The year 2019 was a difficult year for the global economy with world output growth estimated to grow at its slowest pace of 2.9 per cent since the global financial crisis of 2009, declining from a subdued 3.6 per cent in 2018 and 3.8 per cent in 2017. Uncertainties, although declining, are still elevated due to protectionist tendencies of China and USA and rising USA-Iran geo-political tensions. Amidst a weak environment for global manufacturing, trade and demand, the Indian economy slowed down with GDP growth moderating to 4.8 per cent in H1 of 2019-20, lower than 6.2 per cent in H2 of 2018-19. A sharp decline in real fixed investment induced by a sluggish growth of real consumption has weighed down GDP growth from H2 of 2018-19 to H1 of 2019-20. Real consumption growth, however, has recovered in Q2 of 2019-20, cushioned by a significant growth in government final consumption. At the same time, India’s external sector gained further stability in H1 of 2019-20, with a narrowing of Current Account Deficit (CAD) as percentage of GDP from 2.1 in 2018-19 to 1.5 in H1 of 2019-20, impressive Foreign Direct Investment (FDI), rebounding of portfolio flows and accretion of foreign exchange reserves. Imports have contracted more sharply than exports in H1 of 2019-20, with easing of crude prices, which has mainly driven the narrowing of CAD. On the supply side, agricultural growth, though weak, is moderately higher in H1 of 2019-20 than in H2 of 2018-19. Headline inflation rose from 3.3 per cent in H1 of 2019-20 to 7.4 per cent in December 2019 on the back of temporary increase in food inflation, which is expected to decline by year end. Rise in CPI-core and WPI inflation in December 2019 suggests building of demand pressure.

The deceleration in GDP growth can be understood within the framework of a slowing cycle of growth with the financial sector acting as a drag on the real sector. In an attempt to boost demand, 2019-20 has witnessed significant easing of monetary policy with the repo rate having been cut by RBI by 110 basis points. Having duly recognized the financial stresses built up in the economy, the government has taken significant steps this year towards speeding up the insolvency resolution process under Insolvency and Bankruptcy Code (IBC) and easing of credit, particularly for the stressed real estate and Non-Banking Financial Companies (NBFCs) sectors. At the same time, impact of critical measures taken to boost investment, particularly under the National Infrastructure Pipeline, present green shoots for growth in H2 of 2019-20 and 2020-21. Based on first Advance Estimates of India’s GDP growth for 2019-20 recorded at 5 per cent, an uptick in GDP growth is expected in H2 of 2019-20. The government must use its strong mandate to deliver expeditiously on reforms, which will enable the economy to strongly rebound in 2020-21.

GLOBAL ECONOMY IN 2019-20

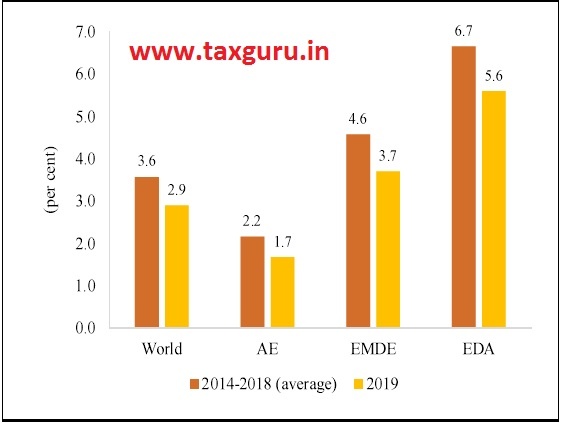

1.1 The World Economic Outlook (WEO) Update of January 2020 published by IMF has estimated the global output to grow at 2.9 per cent in 2019, declining from 3.6 per cent in 2018 and 3.8 per cent in 2017. The global output growth in 2019 is estimated to be the slowest since the global financial crisis of 2009, arising from a geographically broad-based decline in manufacturing activity and trade. Stabilising, yet uncertain, trade tensions between China and the USA have contributed to the decline of world output and trade. The growth of advanced economies has similarly declined from 2.5 per cent in 2017 to 2.2 per cent in 2018 and is estimated to further decline to 1.7 per cent in 2019 (Figure 1). The larger group of OECD countries has also seen a drop in their growth from 2.6 per cent in 2017 to 2.3 per cent in 2018 and is estimated to grow at 1.7 per cent in 2019. WEO has projected the declining growth of global output to rebound in 2020 with a modest uptick to 3.3 per cent.

Figure 1: Growth of global output

Data Source: World Economic Outlook, October 2019 database and January 2020 update

Note: AE – Advanced Economies, EMDE – Emerging Market and Developing Economies, EDA – Emerging and Developing Asia.

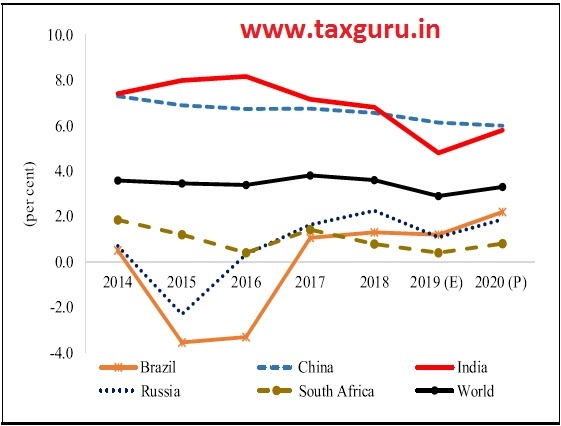

Figure 2: Growth of individual BRICS countries

Data Source: World Economic Outlook, October 2019 database and January 2020 update

Note: E – Estimates of IMF, P – Projections of IMF

1.2 As in other major economies, India’s Gross Domestic Product (GDP) growth also correlates with the growth of global output, an observation earlier made in the Economic Survey of 2015-16. Not surprisingly, the deceleration in India’s GDP growth since 2017 has tracked the decline in world output (Figure 2). However, for three years prior to 2017, when global output growth was not declining, India surged ahead of the rest of the world, recording in 2014-18 an average growth significantly higher than that of any comparable peer, both among advanced and emerging market economies. The WEO Update of January 2020 has projected the growth of Indian economy to increase to 5.8 per cent in 2020 expecting India to contribute significantly to an eventual pickup in the growth of world output. India’s GDP in nominal prices was ` 190.1 lakh crore (US$ 2.7 trillion) in 2018-19.

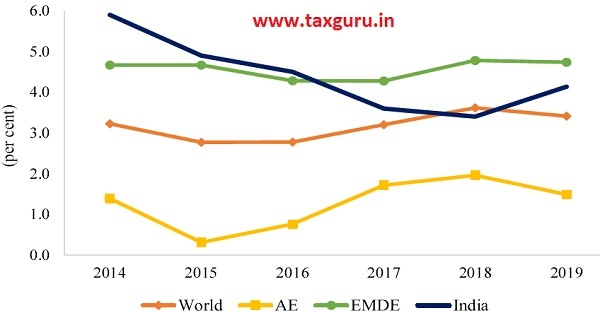

1.3 Along with the weakening of global economic activity, inflation the world over also remained muted in 2019 (Figure 3). Inflation softened in advanced and emerging economies reflecting a slack in consumer demand. From the supply side, lower energy prices in 2019 also contributed to softening of inflation. In India, inflation slightly rose to 4.1 per cent in April-December 2019, after a sharp decline from 5.9 per cent in 2014 to 3.4 per cent in 2018.

Figure 3: Consumer Price inflation across country groups

Data Source: World Economic Outlook, October 2019 database, National Statistical Office

Notes: 1. AE – Advanced Economies, EMDE – Emerging Market and Developing Economies, EDA – Emerging and Developing Asia.

2. For India, years are from April to March and data for 2019 is for April to December.

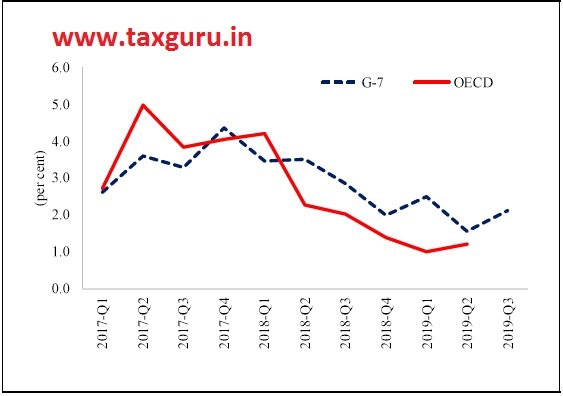

1.4 The global slack in consumer demand affected industrial activity, which slumped in most of the major economies in 2019 (Figure 4 and Figure 5). In particular, global production in automobile industry fell sharply due to a decline in demand, which was caused by changes in technology and emission standards in many countries.

Figure 4: Growth of fixed investment

Data Source: OECD database

Note: Quarters are on calendar year basis.

G-7 refers to the group of seven large advanced economies in the world; namely Canada, France, Germany, Italy, Japan, the United Kingdom and the United States

Figure 5: Growth of index of manufacturing production

Data Source: OECD database

Note: Quarters are on calendar year basis.

OECD is the Organisation for Economic Co-operation and Development with 36 member countries.

India also experienced a similar downturn in the auto industry (IMF’s World Economic Outlook October, 2019 and January 2020).

1.5 As global industrial activity slowed down, there was a drop in growth of manufacturing exports from major economies. Increasing trade barriers as well as trade uncertainty stemming from growing trade tensions also weakened business confidence and further limited trade. India’s manufacturing exports also fell (Figure 6).

