Proposed Parameter For Issuing Equity Share And Other Security For UCB (Urban Co.Operative Bank) As Per Banking Regulation Act 2020 Recommendation By RBI Vishwanathan Committee.

(1) Banking Regulation Act Amendment

As per new Banking Regulation Act 2020 Section 56(i), the following clause shall be substituted, namely:-

Section 12 (1) A co-operative bank may, with the prior approval of the Reserve Bank, issue, by way of public issue or private placement,—

(i) equity shares or preference shares or special shares, on face value or at premium; and

(ii) unsecured debentures or bonds or other like securities with initial or original maturity of not less than ten years,

to any member of such co-operative bank or any other person residing within its area of operation, subject to such conditions and ceiling, limit or restriction on its issue or subscription or transfer, as may be specified by the Reserve Bank in this behalf.

Save as otherwise provided in this Act,—

(i) no person shall be entitled to demand payment towards surrender of shares issued to him by a co-operative bank; and

(ii) a co-operative bank shall not withdraw or reduce its share capital, except to the extent and subject to such conditions as the Reserve Bank may specify in this behalf.”;

(2) Background

Annual Policy Statement for the year 2006-07 to constitute a Working Group to examine the issue of share capital of UCBs and identify alternate instruments /avenues for augmenting the capital funds of UCBs. Accordingly, a Working Group was constituted under the Chairmanship of Shri N.S. Vishwanathan, Chief General Manager-in-Charge, Urban Banks Department, Reserve Bank of India.

First of all as a prudential measure, Reserve Bank has prescribed certain minimum share to borrowings ratio. The State Governments be requested to exempt the Urban Cooperative banks from the existing monetary ceiling on individual shareholding either through a notification or through amendment to the Act, where necessary.

UCBs may be permitted to issue unsecured, subordinated, non-convertible, redeemable debentures / bonds, which can be subscribed to by those within their area of operations and outside.

(3) Parameter for issuing bonds

These bonds could have the following features.

(i) The minimum maturity of the bonds should be 10 years. There need be no upper limit on maturity

(ii) The liability of the bank to the bond holders would be subordinated to the claims of depositors and other creditors but would rank senior to Shareholders, including holders of special shares, if any.

(iii) The bonds can have a fixed or floating interest rate. The interest rate can also be a combination of fixed and floating rates with the latter part being linked to factors like rate of dividend declared for ordinary shareholders etc.

(iv) The Bonds will not have any put option but can have a call option exercisable by the bank, not before five years, with prior permission of the Reserve Bank, which may be granted if it does not result in the regulatory capital falling below the prescribed level.

(v) The bonds will be ordinarily redeemed upon maturity. However, in the case of banks whose CRAR is below the prescribed minimum at the time of redemption, since the depositors have preferential claim over the bondholders, the redemption of the bonds would not be permitted, except against fresh issue of such bonds.

(vi) The bonds will be subjected to a progressive discount for capital adequacy purposes as under:

| Sr. No. | Remaining Maturity | Rate of discount |

| (a) | Less than one year | 100% |

| b) | More than one year and Less than two years | 80% |

| c) | More than two years and less than three years | 60% |

| d) | More than three years and less than four years | 40% |

| e) | More than four years and less than five years | 20% |

(vii) The bank cannot give loan against its own bonds.

(viii) The bank would normally be required to maintain CRR and SLR against the liabilities covered by the bonds. However, Reserve Bank may consider granting exemption from the reserve requirements.

(ix) The bonds may be transferable by endorsement and delivery.

(x) The bonds will be treated as Tier II capital, subject to the total

Tier-II capital not exceeding Tier I capital. However,

Where banks with negative net worth raise funds by way of such bonds through conversion of existing deposits, Reserve Bank may make an exception to this rule and treat these as part of regulatory capital even though Tier I capital is negative.

(4) Parameter for issuing Special Shares

UCBs may be allowed to issue special shares on specific terms and conditions. Banks can also be allowed to issue these shares at a premium, which could be approved by the respective RCS, in consultation with RBI.

The broad features of the special shares could be as under:

(i) Subscription to these shares will be on a non-voting basis.

(ii) They may be issued either at par or at a premium.

(iii) These shares may be issued in predetermined quantities over a specified period of time. They can as such be either wholly or partly underwritten.

(iv) They may be subscribed to by members, non-members including those outside the area of operations of the UCB concerned.

(v) They will be perpetual with a call option that can be exercised only after ten years, with prior permission of RBI, which may be granted in the event of the redemption not resulting in the CRAR falling below the prescribed minimum.

(vi) They will carry return by way of dividend, which shall not be less than the rate of dividend paid on ordinary shares, in terms of return on face value. However they shall be subject to a lock-in clause in terms of which the issuing bank shall not be liable to pay dividend, if

a) the bank’s CRAR is below the minimum regulatory requirement prescribed by Reserve Bank ; or

b) the impact of such payment results in CRAR falling below or remaining below the minimum regulatory requirement prescribed by Reserve Bank of India. However, banks may pay dividend with the prior approval of Reserve Bank when the impact of such payment may result in net loss or increase the net loss, provided the CRAR remains above the regulatory norm.

