The National Financial Reporting Authority (NFRA) of the Government of India has imposed a penalty of ₹4.5 crore on a Chartered Accountant (CA) firm and its associates for audit lapses in the case of M/s Reliance Capital Ltd. The order, issued under Section 132(4) of the Companies Act, 2013, pertains to the statutory audit conducted by M/s Pathak H.D. & Associates (PHD), CA Parimal Kumar Jha, and CA Vishal D Shah for the financial year 2018-19.

Reliance Capital Limited (RCL), a prominent company listed on the Bombay Stock Exchange, engaged in financial services, was subjected to a joint audit by M/s Price Waterhouse & Co LLP (PW) and M/s Pathak H.D. & Associates (PHD) for the said fiscal year. However, PW resigned from the audit without issuing a report, citing suspected fraud in RCL. This raised concerns, prompting NFRA to scrutinize the audit conducted by PHD.

The investigation revealed several instances of non-compliance with the Companies Act, auditing standards, and the Code of Ethics issued by the Institute of Chartered Accountants of India (ICAI). Despite PW’s reporting of suspected fraud, PHD allegedly failed to conduct adequate procedures, leading to material misstatements in RCL’s financial statements.

NFRA found PHD guilty of professional misconduct on various counts, including:

- Failure to Independently Verify Significant Matters: Despite being made aware of significant issues regarding potentially irrecoverable loans and investments amounting to approximately ₹12,571 crore, PHD allegedly neglected to conduct independent procedures, thereby failing in its responsibilities as a joint auditor.

- Engagement in Self-Review: PHD was accused of engaging in self-review by preparing material information for the financial statements, which subsequently became the subject matter of their audit opinion, thus violating ethical standards.

- Misleading Reporting: The audit report issued by PHD included an Emphasis of Matter (EoM) paragraph stating that there were no matters attracting section 143(12), which was deemed misleading and non-compliant with auditing standards.

- Failure to Identify Material Misstatements: PHD allegedly failed to identify material misstatements in RCL’s financial statements, including doubts about the recoverability of loans, adequacy of provisions, and valuation of investments.

- Failure to Assess Fraud Risks: PHD did not adequately evaluate fraud risk factors, leading to non-reporting of material misstatements and inadequacies in the expected credit loss provisions.

After thorough investigation and providing the auditors with an opportunity to present their case, NFRA concluded that the auditors were guilty of professional misconduct. Consequently, monetary penalties amounting to ₹4.5 crore were imposed, along with sanctions barring the engagement partner and quality control review partner from certain audit roles for specified durations.

***

Government of India

National Financial Reporting Authority

*****

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. 008/2024 Date: 12.04.2024

Order under Section 132 (4) of the Companies Act, 2013 in respect of M/s Pathak H.D. & Associates (FRN 107783W) the Audit Firm, CA Parimal Kumar Jha (ICAI Membership No. 124262) the Engagement Partner and CA Vishal D Shah (ICAI Membership No. 119303) the Engagement Quality Control Review Partner

This Order disposes of the Show Cause Notice (SCN) dated 25.07.2023, issued to M/s Pathak HD & Associates, the Audit Firm, CA Parimal Kumar Jha, who was the Engagement Partner (EP) and CA Vishal D Shah, who was the Engagement Quality Control Review (EQCR) Partner, for the statutory audit of Reliance Capital Limited for the Financial Year 2018-19 (the Audit Firm, EP and the EQCR Partner are collectively called ‘Auditors’ hereafter). This Order is divided into the following sections:

A. Executive Summary

B. Introduction and Background

C. Major Lapses in the Audit

D. Findings on the Articles of Charges of Professional Misconduct

E. Sanctions and Penalties

A. EXECUTIVE SUMMARY

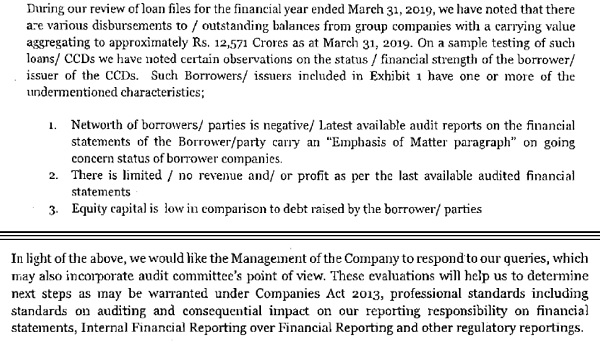

1. Reliance Capital Limited (RCL hereafter), a company listed on the Bombay Stock Exchange, engaged in financial services, was jointly audited by M/s Price Waterhouse & Co LLP (PW) and M/s Pathak HD & Associates (PHD) for the Financial Year 2018-19. The Director General of Corporate Affairs (DGCoA), Ministry of Corporate Affairs (MCA), Government of India, vide its letter dated 29.05.2020 informed the National Financial Reporting Authority (NFRA) that PW had resigned from the audit, without issuing an audit report for FY 2018-19 and filed a report to MCA under section 143(12)1 of the Companies Act, 2013 (the Act) on 11.06.2019. On examination of the matter, it was found that while the ex-auditor PW had filed form ADT-4 with MCA, reporting suspected fraud in RCL, the audit report for the FY 2018-19 issued by PHD on 14.08.2019 stated2 that there were no matters attracting Section 143(12). Hence, we suo motu examined the Audit File of PHD also, under section 132 of the Act, and observed prima facie that there are certain non-compliances with the Act, the Standards of Auditing (SA) and the Code of Ethics, 2009, issued by ICAI. Accordingly, on the satisfaction that sufficient cause exists to initiate action under Section 132(4) of the Act, the subject matter SCN was issued to the Auditors.

2. As per the Consolidated Financial Statements for FY 2018-19, RCL had loans from Banks of around ₹12,000 crore and other external borrowings of around ₹32,000 crores, consisting of debentures, commercial papers and pass-through certificates. RCL was a Core Investment Company (CIC) investing primarily in its group companies. RCL used the above loans and borrowing to extend loans and investments to other group companies. PW reported suspected fraud regarding loans and investments amounting to approximately ₹12,571 crore to some group companies.

3. Despite the reporting of suspected fraud and the resignation by the other joint auditor (PW), the Auditors did not perform adequate procedures as required by the SAs. The material misstatements in the financial statements due to inadequate provision, unjustified valuation of loans and irrational business practices were concurred by the Auditors in disregard of their responsibilities under the Act and SAs. The Auditors also demonstrated a lack of professionalism by rationalising the actions of the Company and ignoring the fundamentals of accounting and auditing.

4. Based on an examination of records and various submissions of the Auditors, including written and oral, this Order concludes that the Auditors failed to meet the relevant requirements of the SAs and violated the Act, and the Code of Ethics in respect of several significant areas of audit. In the areas of the audit identified in this Order, the Auditor was grossly negligent and failed to obtain sufficient appropriate audit evidence to support their opinion, failed to maintain professional skepticism and due diligence, failed to sufficiently and adequately challenge the management assertions and thus failed to identify and report material misstatements in the financial statements of RCL. The major violations discussed in this order include:

a. While PHD was functioning as a joint auditor, PW, the other joint auditor, brought some significant matters to PHD’s notice through various communications starting from the letter dated 24.04.2019. These matters included potentially irrecoverable loans and investments amounting to approximately ₹12,571 crore to group companies portrayed as recoverable. However, PHD failed to carry out any independent procedures on these matters and discharge the responsibilities of a joint auditor in this regard. (Details in Section C1 of this order).

b. PHD indulged in self-review by preparing material information for the financial statements of the Company, which subsequently became the subject matter of their audit opinion, and thus violated the Code of Ethics and SAs. (Details in Section C2 of this order).

c. PHD used the Emphasis of Matter (EoM) para in its audit report in which it concluded that there were no matters attracting section 143(12). The EoM para was in non-compliance with the SAs and was misleading for the users of the financial statements. (Details in Section C3 of this order).

d. PHD concluded without any regard to the merits of the transactions that there were no matters attracting section 143(12). Despite the evidence of documented irregularities in RCL EP did not question the management. In the absence of tests and evidence, the recoverability of the loans of ₹6557 crore (net of impairment) disclosed in the financial statements was doubtful and hence the management’s assertions of the value and rights of these loans were materially misstated in the financial statements, which PHD failed to report. Also, the actual valuation of investments, the rationale for sanctioning loans and investments to potential non-creditworthy entities and the adequacy of provisions remained unverified in all cases. These factors cumulatively contributed to the ROMM due to fraud, which PHD ruled out without adequate audit procedures.