INDIAN ECONOMY IN 2019-20 Size of the economy

1.6 The WEO of October 2019 has estimated India’s economy to become the fifth largest in the world, as measured using GDP at current US$ prices, moving past United Kingdom and France. The size of the economy is estimated at US$ 2.9 trillion in 2019 (Table 1).

Figure 6: Non-agriculture, non-fuel merchandise export1 growth

Data Source: Trade Map Database

Table 1: Top 10 Economies in the world in terms of GDP at current US$ trillion

| Sl. No. | Country | 2017 | 2018 | 2019 (E) | Change in position in 2019 |

| 1 | United States | 19.5 | 20.6 | 21.4 | – |

| 2 | China | 12.1 | 13.4 | 14.1 | – |

| 3 | Japan | 4.9 | 5.0 | 5.2 | – |

| 4 | Germany | 3.7 | 4.0 | 3.9 | – |

| 5 | India | 2.7 | 2.7 | 2.9 | ▲ |

| 6 | United Kingdom | 2.6 | 2.8 | 2.7 | ▼ |

| 7 | France | 2.6 | 2.8 | 2.7 | ▼ |

| 8 | Italy | 2.0 | 2.1 | 2.0 | – |

| 9 | Brazil | 2.1 | 1.9 | 1.8 | – |

| 10 | Korea | 1.6 | 1.7 | 1.6 | – |

Data Source: World Economic Outlook, October 2019 database

Notes: E : IMF’s estimate; ▲ indicates improvement in rank;▼ indicates drop in rank and – indicates unchanged rank

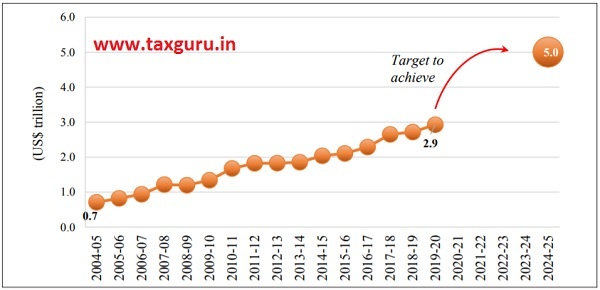

1.7 In July 2019, the Union Budget 201920 had articulated the vision of the Hon’ble Prime Minister to make India a US$ 5 trillion economy by 2024-25. The march towards this milestone has, however, been challenged by less than expected growth of India’s GDP so far this year, on the back of a decline in world output. Yet, given India’s record of growth with macroeconomic stability over the last five years (annual average growth rate of 7.5 per cent and annual average inflation of 4.5 per cent), the economy is poised for a rebound towards the US$ 5 trillion goal (Figure 7).

Figure 7: Increasing size of the Indian economy (GDP at current US$)

Data Source: National Statistical Office, Reserve Bank of India (RBI) and IMF

GVA and GDP growth

1.8 The National Statistical Office (NSO) has estimated India’s GDP to have grown at 4.8 per cent in the first half (H1) (April-September) of 2019-20, lower than 6.2 per cent recorded in the second half (H2)

(October-March) of 2018-19. On the supply side, the deceleration in GDP growth has been contributed generally by all sectors save ‘Agriculture and allied activities’ and ‘Public administration, defence, and other services’, whose growth in H1 of 2019-20 was higher than in H2 of 2018-19 (Table 2).

Table 2: Quarter wise growth of real Gross Value Added (GVA) and GDP (per cent)

| GVA at basic prices | 7.7 | 6.9 | 6.3 | 5.7 | 4.9 | 4.3 |

| Agriculture, forestry & fishing | 5.1 | 4.9 | 2.8 | –0.1 | 2.0 | 2.1 |

| Industry | 9.8 | 6.7 | 7.0 | 4.2 | 2.7 | 0.5 |

| Services | 7.1 | 7.3 | 7.2 | 8.4 | 6.9 | 6.8 |

| GDP at market prices | 8.0 | 7.0 | 6.6 | 5.8 | 5.0 | 4.5 |

Data Source: National Statistical Office

1.9 On the demand side, the deceleration in GDP growth was caused by a decline in the growth of real fixed investment in H1 of 2019-20 when compared to 2018-19 induced in part by a sluggish growth of real consumption. However, growth of real consumption started picking up in Q2 of 2019-20, mostly driven by a significant jump in government final consumption. Growth of private final consumption expenditure also picked up in the same quarter. The contribution of net exports to GDP in Q2 of 2019-20 became less negative as in real terms the contraction of exports was much smaller than contraction of imports. Lower growth of GDP and softer price of crude oil caused a large contraction of imports (Table 3).

Table 3: Real growth of GDP (per cent)

| 2017-18 | 2018-19 (PE) | 2019-20 | ||

| Q1 | Q2 | |||

| Gross Domestic Product | 7.2 | 6.8 | 5.0 | 4.5 |

| Total consumption | 8.6 | 8.3 | 4.1 | 6.9 |

| Government consumption | 15.0 | 9.2 | 8.8 | 15.6 |

| Private consumption | 7.4 | 8.1 | 3.1 | 5.1 |

| Fixed investment | 9.3 | 10.0 | 4.0 | 1.0 |

| Exports of goods and services | 4.7 | 12.5 | 5.7 | -0.4 |

| Imports of goods and services | 17.6 | 15.4 | 4.2 | -6.9 |

Data Source: National Statistical Office

Note: PE – Provisional Estimates.

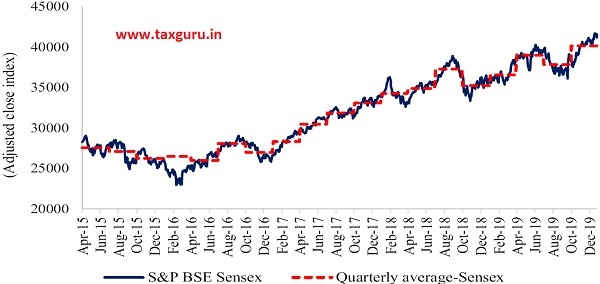

1.10 Despite the deceleration in GDP growth for the sixth consecutive quarter, the stock market continues to be upbeat about the country’s growth prospects. The Bombay Stock Exchange (BSE) Sensex increased by 7.0 per cent at end December 2019 over end March 2019 (Figure 8). This may also reflect the growing perception of India becoming an attractive destination for investment in the backdrop of a decline in the growth of major economies of the world and continued easing of monetary policy by the US Fed. The net FDI and net Foreign Portfolio Investment (FPI) in first eight months of 2019-20 stood at US$ 24.4 billion and US$ 12.6 billion respectively, more than the inflows received in the corresponding period of 2018-19.

1.11 Since 2011-12, India recorded its lowest quarterly GDP growth in Q4 of 2012-13 (Figure 9). After 13 quarters, the economy achieved its highest quarterly growth of 9.4 per cent in Q1 of 2016-17. Again after 13 quarters, the economy has recorded a low growth of4.5 percentinQ2 of2019-20. Itappears thatthe length of the business cycle is about 13 quarters. A study on business cycle measurement in India (Pandey et al. 2018) using growth data since 1996 shows similar results. Their study indicates that when GDP is accelerating the business cycle on average is 12 quarters. However, in the deceleration phase, the business cycle on average reduces to 9 quarters. A resurgence in growth is, accordingly, expected to begin in H2 of 2019-20.

Figure 8: Movement in BSE Sensex

Data Source: BSE

Figure 9: Quarter wise growth of real GDP

Data Source: National Statistical Office

Inflation

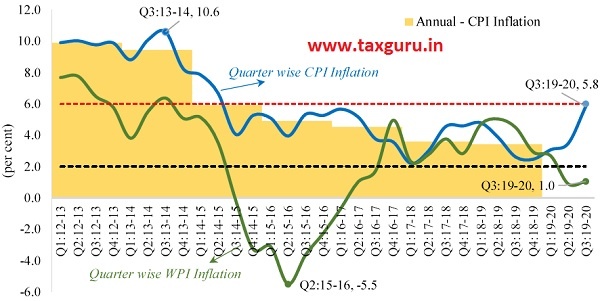

1.12 In H1 of 2019-20, CPI (Headline) inflation was estimated at 3.3 per cent, slightly higher than that in H2 of the previous year. There has been a further uptick in headline inflation in the month of December 2019 to 7.35 per cent contributed mainly by supply-side factors. The food prices spiked following unseasonal rainfall and a flood-like situation in many parts of the country, which affected agricultural crop production. The Wholesale Price Index (WPI) inflation, on the other hand, declined sharply from 3.2 per cent in April 2019 to 2.6 per cent in December 2019, reflecting weakening of demand pressure in the economy (Figure 10).

Figure 10: CPI and WPI inflation

Data Source: National Statistical Office and Department for Promotion of Industry and Internal Trade (DPIIT)

1.13 Core inflation (headline less food and fuel inflation) further reflects the state of demand in the economy. There has been a secular moderation in CPI-core inflation from 6.3 per cent in Q1 of 2018-19 to 4.3 per cent in Q2 of 2019-20, which also reflects a weakening of demand pressure in the economy. The core-CPI and WPI inflation together moderated inflation, as captured by the GDP deflator, which fell from 3.7 per cent in H2 of 2018-19 to 2.1 per cent in H1 of 2019-20. This significantly lowered the nominal growth of GDP as well.

Employment: Formal vs. Informal

1.14 As several polices have been implemented to enhance the formalization of the economy, examining the impact of the same is crucial Due to the changes in methodology and sampling design, labour market estimates based on Periodic Labour Force Survey (PLFS) are not strictly comparable with the results of earlier quinquennial surveys on Employment-Unemployment conducted by National Sample Survey Organization (NSSO). Yet a limited comparability has been attempted to highlight the shift towards increased employability in formal sector jobs.

