Everything we buy from E-commerce to Fashion; from Interest-free Insurance payments to our Dream vacations; from Online Courses to Gym memberships, often the seller of the product (or service) offers Equated Monthly Installments (EMI) as one of the payment options. EMI is a periodic payment made by a borrower to a lender towards a loan opted for. EMI payment can be broken into the interest component and principal component. With the advent of the festive season, several vendors (both online and offline) are offering ‘No-cost EMI’ or ‘Zero Cost EMI’ on a wide range of products like expensive vehicles, homes and electronic appliances, and so on.

Whilst EMI provides the freedom to buy expensive utilities for the common man making it easier for him to pay off the said amount in small chunks periodically without any pinch, there is a cost behind these ‘no-cost EMI’ which someone has to bear. Most of the retailers have tie-ups with financial institutions offering zero cost loans while the actual interest rate charged on such loans can be up to 24 percent.

As per the RBI circular (RBI/2013-14/292 DBS.CO.PPD No. 3578 /11.01.005/2013-14) dated September 17, 2013, wherein it says, “In the zero percent EMI schemes offered on credit card outstandings, the interest element is often camouflaged and passed on to the customer in the form of processing fee. Since the very concept of zero percent interest is non-existent and fair practice demands that the processing charge and rate of interest (RoI) charged should be kept uniform product/segment-wise, irrespective of the sourcing channel, such schemes only serve the purpose of alluring and exploiting the vulnerable customers. The only factor that can justify differential RoI for the same product, tenor being the same, is the risk rating of the customer, which may not be applicable in the case of retail products where the RoI is generally kept flat and is indifferent to the customer risk profile. It is the responsibility of the banks, who are/may be using their good offices to get the better bargain, to make the customers fully aware of these benefits and also pass on the benefits to them fully and indiscriminately. The loan amount sanctioned for the purchase should be after taking into account the discount, rather than giving effect to the benefit by reducing the RoI. Similarly, if there is a moratorium period for payment available, the benefit should be passed on to the customer.”

The above scheme can be further elaborated with the help of an example given below:

Suppose the product you want to purchase costs ₹ 50,000. Under the twelve-month EMI plan, the interest rate charged is 18 percent and you would have to pay an interest amount of ₹ 4,583.

Case a) when a discount is equivalent to interest (popularly used by online retailers)

| Particulars | Amount ₹ |

| Cost of the product (pre discount) | 50,000 |

| Discount offered | (4,583) |

| Cost of the product (post discount) | 45,417 |

| Total interest to be paid (under EMI) | 4,583 |

| Total amount to be paid by you | 50,000 |

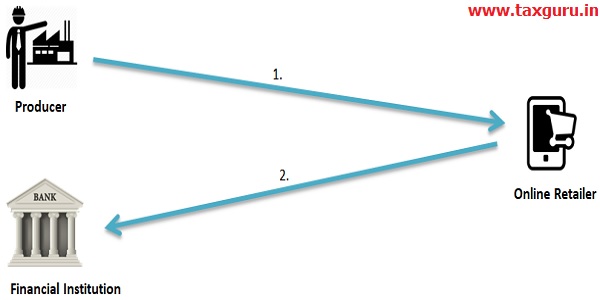

The table can be furthermore elaborated using the given Exhibit:

Let’s say the producer sells the product to the online retailer at the cost of ₹40,000 per unit (MRP for the same is ₹50,000). Profit so earned by the producer is ₹10,000. Assume that online retailer can sell 1000 units per month of the product supplied by the manufacturer. Gross Profit so generated by the online retailer is about ₹1,00,00,000 (i.e 1cr.) per month.

Now the Financial Institution (say Bank) proposes an offer to the online retailer (say to double the profit generated by the retailer alone). For this, the retailer has to give a payment option of NO Cost EMI to the customer. The marketing gimmick of NO Cost EMI attracts more customers for online retailer resulting in double profits generated by the retailer alone.

Further, the Financial Institution charges ₹5,000 from the retailer (i.e. Interest cost which is approximately equal to half of the profit generated by the retailer). As stated earlier there is a cost behind these no-cost EMI which someone has to bear. Here the financial institution is paying the cost behind the no-cost EMI which is ultimately shifted to the consumer in case b.

Lastly, the online retailer will end up earning a profit of ₹5,000 per unit with a double customer base opting for NO Cost EMI. Consequently, the Financial Institution will charge the same with a doubled customer base of retailer opting for NO Cost EMI benefiting both the parties.

Case b) When the interest amount is added to the product price

| Particulars | Amount ₹ |

| Cost of the product | 50,000 |

| Interest to be paid (via EMI) | 4,583 |

| Offer Price (under No Cost EMI) | 54,583 |

| Total amount to be paid by you | 54,583 |

No doubt Consumers will be benefited from the No Cost EMI by not whooping money upfront but at the same time, outdated products may be sold to him. These schemes sometimes lack transparency where product price includes EMI interest. Vulnerable consumers fall into the prey of marketing gimmick of No Cost EMI tends to buy more because of surplus cash (or credit) in hand. These practices/ products thwart the very principle of fair and transparent pricing of products which beholds customer rights and customer protection, especially, in the more vulnerable retail segment. Primary priority should be given to the product. Consumer should not blow all their hard-earned money in one go. They should priorities their needs & wants and shop accordingly. One should ensure sufficient balance in his account to avoid EMI bounce and contemplate the terms & conditions regarding No Cost EMI (especially the duration of the scheme) before selecting the option.

Nicely explained in detail. Thanks

Excellent. Just not look like it is your first article. Keep it up. Long way to go. All the bests.