Consequently, the audit opinion of PHD confirming the management’s assertions of a true and fair view of the financial statements is without adequate basis. (Details in Section C4 of this order).

e. PHD failed to notice that the loans amounting to ₹6557 crore (net of impairment) were sanctioned by RCL violating its lending policy and also failed to examine the fraud risk factors. It failed to identify and respond appropriately to the risk of material misstatement due to fraud in management override of controls and revenue. (Details in Section C5.1 to C5.3 of this order).

f. PHD failed to evaluate the adequacy of the expected credit loss provisions of ₹ 2577 crore on loans. This has resulted in the non-reporting of material misstatements in the financial statements. (Details in Section C5.4 of this order).

5. Based on the investigation and proceedings under Section 132(4) of the Act and after giving the Auditor adequate opportunity to present their case, we find the Auditors guilty of professional misconduct and impose through this Order, the following monetary penalties, and sanctions, which will take effect after 30 days from issuance of this Order.

a. Imposition of a monetary penalty of ₹3 crore (Rupees Three Crore) on the Audit Firm M/s Pathak H.D. & Associates.

b. Imposition of monetary penalties of ₹1 crore (Rupees One Crore) and ₹50 Lakh (Rupees Fifty Lakh) respectively on EP CA Parimal Kumar Jha and EQCR Partner CA Vishal D Shah.

c. In addition, EP and EQCR partners are debarred for 10 years and 5 years respectively from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate.

B. INTRODUCTION AND BACKGROUND

6. NFRA is a statutory authority set up under Section 132 of the Act to monitor the implementation of the auditing and accounting standards and oversee the quality of service of the profession associated with ensuring compliance with such standards. The statutory Auditor, appointed by the members of the company under section 139 of the Act is bound by the duties and responsibilities prescribed in the Act, the rules made thereunder, the SA and the Code of Ethics, the violation of which constitutes professional misconduct. NFRA has the powers of a civil court and is empowered under Section 132(4) of the Act to investigate the prescribed classes of companies and impose penalties for professional or other misconduct of the individual members or firms of chartered accountants.

7. The DGCoA, MCA, Government of India, vide its letter dated 29.05.2020 informed NFRA that the ex-auditor (PW) of RCL had filed a report to MCA under section 143(12) of the Act on 11.06.2019 and resigned from the audit engagement on the same date without issuing an audit report for FY 201819. While examining the matter, it was observed that PHD and PW were appointed as joint statutory auditors of RCL for a term of 5 consecutive years at the Annual General Meeting of the Company held on 27.09.2017 and 26.09.2017. PW filed form ADT-4 with the MCA as per the provisions of section 143(12) of the Act and resigned from the audit. Thus, the audit report for the FY 2018-19, dated 14.08.2019, was signed only by PHD. The audit Report contained an Emphasis of Matter paragraph, referring to the matters reported by PW under section 143(12). The EoM stated that “Based on the facts fully described in the aforesaid note, views of the Company, in-depth examination carried out by the independent legal experts of the relevant records, there were no matters attracting the said Section.”

8. We suo motu decided to examine the audit evidence that led PHD to issue the above report and called for the Audit File3 and other information from the Audit Firm and EP CA Parimal Kumar Jha (Membership No. 124262). On 23.12.2021 the Audit Firm requested an extension of time for submission of requisite documents and an extension of time up to 07.02.2022 was allowed. The Audit Firm submitted the Audit File and other documents electronically through File Transfer Protocol (FTP) on 07.02.2022. An examination of the Audit File, annual reports of the Company and other communications by PHD to NFRA showed a prima facie case of professional misconduct on the part of the Auditors.

9. On satisfaction that a sufficient cause exists to initiate action under Section 132(4) of the Act, an SCN was issued to the Auditors to show cause as to why necessary action for professional misconduct should not be taken under Section 132(4) (c) of the Act read with NFRA Rules 2018.

10. EP, the Audit Firm PHD, and the EQCR Partner submitted their respective replies to the SCN on 26.08.2023. After a detailed examination of the replies along with the supporting evidence submitted, an opportunity for a personal hearing was provided to the Audit Firm, EP and the EQCR on 30.01.2024. The Auditors attended the personal hearing along with their legal counsel, Adv. Stuti Gujral. The personal hearing was adjourned to 19.02.2024 at the request of EP. On his request, the Letter from DGCoA and workpaper of PW mentioned in the SCN were also provided to the Auditors vide NFRA email dated 30.01.2024. The hearing was held on 19.02.2024, and the Auditors requested additional time. Accordingly, the hearing was continued on 21.02.2024 through Video Conferencing. The Auditors i.e. the firm, EP and EQCR submitted a written summary of their submissions made during the personal hearing, along with copies of the documents relied upon, on 01-03-2024. All the written and oral submissions have also been examined in detail before issuing this Order.

11. Given the actions and omissions as auditor, leading to their apparent failure to comply with the Act and the Standards of Auditing, the Audit Firm, EP and EQCR Partner were charged with professional misconduct, as conceived in Section 132(4) of the Act of:

a. Failure to disclose a material fact known to him which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where the statutory auditors are concerned with that financial statement in a professional capacity.

b. Failure to report a material misstatement known to him to appear in a financial statement with which EP is concerned in a professional capacity.

c. Failure to exercise due diligence and being grossly negligent in the conduct of professional duties.

d. Failure to obtain sufficient information which is necessary for the expression of an opinion, or its exceptions are sufficiently material to negate the expressions of an opinion; and

e. Failure to invite attention to any material departure from the generally accepted procedures to audit applicable to the circumstances.

C. MAJOR LAPSES IN THE AUDIT

12. We have examined in detail the written replies to the SCN, and the oral submissions made by the Auditors to each of the omissions and commissions leading to the above-mentioned charges as per the SCN. The Auditors have denied all the charges mentioned in the SCN. Only the charges that are proved have been included in this Order.

C.1. Violations of the Responsibilities of Joint Auditor

13. PHD and PW were appointed as joint statutory auditors of RCL for a term of 5 consecutive years at the Annual General Meeting of the Company held on 27.09.2017 and 26.09.2017. As per the agreement between the joint auditors, made as per SA 299(Revised)4, there was no division of audit work among the joint auditors. Hence both the joint auditors were jointly and severally responsible for the entire audit work. While PHD was functioning as a joint auditor, PW brought some significant matters to PHD’s notice through various communications5 starting from the letter dated 24.04.2019. These matters included potentially irrecoverable loans and investments amounting to approximately ₹12,571 crore made to group companies, which were portrayed as recoverable. Despite these communications, EP failed to carry out any independent procedures on these matters as mandated in Para 14, 16 and 17 of SA 299 (Revised) regarding the responsibilities of a joint auditor. Hence EP and the Audit Firm were charged with non-compliance with SA 299(Revised).

14. The EP denied all the charges and submitted that there are no violations of SAs as the records reflect their repeated and consistent efforts to engage with PW as the joint auditor and such efforts were resisted by PW. Based on the “intensive audit procedures” EP concluded that none of the concerns of PW warranted a report under Section 143(12). The Auditors also listed out the WPs to support their contentions and conclusions. On examination of the detailed replies, we observe the following in this regard.