1.15 As per the latest available data on employment, there has been an increase in the share of formal employment, as captured by ‘Regular wage/salaried’, from 17.9 per cent in 2011-12 to 22.8 per cent in 2017-18 (Figure 11). This 5 percentage points increase in the share of ‘Regular wage/salaried’ group has been on account of 5 percentage points decrease in the share of casual workers, which reflects formalization in the economy. As a result, in absolute terms, there was a significant jump of around 2.62 crore new jobs over this period in the usual status category with 1.21 crore in rural areas and 1.39 crore in urban areas. Remarkably, the proportion of women workers in ‘Regular wage/salaried’ employees category has increased by 8 percentage points (from 13 percent in 201112 to 21 per cent in 2017-18) with addition of 0.7 crore new jobs for female workers in this category. The drop in casual labour has mainly originated from the rural sector where rural labourers have shifted from agricultural to industrial and services activity. In urban region, there has been a shift of employment from self- employed to salaried jobs.

Figure 11: Distribution of workers by all ages in usual status (PS+SS) by statuses in employment

Data Source: Periodic Labour Force Survey 2017-18, Ministry of Statistics & Programme Implementation

Note: PS- Principal Status, SS- Subsidiary Status.

1.16 The provisional Annual Survey of Industries for fiscal year ending March 2018, also shows an increase in jobs in the organized manufacturing sector. Between 2014-15 and 2017-18, total number of workers increased by 14.7 lakh and total persons engaged increased by 17.3 lakh, in the organised manufacturing sector in India.

Fiscal situation

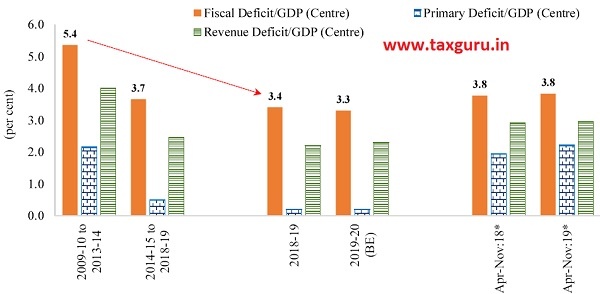

1.17 In 2019-20, Centre’s fiscal deficit was budgeted at ` 7.04 lakh crore (3.3 per cent of GDP), as compared to ` 6.49 lakh crore (3.4 per cent of GDP) in 2018-19 PA (Figure 12). In the first eight months of 2019-20, fiscal deficit stood at 114.8 per cent of the budgeted level .

1.18 Net Tax revenue to the Centre, which was envisaged to grow at more than 25 per cent in 2019-20 BE relative to 2018-19 PA, grew at 2.6 per cent during April to November 2019, which was nearly half its’ growth rate for the corresponding period last year. This is primarily owing to low growth in Gross Tax Revenue (GTR) of 0.8 per cent during first eight months of 2019-20 vis-a-vis 7.1 per cent growth for the corresponding period in 2018-19 (Table 6, Chapter 2). Goods and Services Tax (GST) collections, the biggest component of indirect taxes, grew by 4.1 per cent for the Centre during April-November 2019. However, the uptick in growth of cumulative GST collections for the Centre started in October 2019 and has sustained its momentum in November and December 2019 as well.

1.19 Specifically, the GST (Centre + States) collection for the month of November 2019 was the third highest monthly collection since introduction of GST (July 2017). From April-December 2019, gross GST revenue collection has crossed the mark of ` 1 lakh crore five times with a revenue of ` 1.03 lakh crore in December 2019. This may be the result of concerted efforts taken by the Government to improve tax compliance and revenue collection as well as a reflection of a rebounding economy.

1.20 On the expenditure side, the budgeted expenditure of the Central government grew at 12.8 per cent in April-November 2019 over the corresponding period of the previous year, expending almost 60 per cent of the budget. The capital expenditure during April to November 2019-20 has grown at roughly three times vis-à-vis the same period in 2018-19. Also, revenue expenditure has grown at a higher rate during these eight months of 2019-20, compared to the same period previous year (Chapter 2, Figure 8).

Figure 12: Gross Fiscal Deficit (Centre) as percentage of GDP

Data Source: Union Budget and CGA

Note: * : The figures for 2018 are with respect to GDP (PE) data for 2018-19 and figures for 2019 are provisional and with respect to budgeted GDP for 2019-20.

Monetary policy

1.21 The liquidity condition of banks became comfortable after June 2019 and has remained healthy since then (Chapter 4, Figure 5). Average daily net absorption soared from ` 45.6 thousand crore in June 2019 to ` 256.4 thousand crore in December 2019. Durable liquidity injection was undertaken through four open market operation (OMO) purchase auctions and a US$ 5 billion buy/sell swap auction. Abundant liquidity in the banking system is also reflected in the weighted call money rate, which has mostly traded within the Liquidity Adjustment Facility (LAF) corridor (LAF corridor is the spread between the repo and the reverse repo rate) (Chapter 4, Figure 6).

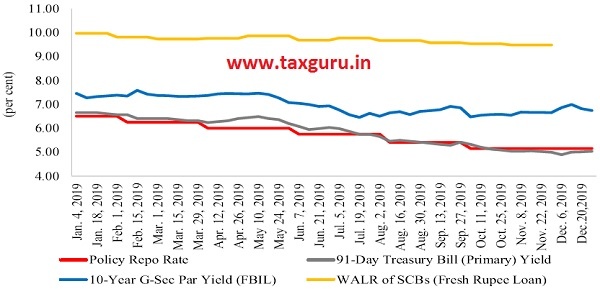

1.22 The stance of the Monetary Policy Committee of Reserve Bank of India continued to be accommodative as it reduced the policy repo rate by 135 basis points since February 2019. The rate cut along with excess liquidity in banks was expected to transmit well into lowering interest rates. However, the transmission has varied across different market segments (Figure 13). The transmission to short term treasury bills was full during this period while it was partial for long term securities. The transmission to credit market was also partial as Weighted Average Lending Rate (WALR) of Scheduled Commercial Banks (SCBs) on fresh rupee loan reduced by only 33 basis points (bps) between February and November 2019. Thus, less than a quarter of the rate cuts by RBI was transmitted by banks to new borrowers. The median of 1-year Marginal Cost of Funds based Lending Rate (MCLR) reduced by 49 bps between February and November 2019; which represents a transmission of about a third of the rate cut by RBI.

Figure 13: Policy rate, yield and lending rate

Data Source: RBI

Note: WALR refers to Weighted Average Lending Rate

Credit growth

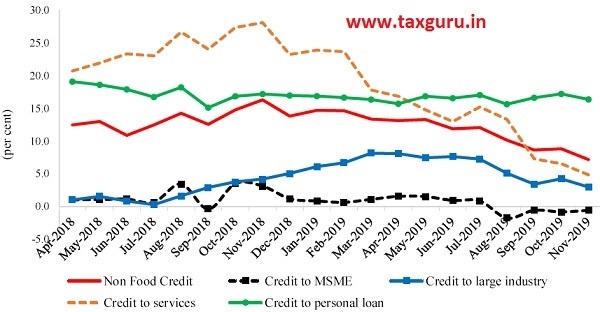

1.23 The growth of bank credit which was picking up in H1 of 2018-19, started decelerating in H2 of 2018-19 and further in H1 of 2019-20. The deceleration was witnessed across all major segments of non-food credit, save personal loans which continued to grow at a steady and robust pace. The deceleration in credit growth was most in the services sector. Credit growth to industry also witnessed a significant decline in recent months, both for MSME sector as well as large industries. Agriculture and allied activities benefited from a higher growth of credit (Figure 14).

1.24 Decline in credit growth has been attributed to growing risk aversion of banks that continue to apprehend the build-up of Non-Performing Assets (NPAs). This is despite the admission of more than 2000 corporate insolvency resolution processes between December 2016 and June 2019.

Figure 14: Growth of non-food bank credit

Data Source: RBI

Note: Growth of sectoral credit corresponds to select 41 Scheduled Commercial Banks.

The IBC process contributed to reducing the NPAs from 11.2 per cent of gross advances in March 2018 to 9.3 per cent in March 2019. However, the NPA ratio remains the same six months forward, at 9.3 per cent, in end September 2019.

1.25 The prospects of easy investment in G-secs is possibly running complementary to the risk aversion being displayed by SCBs. During the first eight months of 2019-20, scheduled commercial banks mobilized the same amount of deposits as in the corresponding period of the previous year. Yet, the SCBs chose to invest thrice the amount in G-secs in the current year, as compared to the previous year while reducing their credit off-take by more than four-fifths. It appears that risk aversion towards lending to the private sector has increased in 2019 (Table 4).

1.26 The risk aversion to lending to the private sector appears to be relatively more in respect of Public Sector Banks (PSBs). As Figure 15 shows, growth of credit from the PSBs was not only much lower than that of private sector banks but credit growth of PSBs also dipped sharply from December 2018 onwards.

External sector performance

1.27 In October and November 2019, major commodity groups have shown a positive growth in exports over the corresponding month of the previous year while imports of major commodity groups have contracted. However, the slower contraction in merchandise exports as compared to imports has so far resulted in improvement in trade balance in 2019-20 (Figure 16).

