Presentation made on Indian Budget 2020 in the programme which was organised by Noida Management Association in association with Noida chapter of ICSI and ICMAI.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation and we will not be responsible in any circumstances, whatsoever. For more details you may also refer to the sources of such information as mentioned therein.

Discussion Points

♦ Indian Economy at a Glance

♦ Mission $5 Trillion Economy and Key Challenges

♦ Global Competitive Index: Indian Parlance

♦ Key Highlights of Economic Survey 2019-20

♦ Key Initiatives under Indian Budget 2020

♦ Impact on Infra and Real Estate Sector

♦ Common Man’s Perspective

♦ Way Forward

Indian Economy at a Glance

♦ India has emerged as the fastest growing major economy in the world and is expected to be one of the top three economic powers of the world over the next 10-15 years, backed by its strong democracy and partnerships.

♦ With more than 1.2 billion people and the world’s third largest economy in purchasing power parity terms, India’s recent growth has been a significant achievement

♦ India’s labour force is expected to touch 160-170 million by 2020, based on rate of population growth, increased labour force participation, and higher education enrolment, among other factors, according to a study by ASSOCHAM and Thought Arbitrage Research Institute.

♦ India has retained its position as the third largest startup base in the world with over 8,900-9,300 startups, with about 1,300 new start-ups being founded in 2019, according to a report by NASSCOM. India also witnessed the addition of 7 unicorns in 2019 till August.

♦ Numerous foreign companies are setting up their facilities in India on account of various government initiatives like Make in India and Digital India.

♦ India is also focusing on renewable sources to generate energy. It is planning to achieve 40 per cent of its energy from non-fossil sources by 2030 which is currently 30 per cent and have plans to increase its renewable energy capacity from to 175 GW by 2022.

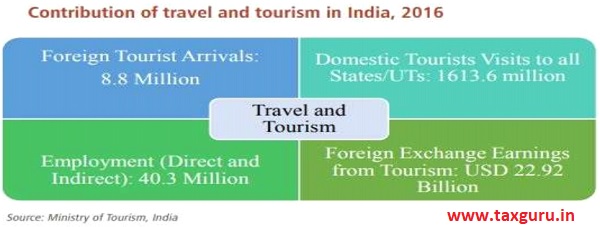

♦ Apart from Information Technology sector, Travel and tourism, health, and professional services can be the other star service sectors. Better delivery of infrastructure, education and essential services would also create a large number of jobs and growth.

Source: IBEF

Outlook for Real Estate

♦ Commercial leasing in real restate space exhibited a strong trend with gross leasing in the top seven cities amounting to a total volume of 59 million square feet, as per Colliers Research.

♦ Residential sales in the top seven cities in 2019 stood at 261,000 units against 242,000 units in 2018. Outlook for Real Estate

Steps Taken by Government in the past year to Improve Sentiment & Revive Demand in Real Estate

♦ Enhancing the limits of loans under the Pradhan Mantri Awas Yojana (PMAY).

♦ Increasing the deductions available for interest/principal repayments on home loans for affordable units,

♦ Trying to inject liquidity for NBFCs through the Reserve Bank of India.

♦ Setting up the Rs 25,000 crore last-mile funding fund for stuck projects.

Expectations of Real Estate Sector from Budget 2020

♦ Waiver of principal/interest (from income tax) of potential buyer for limited period.

♦ Government should consider higher exemption limit for buyers.

♦ The sector expects the Budget 2020 to announce industry status to the real estate sector that will further help in raising low-cost funds and make land acquisition simpler.

♦Central government should provide exemptions so that cement and other core sectors can play a pivotal part in boosting renewable energy.

♦ Central government should release stuck up funds which were meant for infrastructure sectors to bring back ‘buoyancy’ in the economy.

Source: Economic Survey 2019-20

Mission $5 Trillion Economy by 2024-25

In January 2018 at Davos, Switzerland, that Prime Minister Narendra Modi had first spoken about his ambition of seeing India as a US$5 Trillion economy by 2025. He reiterated the target at Niti Aayog’s governing council meeting in New Delhi in June. On July 5th, finance minister Nirmala Sitharaman spoke about the $5 trillion target in her 2019 Budget.

Source: Media Reports

Key Challenges in $5 Trillion Economy

♦ Require GDP growth of 8% which is not there in the current scenario.

♦ A large share of India’s workforce is employed in low productivity activities with low levels of remuneration. A large number of workers that are engaged in the unorganized sector are not covered by labour regulations and social security. According to the India Skill Report 2018, only 47 per cent of those coming out of higher educational institutions are employable.

