Case Law Details

S.G. International Vs Commissioner of Customs (CESTAT Mumbai)

CESTAT Mumbai held that detention of export goods in excess of 3 days without bringing to notice of the Commissioner of Customs/ Chief Commissioner of Customs is unlawful and untenable in law.

Facts- The Appellants had exported goods of FOB value of Rs. 6,40,08,136.70/- claiming total drawback for Rs.11,71,805/-, refund of Integrated Goods and Service Tax (IGST) of Rs.42,32,438/- and Refund of State Levies (ROSL) of Rs.6,91,458/- being taxes/duties suffered on the export products. The goods covered by the shipping bills were duly assessed and cleared for export by Customs following the due procedure. The drawback, IGST refund and ROSL amounts as indicated above have been paid to the appellants after the “Let Export Order” grant and shipment of the goods for export.

On the basis of certain intelligence that the exporter had mis-declared the description of the goods and overvalued the exports to avail of an inadmissible higher amount of drawback, refund of IGST, ROSL, the Commissioner (General), JNCH, Nhava Sheva had directed the custodian CFS-JWR, Panvel to put on hold the goods exported by the appellants vide his letter dated 25.10.2018. However, it was reported by the Custodian that the goods have already been gated out from Container Freight Station (CFS) and were found to have been already shipped on board to Lagos by Maersk Line India Pvt. Ltd., in container No. MSKU0011063 on 30.10.2018. The shipping line was then directed by the Commissioner vide letter dated 7.11.2018, to recall back the container. As directed by the Commissioner the container was recalled back by the Shipping Lines on 29.03.2019.

The Additional Commissioner of Customs, JNCH, Nhava Sheva being the original authority had passed an Order-in-Original, wherein the assessable value was redetermined as Rs.2,34,42,440/- under Rule 6 of Customs Valuation (Determination of Value of Export Goods) Rules, 2007; impugned export goods were confiscated u/s. 113 (i), 113 (i)(a) of the Customs Act, 1962 with an option to redeem the goods on payment of redemption fine of Rs.20,00,000/-; imposition of penalty of Rs.40,00,000/- on the exporter u/s. 114(iii) ibid, and Rs.15,00,000/- on Shri Mohd. Siddique Muchhada, Power of Attorney holder u/s. 114AA ibid; besides the eligible drawback was reduced to Rs.5,25,786/- and other eligible refunds were restricted to lower amount than the one claimed by appellants such as IGST reduced to Rs.14,42,877/- from Rs.42,32,438/-, ROSL was reduced to Rs. 2,67,997/- from Rs.6,91,458/-, and MEIS benefits reduced to Rs.4,78,995/- from Rs.13,17,750/.

Commissioner (A) dismissed the appeal. Being aggrieved, the present appeal is filed.

Conclusion- Held that goods could have been provisionally released to the appellants immediately after panchnama proceedings on 10.04.2019, for which the appellant had made request on 12.04.2019, in terms of Circular No 01/2011-Customs dated 4th January 2011. However, there was a failure on the part of Revenue to complete the proceedings early within the prescribed time frame which had not only affected the interests of the exporters, but has also impacted the revenue interests.

Thus, for the limited extent of determination of eligible amount of drawback, arising on account of change in drawback rate alone and not on account of redetermination of the FOB value, we remand the case back to the original authority for this limited purpose.

FULL TEXT OF THE CESTAT MUMBAI ORDER

These appeals have been filed by M/s S.G. International, the exporter and Shri Mohd. Sadique Muchhada, Power of Attorney holder of the said exporter (herein after, referred to as ‘the appellants’), assailing the Order- in-Appeal No. 732 & 733 (DBK)/2021(JNCH)/Appeals dated 20.09.2021 (herein after, referred to as ‘the impugned order’) passed by the Commissioner of Customs (Appeals), JNCH, Nhava Sheva, Mumbai-II.

2.1 The brief facts of the case are that the Appellants had exported goods of FOB value of 6,40,08,136.70/- in eleven Shipping Bills (S/Bs), i.e., 2 S/Bs dated 20.10.2018 and balance 9 C/Bs, all dated 22.10.2018 claiming total drawback for Rs.11,71,805/-, refund of Integrated Goods and Service Tax (IGST) of Rs.42,32,438/- and Refund of State Levies (ROSL) of Rs.6,91,458/- being taxes/duties suffered on the export products. The goods covered by the shipping bills were duly assessed and cleared for export by Customs following the due procedure. The drawback, IGST refund and ROSL amounts as indicated above have been paid to the appellants after grant of “Let Export Order” and shipment of the goods for export.

2.2 Subsequent to the clearance of the goods for exports, on the basis of certain intelligence that the exporter have mis-declared the description of the goods and over valued the exports in order to avail of inadmissible higher amount of drawback, refund of IGST, ROSL, the Commissioner (General), JNCH, Nhava Sheva had directed the custodian CFS-JWR, Panvel to put on hold the goods exported by the appellants vide his letter dated 10.2018. However, it was reported by the Custodian that the goods have already been gated out from Container Freight Station (CFS) and were found to have been already shipped on board to Lagos by Maersk Line India Pvt. Ltd., in container No. MSKU0011063 on 30.10.2018. The shipping line was then directed by the Commissioner vide letter dated 7.11.2018, to recall back the container. As directed by the Commissioner the container was recalled back by the Shipping Lines on 29.03.2019.

2.3 On 04.2019, the appellants had requested Customs authorities for release of the export goods presenting the copies of the purchase orders and Bank Realization Certificates. On 10.04.2019 the goods were examined by the Custom Officers and representative samples were drawn. On 12.04.2019 appellants again requested for the release of goods on the ground that the consignee was awaiting the goods for nearly five and half months and was reluctant to pay the balance amount.

2.4 Investigations conducted by the Customs in the matter involved testing of the representative samples of the export products to ascertain the actual composition of the goods for determination of appropriate classification of the goods and determining respective drawback rate, market survey of the export products to identify the value of the goods in terms of Customs Valuation (Determination of Value of Export Goods) Rules, 2007. In order to avoid any further delay, on 27.05.2019 the appellants had again submitted a letter to the Commissioner (General) for release of the export goods without any personal hearing. By a letter in F. No.SG/MISC-238/2018- 19/CIU/JNCH dated 13.06.2019, the appellants were communicated about the decision of the competent authority for the provisional release of the export goods subject to their furnishing of a bond for an amount of Rs.6,40,08,137/- being the declared value of the export goods and a bank guarantee for an amount of Rs.75,00,000/-.

2.5 Since the appellants found the conditions of provisional release too harsh, they vide their letter dated 06.2019 and 27.08.2019 requested the concerned authorities to allow the goods to be exported without insisting on the conditions of Bank Guarantee or to reduce the amount of bank guarantee. Since department failed to consider the request of the appellants favourably, the appellants had approached the Hon’ble Bombay High Court, by filing writ petition No. 11061 of 2019 for relief. The Hon’ble High Court of Bombay had disposed of the writ petition vide its order dated 13.02.2020 stating asunder:

“4. Keeping all the contentions of both the parties open, we dispose of the petition as above with liberty to the Petitioner to file an appeal.

5. At this stage, the learned Senior Advocate appearing for the Respondents states that in case the appeal is filed within a period of two weeks, the Respondents will not raise an objection regarding limitation. The Tribunal will take note of this stand of the Respondents.”