Table 4: Net Scheduled Commercial Bank Credit (in Rs. lakh crore)

| April-November | ||

| 2018-19 | 2019-20 | |

| Net Credit of Scheduled Commercial Banks | 5.07 | 0.89 |

| Net Aggregate Deposits of Scheduled Commercial Banks | 3.87 | 3.85 |

| Incremental Credit-Deposit Ratio (per cent) | 131.0 | 23.1 |

| Investment in Government Securities | 1.07 | 3.37 |

Data Source: RBI

Figure 15: Growth in credit of Public & Private Sector Banks

Data Source: RBI

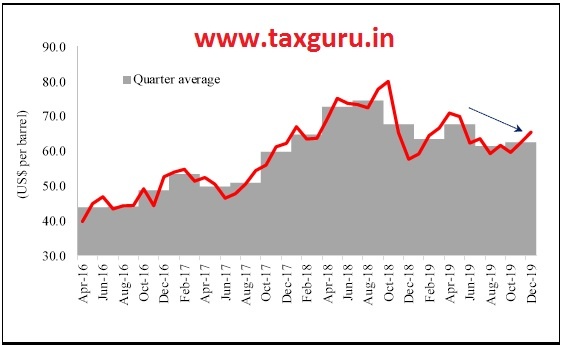

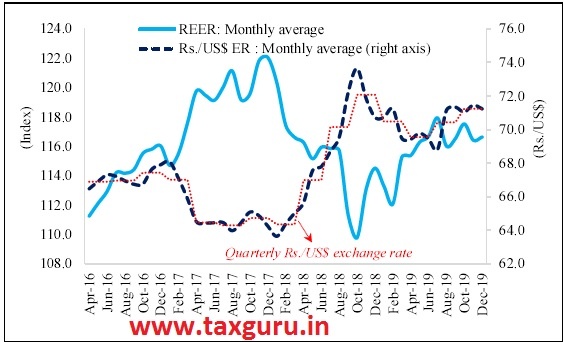

1.28 The contraction in import bill was partly contributed by a decline in oil prices in the current year as compared to 2018-19 (Figure 17), while slower contraction of exports may have resulted from a pick-up in global activity. The depreciation of real exchange rate since July 2019 may have been supportive of resurgence in India’s exports (Figure 18), though the evidence for exchange rate depreciation contributing to exports seems tenuous (Volume 1, Chapter 5).

1.29 Despite muted growth of services exports, the trade balance on the services account continued to be positive in 2019-20. The trade surplus on services account has been estimated at US$ 40.5 billion in H1 of 2019-20 (Figure 19), as compared to US$ 38.9 billion in 2018-19.

Figure 16: Growth of merchandise exports and imports

Data Source: Department of Commerce, Ministry of Commerce and Industry

Figure 17: Crude oil prices (Indian Basket) – US$ per barrel

Data Source: Petroleum Planning and Analysis Cell

Figure 18: Exchange Rate of Indian Rupee

Data Source: RBI

Note: REER refers to Real Effective Exchange Rate (36 currency trade weights)

Figure 19: Growth of services exports and imports

Data Source: RBI

Figure 20: Current Account Deficit as percentage of GDP

Data Source: RBI

1.30 Lower Current Account Deficit (CAD) reflects reduced external indebtedness of the country making domestic economic policy increasingly independent of external influence. The CAD, which was 2.1 per cent of GDP in 2018-19, has improved to 1.5 per cent in H1 of 2019-20 on the back of significant reduction in trade deficit (Figure 20).

1.31 Foreign Direct Investment (FDI) provides a more stable source of financing the CAD as compared to external borrowings. During 2014-19, gross FDI to India has been robust as compared to the previous five years; the trend has continued in 2019-20 as well (Figure 21). In the first eight months of 2019-20, both gross and net FDI flows to the country have been more than the flows received in corresponding period of 2018-19. Net FPI inflow in H1 of 2019-20 was also robust at US$ 7.3 billion as against an outflow of US$ 7.9 billion in H1 of 2018-19 (Figure 22).

Figure 21: Net annual FDI inflows

Data Source: RBI’s monthly bulletins

Figure 22: Quarterly trends in capital inflows

Data Source: RBI

1.32 Consequent to the improvement in current account and higher capital flows into the country, the Balance of Payments (BoP) position of the country has improved from foreign exchange reserves of US$ 302 billion in end March, 2019 to US$ 461.2 billion as on 10th January 2020.

Sectoral developments

1.33 Resources move across sectors in response to changes in relative prices causing different sectors of the economy to grow at different rates. A high growth of GDP does not attract much attention to sectoral contribution to growth as much as low growth of GDP does. Yet, at all levels of growth, structural change is imminent and it is the pace of change that becomes a matter of interest (Table 5).

1.34 Share of agriculture and allied sectors in the total GVA of the country has declined from 2009-14 to 2014-19 mainly on account of relatively higher growth performance of tertiary sectors. This is a natural outcome of the development process that leads to faster growth of non-agricultural sectors.

Table 5: Sectoral shares in GVA (per cent)

| 2009-10 to 2013-14 | 2014-15 to 2018-19 | 2018-19 | H1: 2019-20 | |

| Agriculture, forestry & fishing | 18.3 | 17.4 | 16.1 | 13.9 |

| Industry | 32.3 | 29.6 | 29.6 | 28.3 |

| Mining & Quarrying | 3.2 | 2.4 | 2.4 | 2.1 |

| Manufacturing | 17.5 | 16.6 | 16.4 | 15.4 |

| Electricity, Gas, Water supply & other utility services | 2.4 | 2.6 | 2.8 | 2.9 |

| Construction | 9.2 | 8.0 | 8.0 | 8.0 |

| Services | 49.4 | 52.9 | 54.3 | 57.8 |

| Trade, Hotel, Transport, Storage, Communication and services related to broadcasting | 17.5 | 18.3 | 18.3 | 18.1 |

| Financial, Real estate & Professional services | 19.2 | 20.9 | 21.3 | 24.5 |

| Public Administration, Defence and other services | 12.7 | 13.7 | 14.7 | 15.2 |

Source: National Statistical Office

1.35 The contribution of industrial activities to GVA has also declined from 2009-14 to 2014-19. Manufacturing sector, which contributes more than 50 per cent of industrial GVA, has driven the decline while the share of construction sector has also moderated.

1.36 Services sector has moved ahead faster, distancing itself further from agriculture and industry. Financial, real estate and professional services has driven the increase in the contribution of service sector followed by public administration. Even globally, the services sector has supported global growth partly offsetting the decline in manufacturing activity.

FIRST ADVANCE ESTIMATES: 2019-20

1.37 As per First Advance Estimates, growth in real GDP during 2019-20 is estimated at 5.0 per cent, as compared to the growth rate of 6.8 per cent in 2018-19. The nominal GDP is estimated at ` 204.4 lakh crore in 2019-20 with a growth of 7.5 per cent over the provisional estimates of GDP (` 190.1 lakh crore) for 2018-19.

1.38 The contribution of total consumption and net exports in GDP at current prices are estimated to increase in 2019-20 vis-à-vis 2018-19. Fixed investment as percentage of GDP at current prices is estimated to be 28.1 per cent in 2019-20, lower as compared to 29.3 per cent in 2018-19 (Table 6).

Table 6: Demand side components (as per cent of GDP)

| 2017-18 | 2018-19 | 2019-20 | Percentage points change in share in 2019-20 over 2018-19[Increase (+)/ Decrease (-)] | |

| 1st RE | PE | 1st AE | ||

| Total consumption | 70.0 | 70.6 | 72.1 | 1.5 |

| Government consumption | 11.0 | 11.2 | 11.9 | 0.7 |

| Private consumption | 59.0 | 59.4 | 60.2 | 0.8 |

| Gross Fixed Capital Formation | 28.6 | 29.3 | 28.1 | -1.2 |

| Net exports | -3.2 | -3.9 | -2.8 | 1.1 |

| Exports of goods & services | 18.8 | 19.7 | 18.4 | -1.3 |

| Imports of goods & services | 22.0 | 23.6 | 21.2 | -2.4 |

Source: National Statistical Office

Note: RE – Revised Estimate, PE – Provisional Estimate, AE – Advance Estimate

Table 7: Growth of GVA and GDP at constant (2011-12) prices (per cent)

| 2017-18 | 2018-19 | 2019-20 | Percentage points Change in growth in 2019-20 over 2018-19 [Increase (+)/ Decrease (-)] | |

| 1st RE | PE | 1st AE | ||

| GVA at basic prices | 6.9 | 6.6 | 4.9 | -1.7 |

| Agriculture & Allied Sectors | 5.0 | 2.9 | 2.8 | -0.1 |

| Industry | 5.9 | 6.9 | 2.5 | -4.4 |

| Mining & quarrying | 5.1 | 1.3 | 1.5 | 0.2 |

| Manufacturing | 5.9 | 6.9 | 2.0 | -5.0 |

| Electricity, Gas, Water supply & other utility services | 8.6 | 7.0 | 5.4 | -1.6 |

| Construction | 5.6 | 8.7 | 3.2 | -5.6 |

| Services | 8.1 | 7.5 | 6.9 | -0.7 |

| Trade, hotel, transport, communication and services related to broadcasting | 7.8 | 6.9 | 5.9 | -1.0 |

| Financial, real estate & professional services | 6.2 | 7.4 | 6.4 | -1.1 |

| Public administration, defence and other services | 11.9 | 8.6 | 9.1 | 0.5 |

| GDP at market prices | 7.2 | 6.8 | 5.0 | -1.8 |

Source: National Statistical Office

Note: RE – Revised Estimates, PE – Provisional Estimates, AE – Advance Estimates

1.39 Growth of real GVA at basic prices is estimated at 4.9 per cent in 2019-20, as compared to 6.6 per cent in 2018-19. Deceleration in GVA growth is estimated across all subsec-tors except ‘Public administration, defence and other services’ (Table 7).