(vii) The amounts raised by way of special shares would be treated as Tier-I capital.

(viii) The bank cannot give loan against the shares issued by itself.

(ix) These shares may be transferred by endorsement and delivery.

(5) Parameter for issuing Cumulative Preference Shares

UCBs may be allowed to issue redeemable cumulative preference shares on specific terms and conditions with the prior permission of the respective RCS granted in consultation with RBI. The funds raised through such shares may be treated as Tier II capital.

The broad features of the preference shares are as under:

(i) Subscription to these shares will be on a non-voting basis.

(i) The minimum maturity of the preference shares should be 10 years. There need be no upper limit for maturity.

(ii) The dividend shall be fixed and can be cumulative.

(iii) The liability of the bank to the preference shareholders both for dividend and principal would rank senior only to the ordinary shareholders and holders of special share, if any.

(iv) The preference shares will not have any put option but can have a call option exercisable by the bank not before five years from the date of issue, with prior permission of the Reserve Bank which may be granted if, inter alia, it, does not result in the regulatory capital falling below the prescribed level.

(v) The preference shares will be ordinarily redeemed upon maturity. However, in the case of banks whose CRAR is below the prescribed CRAR at the time of redemption, since the depositors have preferential claim over the preference shareholders, the redemption would not be permitted, except against fresh issue of such shares.

(vi) The preference shares will be subjected to a progressive discount for capital adequacy purposes as under:

| Sr. No. | Remaining Maturity | Rate of discount |

| (a) | Less than one year | 100% |

| b) | More than one year and Less than two years | 80% |

| c) | More than two years and less than three years | 60% |

| d) | More than three years and less than four years | 40% |

| e) | More than four years and less than five years | 20% |

(vii) The bank cannot give loan against its own shares.

(viii) The bank should create a sinking fund @ 20% of the principal in the last five years to maturity.

(ix) The bank would be required to maintain CRR and SLR against the liabilities covered by the preference shares. However, Reserve Bank may consider granting exemption from the reserve requirements.

(x) The preference shares will be treated as Tier-II capital, subject to the total Tier-II capital not exceeding Tier-I capital. However,

Where banks with negative net worth raise funds by way of such shares through conversion of existing deposits, Reserve Bank may make an exception to this rule and treat these as part of regulatory capital even though Tier I capital is negative.

(6) Parameter for issuing Special Deposits

UCBs may be permitted to raise deposits of over 10 year maturity and such deposits can be considered as Tier II capital subject to their meeting certain conditions.

The features to be fulfilled by the long term deposits to be eligible for being treated as Tier II capital could be as under:

(i) Minimum maturity will be 15 years.

(ii) It will be subordinated to the claims of depositors and other creditors but would rank senior to shareholders, including holders of non-voting shares, if any and will be subject to RBI approval for repayment which will be given as long as banks assessed CRAR exceeds 9 per cent.

(iii) It should have floating rate of interest. Premature withdrawal will not be permitted. However, banks would have the option to repay anytime after 10 years with prior permission of RBI.

(iv) The deposits will not be eligible for DICGC cover

(v) The bank cannot give loan against these deposits.

(vi) The bank would be required to maintain CRR and SLR against the liabilities covered by the deposits. However, Reserve Bank may consider granting exemption maintaining the reserve requirements.

(vii) These deposits will be subjected to a progressive discount for capital adequacy purposes as proposed in paragraph 3.3.2 (vi).

(viii) These deposits will be treated as Tier-II capital, subject to the total Tier-II capital not exceeding Tier-I capital. However, the Group recommends that:

Where banks with negative net worth raise such long term deposits through conversion of existing deposits, Reserve Bank may make an exception to this rule and treat these as part of regulatory capital even though Tier I capital is negative.

(7) To dispense with the share linking norms

The regulatory provision requiring a certain percentage of borrowings to be contributed to share capital is intended to ensure a minimum capital for the

UCBs. This requirement was prescribed to ensure that capital was earmarked whenever a loan is disbursed so that the UCBs did not create risk assets disproportionate to their capital. However, now that UCBs are brought under the regime of linking capital adequacy in terms of a ratio to risk assets, prescribing a share to loan ratio on a borrower-to-borrower basis may not be necessary. The Group therefore recommends that:

The extant instructions on share linking to loans may be dispensed with.

(8) Federated Structure

The platform was akin to a stock exchange. It would require a regulator on the lines of SEBI, since it would not fall within the purview of SEBI Act.The Group opines that creating a federated structure on the lines of the one obtaining in Netherlands or in Finland may be faced with legal hurdles as also in bringing the UCBs under the fold of an umbrella of one organisation in view of the different cultural and social settings they are now working in. However, creating a legal framework for facilitating the emergence of such umbrella organisation(s) appears to be the only long term solution to enhance the public and depositors’ confidence in the sector. As this would not only require amendments to the Cooperative Societies Acts but also entails changes to the supervisory and regulatory practices, the Group recommends that:

The entire issue of creating an appropriate legislative and supervisory framework be separately examined taking into consideration the international experiences and systems.

