Introduction:-

Charging section 9 of the CGST Act 2017 deal with collection of CGST.

Section 9 of GST – Levy and collection

Sec 9(1) of CGST Act : Subject to the provisions of sub-section (2), there shall be levied a tax called the central goods and services tax on all Intra-State supplies of goods or services or both, except on the supply of alcoholic liquor for human consumption, on the value determined under section 15 and at such rates, not exceeding twenty per cent., as may be notified by the Government on the recommendations of the Council and collected in such manner as may be prescribed and shall be paid by the taxable person.

The central tax on the supply of petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas and aviation turbine fuel shall be levied with effect from such date as may be notified by the Government on the recommendations of the Council.( Sec 9(2) of CGST Act 2017 )

There are two types of Charges under GST.

Forward Charge : Section 9(1) deals with forward charge.

Reverse Charge : Section 9(3) and 9(4) deals with reverse charge.

Forward Charge : Forward charge or direct charge is the mechanism where the supplier of goods or services is liable to pay tax.

For example: – If a chartered accountant provided a service to his client, the GST will be payable by the chartered accountant.

If a car manufacturing company sold some auto parts to a trader and collected tax from the trader, the manufacturing company remits the tax to the government.

Note: Under the current tax system, most transactions are covered under the forward charge Mechanism.

Exclusion from GST:-

CGST on supply of following items has not been levied immediately. It shall be levied with effect from such date as may be notified by the Government on the recommendation of the GST council:

(a) Petroleum crude

(b) High speed diesel

(c) Motor spirit (commonly known as petrol)

(d) Natural gas

(e) Aviation turbine fuel.

Rates of CGST under CGST Act 2017.:Rate of CGST are 0%, 0.125%, 1.5%, 2.5%, 6%, 9%, 14%. Maximum rate of CGST will be 20%.

Reverse Charge : Reverse charge” means the liability to pay tax by the person receiving goods or services or both instead of the supplier of such goods and/or services under section 9(3) or 9(4) of CGST Act or section 5(3) or 5(4) of IGST Act – section 2(98) of CGST Act

There are two provisions under which GST is payable under reverse charge

Section 9(3) of CGST Act and section 5(3) of IGST Act state that Government can specify categories of supply of goods or services or both, the tax on which is payable on reverse charge basis

Government has notified the following categories of services wherein the tax shall be paid on reverse charge basis by the recipient of services:

(a) Supply of Services by a goods transport agency (GTA)

(b) Services supplied by an individual advocate including a senior advocate.

(c) Services supplied by an arbitral tribunal.

(d) Services provided by the way of sponsorship.

(e) Services provided by Central Government, State government, Union territory or local authority to a business entity.

(f) Services provided by the director of a company or body corporate to the said company or body corporate.

(g) Services provided by the insurance agent.

(h) Services provided by the recovery agent.

(i) Services provided by the author, music composer, photographer, artist.

(j) Services provided by any person by way of transfer of development rights or Floor Space Index (FSI) (including additional FSI) for construction of a project by a promoter [inserted w.e.f. 1-4-2019].

(k) Services provided by way of long term lease of land (30 years or more) by any person against consideration in the form of upfront amount (called as premium, salami, cost, price, development charges or by any other name) and/or periodic rent for construction of a project by a promoter [inserted w.e.f. 1-4-2019].

(l) Services provided by the members of Overseeing Committee to Reserve Bank of India

(m) Services provided by individual Direct Selling Agent (DSAs) other than a body corporate, partnership or LLP to bank or NBFC

(n) Services provided by business facilitator (BF) to a banking company.

(o) Services provided by an agent of business correspondent (BC) to business correspondent

(p) Services provided by way of supply of security personnel to a registered person,

Some goods are also covered under reverse charge.

Second scenario is covered by section 9 (4) of the CGST Act where taxable supplies by any unregistered person to a registered person.

