Captures the budget highlights and the direct tax changes which encapsulates roadmap to Amrit Kaal.

“Faces light up listening to Nirmala Sitaraman budget speech on budget day!’

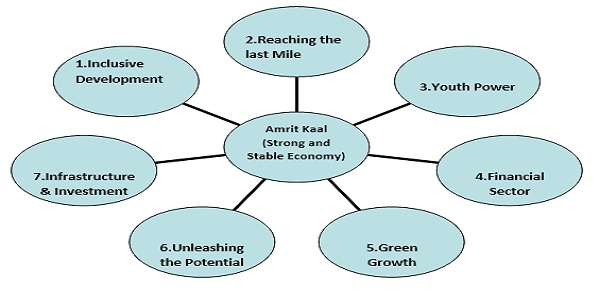

While the previous budget solely focussed on corporate tax incentivising to boost the manufacturing, infrastructure spending and ease of doing business, Budget 2023 focussed not only on building on its previous focus but also augmenting it with socio economic measures. The budget proposes to reach a strong and stable state of economy akin to the sacred nectar or the Amrit through it seven budget priorities (Saptarshi policy).

1. Inclusive Development-Agricultural and cooperatives which includes initiative of building digital public infrastructure for farmers, setting up of agriculture accelerator fund for rural start-ups, horticulture clean plant program, making India global hub for Millets(Anna) by providing support to research at IIMR, Hyderabad. Also 20 lacs crore credit targeted at animal husbandry, Dairy and fisheries sector and setting up decentralised storage facility for farmers to enhance their remuneration.

2. Reaching the last mile includes the expansion of ministry of ministries of AYUSH, Fisheries, Animal Husbandry and Dairying, Skill Development, Jal Shakti and Cooperation. To develop the primitive vulnerable tribal groups (PM PVGT) and aim for saturation of essential government services in multiple domain of health, nutrition education, skill and water at 500 aspirational blocks identified by Govt. Govt. to recruit 38,800 teachers and support staff for the 740 Eklavya Model Residential Schools, serving 3.5 lakh tribal students. Further efforts are made to preserve ancient scriptures digitally.

3. Youth power: With the launching of the Pradhan Mantri Kaushal Vikas Yojana over next 3 years, the budget proposes to launch courses in Artificial intelligence, Robotics and 3D printing. 50 destinations in India to be chosen as a challenge to be best tourist destination for domestic and foreign tourist. States would be encouraged to set up Unity Mall at district level to promote sale of one district one product and handicrafts.

4. Financial Sector: To enable financial lending and enhance financial stability, a National Financial Information registry is to be set up. To expedite handling of administrative work under the companies Act, a Central Data Processing centre shall be set up. MSME to be able to access additional collateral free 2 lac crores of corpus. Introduce one time small saving scheme up to 2 lacs for women at 7.5% and no TDS applicable on such interest. Enhanced maximum deposit limit for senior citizen raised from 15 lacs to 30 lacs. SEBI to create more trained Security Market professionals by award of educational certificates.

5. Green Growth: The government proposes to introduce Green credit program to incentivize sustainable environmental actions vide promotion of green fertilizers and 500 waste to wealth plants “GOBARdhan”. Develop sustainable ecosystems promoting mangroves along coastal lines and optimisation of wetlands. Other green initiative includes promotion of battery storage system, coastal shipping and energy efficient transportation and replacing of old vehicles.

6. Unleashing the potential: Building trust based governance by easing stringent contractual execution for MSME, faster dispute resolution and settlement through Vivad se Vishwas I and II. E Courts to effect administration of justice. Entity Digi Locker to be set up for businesses and trust to facilitate online sharing of documents with business. To reduce dependency on import, to set up R & D facility to develop lab grown diamonds. To tab employment opportunity, introduce 100 labs of 5G service based applications.

7. Infrastructure and Investment: Investment in infrastructure is a huge boost to economy. The outlay of 2.4 lac crores to railways not only creates ‘Raman effect’ of capital spending but also provides an impetus the employment generation. This spending in proposed for 2 tier and 3 tier cities. More than 100 transport infrastructure identified to connect ports and industries end to end. States to get 50 years interest free loan for capital spending in next 3 years.

Budget 2023 thus aims at an all-round sustainable economic development supported by the developments in the 7 priority areas.

Personal tax rates.

