The first in the series looked at the Need for Speed, and how the Code matches up to meet the tough timelines.

The second in the series i.e. this article looks at the big picture on the quality of the Insolvency Process, that the Code has set rolling, in terms of the quality of results. The initial setbacks did not result in the authorities attempting quick fix solutions to the bane of Indian economy, the unscrupulous promoters who have used every reform to their benefit, facilitated by some professional elements who flourish only on the basis of their skills to give a legal cover to the self promoting activities of the promoters.

As per the most recent balance sheet, i.e. March 2016, the paid up capital was 19.59 cr.

With expanded business, its capital structure got skewed with repeated borrowings. Eventually to bring some sanity in the highly leveraged balance sheet, the company leased its assets to a SPV, Synergies Casting Ltd in 2005.

Incorporated on 24th Jan 2005, with the ROC Hyderabad, its manufacturing too is based in Vishakapatnam, the Company is engaged in wheel casting business.

Two years after the lease agreement with Synergies Casting Ltd, Synergies-Dooray Automotive Ltd was declared a sick company in 2007. The way the system operated in India, it let a #Sick company function for ten years, which is a surprise in itself, as it continued to bleed, but could not exit. However, during this time period, there were various attempts at financial restructuring to bring the company back to normalcy.

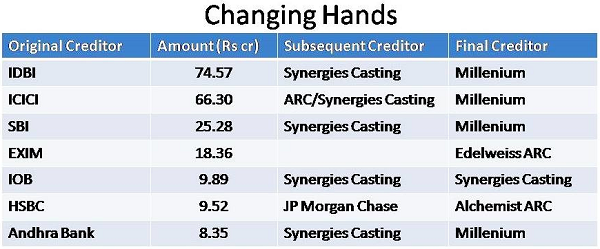

The lenders to the sick Company, assigned their debts, constituting over 90% of the outstanding debt on the balance sheet, to Synergies Casting. The corporate relationship between Synergies Dooray and Synergies Castings deepened, in an attempt to find synergies. It helped that there were synergies both at the board level and also in the business space that they operated. Eventually the original lenders moved out as two large Asset Reconstruction Companies, Alchemist ARC and Edelweiss ARC took over the papers.

In 2016, November 24th an NBFC, Millenium Finance, based at Panjagutta, Hyderabad and incorporated in Dec 1995, entered the picture. The debt that Synergies Casting had taken from Synergies Dooray was in turn assigned to Millenium Finance, not the entire book, but 92% of the book. Synergies Casting sold Rs 750 cr debt to the finance company at a deep discounted consideration of Rs 40 cr. In the process it must have booked a significant amount of capital loss.

As a matter of coincidence, two days after the transaction was completed, Government notified on November 26th, 2016, that #SICA would be repealed.

Soon after Millenium Finance had entered the picture, the Board of Synergies Dooray decided to file an application with the NCLT, Hyderabad bench u/s 10 of the Code. At that stage, the Company had Rs 972.15 cr debt outstanding on its balance sheet.

There were four creditors, Alchemist ARC held 12.56% of the debt, Edelweiss ARC held 8.94%, Synergies Casting still held 9.18% and Millenium Finance held 69.32% of the debt. None of the creditors approached the NCLT with an insolvency application, but the Corporate initiated an Insolvency Application with Ms Mamta Binani, based in Kolkatta, as Interim Resolution Professional.

The Hyderabad Bench vide its order dated 23rd Jan 2017, admitted the application.

That marked the beginning of the most controversial case in the newly implemented Reform, which also had another claim to fame, as the first case to commence insolvency proceedings and to be closed by the Adjudicating Authority as a successful Resolution.

“An Act to consolidate and amend the laws relating to reorganization and insolvency resolution of corporate persons, partnership firms, and individuals in a time bound manner for maximization of value of assets…”

The Committee of Creditors is another critical pillar in the Process of Insolvency, as the stakeholders pursue Resolution under the Code.

Sec 3(10) defines a creditor as “any person to whom a debt is owed and includes a financial creditor, an operational creditor, a secured creditor, an unsecured creditor, and a decree holder.”