2.6 As per the order of the Hon’ble Bombay High Court, appellants had preferred an appeal before the Tribunal within two weeks’ Taking the note of Hon’ble High Court’s Order, the said appeal was admitted and held maintainable by the Tribunal vide its Order No. I/07/2020 dated 27.10.2020. Subsequently, after hearing both the parties, this Tribunal had passed the Final Order No. A/85190/2021 dated 29.01.2021 in the first round of litigation. The extract of the relevant paragraphs of the above order is given below:

“4.5 The goods were examined by the departmental officers and the samples drawn on 10.04.2019, as stated by the appellants in their communication dated 12.04.2019, and not disputed by the revenue.

In para 2 of their letter dated04.01.2021, revenue states as follows:

“2. In this regard, it is to inform that on the basis of certain intelligence goods being exported vide 11 shipping bill No. 8371039 & 8371034 both dated 20.10.2018, 8395903, 8395902, 8397436, 8397455, 8397405, 8397409, 839442, 8397410 and 8397426 all dated 22.10.2018 filed by M/s S G International, were kept on hold at JWR CPS vide Hold No 47/2018-19 dated 25.10.2018 by the Central Intelligence Unit, JNCH.

Subsequently, goods pertaining to above shipping bills were examined under Panchnama dated 10.04.2018 in presence of Shri Mohd. Sadique Muchhada, Power of Attorney holder of M/s S G International concern. At the time of time of examination representative samples were drawn and sealed for the purpose of testing and further investigation. On examination, …”

4.7 From the above it is quite evident that goods could have been provisionally released to the appellants immediately after 10.04.2019, for which the appellant had made request on 12.04.2019. Vide Circular No 01/2011-Customs dated 4th January 2011, following clarification has been given by the Board …..

xx xx xx xx xx

4.10 In our view the failure on the part of revenue to complete the proceedings early within the prescribed time frame has not only affected the interests of the exporters, but has also impacted the revenue

4.11 In view of the discussions as above and to protect the interests of the exporters as well as revenue, we are of the view that revenue should finalize the proceedings against the appellants and adjudicate the matter at the earliest preferably within a period of one month from the date of this Principal Chief Commissioner JNCH, Nhava Sheva, should monitor and ensure that these proceedings are finalized and completed within the above time frame.

4.12 In case revenue is not in position to complete the entire proceedings within one month time, then they should allow the provisional release of the detained export goods immediately within a week from the date of receipt of this order, on execution of the bond equivalent to the value of the goods and security in form of Bank Guarantee of Rs 20,00,000/- (Rupees Twenty Lakhs only). While determining the amount of security, we have taken the note of decisions of Hon’ble Punjab & Haryana High Court and Hon’ble Gujarat High Court referred to by the counsel for appellant.

4.13 In respect of detention and demurrage charges in their letter dated 10.2021, revenue has stated as under:

“3. In regards to detention waiver, it is to that this office will follow Regulation 6(1)(l) of the Handling of Cargo in Customs Areas Regulations, 2009 which states that-

The Customs Cargo Service provider shall –

Subject to any other law for the time being in force, shall not charge any rent or demurrage on the goods seized or detained or confiscated by the Superintendent of Customs or Appraiser or Inspector of Customs or Preventive officer or examining officer as the case may be:”

Taking the note of the above submission made by the revenue before us and admitting that these goods have been detained by them, we are of the opinion that these charges should be waived and proper certificate in this regards be issued by the concerned authorities.

5.1 In view of the discussions as above, the appeal is disposed of as per our observations in para 11, 4.12 & 4.13, supra.”

2.7 In pursuance to the above order of the Tribunal dated 01.2021, the Additional Commissioner of Customs, JNCH, Nhava Sheva being the original authority had passed an Order-in-Original No. 593/2020-21/ADC/NS- II/JNCH/CAC dated 27.02.2021, wherein the assessable value was redetermined as Rs.2,34,42,440/- under Rule 6 of Customs Valuation (Determination of Value of Export Goods) Rules, 2007; impugned export goods were confiscated under Section 113 (i), 113 (i)(a) of the Customs Act, 1962 with an option to redeem the goods on payment of redemption fine of Rs.20,00,000/-; imposition of penalty of Rs.40,00,000/- on the exporter under Section 114(iii) ibid, and Rs.15,00,000/- on Shri Mohd. Siddique Muchhada, Power of Attorney holder under Section 114AA ibid; besides the eligible drawback was reduced to Rs.5,25,786/- and other eligible refunds were restricted to lower amount than the one claimed by appellants such as IGST reduced to Rs.14,42,877/- from Rs.42,32,438/-, ROSL was reduced to Rs. 2,67,997/- from Rs.6,91,458/-, and MEIS benefits reduced to Rs.4,78,995/- from Rs.13,17,750/. The appellants had preferred an appeal against the order of the original authority before the Commissioner of Customs (Appeals) who had rejected the appeal by upholding the order of the original authority in the impugned order dated 20.09.2021. Being aggrieved against the impugned order, the appellants have filed these appeals before the Tribunal.

3.1 Learned Advocate for the appellants submitted that the transaction value declared on the shipping bills is genuine and are at arm’s length prices, as the goods are procured from unrelated sellers in the normal course of The statements obtained from the local suppliers by Customs authorities corroborated the fact that the export goods were supplied at the invoice prices indicated therein and that the entire sale consideration was received through banking channel. Further, he stated that value declared in the invoices and the declaration made in shipping bills were fully received in convertible foreign exchange as proceeds of exports, duly evidenced by eleven Electronic Bank Realisation Certificates (e-BRCs). In view of the above and in the absence of any other evidence, they claimed that the transaction value adopted should be applied in the case, and there is no case of over-valuation or mis-declaration on the part of exporters with an intention to avail ineligible export benefits.

3.2 He further submitted that the market survey report relied upon to redetermine the assessable value is vague and does not contain the specifics of the products such as design, size, fabric construction, fabric weight Hence determination of comparable prices without considering these factors is not a fair comparison and not supported by law. The domestic value of goods cannot be used to redetermine the FOB value of the export goods. In support thereof they relied upon the decision of the Tribunal in the case of J. S. Designers Limited Vs. Commissioner of Customs, ICD Dadri (Noida) 2018 (364) E.L.T. 628 (Tri.-All.).

3.3. It is also reiterated by the learned Advocate that the customs authorities have been time and again made aware of the fact that the appellants have already realized the amounts indicated in the shipping bills in respect of exports from its purchasers abroad through banking channels and the consignee was awaiting for export goods. However, despite production of evidence in the form of e-BRCs for the receipt of payments in convertible foreign exchange as per the FOB value of goods indicated in the invoices and shipping bills, these goods have been detained/seized on the ground of over valuation of goods on the basis of market survey. Hence, he claimed that such an action of Customs is contrary to the law and instructions of the department and thus he stated that the impugned order is not sustainable. In support of their stand, they relied upon the judgements of Hon’ble Supreme Court in the case of Commissioner of Customs, Mumbai Vs. TEX AGE 2016 (340) E.L.T. 3 (S.C.) and Siddachalam Exports Pvt. Ltd Vs. Commissioner of Central Excise, Delhi-III 2011 (267) E.L.T. 3 (S.C.)

