the CGST Act, 2017. However, if the return remains unfurnished within the statutory period of 30 days from issuance of order in FORM GST ASMT-13, then proper officer may initiate proceedings under Section 78 and recovery under Section 79 of the CGST Act, 2017. (Section 62 of CGST Act) (Section 78 of CGST Act) (Section 79 of CGST Act)

(viii) In appropriate cases, based on the facts of the case, the Commissioner may resort to provisional attachment to protect revenue under Section 83 of the CGST Act, 2017 before issuance of FORM GST ASMT-13. (Section 83 of CGST Act)

(ix) Further, the proper officer would initiate action under Section 29(2) of the CGST Act, 2017 for cancellation of registration in cases where the return has not been furnished for the period specified in Section 29. (Section 29 of CGST Act)

(vi) FORM GSTR-3A contains notice for best judgment assessment. Hence, no separate notice is required to be issued for best judgment assessment under Section 62 of CGST Act, 2017. In case of failure to file return within 15 days of issuance of FORM GSTR-3A, the best judgment assessment in FORM ASMT-13 can be issued without any further communication.

(vii) The proper officer is required to upload the summary in FORM GST DRC-07.

4. DUE DATE FOR FILING THE RETURNS

(i) Every registered Taxpayer who is required to furnish return, shall discharge his liability towards tax, interest, penalty, fees or any other amount payable under the CGST Act, 2017, by debiting the Electronic Cash Ledger or Electronic Credit Ledger and include the details in the respective return to be filed. Since the details of tax paid have to be included in the return, the same cannot be filed unless the taxes are paid.

(ii) The provisions of CGST Act, 2017 and the rules made thereunder, as applicable to the respective returns, mandate filing of the GST Returns within the prescribed due dates. Failure to file the returns within the due date will lead to recovery of Late Fees, imposition of penalty, as applicable, and recovery of interest on the delayed payment of tax. Therefore, filing of returns on or before the due date is very essential.

(iii) The types of GST return that a supplier of goods and services or both is required to file is based on the type of taxpayer registered. These types include regular taxpayer, composition taxable persons, e-commerce operators, TDS deductor, non-resident taxpayer, Input Service Distributor (ISD), casual taxable persons, etc.

(iv) The following Table illustrates the types of returns to be filed and its due date:

| From of Return | Applicable provision | Description | Due date |

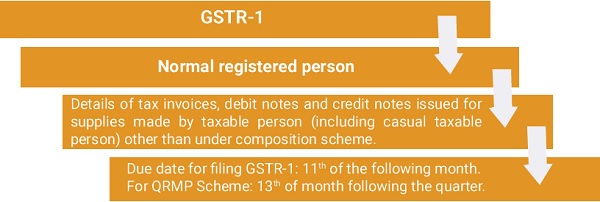

| GSTR-1 | Section 37(1) of CGST Act, 2017 and Rule 59 of the CGST Rules, 2017 |

Details of tax invoices, debit notes and credit notes issued for supplies made by taxable person (including casual tax-able person) other than under composition scheme. |

Monthly – 11th of the following month. For those who opt to file GSTR-3B return on quarterly basis under QRMP Scheme – 13th of month following the quarter. Nil return is required even if there are no transactions in a month/quarter. |

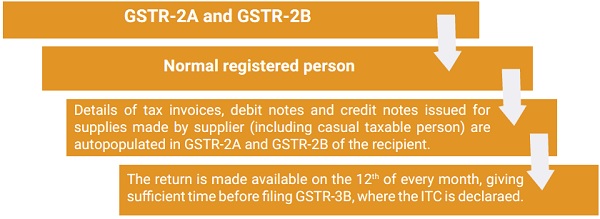

| GSTR-2A & GSTR- 2B | Rule 60 of CGST Rules, 2017 |

These are not returns to be filed but are auto-populated. Details of tax invoices, debit notes and credit notes issued for supplies made by supplier (including casual taxable person) appear in GSTR-2A and GSTR-2B of recipient. | Invoices uploaded by supplier get autopopulated in form GSTR-2A of recipient within 2 days but they get populated in GSTR-2B only after GSTR-1 return is filed. |