1.40 Key indicators of the economy are reflected in Table 8. Given a 4.8 per cent real GDP growth in H1 of 2019-20, the first Advance Estimates imply that growth in H2 of 2019-20 will witness an uptick over H1 of 2019-20. The following developments suggest why it may be so:

First, NIFTY India Consumption Index picked up for the first time this year with a positive year-on-year growth of 10.1 per cent in October 2019 as compared to negative growth in the previous months. The growth continues to remain positive at 5.7 per cent in November 2019 and 0.2 per cent in December 2019.

Second, reinstating the positive confidence in Indian economy the secondary market continues to be upbeat and the BSE Sensex increased by 7.0 per cent (up to 31st December 2019) over end March 2019.

Third, foreign investors continue to show confidence in India. The country has attracted a net FDI of US$ 24.4 billion in April-November of 2019-20 as compared to US$ 21.2 billion in April-November of 2018-19. Net FPI inflow in April-November 2019-20 was positive at US$ 12.6 billion as against an outflow of US$ 8.7 billion in April-November 2018-19.

Table 8 : Key Indicators

| Data categories | Unit | 2016-17 | 2017-18 | 2018-19 | 2019-20 |

| GDP and Related Indicators | |||||

| GDP at current market prices | Rs. lakh Crore | 153.6 | 171.0 | 190.1a | 204.4b |

| GDP at constant market prices | Rs. lakh Crore | 123.0 | 131.8 | 140.8a | 147.8b |

| Growth Rate | (per cent) | 8.2 | 7.2 | 6.8a | 5.0b |

| GVA at current basic prices | Rs. lakh Crore | 139.2 | 154.8 | 172.0a | 185.0b |

| GVA at constant basic prices | Rs. lakh Crore | 113.2 | 121.0 | 129.1a | 135.4b |

| Growth Rate | (per cent) | 7.9 | 6.9 | 6.6a | 4.9b |

| Gross Savings | % of GDP | 30.3 | 30.5 | Na | na |

| Gross Capital Formation | % of GDP | 30.9 | 32.3 | Na | Na |

| Per Capita Net National Income (at current prices) | Rs. | 104659 | 114958 | 126406a | 135050b |

| Production | |||||

| Food grains | Million tonnes | 275.1 | 285.0 | 285.0c | 14.6c |

| Index of Industrial Production (growth) | (per cent) | 4.6 | 4.4 | 3.8 | 0.6d |

| Electricity Generation (growth) | (per cent) | 4.7 | 4.0 | 3.5 | 03.d |

| Prices | |||||

| WPI inflation (average) | (per cent) | 1.7 | 3.0 | 4.3 | 1.5e |

| CPI (Combined) inflation (average) | (per cent) | 4.5 | 3.6 | 3.4 | 4.1e |

| External Sector | |||||

| Merchandise export growth (in US$ term) | (per cent) | 5.2 | 10.0 | 8.8 | -2.0e |

| Merchandise import growth (in US$ term) | (per cent) | 0.9 | 21.1 | 10.4 | -8.9e |

| Current Account Balance | % of GDP | -0.6 | -1.8 | -2.1 | 1.5r |

| Foreign Exchange Reserves (end of year) | US$ Billion | 370.0 | 424.5 | 412.9 | 457.5j |

| Average Exchange Rate | Rs./ US$ | 67.1 | 64.5 | 69.9 | 70.4e |

| Money and Credit | |||||

| Broad Money (M3) growth (annual) | (per cent) | 10.1 | 9.2 | 10.5 | 9.8g |

| Scheduled Commercial Bank Credit (growth) | (per cent) | 8.2 | 10.0 | 13.3 | 7.2g |

–

| Data categories | Unit | 2016-17 | 2017-18 | 2018-19 | 2019-20 |

| Fiscal Indicators (Centre) | |||||

| Gross Fiscal Deficit | % of GDP | 3.5 | 3.5 | 3.4h | 3.3i |

| Revenue Deficit | % of GDP | 2.1 | 2.6 | 2.2h | 2.3i |

| Primary Deficit | % of GDP | 0.4 | 0.4 | 0.2h | 0.2i |

Notes: Na: Not available,

a: Provisional estimates, b: First advance estimate, c: Fouth AE for 2018-19 and first AE for 2019-20, d: (April-November) 2019, e: (April-December) 2019, f: (April-September) 2019, g: November 2019, h: Revised Estimate, i. Budget Estimate, j. End of December 2019

Fourth, the lagged effect of previous cuts in the repo rate is showing up in the build-up of demand pressure. CPI-core inflation has risen from 3.4 per cent in October 2019 to 3.6 per cent in November 2019 and further to 3.8 per cent in December 2019. WPI Inflation has also been rising from zero per cent in October 2019 to 0.6 per cent in November 2019 and 2.6 per cent in December 2019.

Fifth, the terms of trade for farmers has been improving and will lead to increase in rural consumption. Food inflation since April 2019 has been rising.

Sixth, industrial activity is on a rebound and is showing signs of pick up. IIP in November 2019 has registered a growth of 1.8 per cent as compared to a contraction by 3.4 per cent in October 2019 and by 4.3 per cent in September 2019. Along with IIP, growth of eight core industries is also showing signs of recovery by registering a smaller contraction of 1.5 per cent in November 2019 as compared to a contraction of 5.8 per cent in October 2019. This is consistent with business cycle.

Seventh, PMI Manufacturing has registered a steady improvement increasing from 50.6 in October 2019 to 51.2 and 52.7 in November 2019 and December 2019 respectively. PMI Services has also increased from 49.2 in October 2019 to 52.7 in November 2019 and further to 53.3 in December 2019.

Eighth, growth in merchandize exports has been improving as reflected in a contraction by 0.8 percent in Q3 2019-20 which was smaller as compared to a contraction by 3.7 per cent in Q2 2019-20. Accordingly inducement of exports to GDP growth is expected to increase. As per first Advance Estimates of 2019-20, contribution of net exports to the growth of GDP is estimated to increase by 1.1 percentage points over 2018-19.

Ninth, forex reserves have built up from US$ 413 billion in end March 2019 to US$ 461.2 billion as on 10th January, 2020 reflective of increasing confidence of overseas investors in India’s economy.

Tenth, the gross GST revenue collected in the month of December 2019 and November 2019 registered a positive growth rate of 9 per cent and 6 per cent respectively over the corresponding month of the previous year after registering negative growth rates in September and October 2019. During April-December 2019, the gross GST revenue collected has surpassed ` 1 lakh crore five times, pointing towards an increased economic activity overall.

THE RECENT GROWTH DECELERATION: DRAG OF THE FINANCIAL SECTOR ON THE REAL SECTOR

The Slowing Cycle of growth

1.41 The Economic Survey, 2018-19 describes the virtuous cycle of growth wherein increase in the rate of fixed investment accelerates the growth of GDP that in turn induces a higher growth in consumption. Higher growth of consumption improves the investment outlook, which results in still higher growth of fixed investment that further accelerates the growth of GDP, inducing a still higher growth of consumption. This virtuous cycle of higher fixed investment-higher GDP growth-higher consumption growth (Figure 23) generates economic development in the country.

Figure 23: Virtuous cycle of growth

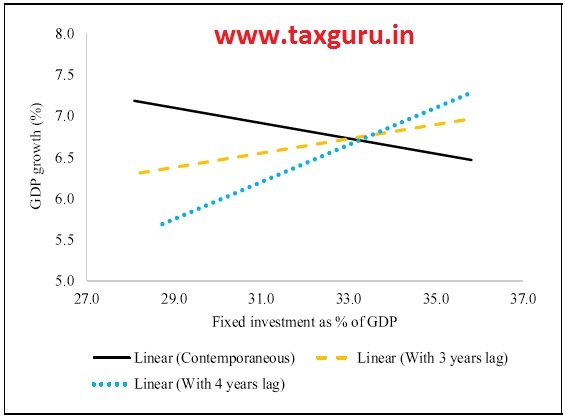

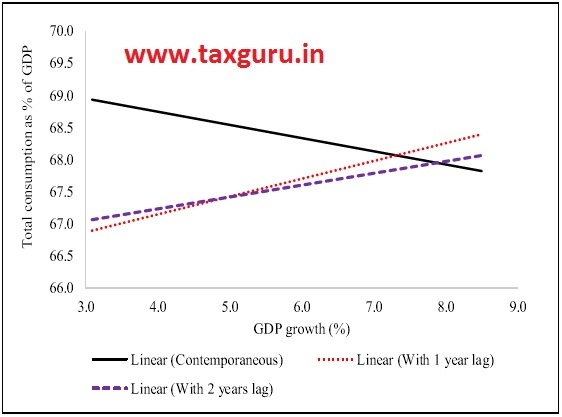

1.42 Conversely, when this virtuous cycle rotates slowly, declining rate of fixed investment decelerates GDP growth with a lag, which eventually causes a deceleration in the growth of consumption as well. In case of India, the lag between rate of fixed investment and its impact on GDP growth is seen to be of three to four years (Figure 24). Similarly, the impact of GDP growth on consumption growth gets reflected in one to two years (Figure 25). Therefore, a contemporaneous comparison of trends of GDP growth and investment is not appropriate, given the negative correlation seen between the two.

1.43 The Indian economy, since 2011-12, has been under the influence of slowing

Figure 24: Lagged effect of Investment on growth (2004-2019)

Data Source: National Statistical Office

Figure 25: Lagged effect of growth on Consumption (2004-2019)

Data Source: National Statistical Office

Figure 26: Real GDP growth and Investment – Annual movement

Data Source: National Statistical Office cycle of growth. The fixed investment rate has started declining sharply since 201112 and subsequently plateaued from 2016-17 onwards. Given the lagged impact of the investment rate on GDP growth shown in Figure 24 (with the effect being most pronounced after four years), the deceleration in growth since 2017-18 is consistent with the framework described here (Figure 26).