(9) Trading Platform

The Group considered the suggestion of NAFCUB for having a separate trading platform for securities issued by UCBs. The Group noted that the suggestion was made by NAFCUB for providing a mechanism for transfer of instruments and liquidity to the investors. However, the Group has suggested a few instruments, which could be transferred through endorsement and delivery. It was of the view that the efficacy of having a separate trading platform for these securities could be examined, if and when, on the basis of experience gained from issue of such instruments by UCBs, a need is felt.

(10) Ability to absorb the loss occurring of takeover of weak banks.

At present there are not many UCBs with the financial strength required to take over other weak banks. The alternate instruments suggested would facilitate the emergence of a larger number of financially strong UCBs that would have the ability to absorb the losses occurring in the process of takeover of weak banks.

(11) Raising capital through issue of ‘non-voting’ shares by urban co-operative banks-concept of private exchange (D. Krishna, Chief Executive, NAFCUB)

(i) In order for urban co-operative banks to access larger number of investors without going to the capital market, a system that would bring together all the members of a group of urban co-operative banks to invest in any of, or in more than one urban bank has been drawn up in this presentation. This class of investors called “non-voting shareholders” will be different from existing “regular” and “nominal” members. While like “nominal” members, the “non-voting shareholders” will also not have the voting rights, the essential difference will be:

(a) they can be from outside the area of operation of banks; and

(b) each investor can own “non-voting shares” of more than one urban bank.

The salient feature of the scheme would that a bank in a small center with limited scope of making members from its area of operation can sell non-voting shares to a large number of investors that are members of other banks across the Country.

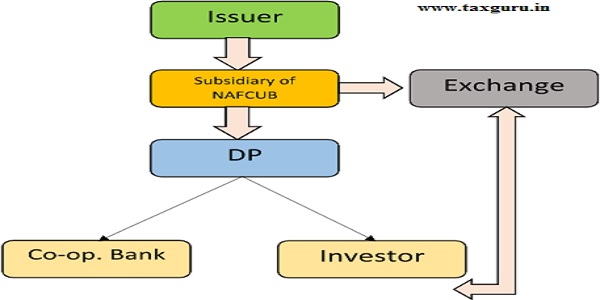

The Model We want to create a ‘private screen based exchange’ of their own wherein shares of Non-Voting types can be issued and traded amongst all members of participating cooperative banks.

To start with, we want to restrict the number of issuing banks. So, in the beginning only those banks having a deposit base of more than 100crore and falling in Grade I or Grade II bracket in Tier II category will be allowed to issue the instrument. Later the other banks can also join by issuing this instrument. All the members of the issuing banks will be allowed to participate in subscribing and trading. So, at an initial stage we can look at an approx. number of 500 Banks issuing shares. These 500 Banks have an approx. 5 million members. If we consider that even if 2% of the members subscribe to the shares issued then we would have an investor base of approx. 1 lakh.

(ii) Instrument

The instrument that we have proposed is a Non-Voting Preference Share.

This is with reference to the minutes of the last meeting, wherein we had found out that Maharashtra State Cooperative Act does not bar the issuance of Preference Shares by cooperative banks.

The features of the same are as follows:

> Non-Voting – The instrument holders would not get voting rights like equity shareholders

> Fixed Dividend – The instrument holders would be entitled to get a fixed dividend on the face value

> Cumulative – The dividend would be cumulative

> Tradable/Transferable – The instrument can be traded in the secondary market created for it.

(iii) Rules and Regulations

How much to issue?

> The banks would be allowed to issue a minimum of 20% of the Net Own Funds or Rs. 1 Crore, whichever is less.

> The maximum limit upto which banks can issue Non-Voting Shares will be 100% of their Net Owned Funds.

How much dividend should the cooperative bank pay?

> The dividend would be decided by the banks on an individual basis and the bank has an option to reset the dividend after every 3 years with cap and floor of the change being 200 basis points.

What are the Exit Options available to the investor?

> Secondary Market – the investor can sell his/her shares on the exchange created and get out of the market

> At the end of the 5th year of issue the investor will have a PUT Option, i.e. the investor will have an option to sell 20% of his holding to the issuing bank at the Market Price or the Face Value, whichever is lower

> At the end of the 8th year of issue the bank will have a CALL Option, i.e. the bank will have an option to buy 20% of the Preference Shares issued at the Market Price or the Face Value, whichever is higher

> Starting from the 8th year, every 3rd year there would be an alternate CALL/PUT Option having the above conditions

Why would the members subscribe to Non-Voting Preference Shares?

> The members would have a chance to invest in the shares of other cooperative banks

> The members holding these Non-Voting Preference Shares would get a fixed dividend every year

> There would be Capital Appreciation of the Non-Voting Preference Share Value.

To establish such a model a sound networking structure should also be in place. We have proposed a networking structure also for this model –

In the model we have tried to keep the Preference Shareholder at par with the equity shareholder and the depositor in terms of advantages and disadvantages.

Author Bio