♦ Low R&D expenditure, especially from the private sector, is a key challenge facing the innovation ecosystem in India. The number of scientific R&D professionals in India at 218 per million population is distressingly low compared to China and USA.

♦ Exports and insufficient domestic demand.

♦ Use of outdated and inappropriate technology is the main reason for low productivity of crops and livestock. There exists a large gap between farm harvest prices (FHP) and retail prices. Prices also tend to fall below the minimum support prices in a good production year, leading to agrarian distress.

Source: NITI Aayog Strategy for New India @ 75

♦ India has huge mineral potential, but high incidence of taxes, shortcomings in licensing regime, inadequate infrastructure hinders working at full potential.

♦ Efficient plants being underutilized, limited technical capabilities, high initial capital expenditure, limited market and policy issues have adversely affected efforts to achieve energy efficiency.

♦ As the gap between the average cost of supply (ACS) and average revenue realized (ARR) persists due to high aggregate technical and commercial (AT&C) losses, distribution companies use load shedding to minimize losses.

Source: NITI Aayog Strategy for New India @ 75

![]()

Global Competitiveness : INDIA

STRENGTHS

| Particulars | Ranking |

| Market Size | 3rd |

| Corporate Governance | 15th |

| Future Orientation of Government | 15th |

| Public Sector Performance | 25th |

| Transport | 28th |

| Innovation | 35th |

| Financial System | 40th |

| Macro Economic Stability | 43rd |

| Checks & Balances | 54th |

WEAKNESS

| Particulars | Ranking |

| Transparency | 66th |

| Business Dynamism | 69th |

| Property Rights | 87th |

| Banking System | 89th |

| Product Market Efficiency | 101st |

| Social Capital | 101st |

| Labour Market | 103rd |

| Utility Infrastructure | 103rd |

| Skill Base | 107th |

| Health | 110th |

| ICT Adoption | 120th |

| Security | 124th |

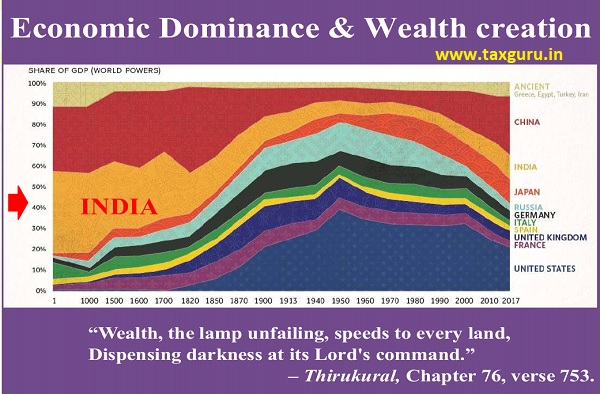

WEALTH CREATION

♦ Exponential rise in India’s GDP and GDP per capita post-liberalisation coincides with wealth generation.

♦ Survey poses that India’s aspiration to become a $5 trillion economy depends critically on strengthening the invisible hand of the market, providing equal opportunities for new entrants, and introducing the idea of trust as a public good, which gets enhanced with greater use.

ENTREPRENEURSHIP

♦ Entrepreneurship as a strategy to fuel productivity growth and wealth creation.

♦ India ranks third in a number of new firms created, as per the World Bank.

♦ 12.2 per cent cumulative annual growth rate of new firms in the formal sector during 2014-18 as compared to 3.8 per cent during 2006-2014.

♦ About 1.24 lakh new firms created in 2018, an increase of about 80 per cent from about 70,000 in 2014.

Source: Business World

Source: Economic Survey 2019-20

PRO-BUSINESS VERSUS PRO-MARKETS

♦ Promoting ‘pro-business’ policy that unleashes the power of competitive markets to generate wealth.

♦Weaning away from ‘pro-crony’ policy that may favour specific private interests, especially powerful incumbents.

DEBT WAIVERS

♦The Survey suggests the government must systematically examine areas of needless intervention and undermining of markets; but it does not argue that there should be no Government intervention.

♦ Eliminating such instances will enable competitive markets spurring investments and economic growth.

JOBS AND GROWTH

♦ Survey says India has unprecedented opportunity to chart a China-like, labour- intensive, export trajectory.

♦ By integrating ‘Assemble in India for the world’ into Make in India, India can raise its export market share to about 3.5 pc by 2025 and 6 pc by 2030.

♦ Exports of network products can provide one-quarter of the increase in value- added required for making India $5 trillion economy by 2025.

EASE OF DOING BUSINESS

♦ A jump of 79 positions to 63 in 2019 from 142 in 2014 in World Bank’s Doing Business rankings.

