For start-ups with little or no revenue and an uncertain future, assigning a valuation sounds vague. Business valuation of any kind is never cut and dry.

Since valuation is a complex issue, start-ups who raise seed capital (Initial Investment) can consider issuing convertible securities to investors where the conversion ratio for converting the same into Equity Stock need not be decided at the time of issue. However, it is to be decided when the company raises its next round of investments (Series-A Investment). This makes it very easy for start-ups to raise funds without having to worry about valuation.

Following forms of Convertible Securities can be evaluated to raise funds without worry about valuation:

> iSAFE Note

It is a kind of convertible security that can be used in early-stage capital raise. It is neither debt nor equity. It shall be converted into equity on occurrence of specified liquidity events like next pricing/valuation round, dissolution, merger/acquisition etc.

- It takes the legal form of compulsorily convertible preference shares (CCPS)

- Authorised and paid up capital will have to be increased by the extent of investment made under iSAFE note

- It doesn’t carry an interest rate and doesn’t have a maturity date

- It can be issued to anyone and for any sum of investment

- Convertible Notes – Debt Instrument

It is a type of short-term debt financing that is used in early-stage capital raise. In other words, Debt Notes are loans to early-stage start-ups from investors who are expecting to be paid back when their note comes due. But, instead of being paid back in principal with interest, as would be the case with a typical loan, the investor can be repaid in equity in your company.

- The company that wants to issue CN should be registered under Start-up India scheme

- It can be issued to foreign investors, NRI and resident Indians and Indian Companies

- Minimum amount to be invested in one tranche by one investor is Rs 25 lakhs

- The maximum tenure of CN should be 5 years. That means it should be converted into equity or should be repaid within 5 years of issue

- Unlike issuance of shares by private placement or preferential allotment, the procedure for issuance of a convertible note is comparatively easier. It can be carried out by way of a special resolution of existing shareholders at the General Meeting.

> Different components of Convertible Notes:

1. Discount: To be applied to the future valuation when it’s time to convert. Percentage of Discount can vary based on time duration to next round of investment.

For e.g. Discount rate be:

– 25% in case the investment round happens within 6 months

– 50% in case the investment round happens after 6 months

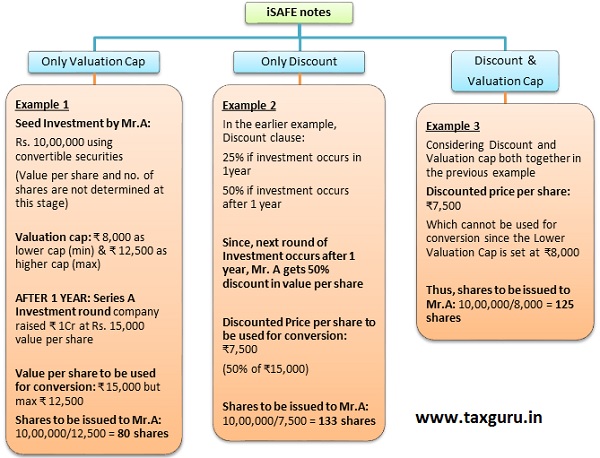

2. Valuation Cap: To set a limit as highest cap and lowest cap to the value per share that is to be used for conversion purpose.

3. Time Period: To set a definite time period by which conversion shall take place when iSAFE notes are issued.

For e.g. in case the next round of investments doesn’t occur by 2 years, seed Investments shall be automatically converted into equity shares using the mutually agreed value.

Thus, different types of Convertible Notes can be as follows:

- Discount, No Valuation Cap

- Valuation Cap, No Discount

- Discount and Valuation Cap

Let us understand the concept of Discount and Valuation Cap with an example:

Authors:

CA Shreyans Dedhia, Partner I’d – shreyans.dedhia@masd.co.in

Author Bio