Decline in fixed investment rate

1.44 The drop in fixed investment by households from 14.3 per cent to 10.5 per cent explains most of the decline in overall fixed investment between 2009-14 to 201419 (Figure 27). Fixed investment in the public sector marginally decreased from 7.2 per cent of GDP to 7.1 per cent during the two

Figure 27: Fixed investment by institutional sector (as per cent of GDP)

Data Source: National Statistical Office periods. However, the stagnation in private corporate investment at approximately 11.5 per cent of GDP between 2011-12 to 201718 has a critical role to play in explaining the slowing cycle of growth and, in particular, the recent deceleration of GDP and consumption.

Drag of financial sector on private corporate investment

1.45 To make sense of the decline in corporate investment when it stems from issues related to the financial sector, we must understand the boom in credit (Mian and Sufi, 2018). It is now well recognized that a sudden credit expansion, which is purely supply led, results in short lived expansion of output and employment but causes significant contraction in the long run. The International Monetary Fund (2017) finds this relationship for 80 countries. In most of these cases, the credit channel works through household debt where households increase demand using debt in the short run and reduce demand later during the deleveraging phase, thereby, resulting in recessions.

1.46 In the Indian context, the credit channel has worked through corporate investment.The bust following the boom was characterized by deleveraging and low investment rate in the corporate sector, eventually causing the recent deceleration of GDP growth. Here, it may be useful to ask if the origins of slowing cycle of growth lie in the enormous lending boom of the mid and late 2000s when nonfood bank credit almost tripled between 2003-04 to 2007-08 and doubled between 2007-08 to 2011-12. Is it possible that this excessive bank lending, driven by the irrational exuberance of the boom period, led to a decline in corporate investments in the future?

1.47 To provide careful evidence on this phenomenon, the relationship between credit expansion by a firm and its future investment is examined. Following the methodology used in Mian & Sufi (2018), the data is organized at firm-year level. For any firm year t, the dependent variable is the growth in investments from year t to t+4 and the explanatory variable is the credit expansion during t-5 to t-1. For instance, in the year 2012, investment growth is the log of difference in fixed assets between 2011-12 and 2015-16 while credit expansion is the difference in the debt to total assets ratio between 200607 and 2010-11. For each of the five firm-years (2011 to 2015), the dependent variable is regressed on the explanatory variable across a cross-section of firms. The statistical significance of the relationship between the two is tabulated below (Table 9).

1.48 Crucially, we note that for the year 2013, the relationship is both negative and statistically significant. This implies that firms that excessively borrowed between 2007-08 to 2011-12 actually ended up investing significantly less during 2012-13 to 2016-2017. As this result is statistically not significant for any other five-year periods, the year 2013 becomes pivotal in explaining the impact of credit exuberance on investment. In fact, the year 2013 being pivotal in the analysis above matches exactly with the fall in investment rate at the macro level seen in Figure 26.

Table 9 : Relationship between credit expansion and investment

| Firm Year | Credit Expansion (Increase in debt/assets ratio) |

Investment (Growth in Fixed Assets) | Relationship |

| 2011 | 2006-10 | 2011-15 | Not Significant |

| 2012 | 2007-11 | 2012-16 | Not Significant |

| 2013 | 2008-12 | 2013-17 | Significant and Negative |

| 2014 | 2009-13 | 2014-18 | Not Significant |

| 2015 | 2010-14 | 2015-19 | Not Significant |

1.49 The year 2007-08 when firms started to borrow excessively coincides with the year in which RBI extended regulatory forbearance to almost all loans (RBI, Prudential Guidelines on Restructuring of Advances by Banks, August 27, 2008). It appears that the firms that were beneficiaries of excess lending, facilitated by regulatory forbearance, seem to have cut down investment the most. Perhaps, the beneficiary firms were the ones that were more focused at de-leveraging, owing to their higher debt to asset ratio, than investing in new assets.

1.50 Post the credit boom, the credit growth of banks also started to slow down. Growth (CAGR) of non-food credit for Scheduled Commercial Banks’ (SCBs) fell from 16.7 per cent in 2009-14 to 10.5 per cent in 2014-19. The decline in the growth of non-food SCB credit followed a rise in the Non- Performing Assets (NPA) of banks from an average of 3.0 per cent of gross advances in 2009-14 to 8.3 per cent in 2014-19. Bank credit growth (CAGR) to large units, MSMEs, infrastructure and even Non-Banking Financial Companies (NBFCs) significantly fell in 2014-19 as compared to 2009-14 (Figure 28).

Decline in household investment

1.51 The household sector includes family households as well as ‘quasi-corporates’.

Figure 28: Credit growth (CAGR) across sectors

Data Source: RBI

Figure 29: Household Fixed investment by asset (as percentage of GDP)

Data Source: National Statistical Office

Unincorporated enterprises belonging to households, which have complete sets of accounts, are called ‘quasi-corporates’. A break-down of household sector investment shows that investment in the groups ‘Machinery and equipment’ and ‘Dwellings, other buildings and Structures’ together account for more than two-thirds of total household sector investment.

1.52 Unincorporated household enterprises, in addition to supplying directly for retail consumption, are also suppliers to incorporated enterprises from the back end of the value chain. The stagnation in machinery and equipment investment of households at around 2.4 per cent of GDP, from 2011-12 to 2017-18 (Figure 29), can possibly be linked with the leveling of private corporate investment during the same period.

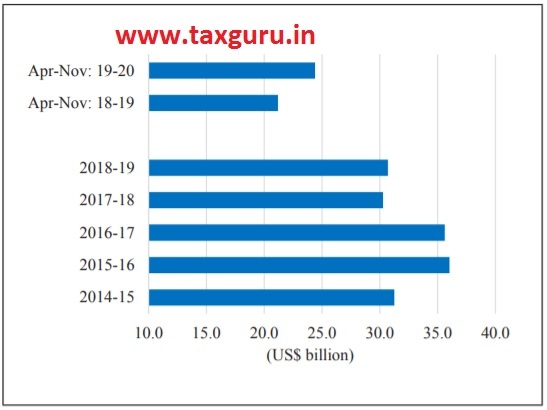

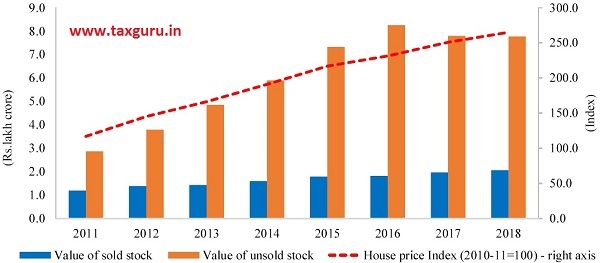

1.53 The decline in household investment in ‘Dwellings, other buildings and Structures’, over 2011-12 to 2017-18 is a reflection of slower growth in purchase of houses by households. The real estate sector, and residential property in particular, has been reeling with issues of delayed project deliveries and stalled projects leading to a build-up of unsold inventory over the years.

Housing prices have remained elevated, even though growth in prices has fallen sharply since Q1 of 2015-16 and remained muted since then. As at end of December 2018, about 9.43 lakh units worth ` 7.77 lakh crore with 41 months of inventory are stuck in various stages of the project cycle across top 8 cities (Figure 30).

Figure 30: Housing unsold inventory, sales and price index

Data Source: Liases Foras (2019), RBI

Note: Years here are calendar years.

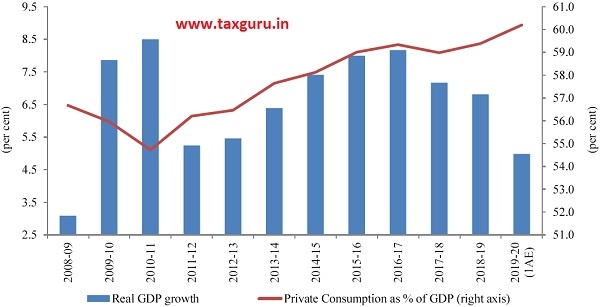

Figure 31: Real GDP growth and Private consumption (as percentage of GDP) Annual movement

Data Source: National Statistical Office

Delayed decline in private consumption

1.54 Private consumption increased as a proportion of GDP from 2009-16, particularly in 2014-16 (Figure 31). Thereafter, it declined in 2017-18 and rose again in 201819, before declining sharply in H1 of 201920. As shown in Figure 25, the effect of GDP growth on consumption manifests after a lag of 1-2 years. Therefore, the declining trend in consumption from 2017-18 reflects partly the effect of decline in GDP growth on consumption.