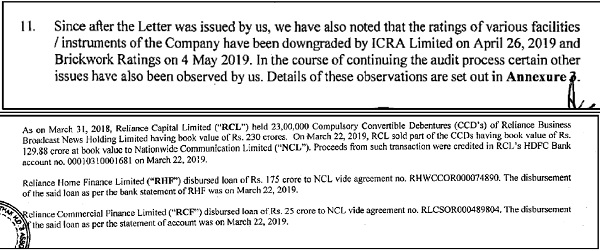

a. In FY 2018-196 RCL had loans from Banks of around ₹12,700 crore and other external borrowings of around ₹32,400 crores, consisting of debentures, commercial papers and pass-through certificates. RCL was a Core Investment Company (CIC) investing primarily in its group companies. On 11.06.2019 PW resigned without issuing an audit report and filed form ADT-4 with the MCA as per the provisions of Section 143(12) of the Act, (i.e., reporting of suspected fraud in the Company). Before the resignation, PW issued a letter dated 24.04.2019 to the Company, copied to the Audit Committee and PHD, regarding its observations concerning loans disbursed, investments, and disposal of Compulsory Convertible Debentures (CCDs) of group companies having a cumulative carrying value of approximately ₹12,571 crore. This letter formed the key basis for PW’s reporting of fraud under section 143(12) of the Act. Following this communication, PW and RCL exchanged various communications7 culminating in the report under 143(12) by PW on 11.06.2019. PHD was copied in these communications. These Group Companies, reported by PW, had serious credit impairment. Many of these group companies used the money to invest in or lend to other group companies with similar credit impairment. The business rationale and recoverability of these loans were not explained.

b. As per the requirements of paragraph 14(c) of SA 299(Revised) PHD was required to agree or disagree with the significant observations raised by PW when they were brought to their notice. However, the Auditors failed to show any evidence in the Audit File of performing any audit procedures to examine and conclude these matters while it was functioning as a joint auditor.

c. PW’s letters dated 24.04.2019 and 14.05.2019 regarding loans and investments were detailed and self-explanatory. The final observations of PW include unresolved issues regarding recoverability, end-use, valuation, unusual mode of transactions and internal control matters. As per the requirements of SA 299 (Revised), EP was required to perform audit procedures and come to an independent conclusion regarding the significant matters. EP examined the issues only after the audit committee specifically asked PHD on 12.06.2019 to examine the issues, i.e. one day after PW filed form ADT-4 and resigned from the Company. From 24.04.2019, when the issue was first raised by PW, till 12.06.2019 EP did not perform any audit procedures on these matters as is evident from the Audit File. There is no evidence in the Audit File that the Auditors disagreed with these observations, as mandated by SA 299 (Revised).

15. We also observe that the written communications between PW and the Company, starting from 25.04.2019, were copied to PHD. On an examination of these communications, as documented by EP, we observe that the contents of these letters are readily understandable. For instance, we note the following from the letter dated 24-04-2019 from PW, addressed to the CFO of RCL and copied to the Audit Committee and PHD.

16. The following are the excerpts from the PW’s letter dated 14.05.2019 addressed to the Audit Committee and CFO, and copied to PHD:

17. On a plain reading of these observations of PW, and the similar other observations contained in their communications, we observe that these were enough to alert the Auditors about possible misstatements due to fraud or error and to invoke the professional skepticism expected of them. However, there is no evidence of any revision in the risk assessment or materiality on account of the information received from PW. There is also no evidence of audit procedures performed in response to these communications on or before the 12th of June 2019, the date on which the Audit Committee asked PHD to examine the matters raised by PW. This conduct of the Auditors is a violation of paragraph 14(c) SA 299 (Revised).

18. The Audit Firm’s claim that they revised the audit strategy on 11.06.2019, before the Audit Committee meeting on 12.06.2019, is contrary to the facts recorded in the Audit File. The WP8 relied upon by EP is dated 12th June 2019 and it specifically mentions that “After discussion with the Audit Committee in their meeting held on June 12, 2019, we conducted a review of the matters raised by PWC in their letter dated May 14, 2019, issued to the management of the Company as part of our audit procedures.” Thus, it is clear from the WP that the Auditors revised the audit strategy and purportedly reviewed the matters raised by PW only at the instance of the Audit Committee. A planning meeting9 with the audit team was held on 11.06.2019, only after PW resigned. Before PW’s resignation neither did EP make any effort to perform audit procedures to evaluate the observations raised by PW, nor was the EQCR partner apprised of the matter.

19. One of the key contentions of EP is that PW did not share the basis/rationale for their letters and there were no new circumstances in FY 18-19 that warranted such a report. EP also argues that PW did not raise such concerns in the previous financial year or during the limited review up to the third quarter of FY 18-19. According to EP, the conclusion of PW “appears to have been influenced by media news” and are “unsustainable”. The Audit Firm goes on to say that it “also appears that PW was finding an excuse to withdraw from the engagement and found an easy route by filing under 143(12) and resigned…..”. We observe, without any comment on the merits of the actions of PW, that the replies of the Auditors are a serious deviation from the fundamental tenets of professional skepticism and professional behaviour10 required of an auditor as per SA 200 and the Code of Ethics 2009. PHD was the statutory auditor appointed under the Act and was responsible for carrying out the audit as per SAs and the Act, and reporting whether the financial statements and accounts represented a true and fair view of the affairs of the Company. Examining and commenting on the conduct of the joint auditor, who is legally on the same footing as that of PHD, is beyond the scope of section 143 of the Act and the SAs.

20. Thus, based on the above, it stands proved that EP and PHD failed to comply with the requirements of SA 299(Revised) regarding the responsibilities of the joint auditor as there is no evidence in the Audit File that the Auditors performed independent procedures on matters brought to their notice and came to any conclusions regarding PW’s observations when it was brought to their notice. Hence the charges in para 13 above regarding violation of SA 299 (Revised) are proved.

C.2. Self-Review of Financial Statements

21. EP and PHD were charged with violations of SA 20011, SA 24012 and the Code of Ethics13 applicable to a Chartered Accountant in Practice, based on the following omissions amounting to self-review of financial statements audited by PHD.

In the Audit Committee meetings held on 12.06.2019, the Audit Committee asked PHD to “fully examine” all the transactions referred to by PW and “provide their well-considered view” to the committee. EP notes this decision as the “mandate” given by the Audit Committee. Thereafter the Audit Committee, on 25.06.2019, noted in their minutes that “in respect of section 143 (12) of the Companies Act, 2013, PHD concluded that, in their opinion, the transactions referred to in the PwC letters do not trigger the provisions of section 143(12) of the Companies Act, 2013.” (Emphasis supplied by us). This was based on a presentation made by EP to the Audit Committee, affirming that the transactions referred to in the PC letters do not trigger the provisions of section 143(12). Before this date, there was no evidence of any independent view taken by the Audit Committee or the Board regarding these transactions, despite receiving various communications from PW since 24.04.2019. This conclusion of PHD is reported in the Director’s report and financial statements, which in turn were audited and reported (including an EoM referring to the same disclosure) by PHD. In light of the above, EP and PHD were charged with preparing material information for the financial statements of the Company, which subsequently became the subject matter of their audit opinion, amounting to self-review.

22. EP denied the charges. He submitted that there is no self-review since they were expected to examine the matters even if the Audit Committee had not requested them to examine it. EP’s submission is that the word “mandate” noted in one of their working paper files should not be given any meaning other than the Audit Committee requesting them to perform what was in any case their duty as statutory auditor of the Company. It further submits that the minutes of the meetings dated 12.06.2019 and 25.06.2019 clearly state that the Audit Committee has conducted a detailed examination of matters. Also, the Board of Directors have taken various initiatives such as legal opinions, before concluding the matter.