4. Learned Authorised Representative (AR) reiterated the findings made by the Commissioner of Customs (Appeal) in the impugned order and submitted that the export goods on inspection by Customs were found to be of too small in sizes, which are rightly classifiable as ‘baby garments’ and not as declared by the exporter as ‘boys or girls dress’; further the test results of the samples drawn during the course of examination provide factual position of the composition of the fabric used for readymade garments; these factors necessitated change in classification under Customs tariff and the identification of respective tariff item under Drawback schedule for determination of applicable rate of As regards the valuation of export goods, the market survey conducted by Customs as per report dated 17.05.2019 has been accepted by Shri Mohd. Sidique Muchhada, Power of Attorney holder of the exporter. Accordingly, the original authority had redetermined the value of export goods under Customs Valuation (Determination of Value of Export Goods) Rules, 2007. It is also stated by him that on account of the mis-declaration of the description of export goods and its value, these are liable for confiscation under Section 113(i) and 113(i)(a) of the Customs Act, 1962 and the appellants are liable for penal action under Section 114(iii) and 114AA ibid. Therefore, he stated that the impugned order is sustainable. In support of their stand, he relied upon the judgement of Hon’ble Supreme Court the case of Om Prakash Bhatia Vs. Commissioner of Customs, Delhi 2003 (155) E.L.T. 423 (S.C.) and the order of the Tribunal in the case of American Eye Light Pvt. Ltd. Vs. Commissioner of Customs (Imports), Mumbai 2013 (290) E.L.T. 720 (Tri.-Mum.).

5. Heard both sides and perused the case We have also considered the additional written submissions given in the form of paper books by learned Advocate for the appellants as well as Authorised Representative for the Revenue.

6. From the factual matrix of the case, it is found that the issue involved in the present case is on the aspect of valuation of export goods, and for determination of the fact whether it amounted to over valuation or not; and the proper determination of consequential benefits available to the exporter upon exportation of such goods; and deciding on the basis of the facts of the case, as to whether the export goods are liable for confiscation and whether the appellants are liable for imposition of penalties under the Customs Act, In this regard, we also find that the original authority, on the basis of Final Order No. A/85190/2021 dated 29.01.2021 passed by this Tribunal in an earlier appeal in the very same case, have adjudicated the case by listing out the issues for determination. The relevant paragraph of the Order-in- Original dated 27.02.2021 is extracted below for ease of reference:

“25. I find that the following issues in the instant case:-

i) Whether the description of goods and value thereof declared by the exporter in the S/Bill are correct or otherwise;

ii) Whether the declared total FOB value of 6,40,08,137/- in respect of goods covered under 11 shipping bills are liable to rejection under Rule-8 of Customs Valuation (Determination of Value of Export Goods) Rules, 2007. Whether the market value of the subject goods is required to be redetermined to Rs.2,34,42,400/- under the Customs Valuation (Determination of Value of Export Goods) Rules, 2007;

iii) Whether Drawback, ROSL, IGST refund which is already been paid to the exporter should be recovered with applicable interest, under Rule 17 of the Customs Excise Duties and Service Tax Drawback Rules, 2017 and Section 75A(2) of the Customs Act, 1962

iv) Whether the goods in question are liable for confiscation under the provisions of Section 113(i) of the Customs Act, They have rendered themselves liable to penalty in terms of Section 114(iii) and 114AA of the Customs Act, 1962.”

7. Further, in order to examine the aspect of valuation of export goods, and whether the appellants had failed to declared the correct value or not, the legal requirements as per the Customs Act, 1962 and the Customs Valuation (Determination of Value of Export Goods) Rules, 2007 made thereunder could be perused in The extract of the above legal provisions are as follows:

“Section 14. Valuation of goods. –

(1) For the purposes of the Customs Tariff Act, 1975 (51 of 1975), or any other law for the time being in force, the value of the imported goods and export goods shall be the transaction value of such goods, that is to say, the price actually paid or payable for the goods when sold for export to India for delivery at the time and place of importation, or as the case may be, for export from India for delivery at the time and place of exportation, where the buyer and seller of the goods are not related and price is the sole consideration for the sale subject to such other conditions as may be specified in the rules made in this behalf:……”

“Rule 8. Rejection of declared value. –

(1) When the proper officer has reason to doubt the truth or accuracy of the value declared in relation to any export goods, he may ask the exporter of such goods to furnish further information including documents or other evidence and if, after receiving such further information, or in the absence of a response of such exporter, the proper officer still has reasonable doubt about the truth or accuracy of the value so declared, the transaction value shall be deemed to have not been determined in accordance with sub-rule (1) of rule 3.

2) At the request of an exporter, the proper officer shall intimate the exporter in writing the ground for doubting the truth or accuracy of the value declared in relation to the export goods by such exporter and provide a reasonable opportunity of being heard, before taking a final decision under sub-rule (1).

Explanation . – (1) For the removal of doubts, it is hereby declared that-

(i) This rule by itself does not provide a method for determination of value, it provides a mechanism and procedure for rejection of declared value in cases where there is reasonable doubt that the declared value does not represent the transaction value; where the declared value is rejected, the value shall be determined by proceeding sequentially in accordance with rules 4 to 6.

(ii) The declared value shall be accepted where the proper officer is satisfied about the truth or accuracy of the declared value after the said inquiry in consultation with the exporter .

(iii)The proper officer shall have the powers to raise doubts on the declared value based on certain reasons which may include-

(a) the significant variation in value at which goods of like kind and quality exported at or about the same time in comparable quantities in a comparable commercial transaction were assessed.

(b) the significantly higher value compared to the market value of goods of like kind and quality at the time of export.

(c) the declaration of goods in parameters such as description, quality, quantity, year of manufacture or production.

Rule2. Definitions. –

(a) “goods of like kind and quality” means export goods which are identical or similar in physical characteristics, quality and reputation as the goods being valued, and perform the same functions or are commercially interchangeable with the goods being valued, produced by the same person or a different person;

Rule 3. Determination of the method of valuation. –

(1) Subject to rule 8, the value of export goods shall be the transaction value.

(2) The transaction value shall be accepted even where the buyer and seller are related, provided that the relationship has not influenced the price.

(3) If the value cannot be determined under the provisions of sub-rule (1) and sub- rule (2), the value shall be determined by proceeding sequentially through rules 4 to 6.

Rule 4. Determination of export value by comparison. –

(1) The value of the export goods shall be based on the transaction value of goods of like kind and quality exported at or about the same time to other buyers in the same destination country of importation or in its absence another destination country of importation adjusted in accordance with the provisions of sub-rule (2).

(2) In determining the value of export goods under sub-rule (1), the proper officer shall make such adjustments as appear to him reasonable, taking into consideration the relevant factors, including-

(i) difference in the dates of exportation,

(ii) difference in commercial levels and quantity levels,

(iii) difference in composition, quality and design between the goods to be assessed and the goods with which they are being compared,

(iv) difference in domestic freight and insurance charges depending on the place of

Rule 5. Computed value method. –

If the value cannot be determined under rule 4, it shall be based on a computed value, which shall include the following:-

(a) cost of production, manufacture or processing of export goods;

(b) charges, if any, for the design or brand;

(c) an amount towards profit.

Rule 6. Residual method. –

(1) Subject to the provisions of rule 3, where the value of the export goods cannot be determined under the provisions of rules 4 and 5, the value shall be determined using reasonable means consistent with the principles and general provisions of these rules provided that local market price of the export goods may not be the only basis for determining the value of export goods.

Rule 7. Declaration by the exporter. –

The exporter shall furnish a declaration relating to the value of export goods in the manner specified in this behalf.”