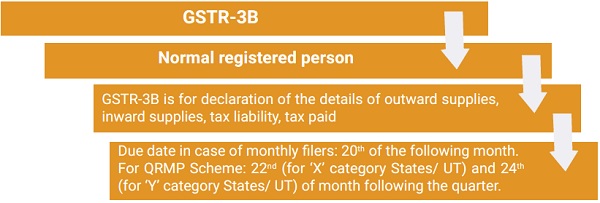

| GSTR-3B | Section 39(1) of CGST Act, 2017 and Rule61 of CGST Rules, 2017 |

To be filed by Taxable person (including casual taxable person), other than those under composition scheme. Return consists of details of outward supplies, inward supplies, value of supplies, ITC availed, tax payable, tax paid, etc. | Monthly – 20th of the following month. Quarterly under QRMP Scheme – 22nd or 24th of the following month after end of Quarter, depending upon the State in which the taxpayer is registered. |

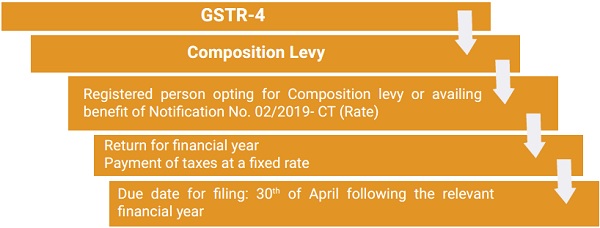

| GSTR-4 | Section 39(2) of CGST Act, 2017 and Rule 62 of CGST Rules, 2017 | Taxable person under Composition scheme. Return consists of details of outward supplies, inward supplies, value of supplies, tax payable, tax paid, etc. | Yearly – 30th of the month following the end of the year. |

| GSTR-5 | Section 39(5) of CGST Act, 2017, and Rule 63 of CGST Rule, 2017 |

Return by Non-resident taxable person, consisting details of outward supplies, value, tax paid, etc. | Monthly, within 13 days from end of taxable period or 07 days after end of validity period of registration. |

| GSTR-5A | Section 39(1) of CGST Act, 2017 and Rule64 of CGST Rules, 2017 |

Taxable per son supplying OIDARservices. consisting details of outward supplies, value, tax paid, etc. | Monthly, within 20 days from end of the month. |

| GSTR-6 | Section 39(4) of CGST Act, 2017 and Rule65 of CGST Rules, 2017 |

Input Service Distributor, consisting details of ITC availed, ITC distributed, etc. | Monthly, within 13days from end of the month. |

| GSTR-7 | Section 39(3) of CGST Act, 2017 and Rule66 of CGST Rules, 2017 |

Return by persons required to deduct Tax at Source (TDS) under Section 51, consisting details of TDS. | Monthly, within 10 days from end of the month. |

| GSTR-8 | Section 39(1) of CGST Act, 2017 and Rule67 of CGST Rules, 2017 |

Return by e-commerce operator, consisting details of tax collected at source (TCS) under Section 52 | Monthly, within 10 days from end of the month. |

| GSTR-9 | Section 44

of CGST Act, 2017 and Rule 80 of CGST Rules, 2017 |

Annual Return for normal taxpayer with turnover more than Rs. 2 Crore. | Yearly, by 31st December after the end of the financial year. |

| GSTR-9A | Annual Return by taxable person under Composition scheme. | Yearly, by 31st December after the end of the financial year. | |

| GSTR-9B | Section 44 of CGST Act, 2017 and Rule 80 of CGST Rules, 2017 | Annual Return by e-commerce operator who are required to collect TCS under Section 52 | Form of return is not yet notified. |

| GSTR-9C | Rule 80(3) of CGST Rules, 2017. |

Self certified reconciliation statement by registered taxpayers whose aggregate turnover during financial year exceeds Rs. five Crore |

Yearly, to be filed along with Annual Return in form GSTR-9 by registered persons whose aggregate turnover during financial year exceeds Rs five Crore. |

| GSTR-10 | Section 45 of CGST Act, 2017 and Rule 81 of CGST Rules, 2017 |

Final Return after cancellation of GST registration | Once, within three months from the date of cancellation. |

| GSTR-11 | Rule 82 of CGST Rules, 2017 |

Inward supply details by per-sons having UIN | The return is auto populated on quarterly basis based on GSTR-1 /5 filed by the input or input services suppliers to UIN Agencies. |

5. INTEREST AND LATE FEES DUE TO DELAY OR NON-FILING OF RETURNS

(i) Filing of returns is mandatory under GST. Even if there is no transaction, a ‘Nil’ return must be filed.