It is the job of the Interim Resolution Professional to ensure that all the debts of the corporate are accounted for and treated fairly in the Insolvency Process. Towards this, and to ensure that all creditors are engaged in the Insolvency Process, the Code provides for certain communication tools to facilitate the IRP reaching out to the Creditors.

There is a public announcement made on the Board’s website and on the concerned corporate debtor’s website. Then the IRP sees to it that announcements are issued in the local newspapers. The announcement issued u/s 15 contains details like Name & Address of the Corporate Debtor, Last date for submission of claims, details of the IRP, the Closure date of the CIRP.

So for illustration, the insolvency application of Synergies Dooray Automotive Ltd was admitted by the Tribunal on 25th Jan 2017 and the last date for submission of claims was 8th Feb 2017, included the following:

“Notice is hereby given that the National Company Law Tribunal Hyderabad bench has ordered the commencement of a corporate insolvency resolution process against M/s Synergies – Dooray Automotive Ltd on 25-01-207.

From the date of her appointment, the IRP, controls the management of the Corporate Debtor. She collates all the information of the corporate regarding business operations, balance sheet transactions, and once the claims are received after the due date, she constitutes the Committee of Creditors.

This Committee is the decision making body in the Resolution Process. It is comprised of the creditors, with each constituent being entitled to voting share, which means the share of the voting rights of a single financial creditor in the committee of the creditors which is based on the proportion of the financial debt owed to such financial creditor in relation to the financial debt owed by the corporate debtor. By the 23rd day from the Insolvency Commencement date, the Committee has to be constituted and furthermore, the Committee has to have its first meeting within seven days of its constitution.

In the first meeting, the first agenda for the Committee is to confirm the appointment of the Interim Resolution Professional as the Resolution Professional. The Committee can as well decide to change the Professional by passing a resolution with two thirds, u/s27.

Regarding the authority of the Committee, the NCLT made several observations in the matter of Gupta Energy Pvt Ltd, went to the extent to state that the NCLT has neither jurisdiction to question the actions of the Committee nor any discretion to examine the resolution plan to dig into as to whether the resolution plan is better or the liquidation better. As per the Statute, the Committee is the competent authority and it cannot transgress into the jurisdiction of CoC.

That gives enormous powers to the Committee, and as such constitution of the Committee in itself is a key challenge to ensure that the right decision is taken in the interest of all the stake holders. There have been instances of both Type 1 and Type II errors being made in the constitution of the Committee.

There have been instances of some creditors being disqualified due to the related party clause, 5 (24)(j). This happened as there are cases of financial creditors taking up equity stake due to conversion of a portion of their debt into equity. Various Debt Restructuring schemes had been introduced by the RBI in the past such as SDR, S4A, which enabled financial creditors such as banks to convert part of their debt into equity in the borrower corporate. Such schemes were introduced in order to strengthen the lenders ability to deal with stressed assets.

So if such financial creditors happened to hold more than 20% of the equity, besides some debt, in the concerned corporate, then such FC became a related party u/s 5 (24)(j),

“a related party in relation to a corporate debtor, means, any person who controls more than twenty percent of voting rights in the corporate debtor on account of ownership or a voting agreement.”

This combined with Clause 21(2),

“The Committee of Creditors shall comprise all financial creditors of the corporate debtor, Provided that a related party to whom a corporate debtor owes a financial debt shall not have any right of representation, participation or voting in a meeting of the Committee of Creditors.”

Thus genuine financial creditors could be debarred from being part of the Committee of Creditors due to the combined effect of Sec 5 and Sec 21.

At the same time, the reverse is also true. A promoter in its attempts to control and influence the Committee of Creditors can work out ways to arraign the debt in such a manner that what was a related party, is reclassified as a genuine creditor. And the promoter is able to insert his people in the Committee.

So when, the new player Millenium #Finance entered into the picture, it took off chunk of the debt from the balance sheet of Synergies Casting onto its own balance sheet. Since Millenium Finance was NOT a related party, it was invited and became part of the Committee of Creditors with voting rights. Not just that, Millenium Finance got entitled to a voting share of 76.33% on the basis of its proportionate share of outstanding debt amongst the creditors eligible to be in the Committee.