23. We examine the detailed replies and observe that EP was required to independently form an opinion on the true and fair view of the financial statements. There is a fundamental difference between the statuary auditor reviewing the work of the preparers independently as compared to, the statutory auditors providing inputs for the company’s records and later on reviewing the same. The financial statements included classes of transactions and account balances arising out of the transactions reported by PW. The financial statements also included a material disclosure14 that the matters reported by PW do not attract section 143(12). Since this disclosure and the related account balances were significant, EP needed to conclude appropriately on the true and fair nature of the numbers and the disclosure. In the backdrop of these responsibilities, we observe the following deficiencies in the audit:

a. In section C1 of this order it has been proved that EP did not perform any independent procedures to agree or disagree with the observations of PW until the date of PW’s resignation i.e. 11.06.2019. Subsequently, in the Audit Committee meetings held on 12.06.2019, the Audit Committee decided to ask PHD to “review and fully examine” all the transactions referred by PW and “provide their well-considered view” to the committee. EP noted this decision as the “mandate” given by the Audit Committee. Thereafter the Audit Committee, on 25.06.2019, noted in their minutes that “in respect of section 143 (12) of the Companies Act, 2013, PHD concluded that, in their opinion, the transactions referred to in the PwC letters do not trigger the provisions of section 143(12) of the Companies Act, 2013.”. This was based on a presentation made by EP to the Audit Committee, affirming that the transactions referred to in the PW’s letters do not trigger the provisions of section 143(12). Before this date, there is no evidence of any independent views by the Board or Audit Committee, which is mandated under Section 177 of the Act to inter alia perform scrutiny of intercorporate loans and investments, valuation of the assets of the company wherever it is necessary, evaluation internal financial controls and risk management system etc. At this juncture, it is crucial to note the requirements under Rule 13 of the Companies (Audit and Auditors) Amendment Rules, 2015. Neither the Board nor the Audit Committee replied to PW after it sent multiple correspondences specifically referring to Section 143(12). The time limit for a reply expected in this case is 45 days as stipulated in sub-rule (2) of Rule 13. But there were no replies from the Audit Committee or Board.

b. The Company then disclosed in the Directors Report that “The company did not agree with the reasons given by PWC for the resignation which were grossly inadequate. The observations given by PWC were examined by the continuing Statutory Auditor of the company. As per the report of the continuing Statutory Auditor, the provisions of section 143(12) of the Companies Act, 2013 did not get triggered. The company had further obtained independent legal opinion from reputed law firm and a senior counsel re-confirming that there were no violations attracting section 143(12) of the Companies Act, 2013.” (Emphasis supplied by NFRA). The Board acknowledged the role of PHD in this disclosure.

c. The above conclusion of EP, as acknowledged by the Audit Committee and the Board, appeared in the financial statements as a material disclosure as follows:

Note 41 (a) Standalone Financial Statements (SFS): “The Company’s previous auditor, after resigning from the office in June 2019 submitted a report under Section 143(12) of the Companies Act, 2013 with the Ministry of Corporate Affairs. The Company has examined the matter and also appointed legal experts, who independently carried out an in-depth examination of the matter and the issues raised therein and have concluded that there was no matter attracting provisions of Section 143(12) of the Companies Act, 2013. The matter is under consideration with the Ministry of Corporate Affairs. (Emphasis supplied by us).

d. This financial statement was then audited and an EoM paragraph was included in the Audit Report referring to the above disclosure note 41(a) by PHD. The EoM para reads as- “We draw attention to Note 41(a) of the Standalone Ind AS financial statements referring to filing under Section 143(12) of the Companies Act, 2013 to the Ministry of Corporate Affairs by one of the previous auditors. Based on the facts fully described in the aforesaid note, views of the Company, in-depth examination carried out by the independent legal experts of the relevant records, there were no matters attracting the said Section”.

24. We now examine how the above material information included in the notes to the financial statements of the Company was prepared by the Auditors and subsequently became the subject matter of their audit opinion, amounting to self-review.

a. The legal expert’s reports obtained by the management, on 07.08.2019, were not based on an investigation of the merits of the issues raised by PW or any “in-depth” examination of the alleged fraudulent loan transactions. They were based only on the correspondence between the Company and PW. The legal opinion was sought and obtained after EP’s conclusion dated 25.06.2019 that the matter did not merit reporting under Section 143(12). This legal opinion was called for to determine whether the facts, circumstances and observations set out in various letters issued by PW were adequate and appropriate for invocation of the provisions of Section 143(12) of the Act. Thus, the Audit Committee as well as the Board’s views on the merits of the transactions were solely based on the conclusions communicated by PHD on 25.06.2019.

b. As confirmed by EP in his reply, the draft note (finally appearing as Note 41(a) in the Standalone Financial Statements (SFS)) was given by the Company to the Auditors only on 13.08.2019 i.e. after EP gave his conclusion on 25.06.2019 that provisions of Section 143(12) of the Act are not attracted in the matter. As explained in paragraph 23(a) above, there was no independent view by the Board or Audit Committee and no disclosure note was made by the management regarding this matter earlier than this date. Thus, there is no evidence to claim that the disclosure note was not based on PHD’s conclusion of the matter. Finally, we note that Auditors audited the same disclosure and stated in its audit report, in the form of an EoM15, that there was no matter attracting section 143(12) of the Act. This clearly amounted to self-reviewing the information prepared by the Auditors themselves. Such review and conclusion on PW’s observations did not come from PHD before the Audit Committee asked them to give a conclusion, even though it was the statutory duty of the auditor to examine and agree or disagree with those observations as per the requirements of SA 299(Revised). The Board or Audit Committee also did not independently form any views on the merits of the allegations raised by PW and went by the conclusions of the PHD.

c. At this juncture it would not be out of place to mention the sequence of events, which is as follows:

i. On 24.04.2019 PW sent a letter highlighting its observations which later formed the basis of fraud reporting by PW under section 143(12) of the Act.

ii. On 11.06.2019, PW resigned as a joint statutory auditor of the Company.

iii. On 12.06.2019 the Audit Committee asked PHD to look into the issues raised by PW and provide their well-considered view.

iv. on 25.06.2019 PHD concluded that no issues were attracting Section 143(12) of the Act and communicated the same to the Audit Committee. The Audit Committee recorded the conclusions in its minutes, which was submitted to the Board.

v. On 07.08.2019 RCL obtained legal opinions, concluding that there were no facts, circumstances and observations set out in various letters issued by PW which were adequate and appropriate for invocation of the provisions of section 143(12) of the Act.

vi. On 13.08.2019 management made the draft financials including the draft of note 41 containing the conclusion of PHD that there were no matters to be reported under section 143(12) of the Act.

vii. On 14.08.2019 audit report was signed by EP, containing the EoM paragraph based on Note 41(a) to conclude that there were no matters to be reported under section 143(12) of the Act.

d. Thus, the sequence of events as mentioned above confirms that the Audit Committee’s conclusion was based solely on EP’s presentation to the Committee in which EP concluded that the PW observations did not attract the provisions of section 143(12) of the Act. The opinions of the two legal counsels did not examine the merits of the transactions. Nor did the PHD subject the points raised by PW to the rigours of audit examination commensurate with fraud risk to agree or disagree with them and arrive at its own conclusions before the “mandate” (discussed in more detail in Sections C1 and C.4). Ultimately the same conclusion appeared in the Board’s Report with acknowledgement of its origin to PHD. It is also disclosed in the Financial Statements in the form of a material assertion. Finally, PHD audited the same disclosure, based on its own opinion, and provided its audit opinion, in the form of an EoM16, that there was no matter attracting section 143(12) in the PW observations. The draft note containing the above disclosure was included in the draft financial statements by the management only one day before the signing of the audit report. Thus, it is evident that the disclosure note emanated from information originally prepared by EP.

e. Reporting under Section 143(12) is a duty cast on the auditor. Section 143(12) mandates that if an auditor of a company in the course of the performance of his duties as auditor, has reason to believe that an offence of fraud involving such amount or amounts as may be prescribed, is being or has been committed in the company by its officers or employees, the auditor shall report the matter to the Central Government. Further, Rule 13 of the Companies (Audit and Auditors) Amendment Rules, 2015 and Form ADT – 4 provide the manner of reporting and SA 240 provides the basic requirements while auditing. These provide that the auditor reporting the suspected fraud will first take it up with the Audit Committee and the Board seeking their views within 45 days and then file the report in the form ADT-4. All these stipulations when read together make it clear that the reporting on fraud in the course of performance of duties as an auditor is applicable when the auditor has reason to believe and has knowledge that a fraud has occurred or is occurring based on evidence obtained and the professional judgements made. Once it is reported to the MCA, the legal determination of the fraud and admitting or ruling out fraud is a regulatory matter. Neither the Company nor the auditor is competent to make a conclusive legal determination17 of a statutory matter reported by the auditor as per his evidence and mandate provided in the Act. The normal course of action in this situation for any prudent Company could be initiating an independent investigation into the alleged matters to bring out the truth. However, the points raised by the PW were not responded to by the Audit Committee and the Board within 45 days following which PW reported the matter under section 143 (12) and also resigned on 11.6.2019. The Audit Committee and the Board thereafter asked the PHD on 12.6.2019 to examine the matter and EP shortly thereafter on 25.06.2019 ruled out any fraud based on their interpretation of the Law and limited and inadequate examination of data produced by the RCL. Using this conclusion of PHD the Company management, its Audit Committee and the Board acquitted themselves of their statutory responsibility in respect of an alleged fraud against them. EP and the Audit Firm, PHD, in turn, became a willing accomplice by displaying gross negligence of their statutory responsibility.

