The valuation of goods is always a matter of concern especially where the goods are imported into India. The value determination may influence the price of goods in India and may impact the competition environment in India. Therefore, proper valuation by custom officer becomes more important and challenging.

As per Custom Act, 1962, the value of goods imported or exported shall be the transaction value i.e. price actually paid or payable subject to condition that,

i) the buyers and sellers are not related

ii) price is the sole consideration for the sale

It becomes more challenging to determine the value of goods when imported from a related party as there are chances of price influence. Related party are defined in Rule 2(2) of Custom Valuation (Determination of Price of imported Goods) Rules, 2007 as,

i. Officers or directors of one another’s business

ii. Legally recognized partners

iii. Employee-employer relationship

iv. Any person controls or holds 5% or more voting power

v. One of them directly or indirectly controls the other

vi. Both of them are controlled by a third person

vii. Together they control a third person

viii. Member of the same family

The valuation of goods is governed by Custom Valuation (Determination of Price of imported Goods) Rules, 2007. As per Rule 3(3) of the said rules, the transaction value shall be accepted if the examination of the circumstances indicates that the relationship does not influence the price. For examination and further investigation into the transactions involving related parties which have the potential to influence the value of goods so imported, Special Valuation Branch (SVB) was created.

The SVBs are presently functioning at the custom houses at Bengaluru, Chennai, Kolkata, Delhi and Mumbai.

Procedure for SVB investigation

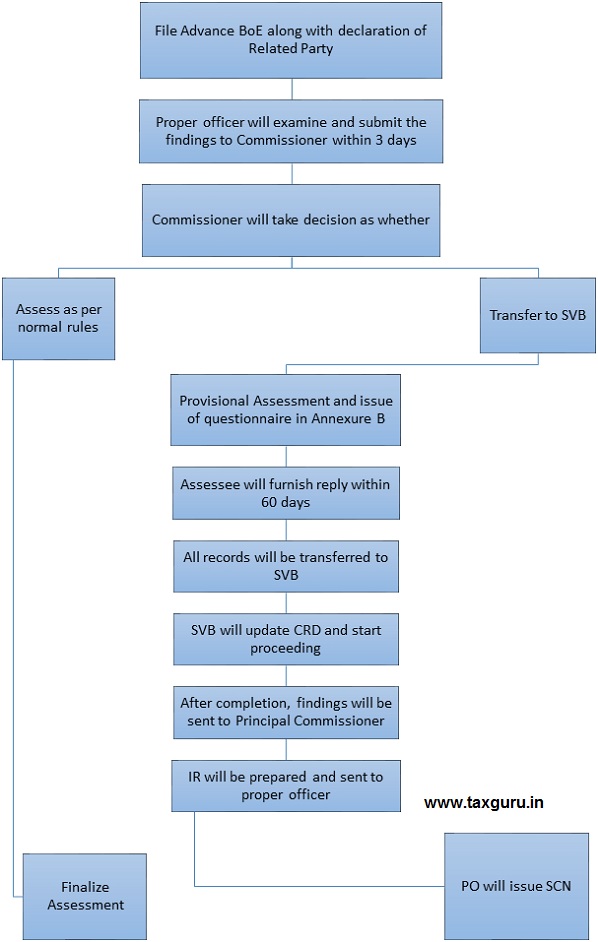

At the time of filing Bill of Entry, importer should also provide information as per Annexure A which is a detailed questionnaire and needs to be submitted only once. Importers are advised to file an advance Bill of Entry so that they get sufficient time for taking a decision on whether the transaction needs to be referred to SVB or not. After the first instance, there would be no need to file advance Bill of Entry.

Within 3 days of filing advance Bill of Entry, the proper officer shall proceed to determine whether the matter should be transferred to SVB. After examination, the proper officer shall submit the findings to the Commissioner for a decision on whether the case should be transferred to SVB or not.

While examining the transaction, the proper officer needs to take into account certain factors which may differ case to case. These factors may include the nature of goods imported, the nature of industry, the season in which goods are imported. It is also important to see whether the difference in value is commercially significant.

If Commissioner is of view that the case is fit for the transfer to SVB, he will direct proper officer to transfer the case to SVB and carry out provisional assessment on the basis of PD Bond without paying any Extra Duty Deposit. Along with the provisional assessment, the Proper Officer, shall require the importer to file further information as required to carry out the final assessment in Annexure B. The importer should submit the documents within 60 days of receiving such requisition from proper officer.

Upon completion of provisional assessment, all records shall be transferred to SVB within 3 working days of releasing goods.

After receiving records SVB initiate proceeding and assign a case number which is then updated in the Central Registry Database (CRD). During the course of investigation, DC/AC may call for further documents and information as required. The importer shall be given proper opportunity as and when required during the investigation proceeding.

The SVB shall complete the proceeding within 2 months of receiving the information in Annexure B which may be extended by taking approval of Jurisdictional Commissioner for further 2 months. The same may also be extended further by taking approval of Chief Commissioner.

After investigation, SVB shall submit the findings to Principal Commissioner for approval and Investigation Report i.e. IR is prepared which is sent to all the custom station where the provisional assessment was done. A copy shall also be sent to DGoV.

When IR is received at custom station, the proper officer shall immediately proceed to finalize the assessment. In case, there is no any variation, the same is finalized. And in case there is variance, the proper officer shall issue a Show-Cause-Notice within 15 days of receipt of IR.

Let’s understand this with an example. X Ltd imported a certain kind of chemical (say, chemical Z) for further processing to produce a final product (say, product T). The chemical Z is so unique that it is used only by X Ltd. However, a product identical to product T is being made in India using a different kind of chemical (say chemical P). At the time of filing advance BoE, X Ltd. declared that the transactional value of chemical Z is US$ 1,000 per carton in Annexure A and declared that the value is approximately closed to the transaction value of chemical P. The transaction value of chemical P is US$ 1,050 per carton. Now, there are three scenarios. All the three scenario are discussed here below,

1. Commissioner is satisfied with the value declared by X Ltd.: In this case, the value of US$ 1,000 per carton will be accepted and the assessment will be finalized.

2. Commissioner seeks further enquiry: In this case, Commissioner will direct proper officer to further enquire into the transaction and clear the goods on the basis of provisional assessment.

3. Transfer to SVB: The Commissioner is of the view that the chemical P used in product identical to product T is generally imported from Middle-East whereas chemical Z has been imported from China. This factor may have a significant influence over the valuation of chemical Z. Therefore, Commissioner will refer the matter to SVB and direct proper officer to clear the goods on provisional basis.

If, in the above example where the proper officer proceeds for the provisional assessment, X Ltd shall file a PD Bond without paying any extra duty.

There is no requirement of renewal of SVB orders now. However, in case where the circumstances or terms and conditions of the agreement changes, the importer shall be required to declare the same at the place of import in Annexure C and the above mentioned proceeding shall follow.

A graphical representation of the whole process is as follows,

About the Author

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.