Coming to personal tax changes, personal tax exemption limit raised from 5 lacs to 7 lacs under the new tax regime. The existing New tax regime are overhauled as under:

| Previous new tax regime | Updated new tax regime | ||

| Income in Lacs | Rate | Income in Lacs | Rate |

| Up to 2.5 | 0 | Up to 3 | 0 |

| 2.5 to 5 | 5% | 3 to 6 | 5% |

| 5 to 7.5 | 10% | 6 to 9 | 10% |

| 7.5 to 10 | 15% | 9 to 12 | 15% |

| 10 to 12.5 | 20% | 12 to 15 | 20% |

| 12.5 to 15 & above | 30% | Above 15 | 30% |

1. The budget provides a tax savings of 25% to an individual with income of 9 lacs and 20% tax savings for income of 15 lacs under new tax savings scheme. Further, benefit of standard deduction of Rs.52,500/- stands extended to salaried as well as pensioners under new tax regime for income above Rs.15.5 lacs. This brings smiles to many middleclass employees and professionals.

2. The highest tax rate applicable is proposed to be reduced to 39% as against 42.74% for income above 5 crores, by restricting the highest surcharge rate to 25%

3. For the purpose capital gains arising on transfer of a residential house or any other asset by reason of investing in a new residential house, for the limited purpose of computing the deduction, the investment in the new house to be restricted to 10 crores, irrespective of actual higher investment.

4. The senior citizens had something to look forward to in this budget. The limit of 3 lakh for tax exemption on leave encashment on retirement of non-government salaried employee is increased to 25 lakhs.

5. Currently, in the absence of PAN, TDS will apply at applicable rates at the time of withdrawal of the PF balance from the EPFO. It now stands rationalized to 20%.

Socio Economic Measures:

1. In order to promote timely payments to MSME, it is proposed to include these payments under the ambit of section 43 of the Act and provide deduction only upon making payments within mandated timelines.

2. The Agnipath scheme 2022, a short service scheme (of 4 years) in the Indian Army and the contributions of such recruits(Agniveers) to the Agniveer Corpus Fund is proposed to be exempt. This is to encourage such them to enrol into short service schemes and build a corpus for their retirement.

3. Relief to sugarcane co-operatives, who can make an application to assessing officer to recompute their tax liability, if there is dispute on account of allowability of sugarcane purchase cost. The AO to allow such deduction on the basis of government approved rates in such previous year.

4. Relief provided to co-operative societies to withdraw cash in a year up to 3 crores and not suffer TDS on cash withdrawal. Further, relief is provided under section 269T to exclude primary agricultural co-operative society for repayment of loans up to 2 lacs in cash.

5. Extension of date of incorporation from 1 April 2023 to 1April 2024 to be eligible for tax exemption provided to start-up.

6. With a view to promote electronic investment in gold, transfer of physical gold into electronic holding and vice versa to be excluded from ambit transfer, and capital gains shall not apply to such transactions.

7. The end date of relocation of funds to IFSC is extended from 31 March 2023 to 31 March 2025. Further, subject to fulfilment of conditions, the income distributed from offshore derivative instruments with offshore banking units is proposed to be exempted.

8. With a view to promote housing, planning, development of towns, cities, development authorities and regulating bodies formed by the central or state government for such activity are exempted from tax on their income irrespective of the nature of activity being commercial activity or not. It is interesting to note that this stand of activity being non-commercial activity for applicability of exemption is applicable to Trusts, business associations.

Simplification of tax benefits for the industry:

1. The limits applicable for eligibility to be taxed under presumptive taxation in section 44DA for business and professionals having turnover up to 3.75 crores having less than 5% of cash receipts and payments during the year.

2. Further deduction on account of payments made to MSME shall be allowed only on payment basis.

3. Budget proposes extending the scope of TDS at lower rates or nil rates by Business Trusts under section 194LBA, subject to obtaining lower withholding certificate.

Deepening tax base and anti-avoidance measures:

1. Gift of money by residents to not-ordinarily residents to become taxable to ensure parity with non-resident receipients.

2. The Income Tax Act that grants exemption under section 2, to notified news agencies from paying tax on income, provided the organisation applies its income or accumulates it solely for collection and distribution of news and does not distribute it to its members. This exemption is proposed to be omitted to capture them in the tax base.

3. Introduction of tax on online gaming (section 115BBJ) where the said income shall be taxed at the rate of 30%. The said income shall be subject to withholding tax under section 194BA at the rates in force and TDS provisions are applicable w.e.f. 1 July 2023.

4. Section 170A of the Act pertains to furnishing of modified return by the successor entity in case of any business re-organization such as amalgamation, demerger, etc. has been amended to include procedure to be followed by the Assessing Officer after the modified return is furnished by the successor entity.

5. The cost of acquisition and cost of improvement of intangible assets or rights to be taken as nil in case of mergers be taken as nil, except when covered under specified cases.

6. Capital gains on transfer or redemption or maturity of market-linked debentures will be deemed to be short term capital gains w.e.f. FY 2023-24.

Thus, the various socio-economic measures and provisions creates a roadmaps to strong and stable Indian economy. The success however lies in the execution of these policies during its journey to the Amrit Kaal.

Author: Latha Sherlekar -Tax Senior II -Deloitte Haskins & Sells LLP (The article is written in personal capacity)