India’s Goods & Services Tax (GST), implemented in 2017, was a major tax reform aimed at simplifying the tax system and enhancing compliance. However, over the years, several issues have emerged, making it a compliance nightmare for taxpayers. In this article, we will delve into the key challenges faced by taxpayers, offer recommendations for improvement, and assess their impact on businesses.

Date: 05-09-2023

To,

Shri Pankaj Chaudhary,

Hon’ble Union Minister of State for Finance,

Ministry of Finance, Government of India,

North Block, New Delhi-110001

Subject: Important Issues faced by Taxpayer in GST since 2017 with recommendation

Respected Sir,

India’s biggest tax reform, the Goods & Services Tax (GST) was introduced on 1 July 2017. The journey of GST in India has been a roller-coaster ride with many hits and misses. Since its inception, the Government has considered several legal and procedural changes to simplify the tax system for the smooth functioning of GST in the country. GST has also brought with it a paradigm shift in the use of technology in tax administration and compliance.

However, even 5 years and multiple policy amendments, it seems that not everything has unfolded as planned.

GST compliances which were envisaged to be easier and less complex, have turned out to be a compliance nightmare with multiple and frequent changes in the tax returns and reporting requirements. Further, the GST portal has been a puzzle and cause of concern for many taxpayers since its inception. Harmony between the provisions of the law and the functionality offered on the GST portal remains elusive. It took months to update the portal on account of changes in the law and process and still, it continued to face technical glitches. Today , we are representing before you some important issues in GST, which are faced by Taxpayer and Professional since 2017, which is directly impacting the business and eventually growth of nation.

Source: Top 10 Issues Faced by Professionals & Taxpayer in GST since 2017

We request your honour to kindly try provide relief on the same:-

Page Contents

- 1) Facility to file Revised Return:-

- 2) Tax Credit Mismatch Issue

- 3) ITC Denial, If Payment Is Not Made To Supplier within 180 Days

- 4) High Rate Of Interest For Late Payment 18%/24%, where As For Late Refund, Interest Rate Is Just6%.

- 5) Form of Annual Return and Reconciliation

- 6) SOME PERTINENT ISSUES FOR SMALL TRADERS and INDUSTRY:-

- 7) Issues for E-Commerce Companies

- 8) E-Way bill and Interstate Trade

- 9) E – INVOICING PROVISIONS:-

- Timeline: e-Invoicing Turnover Limit in India

- 10) WAY FORWARD :-

1) Facility to file Revised Return:-

DETAILS OF ISSUES:

Under GST Law, facility of Revised Return is not provided. If taxpayer makes any mistake while filing of GST Return, then he should be provided facility of filing of revised return, to correct his mistake in reporting. If any mistake happens in Sales, ITC details in GST Return, its revision is not allowed. Circular No 26/2017 dt 29.12.2017 issued to deal with such case and asked to make correction in subsequent GST Return. However subsequent return may not have said details and in such case, circular ask to do it in next-to-next return. This is cumbersome to follow. This also makes difficult to match the return data with books. Amendment facility in subsequent period, doesn’t help taxpayer to keep control of reporting and correction. Thus, Revision is better and has been a long demand of Tax Payer and Professionals.

RECOMMENDATION:

We understand that government doesn’t want to give revised return facility as it will impact recipient’s ITC. However, If revised return of Form GSTR 3B is allowed, it is not going to have impact as such on recipient tax credit. Recipient derives tax credit from GSTR 1. Therefore, revised return of GSTR 3B can be provided without any issue. Income Tax Act allows revision of ITR. Even in the service tax regime, returns filed were allowed to be revised. Even erstwhile VAT law allowed to file revised return. This is also helpful for taxpayer to ensure and check respective months liability is paid. However, till date taxpayer under GST not provided of such facility yet. It is very important issue faced by all taxpayer. To Err is Human. Therefore, we request government to provide facility to correct the mistake and error by way of Revised Return Facility.