(ii) Filing returns for previous month/ quarter is a pre-requisite for filing returns for current month/ quarter.

(iii) The late fee in respect of GSTR-1 is populated in the liability ledger of GSTR-3B filed immediately after a delay.

(iv) Interest @ 18% per annum has to be calculated by the taxpayer on the amount of outstanding tax to be paid. It shall be calculated on the net tax liability identified in the ledger at the time of payment. The time period will be from the next day of filing due date till the actual date of payment.

(v) As per the CGST Act, 2017, the late fee is Rs.100/- per day per Act, i.e., Rs.100/- under CGST & Rs.100/- under SGST (Total Rs. 200/- per day), subject to maximum of Rs. 5000/- per Act (Rs. 5000/- CGST + Rs. 5000/- SGST) per Return.

(vi) There is no late fee separately prescribed under the IGST Act, 2017.

(vii) For GSTR-9/9C, the maximum late fee per Act is capped at 0.25% of the turnover in the State or Union Territory.

6. SCRUTINY OF RETURNS BY PROPER OFFICER

(I) The provisions for scrutiny of GST returns are specified under Section 61 of the Central Goods and Service Tax Act, 2017 and Rule 99 of the CGST Rules, 2017. (Section 61 of CGST Act, 2017) (Rule 99 of CGST Rules, 2017)

(II) A Scrutiny Module for online scrutiny of returns is available for scrutiny of returns filed in FY 2019-20 onwards.

(III) The Superintendent of Central Tax is assigned as a proper officer for performing functions, as stated under Section 61 of the CGST Act, 2017.

(IV) Central Board of Indirect Taxes and Customs (CBIC) has issued SOP (Standard Operating Procedures) to ensure uniformity in selecting returns for scrutiny in 2022 for FY 2017-18 and FY 2018-19 vide Instruction No. 02/2022-GST dated 22.03.2022 and in 2023 for FY 2019-20 onwards vide Instruction No. 02/2023-GST dated 26.05.2023.

(V) As per Section 61 of the CGST Act, 2017, the proper officer, i.e the Superintendent shall scrutinise the return filed by the registered taxpayer for its correctness of input tax credit availment and discharge of tax liability and notify the discrepancies identified to the taxpayer. If the proper officer is satisfied with the taxpayer’s explanation on discrepancies pointed out, no further action will be taken.

(VI) The Directorate General of Analytics and Risk Management (DGARM) selects the GSTIN whose returns are to be scrutinised and communicate the same to the field formations through the DDM portal. The DGARM will make the list of GSTINs available through the DG systems on the scrutiny dashboard of the officers on the ACES-GST

(VII) The list of parameters for selection of GST returns for scrutiny are as follows-

(i) The tax liability in Tables 3.1(a) and (b) of GSTR-3B must match with tax liability in Tables 4, 5, 6. 7A(1), 7B(1), 11A and 11B of GSTR-1 [Net of amendments in Tables 9, 10, and 11(II)].

(ii) Advances adjusted are accurately reflected by reporting the same in Table 11B and Tables 4, 5, 6 and 7 of GSTR-1.

(iii) Reporting and paying in cash the exact tax liability under the reverse charge mechanism using Tables 3.1(d) for tax liability and 4(A)(2) and 4(A)(3) for ITC claimed on it in GSTR-3B. The value in GSTR-3B should be more than the eligible ITC in Tables 3, 4, 5 and 6 of GSTR-2A.

(iv) ITC claimed in Table 4(A)(4) of GSTR-3B should match with amounts marked as eligible ITC in Table 7 of GSTR-2A (Net of amendments in Table 8).

(v) Sales subjected to TCS or TDS under GST in GSTR-3B should match the TDS and TCS credit reflected under Column 6 of Table 9 of the GSTR-2A.

(vi) In Table 3.1(a) and (b) of the GSTR-3B the tax liability should match with the corresponding e-way bills.

(vii) ITC is ineligible for claims for the period after the effective date of cancellation of the supplier’s GST registrations, especially in case of retrospective cancellation of GST registrations.

