Soon before the roll out of GST, the most important concept to understand:

1. Place of supply of goods/ services; and

2. Time of supply of goods/ services

Before proceeding with the above concepts, lets understand when the CGST, SGST & IGST will be levied.

> Intra- State Supply

Location of Supplier & Place of supply ⇒ same State.

Which means 2 taxes will be levied i.e. CGST & SGST.

> Inter- State Supply

Location of Supplier & Place of supply ⇒ different State.

Which means only IGST will be levied.

Here, in this article, various aspects of supply of services are covered.

Let’s understand with a hypothetical example (In case of supply of services):

| Supply of services | Location of supplier | Location of recipient (place of supply) | Understanding | Interstate/ Intrastate | CGST+SGST/ IGST |

| If supply of services | State ‘Z’ | State ‘Z’ | Here, ‘Location of supplier’ & ‘Place of supply’ are same | Intra- State | CGST + SGST

|

| If supply of services | State ‘Z’ | State ‘A’ | Here, ‘Location of supplier’ & ‘Place of supply’ are different- | Inter- State | IGST |

Now understand the concept of location of Supplier, location of supplier of services covers the following aspects which can be better understood in tabular form:

| Location of Supply | For GST purpose |

| If supply made from a registered place of business | Location of such place of business |

| If supply made from a place other than registered place (but it is fixed establishment) | Location of such fixed establishment |

| If supply is made from more than one establishment | Location of establishment most directly concerned with provision of supply |

| If supply is made other then above place | Location of usual place of residence of supplier |

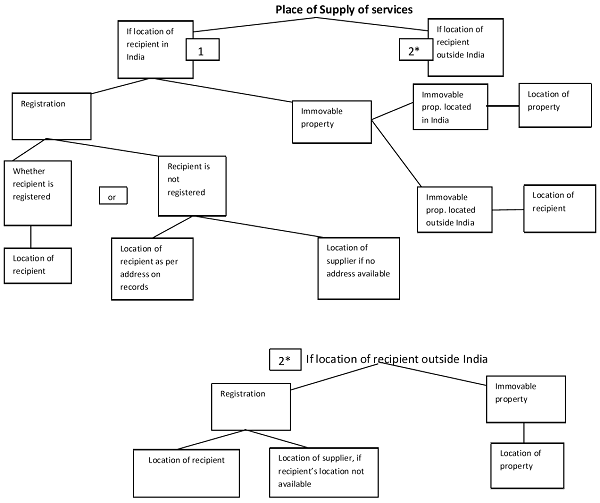

Now understand the concept of Place of supply of services, which covers the following aspects:

If location of recipient outside India

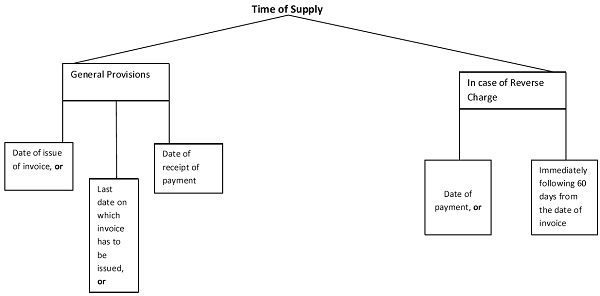

The liability to pay CGST/ SGST on services, shall arise at the time of supply, as determined in terms of the provisions of this section. The time of supply of services shall be earlier of the following dates:

Author: CS Ekta Maheshwari is the Author of this article and is Company Secretary by profession. The Author can be reached at csektamaheshwari14@gmail.com

Disclaimer:

The entire contents of this article is solely for information purpose and have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation.. It doesn’t constitute professional advice or a formal recommendation. The author has undertook utmost care to disseminate the true and correct view and doesn’t accept liability for any errors or omissions. You are kindly requested to verify & confirm the updates from the genuine sources before acting on any of the information’s provided herein above.

Author Bio

hlo mam !!!!!

great article

let me clear only one thing

” the tax /gst collection chargeing is only one time means from manufacturer only…….or it should be levied or charged or collected at every supply of chain……manufacturer to distributor to dealer to consumer etc.

plz. define it