2) Tax Credit Mismatch Issue

DETAILS OF ISSUES:

It is known fact that, when GST was introduced, required IT infrastructure was not available. Monthly Forms of GST which initially thought to be implemented (GSTR 1, GSTR 2 and GSTR 3), could not see light of the day after July 2017. GST law has concept of giving ‘rating/grade like thing’ to taxpayer, to know who is compliant and non-compliant taxpayer. However, even after 6 years of GST, this facility, provided by law is also not been provided so far. However, since beginning GST Law is stretching that, Buyer will get input tax credit only if it is paid by Supplier. However, buyer taxpayer is not provided proper infrastructure by government to comply this. Taxpayers job is to do the business and pay tax to government. GST Law cast additional, big and 100% responsibility on taxpayer to ensure that his supplier pays tax to government. This is not ease of doing business.

The process of the claim of Input Tax Credit (ITC) has undergone several changes over the last 6 years. Earlier, taxpayers were allowed to claim the entire eligible ITC based on their purchase invoices and GSTR-2A was only facilitation, which did not impact the ability of the taxpayer to avail ITC on a self-assessment basis. Subsequently, the ITC was restricted to 120%/110 %/105% (as amended from time to time) of the matched credits with GSTR-2A. Later, through another change in the functionality and law, ITC would not be available unless the details of invoices have been communicated in Form GSTR-2B by the government portal.

Further making matters worse, the Union Budget 2022 imposed another onerous condition that ITC would be available only if it is not restricted in the auto-generated form by the common portal. The restrictions enumerated under the said provisions are to address defaults of the suppliers viz. non-compliance with registration provisions, default in reporting and payment of tax, excess ITC availment, etc., the imposition of such restrictions on the recipient, for the non-compliance of a supplier causes hardships to the recipient, who has no recourse or control over the supplier. Seamless ITC is one of the stated objectives and salient features of GST, now becoming a casualty in the process.

The recent changes in reporting of returns in form GSTR-3B require the recipient to avail ITC as per the GSTR-2B data and reverse the ITC for supplies that are not received by him or in transit. The basic report for claiming ITC would be GSTR-2B and the taxpayer would be cumulatively required to maintain a reconciliation between their purchase register and the ITC claimed in GSTR-3B. Therefore, the recent changes in form GSTR-3B are primarily meant to ease tax administration, which adds to the woes of the taxpayer making compliance difficult and cumbersome.

In addition to the above, the ambiguity in the annual returns and reconciliation statement on several fronts, delay in operationalisation of forms such as ITC-02 have made compliances under GST a nightmarish proposition for taxpayers.

GSTR 2A facility was also provided in year 2019. Till date, government has not provided Best Reconciliation Software to GST ITC Reconciliation, which is basis of ITC match mistake. Isn’t it failure on part of government machinery?

Communication with supplier facility is provided on portal, but it was very recently and that it is not backed by any legal provisions. However, now taxpayers from whole India are receiving notices from authority for reversal of Input Tax Credit from 2017, if not paid by supplier and big demand is raised. While is totally unreasonable, in the absence of above explanation.

In many cases, supplier has paid tax under B2C category, but recipient is not allowed such ITC, as it is not reflecting in his account. In some cases, supplier has paid tax but on different GSTIN, than of his customer by mistake, but time limit to do amendment is over.

Another issue plaguing the taxpayers is fulfillment of condition of payment of tax to the Government exchequer by the supplier, in the absence of any formal tracking mechanism. The Government has now introduced rule 37A in the CGST Rules, providing that such tracking can be done based on status of filing of FORM GSTR 3B of supplier. In case of non-filing of FORM GSTR 3B by supplier for the period of relevant supply, by 30th September following the end of financial year, taxpayer is now required to reverse ITC availed in the GSTR 3B to be filed on or before 30th November following the end of financial year and can re-avail ITC after supplier files FORM GSTR 3B. To the extent, the taxpayer has a valid invoice and has paid the GST component to vendors, the cost is eligible as credit, then the input tax credit should not be denied only on the basis that the vendor has failed to file its GST return.

