Introduction :

Baghban was a Decent film released in the year 2003 which showcased the life of Retired Bank Manager beautifully essayed by Big B along with his onscreen wife essayed by Mrs Hema Malini who had spent all the money earned on raising their

( 3 +1) Male children who almost disown their parents at the time of Post retirement breaking their Hearts barring the adopted one , so today’s topic is to educate the concept of retirement planning in a capsule form.

Recently I conducted a workshop for the General public about retirement planning under the umbrella of Bangalore chapter of ICAI and I would like to share the valuable inputs for the discerning readers who generally are not informed about the various investments opportunities available in the market, my father, an Retired Banker himself always used to say keep others informed so that every body can enjoy the post retirement life smoothly without any financial stress, I am writing from my own experience because many of my clients are above 60 years and you need a lot of patience handling such a clientele but I always offer them the right advice because of constant interaction with the different savings scenario in the present Indian markets.

The present returns on 1 Year Fixed deposits for Senior citizens is at an all time low of 5.5 % and if you are an Ex Banker you will get an additional interest of 0.5 % to 1% depending on the individual bank where you had served.

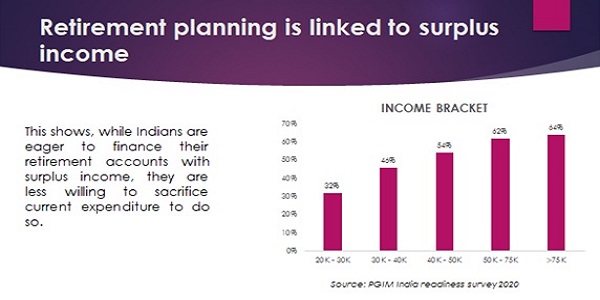

- To many, retirement seems like a distant dream. Especially in India, the concept of retirement planning is still alien. Not many people plan specifically for their old age or save for retirement. Yet, if you want to live a dignified and comfortable life in your latter days, it is imperative to plan for a corpus for retirement with the help of a sound financial plan.

- However, since India does not offer a retirement benefit system in place, the onus is on individual investors. To some extent, schemes like Employee provident funds with the present rate of return of almost 8.5 % can help cover retirement expenses for salaried individuals up to 3 years Post retirement , but business people and independent professionals need to look on to other alternatives.

- Depending on when you begin saving, there are many avenues that can help you build funds towards retirement, such as Public provident funds To Mutual funds. The earlier you incorporate a retirement corpus into your financial planning, the more you will be able to save. This can help you emerge as a wealthy senior citizen, as opposed to being dependent on your children or a family member.

The old rule of thumb used to be that you should subtract your age from 100 – and that’s the percentage of your portfolio that you should keep in stocks. For example, if you’re 45 you should keep 55% of your portfolio in stocks. If you’re 70, you should keep 30% of your portfolio in stocks.

Starting Retirement Planning in your 20s

- When it comes to saving and investing, the sooner, the better. Beginning young can give you a head start and also allow you to experiment with different kinds of products. For instance, in your 20s, you still have about four decades to rectify any bad financial decision you would make.

- For young investors, equities may seem appealing due to their long-term return potential. Mutual fund investments can be a good option to include in retirement plans. Market-linked returns and the power of compounding helps to multiply corpus over time. It can help beat inflation. If you cannot make a lump sum investment, take out a SIP. This can help you inculcate a savings habit.

- Make sure you diversify your investments across different products to benefit from different risk and return profiles.

Starting Retirement Planning in your 30s

- It is still not too late to start planning for your retirement. In your 30s, you would have about 25-30 years to get your financial portfolio together. You can afford to take some risk, but not as much as in your 20s, considering your responsibilities may have also increased.

- Apart from an emergency fund, with at least three months’ worth of expenses, allocate about 50 per cent of your savings towards a retirement fund. This can be a combination of fixed-income investments, as well as equities or mutual funds in India. SIPs are still a good avenue to consider.

Starting Retirement Planning in your 40s

- Better late than never. Starting in your 40s or 50s gives you considerably lesser time to plan for retirement. This is also the time when you may have to make crucial financial decisions, such as your children’s further education or marriage. However, it doesn’t mean that you should ignore your retirement.

