Setting the context

The Goods and Services Tax (GST) has been a revolutionary tax reform in India, simplifying the Indirect Tax structure and bringing about greater transparency. One area that has been a subject of much debate and interpretation is the GST implications on transactions between a director and the company. GST Council continuously strives to bring clarity relating to the tax impact on various transactions between Director and the Company. Recently, in the 52nd GST Council meeting, recommendations are also made for issuing Clarifications regarding taxability of personal guarantee offered by directors to the bank against the credit limits/loans being sanctioned to the company

- Companies need to be vigilant about the kind of transactions they engage in with their directors to ensure compliance with the latest GST guidelines.

- For taxpayers and consultants, understanding these nuances is crucial for compliance and effective tax planning.

As the GST framework continues to evolve, staying updated with the latest changes is not just advisable but essential.

INTRODUCTION

The relationship between a Director and a Company is multifaceted, often blurring the lines between an employer-employee relationship and that of a supplier of services.

This article aims to provide an in-depth analysis of the same, shedding light on key provisions, categorizations, and practical implications. The approach is to dissect the GST implications on various transactions between a director and the company, providing a comprehensive understanding of the legal framework, types of transactions, practical challenges involved and the recent updates from the GST Council.

RCM for transactions between Director and the Company

Key Provision: Entry No. 6 of Notification No. 13/2017-Central Tax (Rate) dated 28.06.2017 stipulates that the tax on services supplied by a director of a company or a body corporate to the said company or body corporate shall be paid by the company or body corporate under the Reverse Charge Mechanism (RCM).

Categorisation of Director’s Services

In this article, we have analysed the Services provided by Director to Company into four broad categories namely:

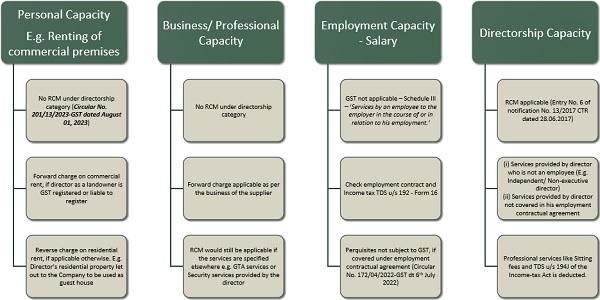

1. Personal Capacity – E.g. Renting of commercial premises

2. Business/ Professional Capacity

3. Employment Capacity – Salary

4. Directorship Capacity – Residual

Note: The above categorisations are made by the author for analysis and comprehensive understanding & presentation purpose – such categorisations are not prescribed in the GST law.

GST on Director services to the Company

A. PERSONAL CAPACITY

Recommendations of 50th meeting of GST Council dt 11th July 2023

It has been decided to clarify that services supplied by a director of a company to the company in his private or personal capacity such as supplying services by way of renting of immovable property to the company or body corporate are not taxable under RCM. Only those services supplied by a director of company or body corporate, which are supplied by him as or in the capacity of director of that company or body corporate shall be taxable under RCM in the hands of the company or body corporate under notification No. 13/2017-CTR (Sl. No. 6) dated 28.06.2017.

Based on the above recommendations, Circular No. 201/13/2023-GST dated 01.08.23 has been issued. Before moving to the circular, to understand the contextual background of this clarification, it is important to appraise the RCM on residential rental services.

Taxability on Renting of residential dwellings

Notification No. 04/2022 -Central Tax (Rate) dated 13th July 2022 amending Notification No 11/2017- Central Tax (Rate) dated 28.06.2017 – Serial No. 12

| Before 18-July-22 | From 18-July-22 |

| – Exemption for Services by way of renting of residential dwelling for use as a residence | – Exemption for Services by way of renting of residential dwelling for use as a residence except where the residential dwelling is rented to a registered person. |

Consequently, amendment was also made to Notification No. 13/2017 – Central Tax(Rate) on RCM vide Notification No.05/2022-Central Tax (Rate) dated 13th July 2022

| S. No. | Category of supply of services | Supplier of service | Recipient of service |

| 5AA | Service by way of renting of residential dwelling to a registered person | Any person | Any registered person |

Circular No. 201/13/2023-GST dated 01.08.23

Whether services supplied by director of a company in his personal capacity such as renting of immovable property to the company or body corporate are subject to Reverse Charge mechanism:

2. Reference has been received requesting for clarification whether services supplied by a director of a company or body corporate in personal or private capacity, such as renting of immovable property to the company, are taxable under Reverse Charge Mechanism (RCM) or not.