8.1 From the records of the case, we find that the appellants have declared the FOB value of export goods as given in their commercial invoices, which is the transaction Further, submitting the declaration form in terms of Rule 7 above, is primarily the responsibility of the exporter. In the present case, it is not in dispute that the values indicated in the Shipping Bills were matching the value particulars declared in the commercial invoices. Further, any exercise in re-determination of value other than the transaction value has to be adopted step-by-step approach on the basis Rule 3 ibid, and after rejection of transaction value as per Rule 8 ibid. In order to establish the allegation of over-valuation of export goods, it is required to go by an evidence or fact indicating that there was a mis- declaration of value at the time of exports in the shipping bills and the value was re-determined as per the above legal provisions. It is not the case of Revenue that the FOB value of export goods declared in the shipping bills was different from the prices indicated in the invoices. The FOB value and the invoice value of the export goods are same and there is no mismatch. There is not even an iota of evidence produced, either in the form of data relating to value of exports of goods of like kind and quality from the data base maintained by the department, to establish prima facie case of over valuation to reject the transaction value. In fact, the Export Commodity Database (ECDB) of the department which has been developed with a view to checking overvaluation and abuse of export incentive schemes is expected to give the weighted averages, standard deviations, outliers on export data which would help in detecting potential cases of export valuation fraud. As per the scheme, the database is made available to Customs Officers for on- line use to check export value declarations and to take considered decisions on export valuation. In terms of the use of ECDB, the Customs officers at the time of sanctioning the drawback claims are expected to verify the export values declared with ECDB data so that they may utilize the legal provisions to decrease the value for the purposes of sanction of drawback claim. There is no discussion in the order of the original authority or in the impugned order of the Commissioner (Appeals) as to whether in valuation of export goods each of the Rules have sequentially been approached as provided therein and how they adopted the Rule 6 as a last resort and how the other methods of valuation under other Rules were not feasible. Despite the submission of the appellants that they had received the entire FOB value of export proceeds in the form of foreign exchange remittances though the banking channel and submitted the e-BRCs, the original authority in disregard to this factual evidence had simply concluded that the exporter had not produced any documentary evidence in the form of purchase order or contract with overseas buyer; the exporter had admitted in his written submission dated 24.02.2021 that they had received only part payment for six S/Bs so far; and the goods were mis-declared for size and composition. Thus, he concluded that no comparative exports could be relied upon for redetermining the value and hence it cannot be determined under Rule 4 and Rule 5 ibid. However, he relied upon the market survey report of the officers of CIU & SIIB of Customs conducted on 17.05.2009, as it has been conducted in the presence of power of attorney holder of exporter and these were market value of the goods of like kind and quality. Further, the impugned order also reiterated the grounds relied upon by the original authority for adjudging the confirmed demands and for upholding the re- determination of export value, as the investigation officers have followed the provision of Customs Valuation (Determination of Value of Export Goods) Rules, 2007 and have proceeded sequentially and resorted to Rule 6, i.e., market survey; and as per the market survey report, which was conducted along with the representative of the exporter. Thus, the impugned order had re-determined the FOB value of the export goods covered under 11 S/Bs as Rs.2,34,42,440/-as against declared value of Rs.6,40,08,137/-. In the impugned order it is also stated that once mis-declaration is established, the onus shifts to the exporter to establish that the price indicated in the invoice relied upon by him is correct.

8.2 We have also perused the details submitted by the appellants in the eleven e-BRCs in the form of ‘Statement of Bank Realisation’ issued by the Directorate General of Foreign Trade (DGFT) reproducing the information received by DGFT from the banks in secured electronic mode with respect to declared FOB value of export goods against individual shipping bill in respect of exports carried out by the appellants in this The relevant details have been extracted as follows in the form of a table:

SNo |

Shipping Bill No/Date |

Declared FOB (in INR Rs.) |

BRC No. and date |

Date of Realisation of money by bank |

Declared &Realised value of export proceeds in Foreign Currency.(in US $) |

|

|

|

|

|

|

|

Declared |

Received |

1 |

8371039/2 0.10.2018 |

8654326.56 |

INDB0000000001002653 Dated 15.04.2019 |

12.04.2019 |

119205.60 |

104304.90* |

2 |

8971034/20. 10.2018 |

6158294.38 |

INDB0000000001268274 Dated 18.07.2020 |

16.07.2020 |

84825.00 |

74221.86* |

3 |

8395903/22. 10.2018 |

4911390.00 |

INDB0000000001148533 Dated 19.11.2019 |

18.11.2019 |

67650.00 |

67650.00 |

4 |

8395902/22 .10.2018 |

4552020.00 |

INDB0000000000941113 Dated 06.02.2019 |

05.02.2019 |

62700.00 |

62700.00 |

5 |

8397436/22. 10.2018 |

4969615.20 |

KKBK0000958003904634 Dated 20.02.2019 |

28.01.2019 |

68452.00 |

68452.00 |

6 |

8397455/22. 10.2018 |

5758022.16 |

INDB0000000001264222 Dated 13.07.2020 |

09.07.2020 |

79311.60 |

79311.60 |

7 |

8397405/2 2.10.2018 |

5771614.90 |

INDB0000000001263271 Dated 11.07.2020 |

08.07.2020 |

79561.50 |

79561.50 |

8 |

8397409/22. 10.2018 |

5816675.70 |

INDB0000000000971883 Dated 05.03.2019 |

02.03.2019 |

80119.50 |

80119.50 |

9 |

8397442/22. 10.2018 |

5732277.63 |

INDB0000000000971797 Dated 05.03.2019 |

02.03.2019 |

78957.00 |

78957.00 |

10 |

8397410/22. 10.2018 |

5790169.44 |

INDB0000000000930657 Dated 22.01.2019 |

21.01.2019 |

79754.40 |

79754.40 |

11 |

8397426/22. 10.2018 |

5889180.73 |

INDB0000000001263435 Dated 11.07.2020 |

08.07.2020 |

81118.20 |

81118.19 |

|

|

Total |

64003586.70 |

|

|

|

|

* Less Commission charges as applicable.

8.2. From the above factual details of the amount of foreign exchange realized in respect of 11 S/Bs, duly authenticated in the DGFT e-BRC portal, we find that entire amount of export goods in foreign exchange as declared in the respective shipping bills have been realized by exporter-appellants. The above table indicates that in respect of 9 S/Bs at Sl. No.3 to 11 above the full FOB value have been realised, and in respect of 2 S/Bs i.e., Sl. No.1 & 2 above, whole of FOB value less commission charges have been realized. In the said e-BRCs, a note on the realised value has been given stating that the realized value in foreign currency may not include commission. It is also seen that in the above referred two shipping bills, the commission charges have been indicated, and after deducting the same, the foreign exchange received as reported in e-BRC indicate the full amount of FOB in respect of those two shipping bills. In view of the above, we find that the entire FOB value of export goods have been realized as duly reported in e-BRCs. We are surprised to note that how both the authorities below could have ignored the basic facts of bank realization of export proceeds in any export transaction. On the basis of above factual details, we find that the conclusion arrived by the original authority in Order-in-Original dated 27.02.2021 as well as the decision of the learned Commissioner (Appeals) confirming the orders of the original authority in the impugned order dated 20.09.2021, and in more particular the conclusion stating that ‘only part payment against 6 S/Bs has been received’ by the exporter-appellants is factually incorrect. Thus, on this ground alone the conclusion arrived in the impugned order on overvaluation of export goods is liable to be set aside as the same is not legally sustainable.