♦ Need for close coordination between the Logistics division of the Ministry of Commerce and Industry, the Central Board of Indirect Taxes and Customs, Ministry of Shipping and the different port authorities.

BANKING SECTOR

♦ A large economy needs an efficient banking sector to support its growth.

♦ The onus of supporting the economy falls on the PSBs accounting for 70 per cent of the market share in Indian banking.

♦ PSBs are inefficient compared to their peer groups on every performance parameter.

♦ The Survey suggests the representation on boards proportionate to the blocks held by employees to incentivise employees and align their interests with that of all shareholders of banks.

PRIVATISATION AND WEALTH CREATION

♦ Privatized CPSEs have been able to generate more wealth from the same resources.

♦ The Survey suggests aggressive disinvestment of CPSEs to bring in higher profitability, to promote efficiency, increase competitiveness, and promote professionalism.

INDIA’S GDP GROWTH

♦ GDP growth is a critical variable for decision-making by investors and policymakers. Therefore, the recent debate about the accuracy of India’s GDP estimation following the revised estimation methodology in 2011 is extremely significant.

THALINOMICS

♦ An attempt to quantify what a common person pays for a ‘Thali’ across India.

♦ A shift in the dynamics of ‘Thali’ prices since 2015-16. Affordability of vegetarian ‘Thalis’ improved 29 pc. Affordability of non-vegetarian ‘Thalis’ improved by 18 pc.

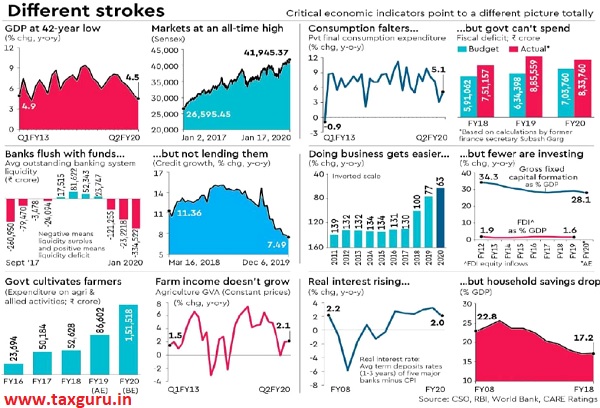

ECONOMIC PERFORMANCE IN 2019-20

♦ India’s GDP growth moderated to 4.8 per cent in H1 of 2019-20, amidst a weak environment for global manufacturing, trade and demand.

♦ Real consumption growth has recovered in Q2 of 2019-20, cushioned by significant growth in government final consumption.

♦ Current Account Deficit (CAD) narrowed to 1.5 pc of GDP in H1 of 2019-20 from 2.1 pc in 2018-19. Headline inflation expected to decline by year-end.

FISCAL DEVELOPMENTS

♦ Revenue Receipts registered a higher growth during the first eight months of 2019-20, compared to the same period last year, led by considerable growth in Non-Tax revenue.

♦ Gross GST monthly collections have crossed the mark of Rs 1 lakh crore for a total of five times during 2019-20 (up to December 2019).

BALANCE OF PAYMENTS

♦ India’s BoP position improved from US$ 412.9 billion of forex reserves in end-March, 2019 to US$ 433.7 billion in end September 2019.

♦ Current account deficit (CAD) narrowed from 2.1 per cent in 2018-19 to 1.5 pc of GDP in H1 of 2019-20.

♦ Foreign reserves stood at US$ 461.2 billion on January 10, 2020.

GLOBAL TRADE

♦ In sync with an estimated 2.9 per cent growth in global output in 2019.

♦ Global trade is estimated to grow at 1 pc after having peaked in 2017 at 5.7 per cent.

♦ It is projected to recover to 2.9 per cent in 2020 with recovery in global economic activity.

EXPORTS

♦ The merchandise exports to GDP ratio declined, entailing a negative impact on BoP position. Slowdown of world output had an impact on reducing the export to GDP ratio, particularly from 2018-19 to H1 of 2019-20.

♦ Growth in Non-POL exports dropped significantly from 2009-14 to 2014-19.

♦ Large Crude oil imports in the import basket correlates India’s total imports with crude prices. As crude price raises so does the share of crude in total imports, increasing imports to GDP ratio.

LOGISTICS INDUSTRY OF INDIA

♦ Currently estimated to be around US$ 160 billion.

♦ Expected to touch US$ 215 billion by 2020.

♦ According to World Bank’s Logistics Performance Index, India ranks 44th in 2018 globally, up from 54th rank in 2014.