(viii) The GSTR-3B filing status of respective vendors must not be ‘No’ while claiming ITC of such invoice or debit note in the GST returns, despite it appearing in the GSTR-2A.

(ix) No ITC should be claimed if the relevant period’s GSTR-3B is filed after the last date allowed under Section 16(4) of the CGST Act, 2017, i.e. 30th November of the year following the financial year in which such invoice/debit note is raised or date of filing annual returns, whichever is earlier. (Section 16(4) of CGST Act)

(x) ITC on import of goods in Table 4(A)(1) of GSTR-3B should match with amounts in Tables 10 and 11 of GSTR-2A and data on ICEGATE.

(xii) Adherence to Rule 42 and 43 of CGST Rules, 2017 for accurate reversals of ITC in Table 4(B) of GSTR-3B. (Rules 42 and 43 of CGST Rules, 2017) Computation and payment of late fee/interest as per Sections 47 and 50 of the CGST Act, 2017, wherever return filing/tax payment is delayed. (Sections 47 and 50 of CGST Act, 2017)

(VIII) A month-wise schedule shall be prepared by the proper officer for scrutiny regarding all GSTINs selected. The priority may be based on the revenue implication involved. GSTINs with a higher revenue implication shall be prioritised.

(IX) The proper officer shall scrutinise the return for its correctness based on the information available on the system in various forms and statements filed by the registered taxpayer and other sources, such as, DGARM, ADVAIT, E-way Bill portal, etc.

(X) The proper officer is expected to depend on the information available to the Department. He should have a minimal interface with the taxpayer and normally should not ask for documents from the taxpayer before the issuance of Form GST ASMT-10.

(xi) As per Rule 99 of the CGST Rules, 2017, when a return is selected for scrutiny, the proper officer shall scrutinise the same as per Section 61 based on information available to him.

(XII) Relevant factors for Scrutiny of Returns:

While scrutinising the returns, certain vital factors need proper verification to ascertain whether the tax liability has been discharged properly and whether the other compliances like availment of ITC, payment of interest, Late fee, etc. is in order. Some of such factors that need to be considered by the Officer while scrutinising the returns, are as under-

(i) Tax liability on account of “Outward taxable supplies (other than zero rated, nil rated and exempted)” and “Outward taxable supplies (zero rated)” declared in FORM GSTR-3B may be verified with corresponding tax liability in respect of outward taxable supplies declared in FORM GSTR-1. If the tax liability in respect of supplies declared in FORM GSTR-1 exceeds the liability declared in FORM GSTR-3B, it may indicate short payment of tax. All amendments to invoices need to be checked to confirm whether they are appropriately reflected in GSTR-1 and GSTR-3B. Also, it has to be verified whether the liability reported in GSTR-1 matches the liability reported in the GSTR-9 return.

(ii) Tax liability on account of “Inward supplies liable to reverse charge” declared in FORM GSTR-3B may be verified with the ITC availed in respect of inward supplies attracting reverse charge, available in FORM GSTR-2A. In respect of inward supplies attracting reverse charge received from a registered person, the details of corresponding invoices and debit/credit notes are available in FORM GSTR-2A. However, the details of such inward supplies from unregistered persons are not available in FORM GSTR-2A, as only registered persons furnish FORM GSTR-1. Also, details of ITC on account of import of services are not available in FORM GSTR-2A. As such, the reverse charge supplies declared in FORM GSTR-3B cannot be less than the inward supplies attracting reverse charge as available in FORM GSTR-2A.

(iii) ITC availed in respect of “Inward supplies from ISD” in FORM GSTR-3B should be verified with FORM GSTR2A. Also, the ITC availed in respect of “All other ITC” in FORM GSTR-3B should be verified with FORM GSTR-2A.

(iv) The taxable value declared on account of “Outward taxable supplies (other than zero rated, nil rated and exempted)” should be verified in FORM GSTR-3B to ascertain that it is not less than the net amount liable for TCS and TDS credit as per FORM GSTR-2A. The details of such TDS and TCS are furnished by the deductors and operators in their FORM GSTR-7 and FORM GSTR-8, respectively, and made available to the registered person in FORM GSTR-2A. Besides such supplies, the registered person may have other supplies also. Liability on account of outward supplies in FORM GSTR-3B should also be verified with the Tax liability as declared in e-way bills.