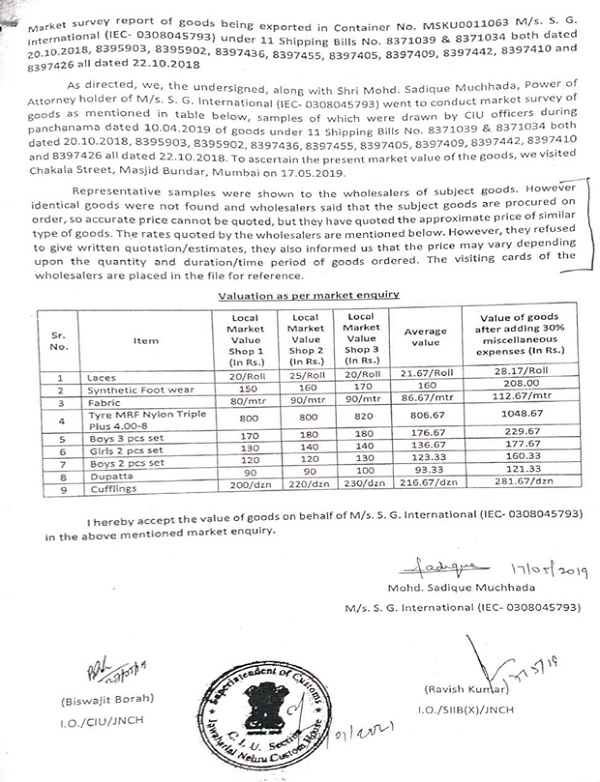

8.3 We have also perused the ‘market survey report’ dated 17.05.2019 in which nine items of the representative samples of export goods drawn during panchnama proceedings dated 10.04.2019, were taken to the local market at Chakala street, Masjid Bundar, Mumbai on 17.05.2019. It is seen from the said market survey report, that the identical goods to that of representative samples were not found in the market and upon showing the samples, the prices indicated in three shops were noted by the Customs officers, as the market value. We further find that the wholesalers from whom the market value was taken as a basis, have stated that accurate price cannot be quoted and they refused to give any written quotation, estimates for the prices mentioned by them. Further the said wholesalers have also informed the Customs officers that the price may vary depending upon the quantity and the duration/time of ordering the goods. Though it is mentioned that the visiting cards of the wholesalers were placed in file for reference, no details to establish the credentials and that the prices quoted are in respect of ‘goods of like kind and quality’ were found in the said markets survey report.

The copy of the said market report, for better appreciation of the facts, is reproduced below:

8.4 In view of the above factual details on the issue of valuation of export goods, we are of the considered view that both the original authority and the learned Commissioner of Customs (Appeals) have not considered the factual details about realization of export proceeds in full as declared in the shipping bills, and on the basis of incomplete details in the ‘market survey report’, without following the rules sequentially as provided under the Customs Valuation (Determination of Value of Export Goods) Rules, 2007 have adopted the indicative prices for the purpose of arriving at the assessable value under Section 14 ibid.

8.5 It is not the case of Revenue that there existed any parallel invoices which are of incriminating evidence to prove that the subject export goods have been over-valued in this Neither was there any data base in ECDB for comparison of transaction value of goods of like kind and quality of those goods that were exported, at or about the same time, to other buyers in the same destination country of importation, nor the value as computed on the basis of cost of production, manufacture or processing of export goods, have been attempted by the authorities below for determining the value of goods in this case. Further, while determining the value as per residual method under Rule 6 ibid, it was nowhere explained how it can be construed that the market survey report prices can be adopted as a reasonable means consistent with the principles and general provisions laid down in these Rules, inasmuch as the local market price of the export goods may not be the only basis for determining the value of export goods.

9. We also find that the Central Board of Excise & Customs (CBEC), Ministry of Finance had issued detailed instructions in Circular 37/2017- Customs dated 09.10.2007, while introducing the Customs Valuation (Determination of Value of Export Goods) Rules, 2007 for the first time. From the perusal of these instructions, it is clear that the Government had spelt out the objective and the manner in which these rules are to be implemented in the field formations, inasmuch as such instructions state that the said rules are meant to provide for a sound legal basis for the valuation of export goods and is also expected to check deliberate overvaluation of export goods and mis-utilization of value based export incentive schemes. It is also mentioned in the said circular, that at the same time of implementing these new Rules, due care has to be taken by Customs to facilitate the movement of bonafide export goods which is vital for the country’s economic growth. The relevant portion of the said CBEC Circular dated 09.10.2007 is extracted below:

“2. The Customs Valuation (Determination of Value of Export Goods) Rules 2007 have been framed in a format similar to the Valuation Rules for the imported goods. Conceptually also, acceptance of Transaction Value for export goods has been emphasized in the said rules, in as much as Rule 3 specifically provides for it.

3. Rule 3 of the said rules also stipulates that the Transaction Value for export goods shall be accepted even where buyer and seller are related, provided that the relationship did not influence the price of the Where the relationship is found to influence the price, as determined by the proper officer on receipt of further information from the exporter, the value of the export goods shall be determined by proceeding sequentially through rules 4 to 6 of the said Valuation Rules. The persons who shall be deemed to be ‘related’ have been specified in Rule 2(2) of the said Valuation Rules, and this provision has been adopted from the Customs Valuation (Determination of Value of Imported Goods) Rules, 2007.

4. Thus transaction value is the primary basis for valuation of export goods and the method specified under Rule 3 will be applicable in the vast majority of cases of export by acceptance of declared In cases where the transaction value is not accepted, the valuation of the export goods shall be done by application of Rules 4 to 6 sequentially.

5. Acceptance of transaction value is, however, subject to the provision of Rule 8 which provides for rejection of declared value for the export goods in certain exceptional These are situations where the assessing officer has reasons to doubt the truth or accuracy of the declared value and further enquiry or investigation is needed to determine the appropriate value. It is hereby instructed that when an investigation / enquiry is undertaken to determine whether or not the Declared Value should be accepted as Transaction Value, the export consignment shall not be ordinarily detained. Wherever there are doubts about the declared value of the export goods, the proper officer shall retain representative sealed samples, wherever considered necessary and feasible, and allow the goods to be exported after due processing. However, it is clarified that in a situation of serious violation such as outright mis-declaration of goods, attempt to export the goods unauthorisedly, i.e., smuggle the goods out of the country, or where there is forgery or fraudulent documentation, the goods may be detained or seized as required. No export consignment shall be detained for reasons of doubts regarding valuation without the approval of the jurisdictional Commissioner of Customs.

6. An ‘Explanation’ relating to rejection of declared value of export goods has been added to Rule 8 to bring clarity and objectivity in exercising the authority for rejection of declared The Explanation clarifies that this rule as such does not provide a method for determination of value, and that it merely provides a mechanism and procedure for rejection of declared value of export goods in certain cases. It also clarifies that where the proper officer is satisfied after consultation with the exporter, the declared value shall be accepted. This Explanation also gives certain illustrative reasons which could form the basis for having doubt about the truth or accuracy of the declared value.

7. While raising doubt about truth or accuracy of the declared value in terms of Rule 8, the proper officer shall issue a query memo specifying reasons for such Meanwhile, the goods will be released for export against a simple undertaking after drawl of representative sample as indicated in para 5. The decision to initiate the process of investigation into valuation aspects, if any, shall be taken at the earliest at the level of Joint/Additional Commissioner.