25. Thus, in this case, PHD ruled out fraud reported by another joint auditor (PW). Also, they did so on being asked by the Audit Committee. It may be noted that the Audit Committee had not even responded to the points raised by PW within the 45 days statutory limit. The management used PHD’s said work (done without adequate rigor) as a disclosure in the financial statements. These financial statements were then audited and an EoM was then included in the Auditor’s report that relied on the disclosure made by the management (which itself was based on the Auditor’s examination). Thus, the actions of PHD amount to self-reviewing the financial statements. Hence the charges in para 21 are established.

C.3. Use of Emphasis of Matter (EoM)

26. As explained above, EP used an emphasis of matter paragraph in their audit report to state that the report filed by the resigned joint auditor does not attract section 143 (12). EP also documented in the Audit File that the PW’s reporting was unwarranted. Its replies to the SCN also underline the same. In this regard, EP and the Audit Firm were charged with issuing an EoM without basis and in violation of Paragraph 8 of SA 706 (Revised).

27. EP denied the charges. On examination of the detailed replies and evidence, we observe the following.

28. In the backdrop of the sequence of events mentioned in paragraph 24(c) above, we now examine the EoM and its shortcomings from the perspective of compliance with the standards. A plain reading of the EoM (quoted in paragraph 23(d) above) shows that the Auditors are taking refuge under the legal opinion for determining that section 143(12) was not attracted. However, a perusal of the sequence of events shows that the determination was made by the Auditors way back on 25.06.2019 (within 12 days of being asked by the Audit Committee), whereas the legal opinion came only on 07.08.2019. Further, the conclusion of the legal experts, that there were no matters attracting section 143(12) was not based on the merits of the issues raised by PW, instead, it was based only on the correspondence between PW and the Company. Also, although it is the admitted position of EP that he has not relied on legal opinions, however, the EoM shows his reliance on the legal opinion because it talks about the examination by legal experts. Hence, this representation in the EoM is misleading for the users of the financial statements and goes to show the unprofessional behaviour of the Auditors.

29. Notwithstanding the above misrepresentation in the EoM, it is also not in accordance with the requirements of the standards. As per Para 8 of SA 706 (revised)18 if the auditor considers it necessary to draw users’ attention to a matter presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance that it is fundamental to users’ understanding of the financial statements, the auditor shall include an EoM paragraph in the auditor’s report, provided the auditor would not be required to modify the opinion in accordance with SA 705 (Revised)19 as a result of the matter. However, as explained in subsequent sections of this Order there were material misstatements since the irrecoverable loans were shown as recoverable by the management. This called for a modification in the audit report as per SA 705 (Revised) as the amounts involved were material. Therefore, the EoM based on Note 41 (a) regarding the PW matter was not in accordance with SA 706 (Revised).

30. As explained in the pre-para the EoM was not the appropriate form of reporting; instead, the Auditors should have modified their report. Without prejudice to the above, however, we examine the EoM para for its compliance with para 9 of SA 706 (Revised). This para makes it clear that the EoM paragraph shall refer only to information presented or disclosed in the financial statements and indicate that the auditor’s opinion is not modified in respect of the matter emphasized. Thus, before providing an EoM, it must be ensured that the subject matter of the EoM is appropriately presented or disclosed in the financial statements. The subject matter in note 41(a) was a subsequent event after the reporting period and hence covered under Ind AS 1020. This standard requires disclosure for non-adjusting events or adjusting the amounts recognised in its financial statements to reflect adjusting events after the reporting period. The reporting of fraud is normally an adjusting event. However, the Company disclosed its judgment that the matter was not reportable under section 143(12) and hence treated it as a non-adjusting event. The disclosure notes identify two events, i.e. the reporting of fraud by the previous auditors under section 143(12) and the initiation of regulatory action by the MCA. Ind AS 10 requires disclosure of the nature of the event and an estimate of its financial impact or a statement that such an estimate cannot be made. However, the note to the financial statements does not give the nature of these two events, such as the subject matter of the report under section 143(12) and the nature of the action initiated by MCA. The nature and impact of the issues raised by the previous auditor were the crux of the matter and critical. Though the Company took the view that the issues raised by the previous auditor did not fall under section 143(12), the issues pointed out by the resigned auditor (PW) were such that they may result in accounting adjustments such as write-off of the company’s assets due to the dubious nature of the loans granted, litigation expenses, compliance cost, loss of goodwill, action by lenders etc. There is neither disclosure in the financial statements of an estimate of such financial impact nor a statement that such an estimate cannot be made. There is no evidence in the Audit File of EP’s examination of any of the above-mentioned matters, which shows gross negligence by EP.

31. Thus, the EoM was based on matters which were not adequately disclosed in the financial statements. Apart from referring to Note 41(a) the EoM also contains PHD’s finding (which was already documented in the WP well before the Board noted this) that the matters reported by PW do not attract Section 143(12). The EoM did not mention that the audit opinion is not modified in this regard.

32. The above actions of PHD violate SA 706(Revised). Because of these violations, the Audit Report provided a misleading impression to the users. As demonstrated by the Audit File, neither RCL nor PHD fully examined the issues raised and reported by PW to conclude that there was no fraud.

33. Based on the above, the charges of issuing a misleading EoM without adequate basis stand proved.

C.4. Impact on Financial Statements of Matters Arising out of the Observations of the Resigned Auditor

34. With respect to the issues pointed out by PW before resigning, EP and PHD were charged with the following.

a. Failure to exercise professional skepticism while examining PW’s observations as PHD failed to assess the impact of these transactions on the Risk of Material Misstatements (ROMM) due to fraud.

b. Failure to challenge the management and also failure to perform audit procedures as required by paragraphs 12 to 14, 23, 24, and 28 to 33 of SA 240.

c. Failure to examine how the assertions in the financial statements were impacted by such deficiencies. The financial statements were materially misstated, as several irrecoverable loans and investments were portrayed as recoverable, but the same were not reported. Therefore, the Auditor’s opinion on the financial statements is without adequate basis.

d. Failure to assess the end use of loans to understand any issues relating to their recoverability. There is no evidence of independent verification of whether loan funds were used by the borrowers for the same purpose as disclosed by the borrowers at the time of sanction of the loan. Therefore, EP and PHD were charged with failure to comply with Paragraphs 22, 30, and 33 of SA 240.

35. As explained in the previous paragraphs of this Order, Auditors formed a conclusion that the matters reported by PW do not attract Section 143(12) of the Act. Without prejudice to our observations above, we note that the statutory duties of the auditor require them to form an opinion on the financial statements as a whole, including the effect of the matters brought to the notice by the erstwhile joint auditor. We also note that EP formed a conclusion on these matters without performing adequate audit procedures and obtaining sufficient appropriate audit evidence as required by SAs.