The Madras High Court in M/s D.Y. Beathel Enterprises v. the State Tax Officer, the Court while allowing the recipient to claim ITC observed that strict action must be taken against a seller who due to omission on his part fails to remit the tax paid by the recipient. Similarly, in Assistant Commissioner (CT), presently Thiruverkadu Assessment Circle, Kolathur, Chennai v. Infiniti Wholesale Ltd., the Madras High Court held that where the purchaser has proved that it has paid the due tax to the seller and furnishes the invoices for the same, it cannot be stopped from availing the ITC. The Court added that such a restriction on claiming ITC cannot be sustained and requires re-consideration. The courts have clearly noted that it is impractical and unrealistic to expect the buyer of supplies to go and verify the supplier’s accounts or to inquire with the department whether the tax paid by them on the inputs has been collected or not

RECOMMENDATION:

a) Some mechanism should be provided for correction of B2C, wrong GSTIN from 2017 at earliest. In Maharashtra VAT Law, Ledger confirmation like concept was introduced. GST Council and government should urgently think of bringing some mechanism to provide relief in these genuine cases.

b) Since proper infrastructure was not provided and GST being new law, 100% responsibility should not be casted upon buyer for payment of tax by supplier. It is first and foremost duty of GST Officer to catch such people who don’t make tax payment to government. If government thinks to recover said ITC from 2017 from buyer businessmen, without being provided proper infrastructure, it will amount to shut down/killing of many small taxpayer’s business.

c) No coercive and hard action should be taken by authority for ITC mismatch issue. Government should provide some mechanism at earliest. It is expected that the judiciary take steps to ensure that ITC is not denied to bona fide purchasers.

d) The Law should not compel the taxpayer to do the impossible i.e to ensure that the supplier has paid the tax to the Government. To the extent, the taxpayer has a valid invoice and has paid the GST component to vendors, the cost is eligible as credit, then the input tax credit should not be denied only on the basis that the vendor has failed to file its GST return .

3) ITC Denial, If Payment Is Not Made To Supplier within 180 Days

DETAILS OF ISSUES:

Sec 16 requires, reversal of ITC (with interest) if payment is not made to supplier within 180 days, from the date of invoice. This provision is introduced to support MSME to get payment on time from customer. However, practically, this provision is hitting hard to MSME. Most of MSME (might be more than 75 – 80%) are not able to payment to their supplier within 180 days. Some time contract provides more time for payment. However, GST Law require to reverse ITC along with interest, if not paid within 180 days.

RECOMMENDATION:

There are other law to govern payment compliance to small taxpayer (MSME Act) and therefore GST law should not specify any time limit for payment to supplier. Also Interest should not be asked for this. This provision, instead of supporting the MSMS, is on ground level / practically, found to be not convenient and raising heavy interest liability on MEMS on account of not compliance. Therefore it is requested that, GST Law should not monitor time limit of payment between supplier or customer or higher time limit (say 2 year) should be provided.

4) High Rate Of Interest For Late Payment 18%/24%, where As For Late Refund, Interest Rate Is Just6%.

DETAILS OF ISSUES:

In case of wrong availment of ITC/delayed payment of tax or any other reason, Interest is demanded at 24%/18%. This is very high. Due to financial crisis, tax payer is not able to make payment of tax and such higher interest rate, is very harsh and demotivating the compliance. Many times it is observed that taxpayer wants to pay Tax plus interest, due to such high interest, it makes him impossible, leading to stress among taxpayers.

RECOMMENDATION:

Even bank rates are now very lower. Around or less than 10% on loan. Therefore, it is requested that Rate of interest under GST should be rational to recover government loss. It is recommended that interest should be equal to interest rate on refund or 1.5 time of interest rate on refund but it should not be more than 12% in today’s scenario where Bank interest on FDs/Loan are reduced drastically.

5) Form of Annual Return and Reconciliation

DETAILS OF ISSUES:

Current Form of GST Annual Return has major issues. It doesn’t provide any tax calculation. Many Taxpayers found it is difficult to fill this form. Tax paid voluntarily through DRC 03 is not linked with Annual Return. Annual Return is important for Government officer too to check that whether taxpayer has paid all taxes correctly or not. However current form of GSTR 9, lacks all such ingredient.