8. In a case where transaction value cannot be determined or the declared value is rejected under Rule 8, and export value has to be determined by comparison in terms of Rule 4, the proper officer shall take utmost care in selecting an export product for an in-depth inquiry. The proper officer will make the adjustments objectively on the basis of the relevant factors, some of which have been illustrated at sub rule (2) of Rule 4.

9. Where the value has to be determined by Computed value method under Rule 5, the proper officer shall give due consideration to the cost-certificate issued by a Cost Accountant or Chartered Accountant or Government approved valuer, as produced by the

10. It is clarified that the main purpose of introducing the Export Valuation Rules is to provide for a sound legal basis for the valuation of export It is also expected to check deliberate overvaluation of export goods and mis- utilization of value based export incentive schemes. At the same time due care has to be taken to facilitate the movement of bonafide export goods which is vital for the country’s economic growth. The assessing officers shall, therefore, exercise due caution to avoid unnecessary queries regarding truth or accuracy of the declared export value. The Export Valuation Rules are not intended to bring about any significant change in the existing pattern of valuation of export goods. It is the responsibility of the supervisory officers to monitor regularly the export valuation practices, so as to ensure proper implementation of the said Valuation Rules without hindering the flow of bona fide export goods.”

We find that in the present case, none of the instructions, either with respect to determination of value in terms of the extant Rules, or with regard to issue a query memo specifying reasons for raising a doubt about truth or accuracy of the declared value in terms of Rule 8 was raised; further, the instruction for allowing/release of the goods for export against a simple undertaking after drawl of representative sample was also not followed. Even in case warranting seizure or detention of export goods, the provisional release of such goods were not allowed within the prescribed time for allowing it to be exported. In fact, in the present case, the goods had already been exported out of the country and subsequently, the same were brought back into the country, for examination of the export goods and to establish the case of overvaluation. The chronological sequence of events in this case and the action taken by the Customs authorities clearly indicative of the fact that action taken by the Department culminating into the impugned order, is completely in violation of the legal provisions under the Customs Valuation (Determination of Value of Export Goods) Rules, 2007and the instructions issued by the CBEC has elaborated above.

10. Thus, we are of the considered view that the conclusion arrived by the learned Commissioner of Customs (Appeals) on this valuation issue in the impugned order is not supported by any evidence or factual detail, to fasten the penal liability for such over valuation on the appellants and thus the impugned order rejecting the transaction value by confirming the re- determination of assessable value of export goods arrived at by the original authority in his order dated 27.02.2021, is contrary to the legal provisions and the manner provided under Customs Valuation (Determination of Value of Export Goods) Rules, 2007, and thus the same is not legally sustainable.

11. From the records of the case, it is seen that the various test reports given by the laboratories of Textile Committee provided the results in the form of identification of fibre blend composition (%) based on the dry mass with % addition for moisture as per IS 3416:1988 and the details of the sample, whether it is ‘woven’ or ‘knitted’ or ‘non-woven’. In order to illustrative the above, we have seen that in the case of S/B 8397436 dated 22.10.2018, the description of the one of goods as declared in the shipping bill was “Boys 3 PC set”; further, on testing 3 representative samples, the test report given by Textile Committee laboratory vide No.0253061920-1316 dated 04.06.2019 state that it is a “garment (RMG- Ready Made Garment)” of ‘knitted’ type containing cotton in 60.2% and the polyester in 39.8%. Similarly the test reports of other 2 samples vide No.0253061920-1317 dated 04.06.2019 state that it is a “garment (RMG- Ready Made Garment)” of ‘knitted’ type containing cotton in 79.5% and the polyester in 20.5% and vide No.0253061920-1318 dated 04.06.2019 state that it is a “garment (RMG-Ready Made Garment)” of ‘knitted’ type containing cotton in 17.5% and the polyester in 82.5%. We also notice that the drawback schedule specifying the ‘drawback rate’ and the amount of ‘drawback cap per unit’ for various commodities would vary and in respect of the impugned goods such rates may be varying depending upon the composition of the product, whether it is made of cotton; or made of blend containing cotton and the man-made fibre; or of man-made fibres; or of silk; are of wool etc. Thus, in our considered view there is no mis-declaration of the description of the goods and these test results are only helpful in determination of appropriate classification of export goods and for determining the correct drawback rate and other eligible export benefits in respect of the exports, if they are dependent on the customs classification of the goods. Further, in the declarations made by the appellants in the shipping bills, though it is stated that there is a mis-declaration of description of export goods, nowhere in the impugned order there is a detailed discussion on the nature of such mis-declaration and how this had impacted on availment of higher drawback and other export benefits; rather they simply relied on the investigation report of the Customs dated 18.01.2019. The learned Commissioner of Customs (Appeals) conforming the order of Original Authority in the order-in-original dated 27.02.2021 had adopted the workings of redetermining the eligible drawback and other export benefits, as given in the investigation report dated 18.10.2019 for restricting the eligible drawback, refund of IGST, ROSL and MEIS benefits providing the same as annexures ‘A’, ‘B’, ‘C’ and ‘D’ of the said order. This shows that neither was there any independent evaluation of the facts, nor application of mind by the original authority; further, the appellate authority had also failed to examine the facts and evidence relevant to the case, for coming to a conclusion that such restriction of the drawback and other export benefits are in compliance with the legal provisions of the Customs Act, 1962 and the relevant rules made thereunder. Thus, we are of the considered view that conclusion arrived at in the impugned order for restricting the drawback to Rs.5,25,786/- and other eligible refunds of IGST to Rs.14,42,877/-, ROSL to Rs. 2,67,997/-, MEIS benefits to Rs. 4,78,995/- are not sustainable. However, having held that the overvaluation of export goods not having been established as per the legal provisions as discussed in paragraphs 8.1 to 10 above, there is no need for redetermination of eligible export benefits under various schemes except in respect of drawback, where on account of the results obtained in test reports received subsequent to the export of goods, the export goods may have to be classified under appropriate classification in the First Schedule to the Customs Tariff on the basis of such test reports given by the laboratories of Textile Committee and the corresponding Drawback Rates, if it varies, then the same have to be applied for determining the eligible amount of drawback on export of goods. Hence, we consider it appropriate to refer the case to the original authority for the limited extent of such determination of eligible amount of drawback arising on account of change in drawback rate alone and not on account of redetermination of the FOB value, as the same is being set aside by this order. As regards the Rewards under MEIS are concerned since these are payable as a percentage (2%, 3% or 5%) of realized FOB value of covered exports, by way of the MEIS duty credit scrip, the redetermination for a lower amount on the basis of market survey value in the impugned order is not sustainable and the same is liable to be set aside. Further, for refund of IGST as per Rule 96 of the CGST Rules 2017, refund is allowed in respect of IGST paid on goods exported out of India, by matching the details in the shipping bill filed by an exporter with the GST Returns data transmitted by GSTN. The matching between the two data sources is done at Invoice level and the IGST refund module has been designed in line with the above rule and has an in built mechanism to automatically grant refund on the basis of match of the laid down parameters, and hence redetermination of refund of IGST by reducing the eligible amount on the basis of market survey value is not legally sustainable and the same is also set aside. In the ROSL scheme, the Central Government provides rebate of State levies comprising of State VAT/CST on inputs including packaging, fuel, duty on electricity generation and duties and charges on purchase of grid power, as accumulated through the stages of production from yarn to finished garments. Thus, redetermination of the reduced amount of ROSL in the impugned order is liable to be set aside as the same is not legally sustainable.