(v) In case of retrospective cancellation of registration of a supplier, the recipient is not entitled to claim ITC in respect of invoices or debit notes issued after the effective date of cancellation of the registration. The effective date of cancellation of registrations of the suppliers is available in FORM GSTR-2A. It may be verified whether the registered person has availed ITC in respect of such invoices or debit notes issued by the suppliers after the effective date of cancellation of their registrations.

(vi) FORM GSTR-2A of the registered person contains the details of “GSTR-3B filing status” of the supplier in respect of each invoice / debit note received by the registered person. Where the said status is “No”, it indicates the supplier has furnished invoice details in his FORM GSTR-1, but has not furnished the return in FORM GSTR-3B for the corresponding tax period. The availment of ITC in respect of such invoices / debit notes should be checked and appropriate action as per the law should be taken.

(vii) If GSTR-3B of a tax period is filed after the last date of availment of ITC in respect of any invoice / debit note then in such cases, no ITC shall be availed in the return, as Section 16(4) of CGST Act, 2017 provides for availment of ITC only till the 30th day of November following the end of financial year to which such invoice or debit note pertains or furnishing of the relevant annual return, whichever is earlier. If any return in FORM GSTR-3B is furnished after such time by the registered person, any ITC availed therein is inadmissible.

(viii) ITC availed in respect of “Import of goods” in FORM GSTR-3B may be verified with corresponding details in FORM GSTR-2A. Also, the details of such imports be cross-verified from ICEGATE portal.

(ix) Rule 42 of the CGST Rules, 2017 provides for manner of determination of input tax credit in respect of inputs or input services and reversal thereof. Rule 43 provides for manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases. It is necessary to verify whether requisite reversals have actually been made by the registered person.

(x) In case of delay in payment of tax, it has to be verified whether interest payable as per the provisions of Section 50 of the CGST Act, 2017 has actually been paid by the registered person.

(xi) In case of delay in filing of returns / statements, it has to be verified whether late fee payable as per the provisions of Section 47 of the CGST Act, 2017 has actually been paid by the registered person.

(XIII) The proper officer shall issue a notice to the taxpayer indicating all the discrepancies noticed and seek his explanation thereon in FORM GST ASMT-10 within 30 days of notice. He shall quantify the tax, interest, and other such sums payable regarding the discrepancies noticed. If the registered taxpayer has already made the additional tax payment through FORM GST DRC-03, then the same should be considered while communicating discrepancies to the taxpayer in FORM GST ASMT-10.

(XIV If the registered taxpayer accepts the discrepancy, he has to make the payment of tax through FORM GST DRC-03, if he does not accept the discrepancy, he has to submit his explanation in respect of the discrepancy vide FORM GST ASMT-11.

(XV) If the response is found to be satisfactory, then the proper officer may inform the taxpayer vide FORM GST ASMT-12.

(XVI) If no explanation is provided by the taxpayer or he fails to pay the tax within 30 days of intimation, the proper officer may proceed to determine the tax and other dues as per Sections 73/Section 74 of CGST Act, 2017, as the case may be. The officer may refer the matter to the Jurisdictional Principal Commissioner or Commissioner, if he believes that an audit or investigation is required to determine the correct amount of liability. The Principal Commissioner or Commissioner can decide the appropriate action, like audit by the tax officers under Section 65, special audit by a Chartered Accountant or a Cost Accountant nominated by Commissioner under Section 66 or inspection, search and seizure in terms of Section 67 and to be accordingly referred to the Audit Commissionerate or Anti Evasion Wing. (Section 65, 66, 67, 73 & 74 of CGST Act, 2017)

(XVII) For each selected GSTIN, the proper officer must scrutinise all the returns of the corresponding financial year and issue a single notice vide FORM GST ASMT-10.