EXTERNAL DEBT

♦ Remains low at 20.1 per cent of GDP as at end September 2019.

♦ After significant decline since 2014-15, India’s external liabilities (debt and equity) to GDP increased at the end of June 2019 primarily by an increase in FDI, portfolio flows and external commercial borrowings (ECBs).

MONETARY POLICY

♦ Remained accommodative in 2019-20.

♦ Repo rate was cut by 110 basis points in four consecutive MPC meetings in the financial year due to slower growth and lower inflation.

GROSS NON PERFORMING ADVANCES RATIO

♦ Remained unchanged for Scheduled Commercial banks at 9.3 per cent between March and September 2019. Increased slightly for the Non-Banking Financial Corporation (NBFCs) from 6.1 per cent in March 2019 to 6.3 per cent in September 2019.

CREDIT GROWTH

♦ The financial flows to the economy remained constrained as credit growth declined for both banks and NBFCs. Bank Credit growth (YoY) moderated from 12.9 per cent in April 2019 to 7.1 per cent as on December 20, 2019.

♦ Capital to risk-weighted asset ratio of SCBs increased from 14.3 per cent to 15.1 per cent between March 2019 and September 2019.

PRICES AND INFLATION

♦ Inflation witnessing moderation since 2014. Consumer Price Index (CPI) inflation increased from 3.7 per cent in 2018-19 (April to December 2018) to 4.1 per cent in 2019-20 (April to December 2019). WPI inflation fell from 4.7 per cent in 2018-19 (April to December 2018) to 1.5 per cent during 2019-20 (April to December 2019).

FOREST AND TREE COVER, AGRICULTURE AND FOOD MANAGEMENT

♦ FTC Increasing and has reached 80.73 million hectare.

♦ Largest proportion of the Indian population depends directly or indirectly on agriculture for employment opportunities as compared to any other sector.

♦ The share of agriculture and allied sectors in the total Gross Value Added (GVA) of the country has been continuously declining on account of relatively higher growth performance of non-agricultural sectors, a natural outcome of the development process.

♦ Agricultural productivity is also constrained by a lower level of mechanization in agriculture which is about 40 pc in India, much lower than China (59.5 pc) and Brazil (75 pc). Livestock sector has been growing at a CAGR of 7.9 pc during the last five years.

INDUSTRY AND INFRASTRUCTURE

♦ The industrial sector as per Index of Industrial Production (IIP) registered a growth of 0.6 pc in 19-20 (April-Nov) as compared to 5 pc during 18-19 (April-Nov). The installed capacity of power generation has increased to 3, 64,960 MW as on October 31, 2019, from 3, 56,100 MW as on March 31, 2019.

SERVICES SECTOR

♦ Services sector accounts for about 55 pc of the total size of the economy and GVA growth. 2/3rd of total FDI inflows into India. About 38 pc of total exports.

♦ FDI into services sector has witnessed a recovery in early 2019-20.

EMPLOYMENT AND HUMAN DEVELOPMENT

♦ The expenditure on social services (health, education and others) by the Centre and States as a proportion of GDP increased from 6.2 per cent in 2014-15 to 7.7 pc in 2019-20 (BE).

♦ India’s ranking in Human Development Index improved to 129 in 2018 from 130 in 2017. With 1.34 pc average annual HDI growth, India is among the fastest-improving countries

♦ Total formal employment in the economy increased from 8 per cent in 2011-12 to 9.98 per cent in 2017-18.

Measures for Boosting Economy

♦ Investment Clearance Cell to be set up at Centre and States.

♦ NIRVIK Scheme launched for higher export credit disbursement.

♦ Schemes to boost manufacturing of mobile phones, electronic equipment and semi conductor packaging.

♦ New schemes for subordinate debt for MSME. App based invoicing finance for MSME. Digital refunds for duties on export.

♦ National Technical Textile Mission to be launched soon.

♦ 2000 k.m. of Strategic Highway to be built.

♦ More Tejas type trains to be introduced to encourage tourism.

♦ Rs 2.83 lakh crores allocated for agriculture and allied activities, irrigation and rural development.

♦ An allocation of Rs 8,000 crore for National Mission on Quantum Computing and Technology.

♦ Milk Production Capacity to be expanded 108T from 53.5T. Fish production capacity to increase to 200 Lakh Tonnes by 2022-2023.

♦ Solar Power Plant to be established on the barren land.

♦ Corporate Tax reduced to 15% for newly incorporated Power and Manufacturing Companies.

♦ Eligibility limit for NBFCs for debt recovery under SARFAESI Act proposed to be reduced to asset size of Rs 100 crores or loan size of Rs 50 Lakhs.