12.1 It is on record that the export goods in 11 S/Bs have left the ‘Indian Customs waters’ and the export was completed; however due to the instructions of the Commissioner of Customs vide letter dated 11.2018, to recall back the container, the goods that were shipped by Maersk Line India Pvt. Ltd., in container No. MSKU0011063 on 30.10.2018 was called back to JNCH, India on 29.03.2019.Though the appellants had raised an issue on competency of the Commissioner of Customs (General), JNCH, Nhava Sheva as he had no jurisdiction to callback the export goods contained in a container that had already shipping out of India, inasmuch as the instructions issued by the Commissioner of Customs (General), JNCH was on the shipping lines and that the goods had already been made available for further examination by Customs, we do not find it necessary to examine the same here.

12.2 Though both sides have not raised the issue, as a matter of objection, that the subject case deals with the drawback, and thus whether the Tribunal has jurisdiction over it or not, we feel that for the purpose of record it is preferable to make a mention on the correct legal position on the basis of the judgement of the Hon’ble Apex The facts of the present case reveal that the main controversy that is required to be addressed is overvaluation and mis-declaration of export goods and consequential export benefits available to the exporter. Thus recovery of drawback, if any, as being paid in excess is only the consequence and not the issue for determination in this case. Thus by following the judgment of Hon’ble Supreme Court in the case of Asean Cableship PTE Ltd. Vs. Commissioner of Customs – 2022 (380) E.L.T. 4 (S.C.), we hold that the present appeals are maintainable before the Tribunal.

13. The impugned order confirming the original authority’s decision in confiscation of goods and imposition of penalty on the appellants had concluded on the basis of certain findings, mentioned therein. In order to appreciate the facts, and for ease of reference the extract of relevant paragraphs in the impugned order are given below:

“12. …I find that this was a case of deliberate overvaluation and mis- declaration of the goods. If they were a genuine exporter, they would have ensure abundant precaution to ensure the goods entered for export were in tune with the declarations. On perusal of the Order, it is found that Test Report reveals mis-declaration with respect to sizes and composition. The appellant has filed the shipping bills certifying the truthfulness of the declaration. Examination revealed gross over valuation. Records reveal that the goods were carted and would have been exported but for the timely intervention of the Customs Officers. Accordingly it is proved beyond doubt that the exporter appellant has grossly overvalued their declared FOB consequently attempted to claim ineligible benefits on the basis of export documents with malafide intention to defraud the Govt. exchequer, which is undoubtedly in breach of Section 50(2) of the Customs Act, 1962 read with Rule 11 of Foreign Trade (Regulations) Rules, 1993. Thus, there is deliberate mis- declaration, mis-statement and suppression of facts regarding the actual value of the impugned goods on the part of the exporter with malafide intention to claim undue drawback, MEIS and IGST Refund.

14. I have carefully gone through the case when the considered the submissions made by the I find that the impugned Order-in- Original No.593/2020-21/ADC/NS-II/JNCH/CAC dated 27.02.2021has been passed by the Addl. Commissioner of Customs, DBK, CAC (NS-II), JNCH, consequent to investigation information. The Adjudicating Authority has observed that there was no mis-declaration so far as the quantity of the goods declared in the S/bills were concerned, however the description of the goods appeared to be different and also not to be commensurate with the value, classification declared. Samples were drawn in the goods were tested by the Textile Committee. Further, Investigation Officers have followed the provisions of the Customs Valuation Rules, 2007 and have proceeded sequentially and resorted to Rule 6, i.e. market survey and as per the market survey report, which was conducted along with the representative of the exporter, redetermining the value of goods covered under 11 S/bills to Rs.2,34,42,440/- as against declared FOB value of Rs.6,40,08,137/-.

16…. It is a matter of fact that it is proved beyond doubt that the overvaluation was deliberate acts on the part of the exporter which is rendered the goods liable for confiscation under Section 113(i) and 113(ia) of the Customs Act, 1962…

17…. In the instant case, Shri Mohd. Sadique Muchhada, Partner and Power of Attorney holder of M/s S G International is also in-charge of the affairs of the company and solely responsible for the conduct of the company; he has used the documents which are false and incorrect with reference to the value and description, classification with malafide intention to avail and undue/excess benefits. It is evident that the omission and commission on the part of partner have contravened the provisions of Section 114AA of the Customs Act, 1962. Therefore, the original adjudicating authority is fully justified in imposing a personal penalty on the partner other than the penalty on the firm.”

The above extract of the impugned order, clearly indicates that the grounds for confiscation of goods and imposition of penalty on the appellants is mainly on account of overvaluation of goods and the alleged mis-declaration of the description and value of the export goods.

14.1 As regards the issue of overvaluation, our detailed discussion on the facts and evidences on record, and our views and conclusion arrived therein have been explained in the foregoing paragraphs at 1 to 11.It is also on record that the Customs authorities did not seize the goods during its examination and panchnama proceedings conducted on 10.04.1019; however they drew representative samples in order to determine the alleged over-valuation and mis-declaration of export goods. We have already seen that in the earlier round of litigation, the appellants had prayed for provisional release of the export goods covered under detention by the Customs authorities, and they filed an appeal on the ground that the order of provisional release under Section 110A ibid, was too harsh on them. While deciding the case of the appellants in the first round of litigation, this Tribunal had already observed that is was quite evident that goods could have been provisionally released to the appellants immediately after panchnama proceedings on 10.04.2019, for which the appellant had made request on 12.04.2019, in terms of Circular No 01/2011-Customs dated 4th January 2011. However, there was a failure on the part of Revenue to complete the proceedings early within the prescribed time frame which had not only affected the interests of the exporters, but has also impacted the revenue interests.

14.2 In view of the above, we deem it necessary to examine the instructions issued by the Central Board of Excise & Customs (CBEC) in the context of provisional release of goods detained for

“Circular No. 01/2011-Customs

F.No.401/179/2009-Cus.III

Government of India

Ministry of Finance

Department of Revenue

Central Board of Excise & Customs

Room No. 227 B, North Block,

4th January 2011, New Delhi-110001

To

All Chief Commissioners of Customs / Customs (Prev).

All Chief Commissioners of Customs & Central Excise.

All Directors General of CBEC.

All Commissioners of Customs / Customs (Prev). All Commissioners of Customs (Appeals).

All Commissioners of Customs & Central Excise.

All Commissioners of Customs & Central Excise (Appeals).

Subject : Provisional release of export – goods detained for investigation – reg.

***

Sir / Madam,

Attention is invited to the Board Circular No.33/2005-Customs dated 02.08.2005 which contains the instructions regarding provisional release of goods entered for exportation and is seized on the ground of mis-declaration in terms of quantity and value.

2. Instances have come to the notice of the Board that export consignments continue to be detained and not allowed clearance on provisional basis on account of pending test reports/investigations for alleged mis-declaration in terms of quantity, value and description of the In one case it was reported that the detained goods were not allowed to be exported provisionally on the ground that Board’s Circular referred above provides for provisional release of only the seized goods.