RECOMMENDATION:

Government should come with new and more logical Annual Return Form. Annual Return Form should provide tax calculation. There should be some flow, some logic and proper patter of reporting of information on GST Portal. It should also consider Tax paid voluntarily earlier through DRC 03

If form become easy, its compliance will be simpler. [We request to refer Maharashtra VAT Audit Report Form 704. It was having some flow and easy to fill]

Government is also learning in GST and that’s why hundreds of notification/circulars are issued to make amendment. However, this sympathy is not provided to taxpayer. GST Law should not try to get success at the cost of lakhs of Taxpayer. GST is there, because of Taxpayer. Therefore, it is very important that government and GST Council should give atmost attention to basic issues of taxpayer which are not resolved since 2017. Else this will increase lot of stress and dissatisfaction among trade and professionals.

In conclusion, a pathbreaking and progressive piece of fiscal law has turned into a horror story from the perspective of a compliance ease promise. It is critical to reckon that the policies and procedures must be designed to reduce the compliance burden on honest taxpayers. It is anticipated that the GST Council would continue to consider the challenges faced while introducing appropriate changes for the seamless flow of ITC, simplification of compliance mechanisms, etc.

6) SOME PERTINENT ISSUES FOR SMALL TRADERS and INDUSTRY:-

GST implies additional operational costs for Small businesses. In a developing country like ours, not all SMEs will be able to afford the cost of computers and accountants required to implement GST (make bills and file tax returns). 28% GST rate on some products like plywood, automobile parts, and electronic items forces potential buyers to opt for unregistered dealers.

It is too difficult to assign MRP to handmade products like local shoes, Banarasi Sarees, etc. Most small artisans are illiterate and therefore unable to write MRP on their products and/or do any paperwork. Dealers are confused about how to rate such products.

Small businesses that have a small turnover and need not pay GST face trust issues. Buyers demand bills from even those sellers who are exempted from GST. Without proof of a certificate of GST exemption, small shop owners find themselves stranded and immobile.

Indian economy is majorly driven by small business units i.e SMEs. It will be unfair to expect small-scale business firms to make the transition to an online IT platform and expect no errors in return filing. It is an uphill task for the majority of our working population which has little hands-on experience with IT solutions. The cost of SRP deployment is a major concern for micro-small-medium scale enterprises.

The high compliance costs under GST have made it difficult for SMEs to operate and compete with larger businesses. The compliance costs involve various activities such as GST Registration, GST Return filing, maintaining records, and undergoing audits. The high costs have resulted in a significant burden for SMEs, reducing their profitability and competitiveness, increased compliance costs and reduced productivity.

7) Issues for E-Commerce Companies

E-commerce giants like Flipkart, Amazon also have not escaped the aftereffects of GST rollout. TCS has to be collected by the e-commerce companies from the sellers at the time of payment.

The capital blockage will hamper day to day operational costs due to TCS provisions. The GST council has fixed the 1 per cent TCS over the deduction made while payment to the sellers.

8) E-Way bill and Interstate Trade

The E-way bill had the potential to liberate interstate trade from all sorts of obstructions. The excitement could be felt among the slightly nervous business community. But on the day when the Finance Budget 2018 was being introduced to the Lower House, the lethargic GST network turned to be a major spoilsport and February 1 turned out to be a watershed moment for the upbeat government. The inability of the network to handle large volume e-way bill requests was at the forefront of public jokes and disappointment. Immediately e-way bill was rolled back. In the aftermath of the failure, goods carrying vehicles were left stranded and highways enjoyed pin drop silence for a few hours. The crumbling GST network has been in the spotlight from the very beginning and it continues to garner unwanted criticism and public grievances.

The GST Council need to find permanent scalable solutions rather than interim ones like the GSTR-3B. The sloppy GSTN Network raises serious concerns over the Government’s claim of a digital powered economy. GSTN is managed by Infosys, a premier IT services company. The e-way bill network was managed by the venerated NIC.