- Begin by cutting down on unnecessary expenses and ensure you allocate at least 50 per cent of your savings for retirement (more if you can manage). The short time-span calls for aggressive wealth building, so look to investing in mutual funds. However, you cannot afford to lose too much money at this juncture. Balance it out with investments in bonds, fixed income and liquid instruments. Also, evaluate your assets and see how they might fit into your retirement plans.

Secrets of a Smart investor

- Smart investors have a few tricks up their sleeves, which can help them retire rich. Here are some tips for you to save smart

- Start as soon as you can. In fact, start saving for retirement now.

- Diversify your investments. Do not put all your money into one bucket, although it may seem very tempting.

- Even if you are a risk-averse investor, put some money in mutual funds so you can benefit from compounding.

- Save your bonuses instead of splurging them on vacations and impulsive buys.

- Increase your investment and savings amount every year, in tandem with the hikes you receive.

- Talk to your partner or spouse about their retirement plan, and whether it would be sensible to link both.

Stages of Retirement planning

1. Accumulation: The stage where you can accumulate or save as much money as you can for your future years. The accumulation stage comprises of:

Your early education years ( 18-22 )

Early career phase ( 22-26)

Your marriage (28-32 )

The years of raising your children (34- 49 )

Till your children move out ( 52 & Above )

A person who has successfully saved money through all these phases is more likely to achieve his/her financial goals.

2. Allocation: Simply saving a part of your income isn’t enough. You need to invest your hard-earned money in high return assets to ensure that you have enough for the future, especially since prices in the coming years will surely be higher. Hence, you must ensure that your investments give you a good return. Further, you may consider investing in assets that will give you high returns, while the remaining money can be invested in slightly risky instruments, in order to open the high risk-high return possibility.

3. Distribution: By the time you reach this stage, you have retired and are collecting money from the channels you set up during the accumulation phase. The success of the distribution stage depends on how well you manage the accumulation stage.

National pension system

> The Notional Pension Scheme (NIPS) 6 o government of Indio project that aims to give retirement benefits to all Indian residents. including those in the unorganized sector.

> NPS is a market-Inked voluntary contribution scheme managed by professional fund managers.

> Any Indian citizen from the age of 18 to 70 who meets the KYC criteria and qualities for either of the NPS models is eligible to invest in the system.

> PFRDA or Pension Fund Regulatory and Development Authority regulated and administered in order to comply with the PFRDA Act 2013.

Mutual fund

- Mutual funds are investment instruments shot enable people to set aside a portion of their income for retirement.

- These funds provide o consistent source of income after retirement; a retie receives on annuity on the investment until they expire.

- To ensure regular returns. retirement mutual fund plans typicality invest in low risk investment options such as government securities.

PMVVY :

(LIC – 7.4 %) scheme details: Senior citizens aged 60 or above can subscribe to Pradhan Mantri Vaya Vandana Yojana (PMVVY) through the LIC website online. This is an immediate pension plan which can be purchased online by paying a lump sum amount. It provides a stated amount as pension for the policy term of 10 years. The purchase price is returned to the subscriber at the end of 10 years.

Under PMVVY, a senior citizen subscriber can get a monthly pension of Rs 9250 for 10 years by purchasing the plan for Rs 15 lakh. After the completion of the 10 years, the purchasing price of Rs 15 lakh will be returned to the subscriber.

The annuity received is taxable in the hands of the recipient.

Secondary Debt Markets

Returns you can expect in the range of 7.75 % to 11.70 % But Most of them come with a ticket size of Rs 1.00 Million and come in both secured and unsecured Debt Instruments, so there is certain amount of Risk Attached.

In the current interest rate scenario, the Retail Debt Market presents a vast range of opportunities for the investor whose knowledge and participation hitherto has been restricted to only Bank/Postal/Corporate deposits. The Debt Markets are suited for investors who seek decent returns over a longer time horizon with periodic cash flows. Here is your Opportunity to invest in secondary debt products which carry better returns as compared to the conventional fixed income giving investment avenues. These debt instruments also comes with high Liquidity, as these securities are listed and tradable

Summary

> One of the most significant aspects of our financial preparation is retirement planning.

> You can’t avoid the fact that your work life will come to an end at some point, and you’ll have to rely on the savings and investments you’ve accumulated.

> So. wise retirement planning can work miracles and allow you to enjoy your golden years in peace.

> Furthermore. with the advancement of technology. finding the best retirement plan by conducting an Internet search is no longer o difficult task.

Author Bio