A. FAQs on Taking Actions during Assessment Proceedings under section 63 of Central Goods & Services Tax Act, 2017 against Unregistered Persons

General

Q.1 Who all fall under “Unregistered Persons” category?

Ans: Following persons will fall under “Unregistered Persons” category:

1. Taxable persons who are not registered under the GST and have not applied for registration under GST Act, but are liable to get registered as per the provisions of the Act.

2. Taxable persons whose registration has been cancelled due to some reason and they are liable to pay tax.

Q.2 When does the procedure of the Assessment of Unregistered Persons start?

Ans: The procedure of the Assessment of Unregistered Persons starts when a tax officer comes to know, either during inspection or survey or enforcement or through the information available with intelligence unit or through any other means, that a taxable person has failed to obtain registration or to pay taxes even though he/she is liable to do so.

Q.3 What is the procedure of the Assessment Proceedings u/s 63 against Unregistered Persons?

Ans: Following is the procedure of the Assessment Proceedings u/s 63 against Unregistered Persons:

1. Adjudicating Authority/ Assessing Authority (A/A) issues a “Show Cause Notice” to the taxable person and, if personal hearing is required, also schedules a date/time and venue for the same. In case of no reply is received from the taxable person, A/A issues a Reminder. Maximum three reminders can be issued.

2. Taxable person can reply to the issued notice offline and also request for a personal hearing in case A/A has not called for a personal hearing in the issued notice. Additionally, if required, he/she can also file offline for application of extension of personal hearing date. If A/A approves application of extension, A/A will issue an adjournment with the new date/time and venue of Personal hearing. Adjournment can be allowed maximum 3 times.

3. If Personal hearing is not required A/A, on the basis of taxable person’s reply, issues ASSESSMENT ORDER – ASMT-15 or DROP PROCEEDING Order. If Personal hearing is required, A/A conducts the personal hearing and on that basis issues the Order. If taxable person does not reply, even after the issue of three reminders, A/A issues the Order as per his/her discretion.

Tabs in Case Details page

Q.4 What are the various tabs available in case detail page?

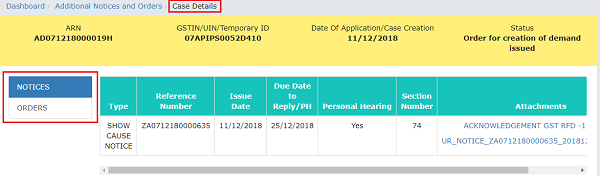

Ans: Two clickable tabs—NOTICES and ORDERS are available in case detail page.

NOTICES : To view issued Notices against you by Adjudicating or Assessing Authority (A/A)

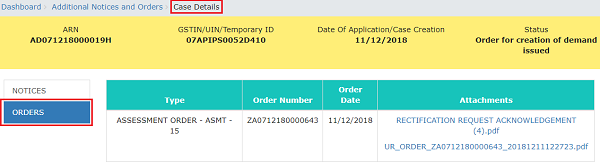

ORDERS : To download order issued against your case by Assessing Authority (A/A)

Viewing Notices and Orders

Q.5 What documents will I receive once Show Cause Notice (SCN) is issued by Tax Official?

Ans: Taxable persons will receive two documents: Show Cause Notice (SCN) in Form GST ASMT- 14, generated by the system, and Annexure, for detailed reasons, uploaded by the Tax Official.

Q.6 Where can I view notices and Orders issued to me?

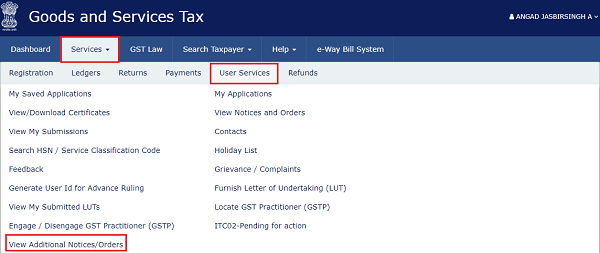

Ans: Taxable persons can view the notices and Orders issued to them by logging to the GST portal with their credentials, made available through SMS on mobile number of Taxable person and navigating to Services > User Services > View Additional Notices and Orders option.

Q.7 In the case of unregistered persons, will they be served the SCN and Reminders by post/special messenger?

Ans: Yes, in the case of unregistered persons, they will be served the SCN and Reminders by post/special messenger.

Q.8 In case notice/order etc. is issued by post/special messenger, then what will be the “Date of issue”?

Ans: Date of delivery will be considered as “Date of issue”.

Personal Hearing

Q.9 How many reminders can be issued to a Taxable person after the issue of SCN?

Ans: After the issue of SCN, maximum 3 reminders can be issued on the Portal.

Q.10 How much time is given to the Taxable persons for responding and attending the Personal Hearing?

Ans: Taxable person in general are given a time of 15 days to attend personal hearing. They can also seek extension (offline) of personal hearing. However, the tax officer can accept the application of extension and grant Adjournments up to maximum of three times.