2.1 Entry No. 6 of notification No. 13/2017 CTR dated 28.06.2017 provides that tax on services supplied by director of a company or a body corporate to the said company or the body corporate shall be paid by the company or the body corporate under Reverse Charge Mechanism.

2.2 It is hereby clarified that services supplied by a director of a company or body corporate to the company or body corporate in his private or personal capacity such as services supplied by way of renting of immovable property to the company or body corporate are not taxable under RCM. Only those services supplied by director of company or body corporate, which are supplied by him as or in the capacity of director of that company or body corporate shall be taxable under RCM in the hands of the company or body corporate under notification No. 13/2017 CTR dated 28.06.2017.

B. Business/ Professional Capacity

Here, the director provides services in a business or professional capacity. No RCM is applicable under the directorship category. Forward charge or Reverse Charge taxability is applicable as per the business of the supplier. Security services / GTA services can be considered as an example here.

Security Services – RCM

Security services (services provided by way of supply of security personnel) provided to a registered person.

Supplier of Service: Any person other than a body corporate.

Recipient of Service: A registered person, located in the taxable territory.

RCM is applicable only if the supplier of service is a person other than a body corporate.

Inference: If Director as a sole proprietor is running Security services business, then Company shall pay tax under RCM under Security services category and not under Directorship category.

With respect to GTA Services, supplier has the option to choose forward charge or reverse charge mechanism and the taxability provisions would be applicable accordingly. GTA services are not discussed in detail here.

C. GST on Employment relationship

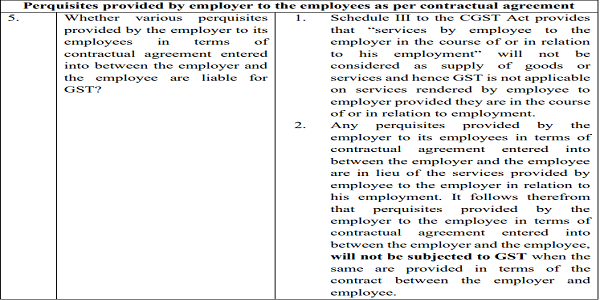

In this category, GST is not applicable as per Schedule III, which states that services by an employee to the employer in the course of or in relation to his employment are not subject to GST.

RELEVANT PROVISIONS OF THE ACT

SCHEDULE III – ACTIVITIES OR TRANSACTIONS WHICH SHALL BE TREATED NEITHER AS A SUPPLY OF GOODS NOR A SUPPLY OF SERVICES

1. Services by an employee to the employer in the course of or in relation to his employment.

SCHEDULE I – ACTIVITIES TO BE TREATED AS SUPPLY EVEN IF MADE WITHOUT CONSIDERATION

(2) Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business:

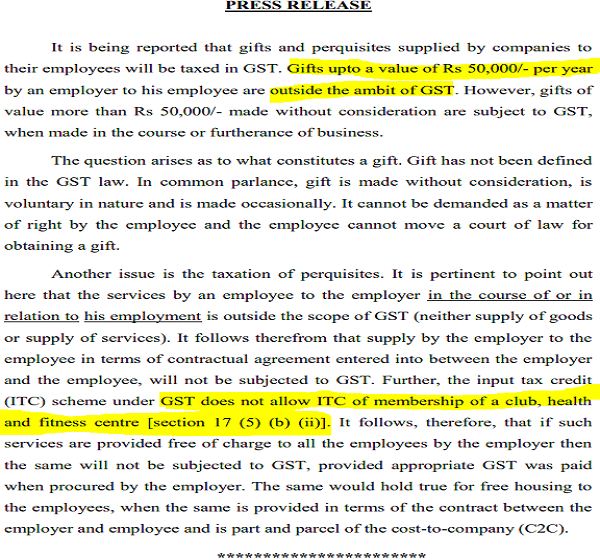

Provided that gifts not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as supply of goods or services or both.