However, in terms of actual work, it is the RP who has to collate all the details and compile the Information Memorandum within two weeks of her appointment. Post confirmation of the CoC, the Information Memo is shared to seek Resolution Applicants.

On the basis of the details available in the Information Memorandum, the short listed Resolution Applicants submit Resolution Plans which is put for the consideration of the Committee of Creditors. The Committee of Creditors is expected to evaluate these alternate Resolution Plans and select the optimum plan. It is absolutely in the discretion of the Committee to decide what is most suitable for the Corporate Debtor.

In the case of Synergies – Dooray, three entities submitted Resolution Plans, out of which two (submitted by SMB Ashes Industries and Suiyas Industries Pvt Ltd) Plans were rejected by the Committee with reasons duly minuted and the third was accepted subject to certain modifications, all of which was duly minuted. The Resolution Plan that was accepted was submitted by Synergies Casting.

The Committee of the #Creditors met only twice in the entire Insolvency process of Synergies Dooray; first on 22nd Feb 2017, when it had appointed Ms Mamta Binani as the Resolution Professional, and thereafter on 24th Jun 2017 when it approved the #Resolution Plan submitted by Synergies Casting.

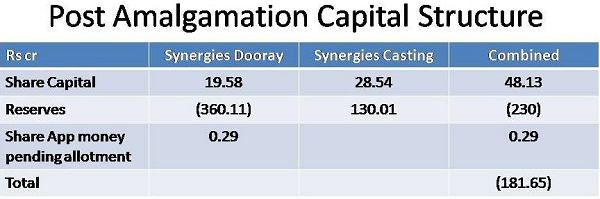

The Resolution Plan so approved envisaged business continuity of the corporate debtor, through Financial #Restructuring, Operational Restructuring, #Capital Restructuring, Payment to Operational Creditors and Statutory Dues, Infusion of fresh funds by the promoters, Payment of Insolvency process costs including the fees of the Resolution Professional. Synergies Dooray Automative Ltd, the corporate debtor was to be amalgamated into its subsidiary, Synergies Castings Ltd, based on the Resolution Plan approved by the Committee.

The merged entity was accorded a series of concessions,

a. The State Government of AP exempted the merged entity from levy of Stamp Duty on the value of assets transferred.

b. Sales Tax Dept accepted the repayment of outstanding amounts in equated annual installments, without any penal interests.

c. Synergies Casting was exempted from the provisions of Sec 79 and entitled to carry forward losses and unabsorbed depreciation as per Sec 72 A of IT Act.

This was the first case the Tribunal had decided upon. The other creditor Edelweiss ARC, who is to get 4.89 crore in three annual installments against its debt book of 86.92 cr, approached the NCLAT against the Tribunal decision without any success.

The fees of Ms Mamta Binani, of Rs 50 lacs was to be paid first in the Waterfall. The remaining cost of the Resolution worked out to be Rs 54 cr to be paid out in three interest free annual instalments. On the total debt of Rs 972 crore, it amounted to a haircut of 94.37%.

Barring the one case of Nandan Hotels, where the claim amount computation is not available, for the balance 21 of the 22 cases where Resolution has been achieved, the average haircut was at 50.40%, amounting to Rs 5,004 crore as detailed along.

Of the total amount of 5,004 in haircut, almost 917 cr is accounted by the case of Synergies. Another 908 cr is accounted for by Kamineni Steel & Power where the haircut was 60%.

Synergies was the first case, and the most controversial. The whole matter had moved through the Resolution journey in a smooth, timely and legal manner, completed in 191 days. It still is the most controversial of all resolutions in the newly formed Insolvency Reform, with an alltime high haircut of 94%.

A year after the Code had come into effect, on 16th Nov 2017, the Insolvency Law Committee was constituted, with the mandate, “to take stock of the functioning and implementation of the Code, identify the issues that may impact the efficiency of the CIRP, and liquidation framework prescribed under the Code, and make suitable recommendations to address such issues, enhance efficiency of processes prescribed and for effective implementation of the Code.”