The GST E-way bill is a major concern for most of the companies which are regularly into the business of transporting goods and sending material over the locations, the transport company is also trying to figure out how it would deal with the GST E-way bill provisions. As soon the bill expires the transport company or the trucker himself has to generate the GST E-way bill on his own. The GST Council must have taken all these concerns into strict consideration and ensured easy and simple e-way bill generation procedure which has been effective from April 1, 2018

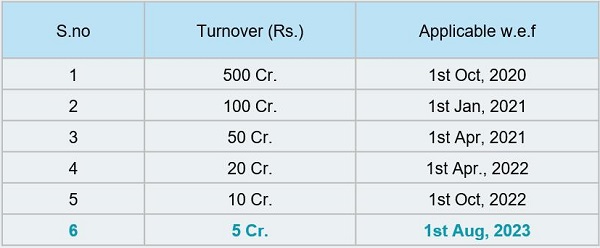

9) E – INVOICING PROVISIONS:-

On the recommendations of the CGST Council, e-invoicing has been introduced vide Notification No. 13/2020- Central Tax dated March 21, 2020 (as amended vide Notification No. 61/2020- Central Tax dated July 30, 2020) for B2B supplies of taxpayers having aggregate turnover of more than INR 500 crore in any preceding financial year from 2017-18 onwards w.e.f. October 1, 2020, with exceptions for certain taxpayers viz., SEZ units, an insurer or banking company or financial institution, GTA, passenger transport service provider and invoicing in case of services by way of admission to exhibition of cinematograph films in multiplex screens. Now, the above notification is further amended vide Notification No. 88/2020- Central Tax dated November 10, 2020, to make e-invoicing mandatory for B2B supplies of all taxpayers having aggregate turnover of more than INR 100 crore in any preceding financial year from 2017-18 onwards w.e.f. January 1, 2021 except notified exceptions.

The Central Board of Indirect Taxes (CBIC) announced Notification No. 10/2023–Central Tax dated May 10, 2023, as an amendment to Notification No. 13/2020 – Central Tax, dated March 21, 2020, to reduce the e-invoicing turnover limit to Rs 5 Crore, to be implemented wef August 1, 2023. This means that e-Invoice generation will be Mandatory for every taxpayer with an annual aggregate turnover exceeding Rs 5 Crore in any year from 2017-18 onwards to generate e-invoices for B2B supplies w.e.f. August 1, 2023.

Timeline: e-Invoicing Turnover Limit in India

In this regard, Rule 48(5) of the CGST Rules, 2017 (“CGST Rules”) states that if the invoice issued by a person to whom Rule 48(4) of the CGST Rules (i.e., e-invoice in Form GST INV-01 as prescribed) applies is not generated in accordance with the said sub- rule, the same will not be considered as a valid tax invoice. Thus, if an invoice is not registered on the IRP, then such an invoice would not be treated as a valid tax invoice as not having valid IRN for availing GST credit and all GST related matters. Therefore, if the Suppliers/ Vendors does not comply with the provisions of e-invoicing, then, the Recipients/Buyers can be disallowed Input Tax Credit (“ITC”) as one of the essential conditions to avail ITC as per Section 16(2)(a) of the CGST Act, 2017 (“CGST Act”) is possession of the tax invoice, which will be valid tax invoice only when such invoice is having valid IRN, digitally signed and having QR code assigned by the IRP. Further, non-compliances of above provisions may also result into levy of penalty under the CGST Act and Rules made there under.

Here the question arises as to how the buyer will know about the Turnover of Supplier’s/Vendor ?

RECOMMENDATION :-

Supplier’s/Vendor’s non-compliance of e-invoicing provisions should not cause denial of ITC to the Buyers/Recipients because Buyer is not bound to know about the Turnover criteria of Suppliers/Vendors and Buyer do not know whether E invoice provisions are applicable to supplier or not.

10) WAY FORWARD :-

- Refining the compliance system of GST: A GST in India continues to be a compliance burden with manifold filing obligations and lengthy returns. This has led to exorbitant compliance costs and efforts. An urgent need is to have rationalized, simplified, robust and reduced compliance conditions with sufficient scope for rectification and amendment to guarantee that correct disclosure can be made with the minimum difficulty and delay.

- Improving the GSTN system: One of the big challenges is that the GST Network (GSTN) compliance portal is yet to reach full operating capacity. From a credit standpoint, the GSTN portal has not accomplished the capability to match the efficacy of invoices. This is perhaps the main reason for fraudulent activities and fake invoices. The basic idea behind the digitalization of returns was to guarantee accurate compliance, leading to an accurate streamlining of credit and taxes.