Q.11 What is the next step if a Taxable person does not attend personal hearing?

Ans: In such a case, a reminder is issued to the Taxable person. Maximum three reminders can be issued. If the Taxable person does not appear within the time specified even after issue of reminder(s), an ex-parte order can be issued by tax official on the basis of available information and records.

SMS/ Email Alert to Person

Q.12 During Assessment/Adjudication proceedings against an unregistered person, at what different stages will a Taxable person receive an intimation via SMS or email?

Ans: During Assessment/Adjudication proceedings against an unregistered person, a Taxable person will receive an intimation via SMS or email if mobile no. and email ID is available with tax authorities and it is entered by the official at the time of Suo Moto registration proceedings. Intimation via SMS or email will be sent at the following stages:

A. Issue of SCN

B. Issue of each Adjournment notice

C. Issue of each Reminder

D. Issue of Assessment Order or Drop Proceeding Order

Q.13 What happens on the GST Portal when an Assessment Order is issued to an Unregistered Person?

Ans: When an Assessment Order is issued to an Unregistered Person, following actions will happen on the GST Portal:

- Intimation of the issue of order is sent to the concerned Taxable person via his/her email ids and SMS.

- Status of ARN/Case ID and RFN will be changed to ‘Order for creation of demand issued’.

- Reference number of the order will be generated.

- Electronic liability register and DCR of the unregistered person shall also get updated with the demand specified in the order

Viewing Statuses

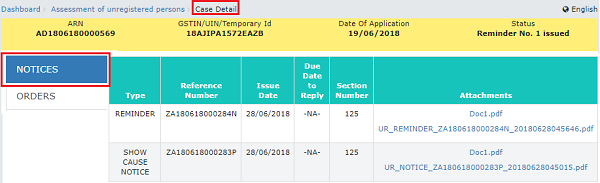

14. During the Assessment/Adjudication proceedings on the case of an Unregistered Person, what all Status changes does the case undergo?

Ans: During the Assessment/Adjudication proceedings on the case of an Unregistered Person, the case may undergo following Status changes:

- Pending for reply by Taxable person: When A/A issues a “Show Cause Notice” to the Taxable person

- Reminder No. 1 issued: When A/A issues first Reminder to the Taxable person in case the Taxable person has not responded to the Show Cause Notice within the time specified therein

- Reminder No. 2 issued: When A/A issues second Reminder to the Taxable person in case the Taxable person has not responded to the Show Cause Notice within the time specified therein

- Reminder No. 3 issued: When A/A issues third Reminder to the Taxable person in case the Taxable person has not responded to the Show Cause Notice within the time specified therein

- Order for creation of demand issued: When ASSESSMENT ORDER – ASMT-15 Order is issued by A/A to the Taxable person

- Order for dropping proceedings issued: When DROP PROCEEDING Order is issued by A/A to the Taxable person

B. Manual on Taking Actions during Assessment Proceedings u/s 63 of Central Goods & Services TAx Act, 2017 against Unregistered Persons

How can I take action during assessment proceedings u/s 63 initiated against me by the Adjudication Authority(A/A)?

To take action during assessment proceedings u/s 63 initiated against you by the Adjudication Authority (A/A), perform following steps:

1. Navigate to View Additional Notices/Orders page to view Notices and Orders issued against you by Adjudicating or Assessing Authority (A/A)

2. Take action using NOTICES tab of Case Details screen: View issued Notices

3. Take action using ORDERS tab of Case Details screen: View issued Order

A. View Additional Notices/Orders

To view issued Notices and Orders, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the portal with valid credentials.

3. Dashboard page is displayed. Click Dashboard > Services > User Services > View Additional Notices/Orders

4. Additional Notices and Orders page is displayed.

- All orders/notices are displayed in descending order. You can search for the orders/notices you want to view using the Navigation buttons provided below.

- Click the View hyperlink to go to the Case Details screen of the issued Notice/Order.

5. Case Details page is displayed.

- The yellow bar on the top contains details related to the case—Case Reference Number (ARN), Temporary ID that has been issued to you, Date of Case Creation and Status of the Case

- The left-side of the page contains two clickable tabs—NOTICES and ORDERS. The NOTICES tab is selected by default. You can click these tabs to view more details about each tab.

- Below the yellow bar, table containing details of the tab is displayed.

B. Take action using NOTICES tab of Case Details screen: View issued Notices

To view issued Notices, perform following steps:

1. On the Case Details page of that particular Case ID, select the NOTICES tab, if it is not selected by default. This tab displays all the notices (Reminder/Adjournment/Show Cause Notice) issued by A/A to you.

2. Click the document name(s) in the Attachments section of the table to download into your machine and view them.

C. Take action using ORDERS tab of Case Details screen: View Order Issued Against Your Case

To download order issued against your case, perform following steps:

1. On the Case Details page of that particular Case ID, click the ORDERS tab. This tab provides you an option to view the issued order, with all its attached documents, in PDF mode.

2. Click the document(s) in the Attachments section of the table to download and view them.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.