♦ A robust mechanism is in place to monitor the health of all scheduled commercial banks.

♦ Rs. 25,000 crores allocated for Tourism Promotion and 23150 crores for Cultural Ministry.

Impact on Real Estate & Infrastructure Sector

♦ Government proposes 100% tax concession to sovereign wealth funds on investment in infra projects. It will attract investments.

♦ Tax holiday on profits earned by Developers of Affordable Housing projects approved by March 31, 2020.

♦ Rs. 100 crores has been allocated to boost infrastructure sector. Govt. extends additional Rs 1.5 lakh tax benefit on interest paid on affordable housing loans to March 2021.

♦ 100 more airports to be developed by 2025.

♦ 100% tax concession to sovereign wealth funds on investment in infra projects.

♦ National Gas Grid to be expanded from 16,200 kms to 27,000 kms

Common Man’s Perspective

♦ Introduction of New Income Tax Regime will reduce tax burden on common man.

♦ Allocation of funds amounting to Rs 85,000 crores for welfare of Backward Class and Scheduled Castes and Rs 53,700 crores for Scheduled Tribes. Manual Scavenging is proposed to be eliminated.

♦ Agricultural Credit target has been increased to Rs 15 Lakh Crores for year 2020 which will benefit the farmers in taking loans.

♦ 16-point action plan for farmers, towards the goal of doubling farmers’ income by 2022.

♦ Deposit insurance for each depositor is increased from 1 Lakh to 5 Lakhs.

♦ Krishi Rail and Krishi Udan to be launched by Indian Railways and Ministry of Civil Aviation respectively for a seamless national cold supply chain for perishables.

♦ ‘Vivad se Vishwas’ scheme for direct tax payers whose appeals are pending at various forum.

♦ Expansion of PM KUSUM Scheme under which 20 lakh farmers would be provided funds to set up standalone solar pumps. Farmers with barren land can set up solar power units so that they can get a living out of it.

♦ Action plan to ease India’s water problems starts with helping 100 districts. Govt proposes Rs 3.6 lakh crore towards piped water supply to households.

♦ Rs 99,300 crore outlay for education sector in 2020-21 and Rs 3,000 crore for skill development. Govt propose National Police University and National Forensic University. With the largest working population, these steps to ensure education for all.

♦ An allocation of ₹69,000 crore for the health sector. ₹12,300 crore for Swachh Bharat this year. Proposal to set up hospitals in Tier-II and Tier-III cities with the private sector using PPP. Expand Jan Aushadhi scheme to provide for all hospitals under Ayushmann Bharat by 2025.

Way Forward

♦ Macroeconomic stability through prudent fiscal and monetary policies. A focused effort on making the logistics sector more efficient is needed.

♦ Virtuous cycle of savings, investment, exports and growth with investment as the “central driver”.

♦ Skills enhancement and apprenticeships program including women. Making the compliance of working conditions regulations more effective and transparent.

♦Promoting innovation, entrepreneurship and startups. Courses for development of scientific temperament should be introduced at early level. Incentives for green R & D.

♦ Demand generation, introduction of new technology, augmentation of industrial infrastructure and promotion of MSMEs.

♦ Modernize agricultural sector. Time to try a new model where farmers learn to be productive by working in association with a professional firm which takes care of farming, marketing, and exports.

♦ Regulatory bodies need to be further strengthened and made truly independent.

♦ To facilitate participation by private sector players in exploration, launch a mission “Explore in India”, by revamping the minerals exploration and licensing policy

♦Boosting minor minerals through a relaxed licensing regime. Single window and time-bound environment and forest clearances.

♦Enhance production from the existing fields of ONGC and OIL using cutting-edge technology through a framework of production enhancement contracts.

♦ Policy makers should look beyond monetary policy

♦ As the country ranks high on macroeconomic stability and market size, Investments and incentives should be brought upon to revive productivity.

♦ Finding balance between technology integration and human capital investment

♦ Environment, social and economic agendas to be merged into a single, inclusive and sustainable growth.

Source: NITI Aayog Strategy for New India @ 75

Thanks

Let us Explore Possibilities

IRECFO is team of diverse professionals having rich and strong multi-dimensional experience of Real Estate Business while working at Top Corporate Level positions with unique competency of taking Deep Dive into such complex matters having multi-level cascading long term impacts on Real Estate Business. We are providing End to End Customized solutions in RERA / IBC and Funding related matters with in depth analysis on business operations and are closely working with many leading developers, lenders and investors, on all sizes of Real Estate projects, to resolve such issues.