As per sec 9(4) of CGST Act – In case of receipt of supply of goods or services or both by a registered person from unregistered supplier, IGST/CGST will be payable by the recipient, in respect of specified categories of goods or services as may be notified by Government on recommendation of GST Council, and all provisions of CGST Act and IGST Act shall apply to such recipient as if he is the person liable for paying the tax in relation to such supply of goods or services or both. – (Amendment Act 2018 – w.e.f. 01.02.2019)

The Government vide Notification No. 24/2019-Central Tax (Rate) dated 30th September, 2019 specified that GST under RCM on purchase of cement by a promoter from an unregistered supplier

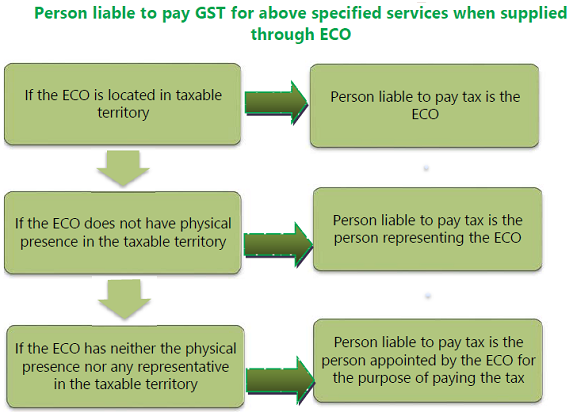

Further . the Government may, on the recommendations of the Council, by notification, specify categories of services the tax on Intra-State supplies of which shall be paid by the electronic commerce operator if such services are supplied through it, and all the provisions of this Act shall apply to such electronic commerce operator as if he is the supplier liable for paying the tax in relation to the supply of such services. (Sec 9(5) of CGST Act 2017)

Provided that where an electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic commerce operator for any purpose in the taxable territory shall be liable to pay tax:

Provided further that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

In case of supply of specified services (like taxi and hotel booking), the e-commerce operator himself will be liable to pay entire IGST/CGST/SGST on such services- (section 9(5) of CGST Act.)

Applicability of the provisions of sections 9(5) – As per the notification No. 17/2017-CT (Tax) dated 28-6-2017 e-commerce operator will be liable to pay entire GST on following activities :-

Service of transportation of passengers – Service by way of transportation of passengers by radio-taxi, motorcar, maxicab and motor cycle. Examples are Uber , Ola etc . The GST rate is 5% and entire tax is payable by e-commerce operator .

Radio taxi means a taxi (including a radio cab), by whatever name called, which is in two-way radio communication with a control office and is enabled for tracking using Global Positioning System (GPS) or General Packet Radio Service (GPRS).

Service of providing accommodation in hotels, inn, campsites – Service by way of providing accommodation in hotels, inn, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes.However, if the person supplying such service is registered under CGST and SGST Act, the e-commerce operator will not be liable to pay GST

Homestay service or guest house service provided through e-commerce operator – If Homestay or guest house service provided through e-commerce operator, the supplier of service will not be liable to pay tax if his turnover is less that Rs 20 lakhs .In that case, the supplier is not required to register and liability to pay tax will be on e-commerce operator ( CBI&C circular No. 27-1-2018 dated 4-1-2018.)

House-keeping like plumbing, carpentering etc . – Services by way of house-keeping, such as plumbing, carpentering etc., except where the aggregate turnover of the person supplying such service through electronic commerce operator is less than Rs 20 Lakhs ,he is not liable to get registered under GST . In that case , the e-commerce operator will be liable to pay

The tax rate on house-keeping services like plumbing, carpentering etc. provided through e-commerce operator is 5% w.e.f. 25-1-2018, subject to non-availment of input tax credit – (Notification No. 11/2017-CT (Rate) dated 28-6-2017 inserted w.e.f. 25-1-2018. )

Following points to be considered for RCM:-

(a) Registration Compulsory to pay tax under reverse charge.

(b) A supplier cannot take ITC of GST paid on goods or services used to make supplies on which the recipient is liable to pay tax.

(c) Self-invoicing is to be done.

Article by Vikas Sharma

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice. Neither the authors accepts any liabilities for any loss or damage of any kind arising out of any information in this document nor for any actions taken in reliance thereon.

(Republished with Amendments. Amendments been made by CA Anita Bhadra)

Author Bio

Can we collect 5% gst on goods service vehicle from government organization or 12% gst

no.

I am a registered Person under GST Act. I have purchased timber from Un-registered person from Out of State then may I pay to tax under Reverse Charge.

(P.BHOOMAIAH)