The Committee comprised of fourteen legal and official luminaries and went into the details. The abnormally high haircut suffered in the case of Synergies was brought to its notice.

It was suggested to the Committee that creditors who have acquired #debt by any assignment of debt within a year prior to commencement of insolvency should be excluded from the CoC.

However, the Committee felt that given the limited experience of interpretation of provisions of the Code by practitioners as well as adjudicating authorities, the protection in section 21(2) whereby any related party to whom the corporate debtor owes a financial debt is excluded from the CoC is sufficient to ensure that the CoC is not sabotaged by the promoters and other related parties of the corporate debtor.

Furthermore the other side of the argument is equally strong, when there is a genuine transaction, and a creditor has in a scrupulous transaction acquired a debt paper, but would be denied the Committee vote simply because the issuer had gone into CIRP within a year of the transaction.

In the specific case the loan book had changed hands multiple times, some of which is detailed alongwith

The other deduction that came from the case; for the purpose determining the voting share in the Committee, the value of the debt should be taken as the amount paid by the buyer of the debt book, rather than the value of the debt in the #Corporate Debtors books. It would have meant that Millenium Finance would have got voting share corresponding to Rs 40 cr, that it had paid to acquire the debt portfolio from Synergies Casting, and not voting share corresponding 792 cr which was the value of the debt in the Corporate Debtors books.

This too has implications on either side. Besides being a commercial contract problem, or a legal problem, it is a philosophical problem.

To fix one loose end so as to prevent the bad promoter from taking advantage of the #Reform, it could prevent genuine transactions in the debt markets. Eventually it would boil down to whether there is one bad promoter affecting the reform process for hundreds of good promoters, or vice versa. If cynicism is to be the guiding principle, and assume the worst, that most of the promoters are out there to hijack the Reform process, than anyway there is not much to talk about any #Reform.

However neither are the authorities completely idealistic. The Insolvency #Law Committee did make couple of relevant recommendations on the basis of the learnings from the specific case.

In particular the provision pertaining to related party required to be amended, so that “financial creditors that are regulated by a financial sector regulator and have become a related party of the corporate debtor solely on account of conversion or substitution of debt into equity shares or instruments convertible into equity shares of the corporate debtor, prior to the insolvency commencement date.”

The role of the Committee of Creditors was put under the microscope in subsequent developments like, in the case of Indian Bank Vs Kadevi Industries Ltd, the NCLT, did not hesitate to question the authority of the Committee of Creditors. While passing the Order of Liquidation on 9th Jan 2018, about five months after the Synergies Dooray Resolution was approved, the NCLT observed,

“…this implies that all the parties involved in the entire #CIRP process are hand in glove and made untruthful / wilful false submissions to the Adjudicating Authority. Therefore, the Adjudicating Authority has taken issue seriously and imposes a cost of Rs. 1,00,000/- (Rs. One Lakh only) each on the Financial Creditors/CoC and on the corporate debtor.”

Although the decision in the matter of Gupta Energy, quoted earlier, came after the matter of Kadevi Industries, the #NCLT has sought to draw a thick line between procedural niceties and the spirit of the Code.

As it turned out, the magnitude of the Haircut itself got cut down as the Insolvency Process gained experience and matured. Since then no case has crossed the 74% mark, and the average haircut has slid down to 50%.

As the process gains more experience, the Process Outputs, both in terms of Time Taken To Resolution and the Haircut for Resolution is expected to improve significantly.

The put in the words of the Insolvency Law Committee that maturely responded to the case, “presently the protection provided in the provision (Section 21(2)) is sufficient to ensure that decisions of the Committee are not influenced by the corporate debtor. It was discussed that should concrete evidence of the lack of improvement in the recovery rate in India emerge even after implementation of the Code for a reasonable time period, amendments to the Code may be considered at such future date.”

This is particularly dependent on the Kingpin of the process, the #Insolvency #Professional.

We explore the Insolvency Professional in detail in Part C, of this series on the Code, who can make or break the Code.

Author Bio