Director Employee or not

> Apparently, the services provided by Director in employment capacity is completely outside GST law. However, it is important to evaluate if the given transaction in scrutiny is appropriately covered under the employment scope and whether the same is adequately supported by documentation.

> There is no definition of the term “employee” or “director” in the GST Laws.

> The term director is defined in Sec 2(34) of the Companies Act, 2013, as a director appointed to the Board of a company.

> The Hon’ble Supreme Court in the case of Apex Engineering, while considering the question of whether the managing director was an employee of the company in the context of the definition of employee in the Employees State Insurance Act, 1948 observed the following:

- ‘A Managing director may have a dual capacity. He may both be a director as well as employee, depending upon the nature of his work and the terms of his employment. Whether or not a Managing director is a servant of the company apart from his being a director can only be determined by the articles of association and the terms of his employment.’

- Thereby, the Supreme Court held that the managing director of the company is an employee of the company for the provisions of the Employees State Insurance Act, 1948.

> It is also pertinent to note CBIC Circular and Press Release issued in this regard.

Circular No. 172/04/2022-GST dated 6th July, 2022

CBIC Press Release dated 10th July 2017

GST on Employment relationship

> In case where he is a director and provides services in the capacity of an employee, then there is no GST as it would be squarely covered under Schedule-III as neither supply of goods nor supply of service.

While determining whether a director is an employee or not, it is quite possible that one may get into quick conclusions merely based on whether TDS is made under Section 192 of the Income Tax Act and Form 16 being issued in this regard. However, while these we could give prima facie conclusion, it is quite essential to analyze the terms of the employment contract to derive a final conclusion on the GST impact.

D. DIRECTORSHIP CAPACITY

This is an implied residuary category, wherein RCM is applicable as per Entry No. 6 of Notification No. 13/2017-CTR dated 28.06.2017. It typically covers the following:

(i) Services provided by director who is not an employee (E.g. Independent/ Non-executive director)

(ii) Services provided by director who is an employee, however the specific transaction is not covered in his employment contractual agreement

Director’s Sitting fees are usually covered in this category of RCM. One can also scrutinize the transactions on which TDS u/s 194J of the Income-tax Act is deducted to identify cases of RCM under Directorship capacity.

NO GST if NO Consideration on Personal Guarantee offered by Director for loan

Further 52nd GST Council Meeting held at New Delhi on 7th Oct 2023 also recommends to provide a clarity that PERSONAL GUARANTEE OFFERED BY DIRECTOR to the bank against the credit limits/loans being sanctioned to the Company is not covered under GST as long as there is no consideration for the same.

The relevant extracts from the ‘Measures for facilitation of trade’ vide the Press Release of the Recommendations of 52nd GST Council Meeting is as below:

ii) Clarifications regarding taxability of personal guarantee offered by directors to the bank against the credit limits/loans being sanctioned to the company and regarding taxability of corporate guarantee provided for related persons including corporate guarantee provided by holding company to its subsidiary company:

The Council has inter alia recommended to:

(a) issue a circular clarifying that when no consideration is paid by the company to the director in any form, directly or indirectly, for providing personal guarantee to the bank/ financial institutes on their behalf, the open market value of the said transaction/ supply may be treated as zero and hence, no tax to be payable in respect of such supply of services.

This provides a larger relief to corporates, since tax authorities were raising tax liability issues in this regard on notional values even in the absence of consideration. A Circular providing detailed clarification in this regard can soon be expected from CBIC.

CONCLUSION

Understanding the GST implications on transactions between a director and a company is crucial for compliance and optimal tax planning. Understanding the compliances and appropriately ensuring documentation would avoid tax litigations. While the framework is complex, a nuanced understanding can help in effective decision-making and risk mitigation.

Author’s Note: This guide is intended to provide a comprehensive understanding of the GST implications on transactions between a director and a company. However, it is advisable to consult with tax professionals for specific issues and challenges.