36. EP’s submission in this regard is that all the observations raised by PW were present in the earlier years as well. According to EP, his observations were based on a thorough and objective examination of the facts of the case, whereas PW appears to have been influenced by news reportage around that time on matters involving other NBFC/HFC entities, to draw illogical and unmerited conclusions about the Company. EP also stated that PHD had carried out a factual verification of the issues raised by PW.

37. We have examined the replies and the work of the Auditors concerning the major observations raised by PW. The major issues raised by PW and the conclusions documented by EP in his presentation to the Audit Committee21 are as given in the following table, with emphasis added by us where EP agreed and noted the same observations as PW.

| Sl. No. |

Issue Raised by PW | PHD’s Conclusions |

| 1. | As per the latest available financial statements of the borrower, the net worth of the entities was negative. The audit report on the financial statements of the borrowers carried an EoM on the going concern assumption. (PW has given a list of 13 borrowers aggregating to approximately 12,571 Crore) |

Out of 13 entities mentioned by PW, 11 had negative net worth, out of which 7 entities have issued CCDs to RCL. If these CCDs are considered equity instruments, then the net worth would become positive. In 1 case exposure of ICD is ₹581 crore, where the net worth is negative ₹7 crore. In the case of the remaining 3 entities total exposure is ₹44 crore, and negative net worth is in lakhs. |

| 2. | As per the latest available financial statements of the borrowers, the debt-equity ratio is more than 10 or negative. | “As the net worth in most cases is negative, the debt-equity ratio can’t be ascertained. However, the CCDs if considered equity,

the debt-equity ratio would improve |

| 3. | The loan balance confirmation circulated to the borrower (on the basis of the authorisation letter provided by the management) has not been responded till date. |

“As per the mails provided to us by the Company, confirmations have been sent to the PW team subsequent to May 14, 2019”. |

| 4. | Based on the records available on the website of the Ministry of Corporate Affairs for the borrower entity, either no/inadequate charge has been created. |

“Observation was raised with regard to 7 entities. In case of 6 entities charges were created before 14.05.2019. In case of 1 entity charges has been created on 17.05.2019”. |

| 5. | Credit Appraisal Memo (CAM) does not adequately cover the credit assessment of the borrower entity and the basis of granting the loan. | i. CAM does not contain appraisal notes of these loans. The Repayment capacities of the borrowers were not analysed. The loan amount sanctioned is disproportionate to the financial strength of the entity.ii. All the loans are given for general and corporate purposes. The purpose of the loan is onward lending, however, no assessment of the ultimate borrower is done.iii. Delays have been observed in servicing interest and principal repayment by the borrower. Despite the delays mentioned above, the Company continued to disburse loans to the borrower. The risk analysis section of CAM does not contain in particular the risk involved in the lending and mitigation policies for those risks.iv. While sanctioning the loans, the liquidity of the underlying assets has not been considered. |

v. ICDs have been given even in cases where there were material provisions made in the case of investments in CCDs of these entities.

38. We observe that the matters noted by EP in the Audit Committee presentation (emphasised in the above table) evidence credit impairment of the borrowing entities. This has a direct impact on the recoverability of the loans. However, EP failed to do any testing to rule out that impairment of such loans was not required. The merits of each of the above are discussed below.

a. Regarding the classification of CCDs fully as equity (sl. no. 1 in the table above), EP replied that while Ind AS 3222 necessitates its categorisation as debt due to the absence of a strict fixed-to-fixed ratio, this classification pertains only to “surface representation”. We observe that as per Ind AS 32, the contractual terms of the CCDs shall be assessed to find out the substance of the transaction, rather than its legal form, to determine whether it is a financial liability or an equity instrument. Thus, the presentation of the financial instruments is also as per the principle of substance over form. Further, if as per the terms of the contract, CCDs are classified as a compound instrument then the full amount cannot be considered as equity23. The value will have to be split between the debt and equity components. There is no evidence of such an assessment done by the Auditors. Thus, EP’s conclusion that “If these CCDs are considered as equity instruments, then the net worth would become positive” is baseless. This observation of EP gives only a possibility (use of “if” condition), and not a professional judgment and conclusion based on recorded evidence to support the audit opinion.

b. Regarding the credit impairment of the borrowers (sl. no. 1 and 2 in the table above) we observe that out of the 13 borrowing entities reported by PW under section 143(12) of the Act, 11 entities were incurring losses, their net worth was completely eroded, and their auditors had reported EoM paragraphs on their being Going Concern. These borrowing entities further invested the borrowed monies in similar entities having weaknesses like negative net worth, losses etc. This posed a serious threat to the recoverability of all these loans. The above and the other factors evidence credit impairment of these loans. But EP conducted no substantive audit procedure or adequate verification to rule out the non-recoverability of these loans; nor was adequate provisioning done. Instead, EP has mentioned in his reply that he relied on comfort letters provided by the promoter group companies, Reliance Innoventures Private Limited and Reliance Infrastructure Limited, in support of the recoverability of these loans highlighted by PW as being impaired. We note that in the WP24 titled closure document, it is documented that the financial strength of these promoter group entities had weakened significantly and they were under stress hence reliance had not been placed25 on the comfort letter while evaluating the recoverability of loans. Similarly, the WP ‘exposure analysis’, relied on by EP for the value of the loans and end use, evidences the irrecoverable loans as most of the loans are used for debt servicing by credit-impaired entities. Moreover, not even in a single case did EP document the ultimate utilisation of funds to understand the exact business purpose and the ultimate beneficiary of this web of multiple layers of transfer of money. There is no independent examination of the cash flow projections of any of these entities to understand the repayment capacity. EP has simply copied data from the financial statements (several financial statements are as on 31st March 2018) and other information provided by the management without any independent examination. None of these data establishes cash inflow streams for any of these entities to ensure repayment capacity and the value of these loans shown as recoverable in RCL’s financial statements.

c. Regarding the non-availability of direct balance confirmations from the borrowers (sl. no. 3 in the table above), we note that except for a few borrowers, there is no evidence to prove that these confirmations were received directly from the borrowers. Thus, the balance confirmations were not in compliance with the requirements of SA 50526. Notwithstanding the above, it must be noted that receiving balance confirmation does not evidence the recoverability of the loan, which was the core issue pointed out by PW in its letters. Further, the documents given by EP along with his reply do not form part of the audit file and hence cannot be entertained.

d. Regarding the creation of charges on assets by the borrower entities (sl. no. 4 in the table above), we observe that there is no adequate evidence in the Audit File that the assets on which the charges are stated to be created existed in the books of the borrower entities. Also, there is no assessment of whether the value of the assets on which the charge has been created covers the full value of loans taken from RCL. Since the assets on which charges were created were in the form of loans and investments in credit-impaired entities, EP was required to assess the value of those investments to conclude that charges were appropriate.

39. Apart from the above, we observe the following deficiencies also in the overall work of the Auditors regarding the recoverability of the loans, arising out of issues mentioned in sl. no. 1 to 1, 2, 5 and 6 in the table above.

a. We observe that as per the Credit Appraisal Memo (CAM), the purpose for which the loans were sanctioned was ‘General corporate purpose and onward lending’. This means that loans were sanctioned for business purposes or onward lending by the borrower. The WP titled ‘Loan End Use Details27 documents end-use details of 3 borrower entities28. The end use was documented as debt servicing/repayment, investments, “Opex” and onward lending. However, the business activities of none of the borrowers were documented to confirm whether the loans sanctioned were utilised for genuine business purposes.

b. As per the WP, out of ₹6577 crore of loans, ₹6252 crore is shown as utilised for debt servicing or repayment. These are potential cases of the evergreening of loans where the previous outstanding loans were repaid out of new loans sanctioned. There is no examination of the bank statements to rule out the possibility of evergreening, despite the indications of circular transactions noted by PW.

c. For all the 3 borrower entities mentioned in the WP29 the CCDs earlier advanced by the Company were completely written off, yet new loans were sanctioned in the FY 2018-19 pointing to their future non-recoverability.

d. EP’s contention that borrower entities have not made continuous default in repayment of their obligations “except for delays of few days” is misleading. Contrary to this statement, the Audit File records that there were significant delays, not just a few days, in servicing interest and principal ranging from 60 to 151 days.

e. Further, EP’s reliance solely on management representation is not in compliance with the requirements of para 3 of SA 580, which states that written representations do not provide sufficient appropriate audit evidence on their own about any of the matters with which they deal.

f. Our observations on EP’s assessment of the risk of material misstatements in the financial statement due to fraud are given in section C.5 of this order. We observe that no adequate consideration of fraud risk factors was given by the Auditors.

g. Although both PW and PHD, have noted that there were borrowing entities that had no employees, had assets only in the form of loans and advances and investments and had minimal capital, the Auditors have not performed any audit procedure to rule out the possibility that the loans and advances and investments were not being made in companies, that are like shell companies established to route the funds to other entities. Serious issues of credit impairment, and going concern issues relating to the borrowers were completely ignored by the Auditors, despite the red flags raised by the joint auditor before resignation. This indicated gross negligence and noncompliance with the statutory duties of an auditor.