(XVIII) The scrutiny of returns shall be completed in a specified period to safeguard revenue. Below are some of the timelines:

| Sr. No. Process Time Line | ||

| 1 | Communicating the list of GSTINs selected for scrutiny by the DGARM to the nodal officer | From time to time |

| 2 | Communicating the list of GSTINs selected for scrutiny by the nodal officer to the proper officer | Within 3 working days from the date of receipt of the list of GSTINs from the DGARM (not applicable for online scrutiny from FY 2019-20 onwards) |

| 3 | Finalisation of scrutiny schedule with the Assistant/ Deputy Commissioner | Within 7 working days of receipt of the list of GSTINs from the nodal officer (from 19-20 scrutiny onwards, it is available online on ACES portal) |

| 4 | Sharing the scrutiny schedule with the DGGST | Within 30 days of receipt of the list of GSTINs from DGARM |

| 5 | Issue of notice in Form GST ASMT-10 | Within a month as specified in the scrutiny schedule |

| 6 | Issue of response in GST ASMT-11 | Within 30 days of receipt of notice under GST ASMT-10 |

| 7 | Issue of order in Form GST ASMT-12 | Within 30 days of receipt of response in Form GST ASMT-11 |

| 8 | Initiating action for determining tax under section 73 and section 74 | If the reply is received: Within 30 days from receipt of reply in GST ASMT-11.

If the reply is not received: Within 15 days of completion of 30 days of service of notice in GST ASMT-10 or further period as may be notified by the proper officer. |

| 9 | Reference to Commissioner for taking appropriate action under section 65, section 66 or section 67 | If the reply is received: Within 30 days from receipt of reply in GST ASMT-11. If the reply is not received: Within 45 days of service of notice in GST ASMT-10. |

(XIX) A Scrutiny Register shall be maintained by the proper officer, i.e. the Superintendent for all the GSTINs allotted for scrutiny in the format prescribed in Instruction No. 02/2022-GST, dated 22.03.2022, issued in GST Policy Wing of CBIC. For scrutiny from the FY 2019-20 onwards, MIS report of scrutiny register along with the ‘Monthly Scrutiny Progress Report’ is available on the dashboard of the officer over the ACES portal.

(XX) The progress of the scrutiny shall be monitored by the jurisdictional Principal Commissioner every month. The proper officer shall prepare a scrutiny progress report at the end of every month in the prescribed format in Instruction No. 02/2022-GST, dated 22.03.2022, issued in GST Policy Wing of CBIC. This report shall be forwarded to the Director-General of Goods and Service Tax by the Principal Chief Commissioner of the concerned zone by the 10th of the succeeding month. The DGGST shall submit this report to the Board by the 20th of the corresponding month.

(XXI) Instruction No. 02/2022-GST issued by GST Policy Wing of CBIC on 22.03.2022 shall be followed for the scrutiny of returns for the financial years 2017-18 and 2018-19 whereas the Instruction No. 02/2023-GST issued on 26.05.2023 will be followed along with the previous instruction for FY 2019-20 onwards.

7. TASKS OF RANGE OFFICERS:

The Range Officer is required to undertake the following functions with regard to scrutiny of returns:

(i) Superintendent is the proper officer for scrutiny of Returns to verify the correctness of returns and issue Notice of discrepancies. He shall verify the correctness of input tax credit availment, tax liability payable by the taxpayer and the payment of tax in the manner prescribed.

(ii) Superintendent shall take corrective measures in terms of Section 65 / 66 / 67 and 73/74 of CGST Act, 2017.

(iii) Superintendent shall issue Notice to return defaulters under Section 46 of the CGST Act, 2017 read with Rule 68 of CGST Rules, 2017.

(vi) Superintendent shall follow up with non-filers for filing pending periodic returns through various means, including emails. In deserving cases, he shall issue GSTR-3A as per Rule 68 of the CGST Rules, 2017.

(v) The records of the scrutiny of returns, completed and pending, along with all relevant details are to be maintained by Range Officer.

(vi) The Inspector in Range has to assist the Superintendent in performing the task of scrutiny of returns.

8. SOPS ISSUED IN RESPECT OF RETURNS

(i) Standard Operating Procedure (SOP) is issued by CBIC vide Instruction No. 02/2022-GST, dated 22.03.2022 for Scrutiny of returns for Financial Year 2017-18 and 2018-19.

(ii) Standard Operating Procedure (SOP) is issued by CBIC vide Instruction No. 02/2022-GSTissued on 26.05.2023 for Scrutiny of Returns for Financial Year 2019-20 onwards.

(iii) Standard Operating Procedure issued by CBIC vide Circular No. 129/48/2019 dated 24.12.2019 is to be followed in case of non-filers of returns.

*****

Source: Handbook of GST Law and Procedures for Departmental Officers issued by Ministry of Finance