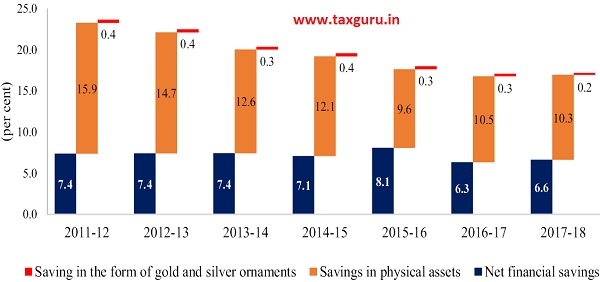

Figure 32: Household savings by asset type (as percentage of GDP)

Data source: National Statistical Office

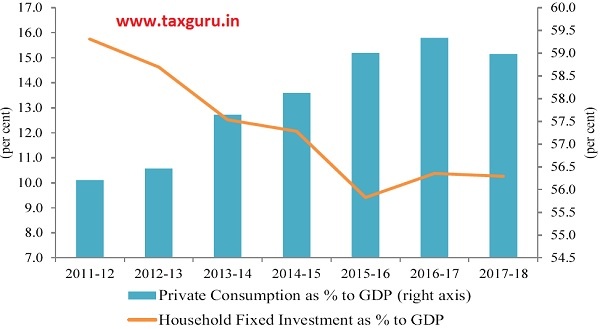

Figure 33: Household fixed investment and Private Consumption (as percentage of GDP)

Data source: National Statistical Office

1.55 Change in household investment contributed to increasing consumption in the period until 2016-17 (Figure 33). A drop in savings in physical assets of households has been observed over this period (Figure 32). Income not saved in physical assets by households is either saved in the form of valuables (gold or silver) or as net household financial savings or is consumed. During 2011-12 to 2016-17, when savings in physical assets dropped, neither savings in gold and silver by households nor net household financial savings rose as a proportion of GDP. Thus, it appears that resources not deployed by households in physical assets 2011-12 onwards were mostly expended on consumption.

OUTLOOK

1.56 The IMF in its January 2020 update of World Economic Outlook has projected India’s real GDP to grow at 5.8 per cent in 2020-21. World Bank in its January 2020 issue of Global Economic Prospects also sees India’s real GDP growing at 5.8 per cent in 2020-21.

1.57 Based on the first Advance Estimates of India’s real GDP growth in 2019-20, an uptick in GDP growth in H2 of 2019-20 is expected as compared to first half of the same year. With a view to making an assessment of the likely growth in GDP, both the downside and upside risks to an expected acceleration in GDP growth are discussed below.

Downside Risks

- Continued global trade tensions could delay the recovery in the growth of global output, which may constrain the export performance of the country. Weaker export growth may reduce the inducement to increase the fixed investment rate in the economy.

- Escalation in US-Iran geo-political tensions may increase the price of crude oil and depreciate the Net FPI inflows may weaken, as a result, adding further pressure on the rupee to depreciate. If a fuller pass-through of the costlier crude oil is allowed, it may fuel inflationary pressure in the economy, cause the growth of private consumption to decline and weaken the inducement to invest. Even if a partial pass-through happens, fiscal deficit may swell, may increase the yield on G-sec and thereby, increase the cost of capital that may again weaken the inducement to invest.

- Growth in advanced countries has weakened with very low inflation. The conventional monetary policy has almost run its full course. Subsequently, quantitative easing may fuel inflation and reduce the real interest rate. At some point in future, if short-term interest rates are raised by the central banks to contain inflation, it may result in capital flight from emerging and developing market economies (EMEs) including India. The rupee may come under pressure making imports costlier. Leakage from the domestic circular flow of income may increase which may adversely impact private consumption and investment. If instead, fiscal expansion is the preferred policy option in advanced countries, increase in short-term interest rates may happen all the more earlier and weaken the growth impulse in EMEs including India.

- The implementation of IBC Code is making progress, albeit slowly. Unless this speeds up, the risk aversion of banks to lend further may not reduce. Risk premiums may then continue to be high and cuts in repo rates may not transmit to lowering lending rates. Private investment may, therefore, remain muted.

- Investment in the public sector may increase, as is expected after the announcement of the National Infrastructure Pipeline (NIP) of projects worth ` 102 lakh crore. If this leads to expansion of fiscal deficit, bond yields may increase, thereby, possibly crowding out private investment. If instead private investment seeks external funding, CAD would widen and depreciate the rupee, bringing in its wake the adverse impact on consumption, investment and growth.

- Should productivity gains not significantly increase with reforms, it may raise the requirement of fixed investment rate to boost economic growth.

- A non-rising gross domestic savings rate may further deteriorate the CAD, depreciate the rupee and make the virtuous cycle more difficult to realize.

Upside Risks

- There are tentative signs that manufacturing activity and global trade are bottoming out. This may positively impact India’s exports. At the same time, there is renewed initiative to boost exports through various reform measures including scaling up of logistics infrastructure that may increase export competitiveness.

- Government’s thrust on affordable housing is evident, in order to boost the real estate sector and consequently the construction activity in the country. Higher investment in housing by households may increase the fixed investment in the economy. Existing unsold housing inventory can be cleared and the balance sheets of both bank/ non-bank lenders cleaned if the real estate developers are willing to take a ‘hair-cut’ by allowing the house-prices to drop.

- Global sentiment continues to favor India as reflected in robust and rising inflows of net FDI into the country. Relocation of investors from other countries to India in the wake of trade tensions will also add to the flow. The announcement of NIP may further increase FDI inflows into the country in both brown-field and green-field infrastructure projects. Continuous relaxation of FDI guidelines may address the concerns of foreign investors and improve the investment climate.

- A boost to Make in India may not only enhance exports but replace imports of products in which India has sufficient scope for expansion in domestic manufacturing.

- India has been making steady progress in improving its rank in the Ease of Doing Business, assessedforabout 190 countries by the World Bank. Earlier the rank had improved with the implementation of GST. Lately the improvement in rank has resulted from progress in trade facilitation as cross-border movement of goods has involved lesser waiting time. As the implementation of GST further settles down, the increased unification of the domestic market may reduce business costs and facilitate fresh investment. Reforms in land and labor market may further reduce business costs.

- Reduction in the base corporate tax rate to 15 per cent for new manufacturing companies may increase the rate of return on investment above the hurdle rate of the cost of capital and encourage a surge in new investments.

- Merger of public sector banks may increase the financial strength of the merged entities, lower the risk aversion and result in lowering of lending rates.

Projection of GDP growth in 2020-21

1.58 On a net assessment, it appears that the upside risks should prevail, particularly when the government, with a strong mandate, has the capacity to deliver expeditiously on reforms. GDP growth of India should strongly rebound in 2020-21 and more so on a low statistical base of 5 per cent growth in 2019-20.

1.59 On a net assessment of both the downside/upside risks, India’s GDP growth is expected to grow in the range of 6.0 to 6.5 per cent in 2020-21.

CHAPTER AT A GLANCE

> The year 2019 was a difficult year for the global economy with world output growth estimated to grow at its slowest pace of 2.9 per cent since the global financial crisis of 2009, declining from a subdued 3.6 per cent in 2018 and 3.8 per cent in 2017.

> Amidst a weak environment for global manufacturing, trade and demand, the Indian economy slowed down with GDP growth moderating to 4.8 per cent in H1 of 2019-20, lower than 6.2 per cent in H2 of 2018-19.

> A sharp decline in real fixed investment induced by a sluggish growth of real consumption has weighed down GDP growth from H2 of 2018-19 to H1 of 2019-20. Real consumption growth, however, has recovered in Q2 of 2019-20, cushioned by a significant growth in government final consumption.

> On the supply side, the deceleration in GVA growth has been contributed generally by all sectors save ‘Agriculture and allied activities’ and ‘Public administration, defence, and other services’, whose growth in H1 of 2019-20 was higher than in H2 of 2018-19.

> India’s external sector gained further stability in H1 of 2019-20, with a narrowing of current account deficit (CAD) as percentage of GDP from 2.1 in 2018-19 to 1.5 in H1 of 2019-20, impressive foreign direct investment (FDI), rebounding of portfolio flows and accretion of foreign exchange reserves. Imports have contracted more sharply than exports in H1 of 2019-20, with easing of crude prices, which has mainly driven the narrowing of CAD.

> Headline inflation rose from 3.3 per cent in H1 of 2019-20 to 7.35 per cent in December 2019-20 on the back of temporary increase in food inflation, which is expected to decline by year end. Rise in CPI-core and WPI inflation in December 2019-20 suggests building of demand pressure.

> The deceleration in GDP growth can be understood within the framework of a slowing cycle of growth. The financial sector acted as a drag on the real sector: investment-growth-consumption, as described in the Economic Survey of 2018-19.

> In an attempt to boost investment, consumption and exports, the government in 2019-20 has taken important reforms towards speeding up the insolvency resolution process under Insolvency and Bankruptcy Code (IBC), easing of credit, particularly for the stressed real estate and NBFC sectors, and announcing the National Infrastructure Pipeline 2019-2025 amongst other measures.

> Based on CSO’s first Advance Estimates of India’s GDP growth for 2019-20 at 5 percent, an uptick in GDP growth is expected in H2 of 2019-20. The government must use its strong mandate to deliver expeditiously on reforms, which will enable the economy to strongly rebound in 2020-21.

REFERENCES

International Monetary Fund. 2017. “Household Debt And Financial Stability”, Chapter 2 in Global Financial Stability Report, October 2017: Is Growth at Risk. IMF

Mian, Atif. and Amir Sufi. 2018. “Finance and business cycles: the credit-driven household demand channel,” Journal of Economic Perspectives, 32(3), 31-58.

Pandey, Radhika, Ila Patnaik, and Ajay Shah. 2018. “Measuring business cycle conditions in India.” Working Papers 18/221, National Institute of Public Finance and Policy. https:// nipfp.org.in/media/medialibrary/2018/04/ WP_221.pdf

“White Paper February 2019,” Liases Foras, accessed January 10 2020, https://www. liasesforas.com/admin/WhitePaper/36/ WhitePaper_2019-05-02_63692396967411. pdf

ANNEX

RECENT REFORMS

Government in 2019-20 has taken important reforms to boost the overall investment, consumption and exports in the economy. Some of the major reforms in this regard are as enumerated below:

Measures to Boost Investment

- In December 2019, Cabinet approved the Insolvency and Bankruptcy Code (Second Amendment) Bill, 2019. The amendments aim at fast-tracking the insolvency resolution process and to further improve the ease of doing business.