40. All of the above shows that EP neither did adequate audit procedures, nor challenged the management on the irregularities in the sanction of loans, and reached a conclusion that the issues raised by PW were not attracting the provisions of section 143(12) of the Act. In reaching such conclusions the Auditors violated the applicable SAs as well. In the absence of tests and evidence, there was no assurance about the recoverability of the loans and hence the management’s assertions about the value and rights of these loans were materially misstated30 in the financial statements, which PHD failed to report. Also, the actual valuation of investments, the rationale for sanctioning loans and investments to potential non-creditworthy entities and the adequacy of provisions remained inadequately examined in all cases. These factors cumulatively contributed to the ROMM due to fraud, which PHD ruled out without adequate audit procedures31, despite having been raised by the resigned joint auditor. The conclusion drawn by the Auditors that there were no material misstatements in the financial statements, either due to fraud or error, is therefore without adequate basis since there is no sufficient evidence showing that the loans of ₹6557 crore (net of impairment) disclosed in the financial statements are fairly presented and are fully recoverable. Consequently, the opinion of PHD confirming the management’s assertions is without adequate basis. Hence, the charges mentioned in para 34 and 35 above are proved.

41. Such lapses in adequately responding to audit risks are viewed seriously by international audit regulators. In the matter of Ciro E. Adams, CPA, LLC, and Ciro E. Adams, CPA32, the US audit regulator PCAOB imposed sanctions on an auditor for failure to obtain sufficient appropriate audit evidence supporting significant accounts, including accounts designated as a fraud risk or significant risk and not complying with multiple PCAOB auditing standards. The sanctions included censuring the Firm and Ciro E. Adams (Adams), revoking the Firm’s registration, barring Adams from being an associate person of a registered public accounting firm, and requiring Adams to complete 40 hours of continuing professional education and a civil money penalty of $40,000.

C.5. Other Omissions/Commissions in Obtaining Sufficient Appropriate Audit Evidence in Key Areas of Audit

C.5.1. Verification of Lending Policy

42. EP and PHD were charged with the failure to obtain sufficient appropriate audit evidence as required by SA 50033 regarding compliance with the Lending Policy despite observing marked deviations from the auditee’s lending Policy documented in the Audit File.

43. EP submitted that the decision-making process lies in the hands of its management and the auditor has no role in these decisions. PHD submits that it understood that the policy and the weaknesses in internal control had been reported in the qualified opinion on its report on Internal Controls over Financial Reporting (ICFR).

44. In this regard we observe as follows:

a. In the WP “Audit Planning Memorandum” EP identified Loans as a Significant Risk/Fraud Risk. A review of the Lending Policy was one of the audit procedures planned to address the risk. Accordingly, EP documented the Lending Policy. The testing of compliance with the policy by EP was limited to loan approval by the authorised officer as per the policy. We note that the Lending Policy34 of the Company states that “The lending would be based on the Company’s judgement on, ability to pay, logical reasons for why the borrower has opted for the Company, the possibility of recovery on time, opportunities, future potential etc…….. The basic financial ratio, diversification of earning, alternate source of repayment, borrowers’ trade cycle, market reputation, and capital structure, would be considered either on a discrete or aggregate basis. While the financials would be taken into consideration in making the judgement, the same would not be the sole criterion for sanction or otherwise. Thus, the Company would go beyond numbers while extending any financial assistance. The probabilities and the reasons for which repayment may not happen as expected would be explored/tested while making such call.”

b. However, the disbursements made by the Company were not in line with the above requirement of the Lending Policy, as evidenced by the observations made by PW and the CAMs documented by EP (e.g. borrowers like Reliance Venture Asset Management, Reliance Digitech, and Reliance Alpha). The presence of the lending policy in the Audit File and documentation of the glaring deviations from the policy evidence that Auditors were aware of the deviations. The policies and procedures set by those charged with governance form the basis of the internal controls of a Company. Such deviations from the policy are evidence that the internal controls over loan sanction and monitoring were not functioning properly in the Company. These deviations also indicate management override of controls in loan sanctioning and hence a fraud risk. A qualified opinion under ICFR does not absolve EP of his responsibility to report on this non-compliance. On the contrary, it shows that weaknesses in loan sanctioning and monitoring were overlooked by EP who chose to take refuge under the qualified opinion in ICFR which mentions only a weakness in loan documentation.

c. EP responded that the Lending Policy is a management decision and that the auditor has no role in its verification, is misplaced and shows a poor understanding on his part, of the requirements of the Standards and the Law. Section 143(1)(a) of the Act requires the auditor to inquire into whether loans and advances made by the company have been properly secured and whether the terms on which they have been made are prejudicial to the interests of the company or its member Thus, though the Company has the discretion to determine the terms and conditions of sanctioning the loans, the auditor must inquire whether or not those loans are prejudicial to the interest of the Company. RCL is a Core Investment Company. Its business involves transacting in loans to group concerns, its major income is from interest and the strength of the Company is derived from its loans and investments. Thus, if the Company is investing in entities which are credit impaired/ financially weak, in violation of its own lending policy, then it is prejudicial to the interest of the stakeholders. The recoverability of the loans was also required to be assessed properly and adequate provisions needed to be made in the accounts where necessary. Not evaluating this work of the auditee shows gross negligence and a lack of professional skepticism on the part of the Auditors.

45. In light of the above, all the charges in paragraph 42 of failure to obtain sufficient appropriate audit evidence regarding compliance with lending policy stands proved.

C.5.2. Direct Confirmation

46. EP and PHD were charged with non-compliance with requirements of para 26 of SA 33035 in analysing contradictory audit evidence. While it was documented36 that the ICD given by RCL amounting to ₹581 crore was not reflected in the books of Reliance Integrated Services Limited (RISL), there was a balance confirmation for this amount documented in the Audit File.

47. EP submitted that the matter was conveyed to the Company and the Company informed that RISL netted off the loan from RCL and the onward lending it made to Reliance Communications and it is a matter of presentation only. This is a post-dated rationalisation and cannot be accepted for the reasons discussed below.

48. We observe that the total balance sheet size of RISL for the FY 2017-18 was only ₹20.7 crore, without the above-said transaction. This is only 3.5% of the loan amount of ₹581 crore. Thus, the balance sheet size is negligible as compared to the loan amount. During the oral hearing, EP submitted that RISL had created a charge on the assets in favour of RCL. Neither the liability towards RCL nor the assets represented by the loan to Reliance Communications appear in the audited balance sheet of the borrower. Yet a charge was created on its assets, and the balance confirmation was provided! Moreover, RCL convinced the Auditors by rationalising this fully illegal accounting treatment which flays the standards in this regard. No Standard of Accounting permits a loan taken from and given to separate legal entities to be ‘netted off’ in the balance sheet. Such a practice would lead to gross misstatements of accounts and any explanations and rationalisations for the same are indications of fraud risk factors as explained in SA 240. The replies of EP and the facts show the absence of due diligence and gross negligence. Despite the presence of a report under Section 143(12), these factors did not prompt EP to revise the risk assessment or perform additional procedures to rule out the existence of any material misstatements due to fraud or error, such as the authenticity of the confirmations or validity of the charges in all the cases. Thus, EP ignored the contradictory evidence and did not perform any further procedures to confirm the facts in accordance with the requirements of para 26 of SA 330 and failed to obtain sufficient appropriate audit evidence as required by SA 500 to support the audit opinion.