3. In this regard it is observed that inordinate detention of the seized goods entered for exportation results in delays in fulfillment of export order and at times cancellation of such Detention of goods also adds to congestion in ports besides resulting in payment of demurrage charges to the Custodians. Accordingly, the matter has been re-examined by the Board with the view to ameliorate the aforementioned difficulties faced by exporters and to streamline the procedure of provisional release/exportation of seized goods/ goods under investigation on account of mis-declaration in terms of quantity and value etc.

4. Seizure should be resorted to only when the Customs officers have a reason to believe that the goods in question are liable to confiscation under the Customs Act, 1962 and thereafter the provisions of Section 110A of the Customs Act, 1962 would come into However, there may be situations when the goods are to be detained for purpose of tests etc. to confirm the declaration. In such cases the endeavour should be to quickly undertake the necessary action (test/enquiry etc.) and take appropriate legal action thereafter so that the period of detention is kept to the minimum. Thus, the following course of action is prescribed in respect of goods entered for exportation:

(a) In case the export goods are found to be mis-declared in terms of quantity, value and description and are seized for being liable to confiscation under the Customs Act, 1962, the same may be ordered to be released provisionally on execution of a Bond of an amount equivalent to the value of goods along with furnishing an appropriate security in order to cover the redemption fine and

(b) In case the export goods are either suspected to be prohibited or found to be prohibited in terms of the Customs Act,1962 or ITC (HS), the same should be seized and appropriate action for confiscation and penalty

(c) In case the export goods are suspected of mis-declaration or where declaration is to be confirmed and further enquiry/confirmatory test or expert opinion is required (as in case of chemicals or textiles materials), the goods should be allowed exportation The exporters in these cases are required to execute a Bond of an amount equal to the value of goods and furnish appropriate security in order to cover the redemption fine and penalty in case goods are found to be liable to confiscation. In case exports are made under any Export Promotion/Reward Schemes, the finalization of export incentives should be done only after receipt of the test report/finalisation of enquiry and final decision in the matter. The Bond executed for provisional release shall contain a clause to this effect,

(d) Export goods detained for purpose of tests must be dealt with on priority and the export allowed expeditiously unless the prohibited nature of goods is confirmed. Continued detention of any export goods in excess of 3 days must be brought to the notice of the Commissioner of Customs, who will safeguard the interest of the genuine exporters as well as the revenue.

5. A suitable public notice for information of trade and standing order for guidance of staff may be issued.

6. Difficulty faced, if any, in implementation of this Circular may be immediately brought to the notice of the Board. ”

On perusal of the above CBEC instructions, we find that the Government had intended to alleviate the difficulties faced by exporters which was arising on account of detention of export goods and consequential delays in fulfillment of export order, payment of demurrage charges by exporters to the Custodians, reducing the period of detention to the minimum, by streamlining the customs procedure of provisional release/exportation of seized goods/goods under investigation on account of mis-declaration in terms of quantity and value etc. We find that by applying the above instructions to the facts of the present case, it is clear that the export goods which were suspected of mis-declaration and where such declaration is to be confirmed and further enquiry/confirmatory test is required (as it is the case textiles materials), the goods should have been allowed for exportation provisionally, in order to safeguard the interest of the genuine exporters as well as the revenue. The detention of any export goods in excess of 3 days must have been brought to the notice of the Commissioner of Customs/ Chief Commissioner of Customs, to ensure finalization of the case. However, none of these instructions were followed in the present case and the goods were kept under customs detention from 10.04.2019 till an order for provisional release was communicated vide letter dated 13.06.2019; and this continued even during the first round of dispute till this Tribunal had passed an order on 29.01.2021, for either adjudication of the case within one month from the date of such order or if that was not feasible, then to provisionally release the detained export goods within a week of receipt of such order on execution of bond equivalent to the value of the goods and security in the form of Bank Guarantee of Rs.20,00,000/-. Further, in the absence of any document or other evidence proving overvaluation of export goods, the claim of the Revenue that the appellants have mis-declared the description of the goods to claim higher ineligible export benefits does not sustain. Thus, we are of the considered view that the action taken by the department in the impugned order for confirmation of the adjudged demands along with confiscation of goods and imposition of penalty on the appellants is not legally sustainable.

15. We also find that the decision of the Hon’ble Supreme Court in the case of Commissioner of Customs, Mumbai TEX-AGE (supra) in Civil Appeal Nos. 4465-4473 of 2008, also supports the views taken by us in this case as above. The extract of the aforesaid judgement is given below:

“The respondents are engaged in the export of readymade garments. It has been making those exports from time to time. These exports were made after fulfilling all the legal requirements. It is also not in dispute that against those exports entire remittance was received by the respondents. The respondents have been claiming duty drawback and other benefits in respect of these exports which were also released to the respondents.

2. However, on the basis of the alleged intelligence received in the Bombay Zonal Unit of Directorate of Revenue Intelligence that the exporter was engaged in the fraudulent exports of low quality readymade garments from Nhava Sheva Sea Port by resorting to overvaluations in order to claim undue export benefits, investigations were carried out and on that basis, show cause notice was issued to the respondents which resulted in imposition of penalty The respondents filed appeal there against before the Customs Excise & Service Tax Appellate Tribunal (CESTAT). The CESTAT allowed this appeal thereby quashing the deduction and the penalties etc. [2008 (221) E.L.T. 395 (Tri. – Mumbai)]. This judgment of CESTAT is under challenge in these appeals.

3. A perusal of the judgment of the CESTAT shows that the entire material placed before it has been discussed and on that basis, a finding of fact is arrived at to the extent that the allegations of flow back of the remittances by way of Hawala could not be proved by the It is further recorded by the CESTAT that the invoices etc. which were raised of particular amounts were duly checked by the Department at the time when the exports were being made. However, the entire amount as reflected in the said invoices was received by the respondents.

4. In view of the aforesaid finding of fact and in the absence of any evidence to show that the money was remitted by way of Hawala, we are of the opinion that the case of over-invoicing has not been established by the We do not find any infirmity in the order of the CESTAT. The finding recorded is a pure question of fact and no question of law arises for consideration.

5. The appeals are, accordingly, dismissed.”

We further find that the case law cited by the learned AR in Om Prakash Bhatia (supra) is not applicable to the present case, inasmuch as the fact of the case before us is fundamentally different. It may be noted that in the present case, the appellants-exporter had produced e-BRC certifying the repatriation of foreign exchange for the full FOB value in respect of all eleven S/Bs through the banking channel as opposed to the case in Om Prakash Bhatia where the exporter had not led any evidence that export value mentioned in the shipping bill was the true sale consideration and the claim for drawback filed by the exporter was withdrawn. Thus, the facts of the present case is distinguishable from the one quoted in the Om Prakash Bhatia (supra) and thus the same is not relevant to this case.

16. In view of the above detailed discussions and findings recorded therein, we conclude that the impugned order upholding the order of original authority in confirmation of adjudged demands, confiscation of goods and imposition of penalty on appellants, is not legally sustainable and hence the same is set Further, for the limited extent of determination of eligible amount of drawback, arising on account of change in drawback rate alone and not on account of redetermination of the FOB value, we remand the case back to the original authority for this limited purpose. Needless to say that adequate opportunity for personal hearing is given to the appellants, so that all the relevant facts are taken into consideration while arriving at such re-determination of eligible amount of drawback in this case.

17. In the result, we allow the appeals filed by the appellants by setting aside the impugned order.

(Order pronounced in open court on 20.11.2023)