- On 31st December 2019, the government released the Report of the Task Force on National Infrastructure Pipeline (NIP) for each of the years from 2019-20 to 2024-25. The report has submitted proposals for projects whose aggregate value is estimated at ` 102 lakh crore.

- Government has brought in Taxation Laws (Amendment) Ordinance 2019 to make certain amendments in the Income-tax Act 1961 and the Finance (No. 2) Act 2019.

(i) A new provision has been inserted in the Income-tax Act with effect from 2019-20 which allows any domestic company an option to pay income-tax at the rate of 22 per cent subject to condition that they will not avail any exemption/incentive. The effective tax rate for these companies shall be 25.17 per cent inclusive of surcharge & cess. Also, such companies shall not be required to pay Minimum Alternate Tax.

(ii) In order to attract fresh investment in manufacturing and thereby boost the ‘Make-in-India’ initiative of the Government, a new provision has been inserted in the Income-tax Act with effect from 2019-20 which allows any new domestic company incorporated on or after 1st October 2019 making fresh investment in manufacturing, an option to pay income-tax at the rate of 15 per cent. This benefit is available to companies which do not avail any exemption/incentive and commences their production on or before 31st March, 2023. The effective tax rate for these companies shall be 17.01 per cent inclusive of surcharge & cess. Also, such companies shall not be required to pay Minimum Alternate Tax. Corporate income tax rates in India are now amongst the lowest in the world.

- Rapid growth requires rapid investment which in turn is dependent on robust supply of credit. Government has taken notable steps in this regard:

(i) Budget 2019-20 announced an infusion of Rs. 70,000 crore into Public Sector Banks (PSBs) to boost credit and investment in the economy. As of November 2019, Rs. 60,314 crore has been infused from this provision, thereby, equipping banks for growth and investment.

(ii) Strong banks are imperative to achieve a US$ 5 trillion economy. Along with numerous governance reforms, government has proposed an amalgamation of 10 PSBs to form 4 merged entities with a view to create next generation banks with strong national presence and global reach. Operational efficiency gains arising due to this consolidation are expected to reduce the cost of lending.

(iii) The Monetary Policy Committee of RBI changed its stance from calibrated tightening to neutral in February 2019 and to accommodative from June 2019 onwards. Accordingly, the policy rate has been reduced by 135 bps since February 2019.

(iv) In order to enhance debt flow to housing and infrastructure projects, government has proposed to establish an organization, Credit Enhancement for Infrastructure and Housing Projects.

(v) As per RBI, all new floating rate retail loans and floating rate loans to micro and small enterprises extended by banks with effect from 1st October 2019 are to be linked to one of the specified external benchmarks. These benchmarks consist of the policy repo rate, Government of India 3-months or 6-months Treasury Bill yields, or any other benchmark indicated by the Financial Benchmarks India Private Ltd (FBIL).

- Government has taken various measures to boost the growth of the auto sector:

(i) one-time registration fees being deferred till June 2020,

(ii) BS IV vehicles purchased till 31st March 2020 to remain operational for entire period of registration

(iii) additional 15 per cent depreciation on all vehicles to increase to 30 per cent acquired during the period from now till 31st March 2020,

(iv) both Electrical Vehicles (EVs) and Internal Combustion Vehicles (ICVs) will continue to be registered and,

(v) to boost demand, government will lift the ban on replacing old vehicles with purchage of new vehicles by Goverment Departments.

- In December 2019, modifications to the MSME Interest Subvention Scheme were approved to further smoothen operational difficulties and to improve access to credit at a reduced cost.

- Government has approved creation and launch of Bharat Bond Exchange Traded Fund (ETF) to create an additional source of funding for Central Public Sector Undertakings (CPSUs), Central Public Sector Enterprises (CPSEs), Central Public Financial Institutions (CPFIs) and other government organizations. Bharat Bond ETF would be the first corporate bond ETF in the country.

- With a view to boosting the realty sector and incentivising the consumers to buy houses, the government has taken some notable measures

(i) Government has approved the establishment of a ‘Special Window’ fund to provide priority debt financing for the completion of stalled housing projects that are in the ‘Affordable and Middle-Income’ Housing sector. For the purpose of the fund, government shall act as the Sponsor and the total commitment to be infused by the government would be upto Rs. 10,000 crores. The fund is seeking matching contributions from banks, LIC and others to generate a total corpus of around Rs. 25,000 crore. The fund will be set up as a Category-II AIF (Alternate Investment Fund) debt fund registered with SEBI and would be run professionally.

(ii) Eligible beneficiaries of Pradhan Mantri Awas Yojana (Gramin) are to be provided 1.95 crore houses with amenities like toilets, electricity and LPG connections during its second phase (2019-20 to 2021-22).

(iii) External Commercial Borrowings (ECB) guidelines will be relaxed to facilitate financing of home buyers who are eligible under the Pradhan Mantri Awas Yojana (PMAY), in consultation with RBI. This is in addition to the existing norms for ECB for affordable housing.

(iv) House Building Advance: The interest rate on House Building Advance shall be lowered and linked with the 10 Year G Sec Yields.

(v) Additional deduction up to Rs. 5 lakh for interest paid on loans borrowed up to 31st March, 2020 for purchase of house valued up to Rs. 45 lakh to promote affordable housing.

(vi) Banks to launch Repo rate /external benchmark linked loan products. Reduced EMI for housing loans by directly linking Repo rate to interest rates

(vii) Additional liquidity support to HFCs of ` 20,000 crore by National Housing Bank (NHB), thereby, increasing it to Rs. 30,000 crore.

- To guarantee support and enable NBFCs/Housing Finance Companies (HFCs) to resolve any temporary liquidity or cash flow mismatch issues, government has rolled out the ‘Partial Credit Guarantee Scheme’ for purchase of high-rated pooled assets from financially sound NBFCs / HFCs by PSBs. The amount of overall guarantee is limited to first loss of up to 10 per cent of fair value of assets being purchased by the banks under the Scheme, or ` 10,000 crore, whichever is lower, as agreed by Department of Economic Affairs (DEA). The scheme would cover NBFCs / HFCs that may have slipped into SMA-0 category during the one-year period prior to 1st August 2018, and asset pools rated ‘BBB+’ or higher.

- The Stand Up India Scheme has been extended upto the year 2025. The Scheme aims to facilitate bank loans between ` 10 lakh to ` 100 lakh to atleast one Scheduled Caste (SC) or Scheduled Tribe (ST) borrower and atleast one woman borrower per bank branch for setting up a greenfield enterprise. In case of non-individual enterprises, at least 51 per cent of the shareholding and controlling stake should be held by either an SC/ST or woman entrepreneur.

- Government has put in place an investor friendly FDI policy by liberalizing the policy to allow upto 100 per cent FDI by automatic route on most of the sectors.

- To mitigate genuine difficulties of startups and their investors, Section 56(2)(viib) of the Income-Tax Act (regarding angel tax) will no longer be applicable to startups registered with DPIIT.

Measures to boost Consumption

Government has taken various measures to boost the incomes especially rural incomes to usher spending and consumption levels in the economy.

- Increase in the Minimum Support Prices (MSPs) for all mandated Rabi crops and Kharif crops for 2019-20 season.

- To provide an assured income support to the small and marginal farmers, the cash transfer scheme Pradhan Mantri Kisan Samman Nidhi (PM-KISAN) providing an income support of ` 6,000 per year has been extended to all eligible farmer families irrespective of the size of land holdings.

- With a move towards attaining universal social security, Government has approved a new scheme that offers pension coverage to the trading community. Under this scheme all shopkeepers, retail traders and self-employed persons are assured a minimum monthly pension of ` 3,000 per month after attaining the age of 60 years.

- e.f. 1st August 2019, GST rate on all electric vehicles has been reduced from 12 per cent to 5 per cent and of charger or charging stations for EVs from 18 per cent to 5 per cent . Hiring of electric buses (of carrying capacity of more than 12 passengers) by local authorities will be exempted from GST.

Measures to boost Exports

- The scheme for Remission of Duties or Taxes on Export Product (RoDTEP) will replace Merchandise Exports from India Scheme (MEIS) for reimbursement of taxes & duties for export promotion. Textiles and all other sectors which currently enjoy incentives upto 2 per cent over MEIS will transit into RoDTEP. In effect, RoDTEP will more than adequately incentivize exporters than existing schemes put together.

- Special Economic Zones (Amendment) Bill, 2019 has been approved wherein a trust or any entity notified by the Central Government will be eligible to be considered for grant of permission to set up a unit in Special Economic Zones.

- In order to boost credit to the export sector, RBI enhanced the sanctioned limit to be eligible under priority sector lending norms. The limit has been raised from ` 25 crore to ` 40 crore per borrower. Furthermore, the existing criterion of ‘units having turnover of up to ` 100 crore’ has been removed.

- Export Credit Guarantee Corporation (ECGC) will expand the scope of Export Credit Insurance Scheme (ECIS) to offer higher insurance cover to banks lending working capital for exports. This will enable reduction in overall cost of export credit including interest rates, especially to MSMEs

- Government has approved the Sugar export policy for evacuation of surplus stocks during sugar season 2019-20. This shall involve providing a lump sum export subsidy at the rate of ` 10,448 per Metric Tonne (MT) to sugar mills for the sugar season 2019-20. The total estimated expenditure of about ` 6,268 crore will be incurred for this purpose.

- For enabling handicrafts industry to effectively harness e-commerce for exports, mass enrolment of artisans across India will be effected in collaboration with Ministry of Textiles.

Note

1. Total merchandise exports of product categories under HS code 28 to 96 are considered as manufacturing exports.