49. Thus, the charge of non-compliance with requirements of para 26 of SA 330 of analysing contradictory audit evidence stands proved.

C.5.3. Assessment of Risk of Material Misstatement (ROMM) due to Fraud

50. EP and PHD were charged with the failure to issue an audit opinion that was appropriate to the circumstances. EP failed to identify revenue recognition and management override of controls as fraud risk as per the requirements of Paragraphs 26 and 31 of SA 240. Though the EP identified loans as a significant risk in the WPs and also noted the procedures to be performed to address the same, they ignored the contradictory evidence while concluding that the financial statements are free from material misstatements, thus failed to comply with Paragraphs 26 and 27 of SA 330.

51. In response to the above EP submitted that he had applied all the required procedures during the audit to ascertain whether there was a management override of controls. EP submits that the WPs37 clearly state that revenue has been considered as a significant risk/fraud risk. Further, he states that irrespective of the risk the ET carried out an in-depth examination of records of the Company to comply with the SAs.

52. We find that there is no identification of fraud risk in revenue and management override of controls. There is no WP to identify or rebut risks of fraud in revenue or respond appropriately to risks of fraud in revenue and management override of controls. There is no compliance with Paragraph 32 of SA 240 such as proper testing of journal entries, reviewing accounting estimates for biases or evaluating whether the circumstances producing the bias. The substantive tests claimed to have been performed are limited to noting down the management submissions and records produced by the entity. Audit procedures responsive to a fraud risk are much more intensive than other procedures. The replies of EP show the disregard for the mandatory provisions of SA 240 and SA 330. Management may override controls to intentionally misstate the nature and timing of revenue or other transactions. Specific examination of fraud risk factors (incentive or pressure to commit fraud, a perceived opportunity to do so and some rationalization of the act) is absent. We have already discussed in the preceding pages, the rationalisation on the part of the management in the case of Reliance Integrated Services Private Limited (RISPL). Another instance of rationalisation is in the case of the sale of CCD above fair value, noted by both PW and PHD. RCL sold its investment in CCDs (face value ₹2160 crore, fair value of ₹1,333 crore) of Reliance Land Pvt Ltd at face value to Reliance Value Services Pvt Ltd, showing a gain of ₹827 crore. The transaction amount was then transferred by RCL through multiple layers in multiple tranches, on the same day, between several group companies under different contexts. EP stated that “Reliance Land Limited was in the process of getting its equity shares listed in the stock exchange. In view of the above, the investment by RCL in Reliance Land Limited had to be restructured by sale of CCD to another group company and the same was done at the face value. The matter was discussed with the management as well as the audit committee and was not considered as a transaction at unusual value”. This reply, which merely refers to the discussion with the management and the Audit Committee without detailing what was discussed and without disclosing why a prima facie unusual transaction (sale at 1.62 times the fair value and transfer in multiple tranches on the same day) was not considered so, indicates that the transaction was recorded in the books to window-dress the accounts of Reliance Land Limited by showing a higher value of its CCDs ahead of the listing of its shares. In this scheme of transactions, RCL booked a profit of ₹827 crore and gave more loans to already credit-impaired entities (Reliance Digitech Ltd and Reliance Venture Asset), who repaid their outstanding loans using this amount. Despite the underlying design of all these unusual transactions, defying accounting and financial rationale, the Auditors accepted the rationalisation given by RCL without necessary examination and verification.

53. As per para 32(c) of SA 240, the auditor is required to evaluate whether the business rationale (or the lack thereof) of unusually significant transactions suggests that they may have been entered into to engage in fraudulent financial reporting or to conceal misappropriation of assets. The sale of CCD at a value more than its fair value (1.62 times), and then the transfer of funds between multiple entities in multiple tranches on the same day was an unusual transaction. Despite this, the Auditors did not raise any queries or do any independent examination. Thus, the Auditors were grossly negligent and lacked professional skepticism.

54. In another instance, even though the Credit Appraisal Memo (CAM) of group companies was recorded in the Audit File, PHD failed to perform any audit procedures to obtain sufficient appropriate audit evidence to rule out management override of controls. In the CAM of Crest Logistics38, for instance, the loan was sanctioned for ₹511 crore at 11% interest, while an exposure of ₹1368 crore was already outstanding. It was also noted that the PAT for three FYs ending on 31st March 2013, 2014 and 2015 are negative, lowest loss being ₹702 crore. Interest was payable annually. The source of repayment was shown as “NA”. There was no explanation as to why the latest financial position of the Borrower was not recorded and how the borrower was expected to repay the interest and principal. There was no examination of the creditworthiness, such as ratings, end use of funds or projected cash flows. The CAM was signed by the CFO. In all cases of CAM the work of the ET was found to be limited to noting down the management’s data. There was no further examination of deviations from the credit policy, the process followed to sanction, disbursal etc. to ascertain management override of controls. There is an absence of the procedures prescribed in Paragraph 32 of SA 240 such as testing of journal entries and other adjustments throughout the period, retrospective review of management judgements, evaluation of their business rationale etc. The Auditors claim to have performed these but the same is not evidenced in the Audit File.

55. Thus, the charge of noncompliance with Paragraphs 26 and 31 of SA 240 and Paragraphs 26 and 27 of SA 330 regarding failure to identify and respond appropriately to ROMM due to fraud in management override of controls and revenue stands proved. This has resulted in the issue of an audit opinion without sufficient appropriate audit evidence. All the charges in paragraph 50 above thus stand proved.

56. Such lapses in the audit of revenue and the absence of professional skepticism are viewed seriously by audit regulators across the world. In the matter of Haynie & Company39, the US audit regulator PCAOB imposed sanctions on an auditor for failure to appropriately evaluate whether the revenue is reported in conformity with the applicable financial reporting framework. The sanctions included censuring the Firm, requiring the Firm to engage an independent consultant to review and make recommendations concerning its system of quality control and a civil money penalty of $400,000.

C.5.4. Verification of Expected Credit Loss (ECL) on Financial Assets in Compliance with Ind AS 109

57. EP and PHD were charged with failure to obtain sufficient appropriate audit evidence regarding the reasonability of the estimate of ECL and related disclosures in the financial statements. This has led to a failure to report material misstatements of under-provisioning and consequent overstatement of profits in the financial statements.

58. In response to this charge, EP submitted that the audit procedures performed were adequate as per SAs. He stated that the values of loans appearing in the financial statements at the year-end were compared with the valuation report provided by the independent valuer which is more than the values reported in the financial statements. This, in his opinion, ruled out the possibility of management bias, thus confirming the reliability of ECL.

59. This stand of EP shows an absence of professionalism and gaps in his knowledge of the matter. The factors determining ECL are detailed in Ind AS 10940. The asset-based approach to valuation (as is found in the valuation report) focuses on a company’s net asset value (NAV), or the fair market value of its total assets minus its total liabilities, to determine what would be the cost to recreate the business. There is no evidence that it captures the future income, the possibilities of loss, expected cashflows, or credit concerns of the business. ECL, on the other hand, estimates the expected credit losses that result from default events that are possible within 12 months (in a 12-month ECL scenario) or the expected credit losses that result from all possible default events over the expected life of the financial instrument (in a Lifetime ECL scenario). In this case, these two estimates (NAV and ECL) are not comparable to validate the ECL model. Moreover, in the valuation reports obtained41 the expert mentioned that the data/information was provided by the management and was used without any verification. Further, it also mentioned that the report should be used only for the estimation of the fair value of CCDs and should not be relied upon for any other purposes.

60. It was the responsibility of EP to test the ECL as per the requirements of the standard. However, there is no original work by EP other than noting down42 the ECL model of the Company and doing mathematical calculations. For instance, we note the following deficiencies in this regard.