- Further rate streamlining: A uniform and rationalized tax rate structure is a central characteristic of any effective GST legislation. Although the GST legislation has made some advances on this front, much work is needed to attain this target. Many nations implementing GST have only one rate for all items. From zero to 28%, India has seven rates, and this number goes up if we also take into account compensation rates. It would be better to reduce the GST tax rates to two or three.

- HS codes:There is also the requirement to restructure the GST rate list and make it compatible with machine processing. The GST uses harmonized structure (HS) codes for classifying most items. All GST rates should confirm to HS’s six-digit standard description.

- Formation of the GST Appellate Tribunal: Even after half a decade of GST execution, the GST Appellate Tribunal is yet to be established. This has resulted in multiple court cases, heavy interest costs and GST refunds being trapped. The wait for the creation of a statutory appellate tribunal discourages the dispute resolution method. The GST has resulted in a sharp rise in litigation largely because of ambiguous legal stipulations and how officials have issued orders.

- Increased investment in technology: With technology impacting all parts of the business, greater investment in technology for updating the user interface and making it simpler to use, especially for small and medium enterprises, could place the GST in India on par with the rest of the world and help accomplish the bigger goal of the ease of doing business.

- Raising the exemption limit: The government must set small business firms free by lifting the exemption limit. As per GST data, out of 14 million registrations, companies with less than INR15 million annual turnover account for 84%, but contribute less than 7% of the tax collected. The exemption limit must be lifted to INR15 million for goods and services. This is a monthly turnover of INR1.5 million, which at 10% of the profit margin converts into just INR120,000.

- Creation of federal institution: We need to create another institution in the form of a GST state secretariat that can bring together senior officers from the Centre and states in an institutional forum registered under the Society Act. This forum could also providea common point of contact for trade and industry to redress grievances on non-policy matters.

- NON COMPLIANCE OF E INVOICING PROVISIONS BY SUPPLIERS: –

Under the GST law, a tax invoice evidences as an important evidence to claim the Input Tax Credit (ITC). Section 16 of CGST Act 2017 states that a registered buyer cannot claim ITC unless he possesses a valid tax invoice or a debit note and such ITC appears as eligible one in GSTR-2B. If they possess an invalid invoice without IRN and signed QR code, it affects or delays the buyer’s eligibility to claim ITC.

Technically, details of an invoice without IRN cannot get auto-populated into GSTR-1 of the supplier and accordingly may never reflect in buyer’s GSTR-2A and GSTR-2B. The buyer cannot claim such amount as ITC where the tax is not deposited by the supplier with the government.

Supplier’s/Vendor’s non-compliance of e-invoicing provisions should not cause denial of ITC to the Buyers/Recipients because Buyer is not bound to know about the Turnover criteria of Suppliers/Vendors and Buyer do not know whether E invoice provisions are applicable to supplier or not.

Sir, We humbly request you to kindly consider above issue and take it to GST Council and try to provide give relief for same. Most of GST Issues will be resolved if government consider above issues and provide positive relief on it.

As Winton Churchill remarked ‘success is not final, failure is not fatal; it is the courage to continue that counts!’ Therefore, the GST reform has come a long way but still, multiple challenges are to be addressed to make it a success and achieve the objectives that were stated during its launch.

Thanks and Regards,

Chandani

Email Id : chandani.gadhia@rediffmail.com

Contact: 9322118767

Copy to: a) Hon’ble Smt. Nirmala Sitharaman, Union Minister of Finance and Chairman, Goods and Service Tax Council, Ministry of Finance, Government of India, North Block, New Delhi – 110001

b) Hon’ble GST Council Secretariat 5th Floor, Tower II, Jeevan Bharti Building, Janpath Road, Connaught Place, New Delhi-110 001

c) The Chairman of Central Board of Indirect Tax and Custom, North Block, New Delhi – 110001

d) Hon’ble State Finance Minister, Maharashtra Mantralaya Mumbai – 40003.

Source: Top 10 Issues Faced by Professionals & Taxpayer in GST since 2017

Author Bio