India is home to over 26 million small and medium enterprises (SMEs) that account for nearly 20% of the country’s GDP. While small enterprises like grocery stores, brick-kilns, small restaurants, etc.; are driving the economic growth by providing employment opportunities in large numbers, they are still facing challenges when it comes to finding the right finance option. Finance is critical to the growth and development of any industry, and it becomes more important for SMEs which are operating on a small scale.

Various banks and Non-banking finance companies (NBFCs) like Aditya Birla Finance Limited are offering several SME loans to cater to different requirements of these entrepreneurs, but it is necessary to choose the right option as per the needs.

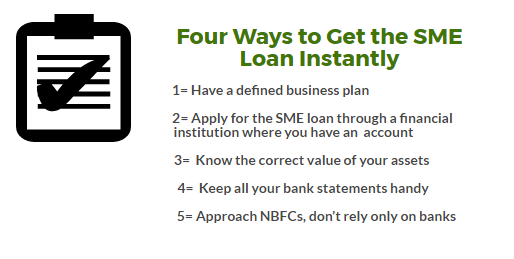

Some of the loan options to meet funding requirements are-

1. Working Capital Loan: As the name itself implies, this loan offers ‘working capital’ to manage the day-to-day functioning of the business. It can be further divided into the following two categories—

- Secured Loans: As this loan is backed by assets, like land, bank account, equipment, etc.; it curtails the risk assumed by the lender. Note, the lender has all rights to forfeit the pledged asset if the borrower fails to repay the loan amount.

- Unsecured Loans: As this loan option doesn’t require collateral, it is offered at high interest rates. One can opt for this loan option, depending on its running and recurring costs.

2. Term Loan: This loan is extended by financial institutions to assist the SME sector in carrying out its various long-term business projects. As it carries competitive interest rates with fixed repayment schedules, it is an extremely popular SME loan option among entrepreneurs.

3. Overdraft: Here the word overdraft means, withdrawing more money from your current account than what has been deposited. It is a credit facility extended by banks in exchange for some collateral or securities, like fixed deposits, life insurance policy, property, etc. Based on the assets given as collateral, the bank offers an open-ended loan which a business can utilise to fund its requirements. Here the interest will be charged on the loan amount actually used and not on its total value.

4. Bill Discounting: It means, advance selling of the bill to an intermediary before it is due for payment. Here, the credit period may vary between 30-120 days. It is mainly applied in those scenarios when a buyer purchases goods from the seller and the payment is made through the letter of credit. On the basis of the credit worthiness of the buyer, the bank offers discounts on the amount that requires being paid at the end of the credit tenure. It is a useful way to get instant funds at a discounted rate. However, the bank may ask you to submit some documents like truck/railway receipts, invoice challans, bill of lading, etc.; to authenticate the transaction.

Other Alternatives

1. Letter of Credit: Mainly used by businesses who are involved in foreign trade, this is a letter from a bank that guarantees the payment and assures that a buyer’s payment to a seller will be received on time. Also known as Documentary Credit, this letter acts as a trust point between the buyer and seller and plays an imperative role in the international trade where both the parties may not know each other personally and are also separated by distance and laws.

In the event, when the buyer is unable to make payments, the seller will approach the bank for payment, who after analyzing the situation will honor the demand (assuming all the requirements are met).

2. Gold Loan: The exchangeability of gold along with its inherit properties make gold loans an extremely viable SME loan option for entrepreneurs who are looking for some immediate financial assistance. Various banks and financial institutions are offering gold loans with the collateral return on repayment of the loan amount.

NBFCs or Non-Banking Financial Companies have understood the potential for growth in the SME sector, and therefore, they are offering various SME loan options to these enterprises. In fact, most NBFCs in the country have stepped in to meet capital requirements of SMEs, when banks in India are laden with bad loans.

A Word of Caution

There are various ways through which SME loans can be availed, however, it is pertinent to align your loan with your business requirements. So first, have a clear understanding of your business requirements and then only choose the right loan option.